Getlink PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and technological advances are reshaping Getlink's strategic landscape—our concise PESTLE highlights key external risks and opportunities you need to know; purchase the full analysis for a complete, actionable report ready for investor decks, strategy sessions, or competitive benchmarking.

Political factors

Post-Brexit Regulatory Stability

As of late 2025 the UK-EU relationship has stabilized into a structured framework that reduced border friction for Getlink, with cross-border delays at the Eurotunnel reported down 18% year-on-year and average customs clearance time cut to 22 minutes.

Ongoing bilateral agreements on customs and security protocols—covering 95% of freight movements—are essential to maintaining daily throughput near pre-Brexit capacity of ~17,000 trucks and 10,000 passengers.

Investors watch diplomatic ties closely: a 2025 scenario analysis by Getlink shows a 6–9% swing in EBITDA under higher-friction outcomes, directly linking political stability to terminal operational efficiency.

Energy Sovereignty and ElecLink

Government prioritization of energy security in France and the UK has raised ElecLink’s strategic value; the 1 GW HVDC link can transfer ~7.9 TWh/year, roughly 1.5% of UK annual demand (2024: ~520 TWh) and strengthens grid resilience.

Political backing for cross-border sharing reduces volatility risk and supports market integration, enhancing Getlink’s position amid EU–UK interconnector policies and 2025 capacity market reforms.

This alignment with national energy targets underpins long-term viability for Getlink’s diversification, with ElecLink contributing recurring regulated revenue and capex visibility into the late 2020s.

Geopolitical Security Measures

The Channel Tunnel, handling about 21 million passengers and 1.6 million freight units in 2023, is critical national infrastructure requiring constant coordination with state security agencies to deter unauthorized crossings and terrorism.

Since 2018 policy shifts on migration have driven Getlink to invest roughly €120–€180 million in enhanced surveillance, fencing and detection tech through 2025, reflecting rising capex needs tied to border security mandates.

Getlink must comply with state-mandated security measures while optimizing operations to avoid adding delay to services that delivered €1.1 billion revenue in 2024, balancing safety and transit speed.

Intergovernmental Commission Oversight

The Intergovernmental Commission (IGC) retains strong regulatory control over Channel Tunnel safety and economics, overseeing inspections and approving cross-Channel rolling stock; in 2024 the IGC conducted 18 major audits and approved 3 new vehicle types affecting Getlink fleet planning.

Political appointments to the IGC can shift audit frequency and approval timelines, with delays potentially impacting Getlink capex and revenue—Getlink reported €1.1bn capex guidance in 2024 that depends partly on timely IGC clearances.

Maintaining collaborative relations with the IGC reduces bureaucratic delays and supports smoother implementation of operational changes, critical as freight volumes rose 4.2% in 2024 versus 2023.

- IGC ran 18 major audits in 2024

- 3 new rolling stock approvals in 2024

- Getlink 2024 capex guidance ~€1.1bn

- Freight volumes +4.2% in 2024

Trade Policy and Freight Volume

Fluctuations in UK-EU trade deals materially affect Le Shuttle Freight volumes; post-Brexit customs changes cut truck crossings by about 10% in 2021, while 2023 recovery lifted freight throughput toward pre-2020 levels with Getlink reporting freight revenue of €387m in 2023, up 6% year-on-year.

Political shifts toward protectionism or new free-trade arrangements can reduce or boost demand for cross-channel logistics, making Getlink revenue highly sensitive to macro-political shifts that govern cross-border goods movement.

- 2023 freight revenue €387m (Getlink)

- Post-Brexit truck crossings down ~10% in 2021, recovering by 2023

- Trade policy volatility directly tied to demand for Le Shuttle Freight

Getlink: UK–EU stability key as border delays fall, capex high and EBITDA risk rises

Political stability in UK–EU relations and IGC oversight are crucial for Getlink: border delays down 18% (2025), customs clearance 22 minutes, freight +4.2% (2024), 2024 capex ~€1.1bn; ElecLink transfers ~7.9 TWh/year supporting energy targets; security-driven capex €120–180m (2018–2025) and freight revenue €387m (2023) link political outcomes to EBITDA volatility of 6–9% in stress scenarios.

| Metric | Value |

|---|---|

| Border delays change (2025) | -18% |

| Customs clearance | 22 min |

| Freight vol. change (2024) | +4.2% |

| Capex guidance (2024) | ~€1.1bn |

| Freight revenue (2023) | €387m |

What is included in the product

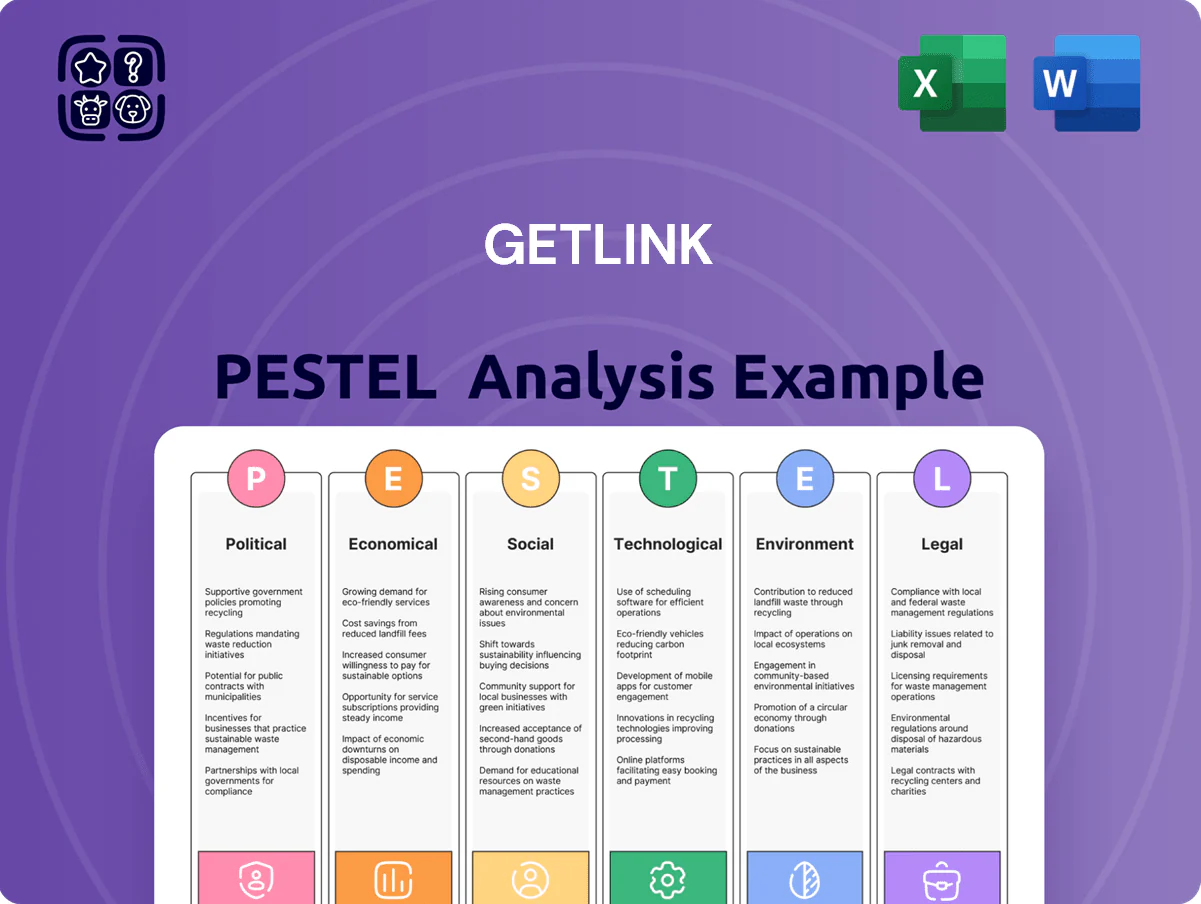

Explores how external macro-environmental factors uniquely affect Getlink across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives and investors.

Condenses Getlink's full PESTLE into a concise, shareable summary that’s visually segmented by category for quick interpretation and easy inclusion in presentations or planning sessions.

Economic factors

Inflationary Pressure on Operating Costs

By end-2025, persistent Eurozone and UK inflation raised labor costs ~8–10% YoY and pushed electricity prices for rail operations up ~20% vs 2022, squeezing Getlink margins despite index-linked contracts that pass portions of costs to customers; extreme energy spikes in 2022–24 still left residual exposure, requiring delicate pricing vs competitiveness decisions as operating overheads rose materially.

Currency Exchange Rate Volatility

Getlink operates in GBP and EUR, exposing it to GBP/EUR volatility; a 5% move in 2023–2024 would change reported revenue by roughly €20–30m given 2024 revenue ~€1.1bn. Such swings affect cross-border leisure travel demand—sterling weakness vs euro makes Channel crossings pricier for UK tourists. Getlink uses hedging (forwards/options) to smooth short-term FX P&L, but sustained trends in GBP/EUR continue to pressure long-term margins.

Consumer Discretionary Spending Trends

The demand for Le Shuttle and Eurostar is closely tied to Western European disposable income; Euro area real disposable income fell 1.2% in 2023 after inflation, pressuring leisure travel and reducing passenger vehicle volumes for Getlink.

High interest rates in 2024—ECB policy rate averaging ~3.75%—kept borrowing costly, further dampening discretionary trips and lower-margin car volumes.

By contrast, a strong 2024 tourism rebound saw international arrivals to France and the UK rise ~8–10%, boosting high-margin passenger traffic that materially supports Getlink’s EBITDA.

Electricity Market Integration

ElecLink revenue hinges on France-UK price spreads; 2024 average day-ahead spread was about €6–€12/MWh, but peaks exceeded €50/MWh during tight supply, driving volatile earnings.

National energy mixes and industrial demand shape these differentials—France’s nuclear output (≈63% 2023) vs UK gas/renewables mix increases arbitrage potential for Getlink.

Capitalizing on arbitrage via ElecLink supports Getlink’s diversification, with interconnector capacity of 1 GW offering meaningful upside when spreads widen.

- 2024 day-ahead France-UK spreads: €6–€12/MWh avg; peaks >€50/MWh

- France nuclear share ≈63% (2023); UK rising gas/renewables

- ElecLink capacity 1 GW enabling significant revenue during wide spreads

Capital Intensive Infrastructure Investment

Maintaining the 50.5 km Channel Tunnel and associated rolling stock demands continuous capital expenditure; Getlink reported capex of €473m in 2024 and plans multi-year investments into 2025–26 for renovation and fleet upgrades.

Financing costs are sensitive to global rates—EUR IBOR and swap rates rose in 2022–24, pushing Getlink’s net finance expense to €128m in 2024; careful debt management is required to protect operating cash flow.

- 2024 capex €473m

- Net finance expense €128m (2024)

- Channel Tunnel length 50.5 km

- Rate volatility risk into 2026

Inflation, FX and capex squeeze margins; ElecLink arbitrage boosts 2024 EBITDA

Inflation-driven labor/electricity cost rises (labor +8–10% YoY; 2022–24 energy spikes) squeezed margins despite partial indexation; 2024 capex €473m and net finance expense €128m heightened cash pressure. GBP/EUR moves (~5% swings ≈€20–30m revenue impact on 2024 €1.1bn) affect demand and reported results; hedging mitigates short-term FX P&L but not structural trends. Leisure demand fell with real disposable income down 1.2% in 2023, though 2024 tourism +8–10% helped passenger EBITDA; ElecLink 1 GW exploits France-UK spreads (2024 avg €6–€12/MWh, peaks >€50/MWh).

| Metric | 2023–24 |

|---|---|

| Revenue (2024) | ≈€1.1bn |

| Capex (2024) | €473m |

| Net finance expense (2024) | €128m |

| GBP/EUR 5% impact | ≈€20–30m rev |

| ElecLink capacity | 1 GW |

| France-UK spread (2024) | €6–€12/MWh avg; peaks >€50/MWh |

Same Document Delivered

Getlink PESTLE Analysis

The preview shown here is the exact Getlink PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and technological advances are reshaping Getlink's strategic landscape—our concise PESTLE highlights key external risks and opportunities you need to know; purchase the full analysis for a complete, actionable report ready for investor decks, strategy sessions, or competitive benchmarking.

Political factors

Post-Brexit Regulatory Stability

As of late 2025 the UK-EU relationship has stabilized into a structured framework that reduced border friction for Getlink, with cross-border delays at the Eurotunnel reported down 18% year-on-year and average customs clearance time cut to 22 minutes.

Ongoing bilateral agreements on customs and security protocols—covering 95% of freight movements—are essential to maintaining daily throughput near pre-Brexit capacity of ~17,000 trucks and 10,000 passengers.

Investors watch diplomatic ties closely: a 2025 scenario analysis by Getlink shows a 6–9% swing in EBITDA under higher-friction outcomes, directly linking political stability to terminal operational efficiency.

Energy Sovereignty and ElecLink

Government prioritization of energy security in France and the UK has raised ElecLink’s strategic value; the 1 GW HVDC link can transfer ~7.9 TWh/year, roughly 1.5% of UK annual demand (2024: ~520 TWh) and strengthens grid resilience.

Political backing for cross-border sharing reduces volatility risk and supports market integration, enhancing Getlink’s position amid EU–UK interconnector policies and 2025 capacity market reforms.

This alignment with national energy targets underpins long-term viability for Getlink’s diversification, with ElecLink contributing recurring regulated revenue and capex visibility into the late 2020s.

Geopolitical Security Measures

The Channel Tunnel, handling about 21 million passengers and 1.6 million freight units in 2023, is critical national infrastructure requiring constant coordination with state security agencies to deter unauthorized crossings and terrorism.

Since 2018 policy shifts on migration have driven Getlink to invest roughly €120–€180 million in enhanced surveillance, fencing and detection tech through 2025, reflecting rising capex needs tied to border security mandates.

Getlink must comply with state-mandated security measures while optimizing operations to avoid adding delay to services that delivered €1.1 billion revenue in 2024, balancing safety and transit speed.

Intergovernmental Commission Oversight

The Intergovernmental Commission (IGC) retains strong regulatory control over Channel Tunnel safety and economics, overseeing inspections and approving cross-Channel rolling stock; in 2024 the IGC conducted 18 major audits and approved 3 new vehicle types affecting Getlink fleet planning.

Political appointments to the IGC can shift audit frequency and approval timelines, with delays potentially impacting Getlink capex and revenue—Getlink reported €1.1bn capex guidance in 2024 that depends partly on timely IGC clearances.

Maintaining collaborative relations with the IGC reduces bureaucratic delays and supports smoother implementation of operational changes, critical as freight volumes rose 4.2% in 2024 versus 2023.

- IGC ran 18 major audits in 2024

- 3 new rolling stock approvals in 2024

- Getlink 2024 capex guidance ~€1.1bn

- Freight volumes +4.2% in 2024

Trade Policy and Freight Volume

Fluctuations in UK-EU trade deals materially affect Le Shuttle Freight volumes; post-Brexit customs changes cut truck crossings by about 10% in 2021, while 2023 recovery lifted freight throughput toward pre-2020 levels with Getlink reporting freight revenue of €387m in 2023, up 6% year-on-year.

Political shifts toward protectionism or new free-trade arrangements can reduce or boost demand for cross-channel logistics, making Getlink revenue highly sensitive to macro-political shifts that govern cross-border goods movement.

- 2023 freight revenue €387m (Getlink)

- Post-Brexit truck crossings down ~10% in 2021, recovering by 2023

- Trade policy volatility directly tied to demand for Le Shuttle Freight

Getlink: UK–EU stability key as border delays fall, capex high and EBITDA risk rises

Political stability in UK–EU relations and IGC oversight are crucial for Getlink: border delays down 18% (2025), customs clearance 22 minutes, freight +4.2% (2024), 2024 capex ~€1.1bn; ElecLink transfers ~7.9 TWh/year supporting energy targets; security-driven capex €120–180m (2018–2025) and freight revenue €387m (2023) link political outcomes to EBITDA volatility of 6–9% in stress scenarios.

| Metric | Value |

|---|---|

| Border delays change (2025) | -18% |

| Customs clearance | 22 min |

| Freight vol. change (2024) | +4.2% |

| Capex guidance (2024) | ~€1.1bn |

| Freight revenue (2023) | €387m |

What is included in the product

Explores how external macro-environmental factors uniquely affect Getlink across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives and investors.

Condenses Getlink's full PESTLE into a concise, shareable summary that’s visually segmented by category for quick interpretation and easy inclusion in presentations or planning sessions.

Economic factors

Inflationary Pressure on Operating Costs

By end-2025, persistent Eurozone and UK inflation raised labor costs ~8–10% YoY and pushed electricity prices for rail operations up ~20% vs 2022, squeezing Getlink margins despite index-linked contracts that pass portions of costs to customers; extreme energy spikes in 2022–24 still left residual exposure, requiring delicate pricing vs competitiveness decisions as operating overheads rose materially.

Currency Exchange Rate Volatility

Getlink operates in GBP and EUR, exposing it to GBP/EUR volatility; a 5% move in 2023–2024 would change reported revenue by roughly €20–30m given 2024 revenue ~€1.1bn. Such swings affect cross-border leisure travel demand—sterling weakness vs euro makes Channel crossings pricier for UK tourists. Getlink uses hedging (forwards/options) to smooth short-term FX P&L, but sustained trends in GBP/EUR continue to pressure long-term margins.

Consumer Discretionary Spending Trends

The demand for Le Shuttle and Eurostar is closely tied to Western European disposable income; Euro area real disposable income fell 1.2% in 2023 after inflation, pressuring leisure travel and reducing passenger vehicle volumes for Getlink.

High interest rates in 2024—ECB policy rate averaging ~3.75%—kept borrowing costly, further dampening discretionary trips and lower-margin car volumes.

By contrast, a strong 2024 tourism rebound saw international arrivals to France and the UK rise ~8–10%, boosting high-margin passenger traffic that materially supports Getlink’s EBITDA.

Electricity Market Integration

ElecLink revenue hinges on France-UK price spreads; 2024 average day-ahead spread was about €6–€12/MWh, but peaks exceeded €50/MWh during tight supply, driving volatile earnings.

National energy mixes and industrial demand shape these differentials—France’s nuclear output (≈63% 2023) vs UK gas/renewables mix increases arbitrage potential for Getlink.

Capitalizing on arbitrage via ElecLink supports Getlink’s diversification, with interconnector capacity of 1 GW offering meaningful upside when spreads widen.

- 2024 day-ahead France-UK spreads: €6–€12/MWh avg; peaks >€50/MWh

- France nuclear share ≈63% (2023); UK rising gas/renewables

- ElecLink capacity 1 GW enabling significant revenue during wide spreads

Capital Intensive Infrastructure Investment

Maintaining the 50.5 km Channel Tunnel and associated rolling stock demands continuous capital expenditure; Getlink reported capex of €473m in 2024 and plans multi-year investments into 2025–26 for renovation and fleet upgrades.

Financing costs are sensitive to global rates—EUR IBOR and swap rates rose in 2022–24, pushing Getlink’s net finance expense to €128m in 2024; careful debt management is required to protect operating cash flow.

- 2024 capex €473m

- Net finance expense €128m (2024)

- Channel Tunnel length 50.5 km

- Rate volatility risk into 2026

Inflation, FX and capex squeeze margins; ElecLink arbitrage boosts 2024 EBITDA

Inflation-driven labor/electricity cost rises (labor +8–10% YoY; 2022–24 energy spikes) squeezed margins despite partial indexation; 2024 capex €473m and net finance expense €128m heightened cash pressure. GBP/EUR moves (~5% swings ≈€20–30m revenue impact on 2024 €1.1bn) affect demand and reported results; hedging mitigates short-term FX P&L but not structural trends. Leisure demand fell with real disposable income down 1.2% in 2023, though 2024 tourism +8–10% helped passenger EBITDA; ElecLink 1 GW exploits France-UK spreads (2024 avg €6–€12/MWh, peaks >€50/MWh).

| Metric | 2023–24 |

|---|---|

| Revenue (2024) | ≈€1.1bn |

| Capex (2024) | €473m |

| Net finance expense (2024) | €128m |

| GBP/EUR 5% impact | ≈€20–30m rev |

| ElecLink capacity | 1 GW |

| France-UK spread (2024) | €6–€12/MWh avg; peaks >€50/MWh |

Same Document Delivered

Getlink PESTLE Analysis

The preview shown here is the exact Getlink PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.