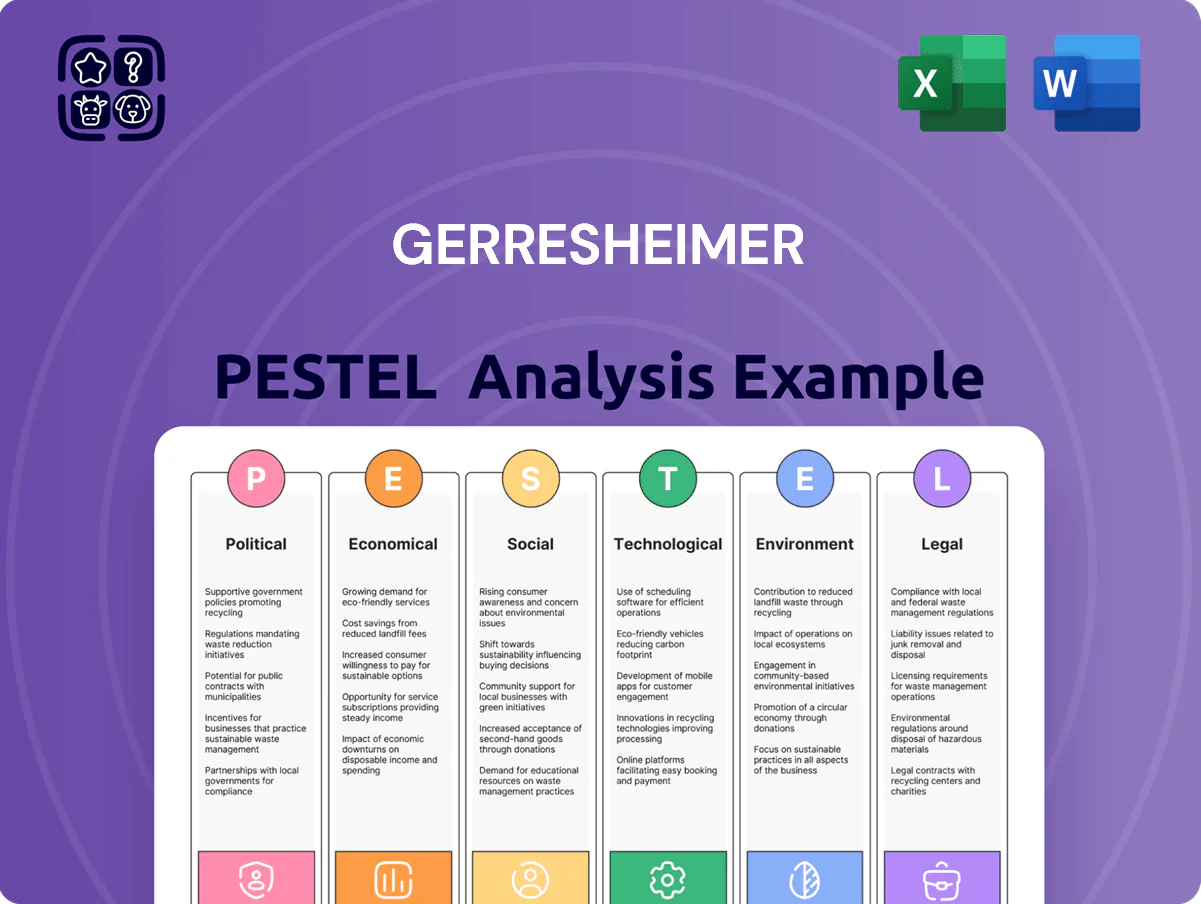

Gerresheimer PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, regulatory pressures, and ESG trends are reshaping Gerresheimer’s growth trajectory—our concise PESTLE snapshot highlights key external risks and opportunities to inform smarter strategies. Purchase the full PESTLE analysis for a comprehensive, fully editable report with actionable insights tailored for investors, consultants, and executives.

Political factors

Geopolitical trade dynamics and regionalization

Regionalization forces Gerresheimer to balance production across Europe, Asia and the Americas; in 2024 roughly 48% of sales were Europe, 30% Americas, 22% Asia, so footprint shifts affect capacity planning.

Rising trade tensions risk tariffs on medical glass/plastics; a 5% tariff on €1bn of components would raise input costs by €50m, pressuring margins and pricing strategies.

Management is expanding local-for-local sites—Gerresheimer planned €120m capex for 2024–25—to reduce cross-border disruption risk and secure pharma supply chains.

Impact of the US Inflation Reduction Act

The US Inflation Reduction Act’s drug price negotiation drives pharma to shift R&D toward high-margin biologics; 2024 CMS projections estimate savings of $100–200bn over a decade, pressuring manufacturers to protect margins and favor premium delivery systems.

Gerresheimer faces demand tilt toward high-end syringes and auto-injectors as customers deprioritize low-margin generics; the injectable device market for biologics grew ~6.8% YOY to $22.5bn in 2024, benefiting specialized glass and polymer components.

To capture profitable segments, Gerresheimer must align portfolio and capacity with therapeutic areas insulated from price cuts—oncology and specialty biologics accounted for ~45% of global biologics spend in 2024—and focus investments in advanced prefilled systems and regulatory support.

European Union pharmaceutical legislation updates

Geopolitical stability in emerging production hubs

Gerresheimer's large manufacturing footprint in India and China—accounting for roughly 30% of 2024 group production capacity—makes geopolitical stability vital to maintain uninterrupted supply chains and GMP-compliant output.

Regulatory shifts, such as tighter foreign investment rules or export controls, could impede exports or profit repatriation, impacting the 2024–25 cash flow and ROIC targets.

Continuous monitoring of local politics enables proactive risk mitigation for capital allocation and protects ~€300–500m planned regional investments through 2025.

- High exposure: ~30% capacity in India/China

- Financial risk: €300–500m regional investments through 2025

- Key risk: export controls, FDI rule changes

- Mitigation: active local political monitoring

Governmental support for biotech innovation

Post-2020 stimulus and vaccine industrialization programs have seen >$150bn in national incentives globally by 2024, boosting demand for primary packaging; Gerresheimer, with 2024 sales of €1.5bn and ~30% pharma-related revenue, captures stronger order flow for vials and prefillable syringes.

Alignment with government-funded healthcare contracts—seen in EU and US grants totalling €12–€20bn for manufacturing capacity in 2023–25—provides Gerresheimer predictable multi-year demand and supports margin stability.

- Increased govt subsidies (> $150bn global) drive packaging demand

- Gerresheimer 2024 sales ~€1.5bn, ~30% pharma exposure

- EU/US grants €12–€20bn 2023–25 enable multi-year contracts

Gerresheimer ramps €120m capex to localize capacity as pharma policy fuels device boom

Political risks (trade barriers, FDI/export controls) and regional policy shifts force Gerresheimer to localize capacity—48% sales Europe/30% Americas/22% Asia (2024)—and invest €120m capex (2024–25) to protect €300–500m regional investments; US IRA and EU pharma reforms favor biologics/biosimilars, boosting high-end device demand (injectable devices market $22.5bn in 2024, +6.8% YOY).

| Metric | 2024/2025 Data |

|---|---|

| Sales split | Europe 48% / Americas 30% / Asia 22% |

| Group sales | €1.5bn (2024) |

| Capex | €120m (2024–25) |

| Regional investments at risk | €300–500m |

| Injectable device market | $22.5bn (+6.8% YOY) |

| Govt incentives | >$150bn global; EU/US grants €12–20bn (2023–25) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Gerresheimer across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends, regional regulatory context, and forward-looking insights to support executives, consultants, and investors in identifying risks, opportunities, and strategy-ready recommendations.

A concise, visually segmented PESTLE summary for Gerresheimer that clarifies external risks and opportunities at a glance, ready to drop into presentations or share across teams to streamline strategic planning and client reports.

Economic factors

Energy price volatility in glass manufacturing

The production of molded and tubular glass is highly energy-intensive, making Gerresheimer sensitive to natural gas and electricity prices; energy represents roughly 20–25% of variable production costs in glass operations as of 2024. By late 2025 energy market stabilization saw benchmark European gas TTF volatility drop to ~18% from peaks >60% in 2022–23, improving margin predictability. Gerresheimer continues hedging programs covering ~70% of near-term consumption and investing in efficiency projects expected to cut site energy intensity by 10–15% through 2026 to mitigate future shocks.

Growth of the GLP-1 weight loss market

The massive surge in demand for GLP-1 obesity and diabetes treatments—global prescriptions for 2024 grew ~85% year-over-year to an estimated 12 million treatment courses—has become a primary economic driver for drug delivery device makers. Gerresheimer has expanded autoinjector and pen capacity, investing roughly €120 million in 2023–2025 to scale production and target >20% revenue exposure to GLP-1 devices by 2025. This market tailwind offers a strong buffer against cyclical downturns in other end markets, supporting more stable top-line growth and improving capacity utilization.

Inflationary pressures on labor and raw materials

Persistent inflation in labor and raw materials—global input costs up ~8–10% YoY in pharma packaging in 2024—forces Gerresheimer to deploy disciplined pricing and productivity measures; pass-through clauses in long-term contracts mitigate but cannot absorb full inflation given customer sensitivity. The company targets lean manufacturing and automation investments—capex rose to €85m in 2024—to protect EBITDA margin, which held near 12% despite cost pressures.

Interest rate environments and capital expenditure

Higher interest rates versus the prior decade raise Gerresheimer’s financing costs for global expansion, increasing weighted average cost of capital above its historical ~6–7% range; 2024 ECB and Fed policy rates averaging 3.5–5% lifted borrowing spreads for corporates.

Gerresheimer must manage debt mix and free cash flow to fund plants in North Carolina and Europe, where capex guidance was about €200–250m for 2024–25.

A stable or easing rate path into late 2025 would reduce the company’s hurdle rate, improving NPV on future projects and lowering interest expense if refinancing at lower yields occurs.

- Higher rates → higher WACC (historical ~6–7% baseline)

- Capex plan ~€200–250m for 2024–25

- Debt/cash management critical for US and EU plants

- Rate decline in late 2025 would cut financing costs and raise project viability

Currency exchange rate fluctuations

As a Euro-reported global supplier, Gerresheimer faces transaction and translation risks from USD and other currency revenues; in 2024 roughly 30–40% of sales were dollar-linked, making EUR/USD swings materially affect reported EPS and export competitiveness.

The company uses derivatives and forward contracts—hedging about 60–80% of short-term exposures in recent years—to stabilize cash flow and deliver clearer guidance to investors.

- ~30–40% revenue USD-exposed (2024)

- Hedges cover ~60–80% short-term FX exposure

- EUR/USD volatility directly affects EPS and export pricing

Energy-heavy glass maker pivots to GLP‑1 growth, cuts intensity, manages FX & input pressures

Energy costs ~20–25% of glass variable costs (2024); hedges cover ~70% near-term; energy-efficiency projects target −10–15% intensity by 2026. GLP‑1 demand drove ~€120m capex (2023–25) aiming >20% revenue exposure by 2025. Input inflation ~8–10% (2024) pressured margins; EBITDA ~12% (2024). Capex guide €200–250m (2024–25); USD exposure ~30–40% of sales; FX hedges 60–80%.

| Metric | 2024/2025 |

|---|---|

| Energy share | 20–25% |

| Energy hedged | ~70% |

| GLP‑1 capex | €120m |

| Revenue GLP‑1 target | >20% |

| Input inflation | 8–10% |

| EBITDA margin | ~12% |

| Capex guidance | €200–250m |

| USD exposure | 30–40% |

| FX hedges | 60–80% |

Preview the Actual Deliverable

Gerresheimer PESTLE Analysis

The preview shown here is the exact Gerresheimer PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Everything displayed in this preview—content, layout, and analysis—is part of the final file you’ll download immediately after payment.

No placeholders or teasers: this is the real, finished PESTLE report you’ll own and can apply directly to strategic or investment decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, regulatory pressures, and ESG trends are reshaping Gerresheimer’s growth trajectory—our concise PESTLE snapshot highlights key external risks and opportunities to inform smarter strategies. Purchase the full PESTLE analysis for a comprehensive, fully editable report with actionable insights tailored for investors, consultants, and executives.

Political factors

Geopolitical trade dynamics and regionalization

Regionalization forces Gerresheimer to balance production across Europe, Asia and the Americas; in 2024 roughly 48% of sales were Europe, 30% Americas, 22% Asia, so footprint shifts affect capacity planning.

Rising trade tensions risk tariffs on medical glass/plastics; a 5% tariff on €1bn of components would raise input costs by €50m, pressuring margins and pricing strategies.

Management is expanding local-for-local sites—Gerresheimer planned €120m capex for 2024–25—to reduce cross-border disruption risk and secure pharma supply chains.

Impact of the US Inflation Reduction Act

The US Inflation Reduction Act’s drug price negotiation drives pharma to shift R&D toward high-margin biologics; 2024 CMS projections estimate savings of $100–200bn over a decade, pressuring manufacturers to protect margins and favor premium delivery systems.

Gerresheimer faces demand tilt toward high-end syringes and auto-injectors as customers deprioritize low-margin generics; the injectable device market for biologics grew ~6.8% YOY to $22.5bn in 2024, benefiting specialized glass and polymer components.

To capture profitable segments, Gerresheimer must align portfolio and capacity with therapeutic areas insulated from price cuts—oncology and specialty biologics accounted for ~45% of global biologics spend in 2024—and focus investments in advanced prefilled systems and regulatory support.

European Union pharmaceutical legislation updates

Geopolitical stability in emerging production hubs

Gerresheimer's large manufacturing footprint in India and China—accounting for roughly 30% of 2024 group production capacity—makes geopolitical stability vital to maintain uninterrupted supply chains and GMP-compliant output.

Regulatory shifts, such as tighter foreign investment rules or export controls, could impede exports or profit repatriation, impacting the 2024–25 cash flow and ROIC targets.

Continuous monitoring of local politics enables proactive risk mitigation for capital allocation and protects ~€300–500m planned regional investments through 2025.

- High exposure: ~30% capacity in India/China

- Financial risk: €300–500m regional investments through 2025

- Key risk: export controls, FDI rule changes

- Mitigation: active local political monitoring

Governmental support for biotech innovation

Post-2020 stimulus and vaccine industrialization programs have seen >$150bn in national incentives globally by 2024, boosting demand for primary packaging; Gerresheimer, with 2024 sales of €1.5bn and ~30% pharma-related revenue, captures stronger order flow for vials and prefillable syringes.

Alignment with government-funded healthcare contracts—seen in EU and US grants totalling €12–€20bn for manufacturing capacity in 2023–25—provides Gerresheimer predictable multi-year demand and supports margin stability.

- Increased govt subsidies (> $150bn global) drive packaging demand

- Gerresheimer 2024 sales ~€1.5bn, ~30% pharma exposure

- EU/US grants €12–€20bn 2023–25 enable multi-year contracts

Gerresheimer ramps €120m capex to localize capacity as pharma policy fuels device boom

Political risks (trade barriers, FDI/export controls) and regional policy shifts force Gerresheimer to localize capacity—48% sales Europe/30% Americas/22% Asia (2024)—and invest €120m capex (2024–25) to protect €300–500m regional investments; US IRA and EU pharma reforms favor biologics/biosimilars, boosting high-end device demand (injectable devices market $22.5bn in 2024, +6.8% YOY).

| Metric | 2024/2025 Data |

|---|---|

| Sales split | Europe 48% / Americas 30% / Asia 22% |

| Group sales | €1.5bn (2024) |

| Capex | €120m (2024–25) |

| Regional investments at risk | €300–500m |

| Injectable device market | $22.5bn (+6.8% YOY) |

| Govt incentives | >$150bn global; EU/US grants €12–20bn (2023–25) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Gerresheimer across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends, regional regulatory context, and forward-looking insights to support executives, consultants, and investors in identifying risks, opportunities, and strategy-ready recommendations.

A concise, visually segmented PESTLE summary for Gerresheimer that clarifies external risks and opportunities at a glance, ready to drop into presentations or share across teams to streamline strategic planning and client reports.

Economic factors

Energy price volatility in glass manufacturing

The production of molded and tubular glass is highly energy-intensive, making Gerresheimer sensitive to natural gas and electricity prices; energy represents roughly 20–25% of variable production costs in glass operations as of 2024. By late 2025 energy market stabilization saw benchmark European gas TTF volatility drop to ~18% from peaks >60% in 2022–23, improving margin predictability. Gerresheimer continues hedging programs covering ~70% of near-term consumption and investing in efficiency projects expected to cut site energy intensity by 10–15% through 2026 to mitigate future shocks.

Growth of the GLP-1 weight loss market

The massive surge in demand for GLP-1 obesity and diabetes treatments—global prescriptions for 2024 grew ~85% year-over-year to an estimated 12 million treatment courses—has become a primary economic driver for drug delivery device makers. Gerresheimer has expanded autoinjector and pen capacity, investing roughly €120 million in 2023–2025 to scale production and target >20% revenue exposure to GLP-1 devices by 2025. This market tailwind offers a strong buffer against cyclical downturns in other end markets, supporting more stable top-line growth and improving capacity utilization.

Inflationary pressures on labor and raw materials

Persistent inflation in labor and raw materials—global input costs up ~8–10% YoY in pharma packaging in 2024—forces Gerresheimer to deploy disciplined pricing and productivity measures; pass-through clauses in long-term contracts mitigate but cannot absorb full inflation given customer sensitivity. The company targets lean manufacturing and automation investments—capex rose to €85m in 2024—to protect EBITDA margin, which held near 12% despite cost pressures.

Interest rate environments and capital expenditure

Higher interest rates versus the prior decade raise Gerresheimer’s financing costs for global expansion, increasing weighted average cost of capital above its historical ~6–7% range; 2024 ECB and Fed policy rates averaging 3.5–5% lifted borrowing spreads for corporates.

Gerresheimer must manage debt mix and free cash flow to fund plants in North Carolina and Europe, where capex guidance was about €200–250m for 2024–25.

A stable or easing rate path into late 2025 would reduce the company’s hurdle rate, improving NPV on future projects and lowering interest expense if refinancing at lower yields occurs.

- Higher rates → higher WACC (historical ~6–7% baseline)

- Capex plan ~€200–250m for 2024–25

- Debt/cash management critical for US and EU plants

- Rate decline in late 2025 would cut financing costs and raise project viability

Currency exchange rate fluctuations

As a Euro-reported global supplier, Gerresheimer faces transaction and translation risks from USD and other currency revenues; in 2024 roughly 30–40% of sales were dollar-linked, making EUR/USD swings materially affect reported EPS and export competitiveness.

The company uses derivatives and forward contracts—hedging about 60–80% of short-term exposures in recent years—to stabilize cash flow and deliver clearer guidance to investors.

- ~30–40% revenue USD-exposed (2024)

- Hedges cover ~60–80% short-term FX exposure

- EUR/USD volatility directly affects EPS and export pricing

Energy-heavy glass maker pivots to GLP‑1 growth, cuts intensity, manages FX & input pressures

Energy costs ~20–25% of glass variable costs (2024); hedges cover ~70% near-term; energy-efficiency projects target −10–15% intensity by 2026. GLP‑1 demand drove ~€120m capex (2023–25) aiming >20% revenue exposure by 2025. Input inflation ~8–10% (2024) pressured margins; EBITDA ~12% (2024). Capex guide €200–250m (2024–25); USD exposure ~30–40% of sales; FX hedges 60–80%.

| Metric | 2024/2025 |

|---|---|

| Energy share | 20–25% |

| Energy hedged | ~70% |

| GLP‑1 capex | €120m |

| Revenue GLP‑1 target | >20% |

| Input inflation | 8–10% |

| EBITDA margin | ~12% |

| Capex guidance | €200–250m |

| USD exposure | 30–40% |

| FX hedges | 60–80% |

Preview the Actual Deliverable

Gerresheimer PESTLE Analysis

The preview shown here is the exact Gerresheimer PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Everything displayed in this preview—content, layout, and analysis—is part of the final file you’ll download immediately after payment.

No placeholders or teasers: this is the real, finished PESTLE report you’ll own and can apply directly to strategic or investment decisions.