Getty Realty Porter's Five Forces Analysis

Don't Miss the Bigger Picture

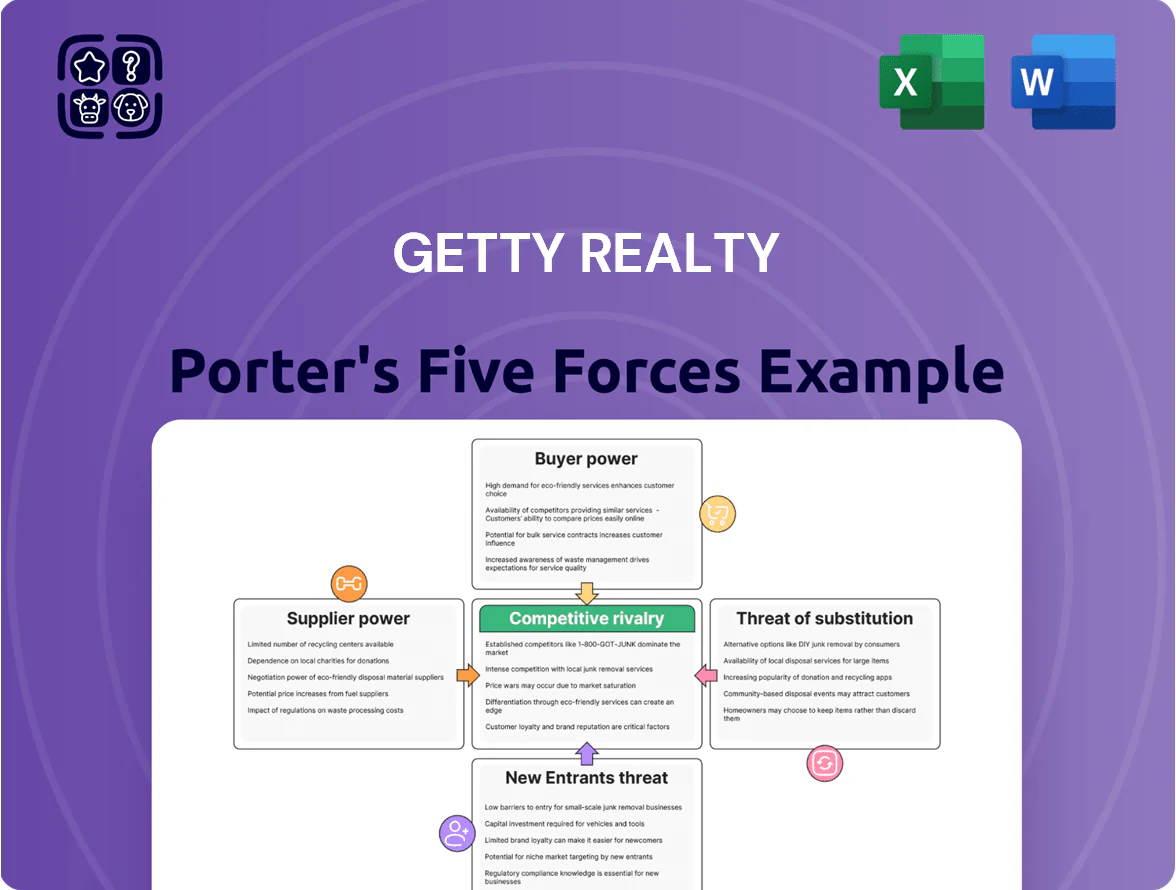

Getty Realty faces moderate buyer power and low threat of substitutes, while supplier leverage and entry barriers hinge on location-driven asset quality and capital intensity.

This snapshot highlights competitive tension from institutional landlords and cyclical tenant demand—key drivers of rent stability and valuation risk.

This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Getty Realty’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Access to Global Capital Markets

As a REIT, Getty Realty depends on debt and equity markets for acquisitions; in 2025 it carried about $1.1 billion debt and access to capital shapes growth pace.

Commercial banks and bondholders—who provided ~65% of external funding in 2024—wield pricing power over Getty’s cost of capital and covenant terms.

With US interest rates stabilizing near 5% by late 2025, capital suppliers became critical to preserve Getty’s investment spread, which reported a portfolio cap rate ~5.8% in 2024.

Prime Real Estate Landowners

The finite supply of high-traffic corner sites gives landowners strong leverage in acquisitions; Getty Realty competed for such parcels in 2024 when U.S. retail land vacancy hit 5.6%, pushing bid premiums as much as 18% in metro markets. Getty faces rivals including retail developers and cities, which in 2023-24 increased land values near highways by ~12% annually, raising entry costs and keeping sellers in a dominant bargaining position.

Construction and Environmental Service Firms

Specialized contractors for underground storage tank (UST) maintenance and c-store renovations form a narrow supplier group with required certifications (EPA UST, state remediation licenses) and technical skills; about 60–70% of UST work in 2024 was performed by firms with national/regional reach, concentrating capacity.

Because only ~150–200 US firms can handle large-scale environmental remediation to ASTM and state standards, their pricing power stays high; median remediation project margins rose to ~18% in 2024, so Getty Realty faces limited bargaining leverage.

Fuel Wholesalers and Distributors

Getty Realty is a landlord whose tenants’ margins hinge on fuel wholesalers and convenience-product distributors; in 2024 the top 4 U.S. fuel distributors handled ~70% of retail gasoline volumes, concentrating supply risk.

Supply-chain disruptions—like the 2021 Colonial Pipeline outage that spiked fuel prices by ~10% regionally—reduce dealer cash flow and can raise tenant default risk against Getty leases.

Because distribution is consolidated, suppliers exert indirect but material pressure on Getty’s rent stability and portfolio cash flow.

- Top 4 distributors ≈70% market share (2024)

- Colonial outage 2021: ~10% regional price spike

- Supply shocks → lower tenant EBITDA → higher default risk

- Indirect supplier power affects Getty’s revenue stability

Regulatory and Compliance Bodies

Regulatory agencies supply the permits and environmental clearances that determine whether Getty Realty’s retail properties can operate, giving regulators de facto veto power over asset income and reuse.

By late 2025, tighter state and federal rules—e.g., rising cleanup liabilities averaging $150k–$500k per site in recent EPA enforcement actions—will force Getty to spend on compliance or face decommissioning risks.

This oversight is a non-negotiable supplier of legal operating rights in petroleum retail, so changes in zoning or environmental law directly reduce asset liquidity and increase holding costs.

- Regulators = gatekeepers to revenue

- EPA/site cleanup costs ~$150k–$500k per site

- Late-2025 rule changes require capex to retain marketability

- Non-negotiable legal right to operate

Suppliers’ leverage caps Getty Realty: $1.1B debt, 70% distributor share, $150k–$500k cleanup

Suppliers—capital providers, landowners, specialized UST/remediation firms, fuel distributors, and regulators—hold high bargaining power over Getty Realty, constraining financing costs, acquisition pricing, remediation capex, tenant cash flow, and operating rights; key figures: $1.1B debt (2025), portfolio cap rate ~5.8% (2024), top-4 fuel distributors ≈70% share (2024), remediation margins ~18% (2024), cleanup costs $150k–$500k/site.

| Supplier | Key metric |

|---|---|

| Debt/equity | $1.1B debt (2025) |

| Landowners | Vacancy 5.6% (2024); bid premiums +18% |

| Fuel distributors | Top‑4 ≈70% (2024) |

| Remediation firms | Margins ~18%; cleanup $150k–$500k |

What is included in the product

Uncovers key competitive drivers, buyer/supplier power, entry barriers, substitutes, and industry rivalry specific to Getty Realty, highlighting disruptive threats, pricing influence, and strategic defenses to protect market share.

Getty Realty Porter's Five Forces in one concise sheet—instantly reveals tenant bargaining power, entry threats, and lease concentration risks to speed strategic decisions.

Customers Bargaining Power

Tenant Concentration Among Major Operators

Around 60% of Getty Realty’s 2025 rental income comes from a handful of large convenience-store and petroleum marketers, so these institutional tenants can demand lower rents or stricter tenant-friendly clauses.

Industry consolidation cut the top-10 c-store operators’ store counts by 12% via M&A through 2024–25, boosting their bargaining leverage at master-lease renewals.

Availability of Alternative Financing Solutions

Large tenants often choose between leasing from Getty Realty or buying with capex; in 2024 roughly 28% of major retail chains used internal financing or mortgages for store ownership, per industry data. If Getty’s sale-leaseback yields exceed typical mortgage rates (5–6% in 2024) or corporate bond spreads, tenants may avoid the REIT route. That optionality caps Getty’s ability to push rents well above local market equilibrium, keeping rent growth near CPI-linked levels.

Master Lease Structural Protections

Master leases give Getty Realty cross-collateralized security across sites, but they also concentrate negotiating leverage: multi-site tenants controlling >40% of a portfolio can threaten non-renewal to win concessions on maintenance or caps on rent escalators.

Shift Toward Electric Vehicle Infrastructure

As EV charging demand rises—US EV registrations grew 60% in 2023 and EV sales hit 7.6% of light‑vehicle sales in 2024—tenants pressure Getty Realty to offer sites with grid upgrades and flexible retail space; tenants favor landlords who co-invest in infrastructure to avoid capex.

This shifts bargaining power to tenants, forcing Getty to retrofit assets or lose high‑quality lessees and rental premiums tied to EV readiness.

- 2024 EV sales 7.6% of US light vehicles

- Tenants favor co-investment in grid upgrades

- Flexible non-fuel retail space increases lease appeal

Local Market Saturation and Site Performance

In saturated local markets, tenants can walk from underperforming sites at lease end, so Getty faces real churn risk where convenience-store density exceeds 25 stores per 100,000 people (2024 retail density data).

Tenant relocation options force Getty to invest in property upkeep and site advantages; Getty reported 97% portfolio occupancy in 2024, reflecting this focus on responsiveness.

- High density gives tenants leverage

- Tenant mobility enforces site quality

- Getty 97% occupancy (2024)

Large tenants & c‑store consolidation cap rents, EV upgrades bite as occupancy masks churn

Major tenants (≈60% of 2025 rents) and top-10 c‑store consolidation (‑12% store counts 2024–25) give customers strong leverage, keeping rent growth near CPI and forcing Getty to co‑invest in EV/grid upgrades; 97% occupancy in 2024 masks churn risk where density >25 stores/100k.

| Metric | Value |

|---|---|

| Share of rents from large tenants (2025) | ≈60% |

| Top‑10 c‑store count change (2024–25) | ‑12% |

| US EV sales (2024) | 7.6% |

| Portfolio occupancy (2024) | 97% |

| Density level raising churn risk | >25/100k |

Preview the Actual Deliverable

Getty Realty Porter's Five Forces Analysis

This preview shows the exact Getty Realty Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders, no mockups; it’s the final, professionally formatted document ready for download and use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Getty Realty faces moderate buyer power and low threat of substitutes, while supplier leverage and entry barriers hinge on location-driven asset quality and capital intensity.

This snapshot highlights competitive tension from institutional landlords and cyclical tenant demand—key drivers of rent stability and valuation risk.

This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Getty Realty’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Access to Global Capital Markets

As a REIT, Getty Realty depends on debt and equity markets for acquisitions; in 2025 it carried about $1.1 billion debt and access to capital shapes growth pace.

Commercial banks and bondholders—who provided ~65% of external funding in 2024—wield pricing power over Getty’s cost of capital and covenant terms.

With US interest rates stabilizing near 5% by late 2025, capital suppliers became critical to preserve Getty’s investment spread, which reported a portfolio cap rate ~5.8% in 2024.

Prime Real Estate Landowners

The finite supply of high-traffic corner sites gives landowners strong leverage in acquisitions; Getty Realty competed for such parcels in 2024 when U.S. retail land vacancy hit 5.6%, pushing bid premiums as much as 18% in metro markets. Getty faces rivals including retail developers and cities, which in 2023-24 increased land values near highways by ~12% annually, raising entry costs and keeping sellers in a dominant bargaining position.

Construction and Environmental Service Firms

Specialized contractors for underground storage tank (UST) maintenance and c-store renovations form a narrow supplier group with required certifications (EPA UST, state remediation licenses) and technical skills; about 60–70% of UST work in 2024 was performed by firms with national/regional reach, concentrating capacity.

Because only ~150–200 US firms can handle large-scale environmental remediation to ASTM and state standards, their pricing power stays high; median remediation project margins rose to ~18% in 2024, so Getty Realty faces limited bargaining leverage.

Fuel Wholesalers and Distributors

Getty Realty is a landlord whose tenants’ margins hinge on fuel wholesalers and convenience-product distributors; in 2024 the top 4 U.S. fuel distributors handled ~70% of retail gasoline volumes, concentrating supply risk.

Supply-chain disruptions—like the 2021 Colonial Pipeline outage that spiked fuel prices by ~10% regionally—reduce dealer cash flow and can raise tenant default risk against Getty leases.

Because distribution is consolidated, suppliers exert indirect but material pressure on Getty’s rent stability and portfolio cash flow.

- Top 4 distributors ≈70% market share (2024)

- Colonial outage 2021: ~10% regional price spike

- Supply shocks → lower tenant EBITDA → higher default risk

- Indirect supplier power affects Getty’s revenue stability

Regulatory and Compliance Bodies

Regulatory agencies supply the permits and environmental clearances that determine whether Getty Realty’s retail properties can operate, giving regulators de facto veto power over asset income and reuse.

By late 2025, tighter state and federal rules—e.g., rising cleanup liabilities averaging $150k–$500k per site in recent EPA enforcement actions—will force Getty to spend on compliance or face decommissioning risks.

This oversight is a non-negotiable supplier of legal operating rights in petroleum retail, so changes in zoning or environmental law directly reduce asset liquidity and increase holding costs.

- Regulators = gatekeepers to revenue

- EPA/site cleanup costs ~$150k–$500k per site

- Late-2025 rule changes require capex to retain marketability

- Non-negotiable legal right to operate

Suppliers’ leverage caps Getty Realty: $1.1B debt, 70% distributor share, $150k–$500k cleanup

Suppliers—capital providers, landowners, specialized UST/remediation firms, fuel distributors, and regulators—hold high bargaining power over Getty Realty, constraining financing costs, acquisition pricing, remediation capex, tenant cash flow, and operating rights; key figures: $1.1B debt (2025), portfolio cap rate ~5.8% (2024), top-4 fuel distributors ≈70% share (2024), remediation margins ~18% (2024), cleanup costs $150k–$500k/site.

| Supplier | Key metric |

|---|---|

| Debt/equity | $1.1B debt (2025) |

| Landowners | Vacancy 5.6% (2024); bid premiums +18% |

| Fuel distributors | Top‑4 ≈70% (2024) |

| Remediation firms | Margins ~18%; cleanup $150k–$500k |

What is included in the product

Uncovers key competitive drivers, buyer/supplier power, entry barriers, substitutes, and industry rivalry specific to Getty Realty, highlighting disruptive threats, pricing influence, and strategic defenses to protect market share.

Getty Realty Porter's Five Forces in one concise sheet—instantly reveals tenant bargaining power, entry threats, and lease concentration risks to speed strategic decisions.

Customers Bargaining Power

Tenant Concentration Among Major Operators

Around 60% of Getty Realty’s 2025 rental income comes from a handful of large convenience-store and petroleum marketers, so these institutional tenants can demand lower rents or stricter tenant-friendly clauses.

Industry consolidation cut the top-10 c-store operators’ store counts by 12% via M&A through 2024–25, boosting their bargaining leverage at master-lease renewals.

Availability of Alternative Financing Solutions

Large tenants often choose between leasing from Getty Realty or buying with capex; in 2024 roughly 28% of major retail chains used internal financing or mortgages for store ownership, per industry data. If Getty’s sale-leaseback yields exceed typical mortgage rates (5–6% in 2024) or corporate bond spreads, tenants may avoid the REIT route. That optionality caps Getty’s ability to push rents well above local market equilibrium, keeping rent growth near CPI-linked levels.

Master Lease Structural Protections

Master leases give Getty Realty cross-collateralized security across sites, but they also concentrate negotiating leverage: multi-site tenants controlling >40% of a portfolio can threaten non-renewal to win concessions on maintenance or caps on rent escalators.

Shift Toward Electric Vehicle Infrastructure

As EV charging demand rises—US EV registrations grew 60% in 2023 and EV sales hit 7.6% of light‑vehicle sales in 2024—tenants pressure Getty Realty to offer sites with grid upgrades and flexible retail space; tenants favor landlords who co-invest in infrastructure to avoid capex.

This shifts bargaining power to tenants, forcing Getty to retrofit assets or lose high‑quality lessees and rental premiums tied to EV readiness.

- 2024 EV sales 7.6% of US light vehicles

- Tenants favor co-investment in grid upgrades

- Flexible non-fuel retail space increases lease appeal

Local Market Saturation and Site Performance

In saturated local markets, tenants can walk from underperforming sites at lease end, so Getty faces real churn risk where convenience-store density exceeds 25 stores per 100,000 people (2024 retail density data).

Tenant relocation options force Getty to invest in property upkeep and site advantages; Getty reported 97% portfolio occupancy in 2024, reflecting this focus on responsiveness.

- High density gives tenants leverage

- Tenant mobility enforces site quality

- Getty 97% occupancy (2024)

Large tenants & c‑store consolidation cap rents, EV upgrades bite as occupancy masks churn

Major tenants (≈60% of 2025 rents) and top-10 c‑store consolidation (‑12% store counts 2024–25) give customers strong leverage, keeping rent growth near CPI and forcing Getty to co‑invest in EV/grid upgrades; 97% occupancy in 2024 masks churn risk where density >25 stores/100k.

| Metric | Value |

|---|---|

| Share of rents from large tenants (2025) | ≈60% |

| Top‑10 c‑store count change (2024–25) | ‑12% |

| US EV sales (2024) | 7.6% |

| Portfolio occupancy (2024) | 97% |

| Density level raising churn risk | >25/100k |

Preview the Actual Deliverable

Getty Realty Porter's Five Forces Analysis

This preview shows the exact Getty Realty Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders, no mockups; it’s the final, professionally formatted document ready for download and use.