Gibson, Dunn & Crutcher Porter's Five Forces Analysis

From Overview to Strategy Blueprint

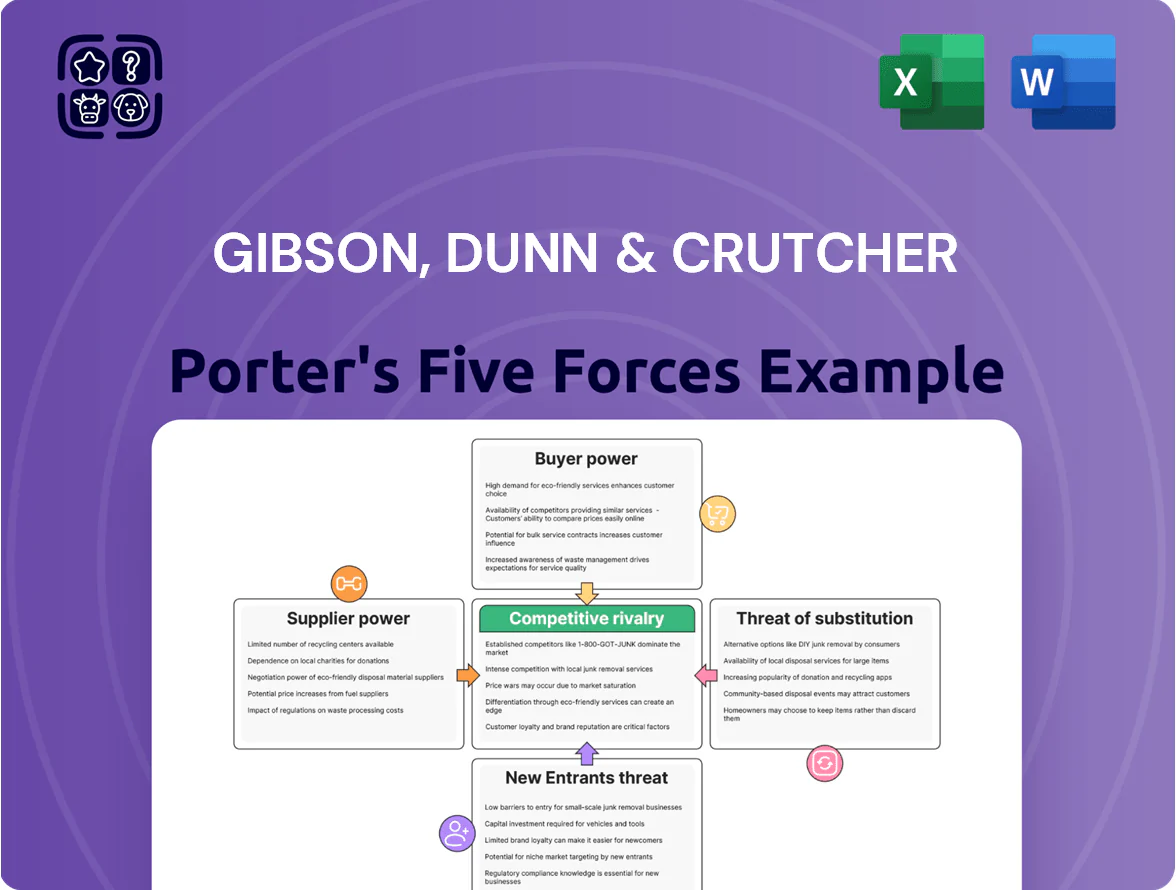

Suppliers Bargaining Power

Scarcity of elite legal talent

For Gibson Dunn, primary suppliers are elite attorneys from top law schools; by late 2025 demand for graduates of T14 schools and experienced laterals rose ~8% year-over-year, tightening supply and boosting leverage.

Intense competition lets candidates push pay and hybrid work; Gibson Dunn sustains premium salaries—associate pay bands rose about 10% in 2024–25—to limit poaching and retain rainmakers.

Specialized technology and AI providers

Legal tech vendors supplying AI-driven discovery, research, and practice-management tools exert moderate supplier power over Gibson Dunn as these systems underpin firm efficiency; 2025 surveys show 62% of AmLaw 200 firms report generative-AI tools as mission-critical.

Gibson Dunn relies on a handful of key developers for proprietary capabilities, and industry consolidation left the top three legal-AI suppliers with ~54% market share in 2024, boosting their pricing leverage.

Switching costs are high: migrating integrated platforms often costs 6–12 months of workflow disruption and estimated USD 2–5 million in implementation and training for a firm of Gibson Dunn’s size, giving suppliers room to raise prices.

Commercial real estate in premium markets

Landlords in premium hubs like New York, London and Hong Kong keep strong leverage—Class A Midtown Manhattan and Mayfair rents averaged $120–150/ft2/year in 2024, and Central HK top rents hit HK$200/ft2/month—so securing prestige addresses drives higher lease costs for Gibson Dunn. Still, hybrid work reduced required office area by ~20% across law firms by 2025, giving tenants some negotiating room on term length and fit-out concessions.

Professional liability insurance carriers

Gibson Dunn needs very large professional liability policies for multibillion-dollar deals and major litigation; only a few global carriers (AIG, Chubb, Lloyd’s syndicates) can underwrite limits often exceeding $100m, so insurers hold pricing and protocol influence.

Premiums jumped industry-wide ~20–35% from 2020–24; a geopolitical or macro risk spike would raise Gibson Dunn’s costs and tighten coverage terms quickly.

- Few carriers: AIG, Chubb, Lloyd’s

- Typical limits: often >$100m

- Premium rise 2020–24: ~20–35%

- Global risk spikes raise costs, tighten terms

Expert witnesses and specialized consultants

Complex litigation for Gibson, Dunn & Crutcher often needs world-renowned experts in niche science, finance, or tech; such experts charged median expert witness fees of $600–900/hr in 2024 and occasional flat retainer up to $200,000, boosting supplier power.

The firm’s reliance on these experts for high-profile wins strengthens experts’ bargaining position, as their credibility can sway jury outcomes and settlement values by millions.

- Experts = scarce, high-fee suppliers

- Median fees $600–900/hr (2024)

- Retainers up to $200,000

- Can shift case value by $M+

Suppliers Tighten: Elite Talent Scarce, Pay & Insurance Costs Surge; Legal‑AI Dominates

Suppliers exert moderate-to-strong power: elite attorney supply tightened ~8% YoY to late-2025, associate pay rose ~10% in 2024–25, legal-AI vendors held ~54% market share (2024) with 62% of AmLaw200 calling generative AI mission-critical (2025), key insurers (AIG, Chubb, Lloyd’s) underwrite >$100m limits with premiums +20–35% (2020–24), expert witnesses median $600–900/hr (2024).

| Supplier | Key stat |

|---|---|

| Elite hires | Supply -8% YoY (2025) |

| Associate pay | +10% (2024–25) |

| Legal-AI | 54% top3 share (2024); 62% AmLaw200 (2025) |

| Insurers | Limits >$100m; premiums +20–35% (2020–24) |

| Experts | $600–900/hr (2024) |

What is included in the product

Tailored exclusively for Gibson, Dunn & Crutcher, this Porter's Five Forces overview uncovers key drivers of competition, supplier and buyer influence, entry barriers, and substitute threats that shape the firm's pricing power and long-term profitability.

A concise Gibson, Dunn & Crutcher Porter's Five Forces sheet that distills competitive pressure into actionable insights—ideal for rapid strategy sessions or investor briefs.

Customers Bargaining Power

Sophisticated corporate procurement departments

Corporate legal ops teams now control vendor selection and spend; 68% of Fortune 500 buyers reported using legal operations platforms in 2024, letting them benchmark firms by cycle time, win rates, and per-matter cost.

Buyers push alternative fee arrangements (AFAs); AFAs rose to 32% of major corporate matters in 2024 versus 18% in 2019, cutting billable-hour revenue and margins for many firms.

By 2025, pricing power has materially shifted: top 200 corporate buyers negotiate discounts averaging 22% and demand KPIs tied to fixed fees, concentrating leverage with institutional clients.

Low switching costs for non-specialized work

While Gibson, Dunn & Crutcher leads in high-stakes litigation and M&A, routine legal work—estimated at ~30% of firm revenue in Big Law averages—can shift easily to other Am Law firms; clients use that portability to demand fee concessions across broader portfolios. In 2024 client-side pressure pushed average partner rates down 1.5% year-over-year, so Gibson Dunn must show superior value and cross-practice synergies to retain mandates.

Concentration of revenue among major financial institutions

A significant portion of Gibson, Dunn & Crutcher’s revenue comes from a core group of global banks and private equity firms—about 30–40% of firmwide revenue in 2024 came from the top 20 institutional clients, per industry estimates. These high-volume clients wield strong bargaining power to secure discounted rates and strict SLAs, pushing average hourly realization down by an estimated 8–12%. Losing a single top institutional client could cut annual pre-tax profit by roughly 3–6%, given margin concentration and fixed-cost structure.

In-house legal department expansion

Large corporates grew in-house legal headcount: FT reported 2024 surveys show 68% of S&P 500 companies expanded internal teams since 2019, shifting routine M&A, compliance, and contract work away from firms like Gibson Dunn.

Clients now buy outside counsel mainly for bet-the-company or high-stakes litigation, shrinking mid-tier fee pools and increasing buyer leverage over pricing, staffing, and scope.

- 68% of S&P 500 expanded in-house since 2019

- Outside counsel now used mainly for highest-risk matters

- Mid-tier fee pool contracting, raising client bargaining power

Transparency through legal rankings and peer reviews

The rise of legal rankings and peer reviews gives clients granular data on Gibson Dunn’s win rates, billable hours, and client satisfaction—Bloomberg/BTI data in 2024 shows top firms’ RFP success tied to published outcomes.

Clients benchmark Gibson Dunn against rivals in RFPs, so fee premiums need clear, documented advantages; without them, price compression follows.

- Detailed rankings enable precise benchmarking

- 2024 surveys link published results to higher RFP win rates

- Data parity limits unjustified premium pricing

Buyers’ Muscle: Legal Ops + AFAs Drive 22% Cuts, Top 20 Clients Command 30–40%

Buyers hold strong leverage: 68% of Fortune 500 use legal ops platforms (2024), AFAs rose to 32% of major matters (2024), and top 200 buyers negotiate average 22% discounts by 2025, concentrating power with 20 clients that supplied ~30–40% of Gibson Dunn’s 2024 revenue.

| Metric | Value |

|---|---|

| Fortune 500 legal ops adoption (2024) | 68% |

| AFAs share (2019 → 2024) | 18% → 32% |

| Avg discount from top 200 buyers (2025) | 22% |

| Revenue from top 20 clients (Gibson Dunn, 2024) | 30–40% |

Preview the Actual Deliverable

Gibson, Dunn & Crutcher Porter's Five Forces Analysis

This preview shows the exact Gibson, Dunn & Crutcher Porter’s Five Forces analysis you'll receive—fully formatted, professionally written, and ready for immediate download after purchase, with no placeholders or samples.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Suppliers Bargaining Power

Scarcity of elite legal talent

For Gibson Dunn, primary suppliers are elite attorneys from top law schools; by late 2025 demand for graduates of T14 schools and experienced laterals rose ~8% year-over-year, tightening supply and boosting leverage.

Intense competition lets candidates push pay and hybrid work; Gibson Dunn sustains premium salaries—associate pay bands rose about 10% in 2024–25—to limit poaching and retain rainmakers.

Specialized technology and AI providers

Legal tech vendors supplying AI-driven discovery, research, and practice-management tools exert moderate supplier power over Gibson Dunn as these systems underpin firm efficiency; 2025 surveys show 62% of AmLaw 200 firms report generative-AI tools as mission-critical.

Gibson Dunn relies on a handful of key developers for proprietary capabilities, and industry consolidation left the top three legal-AI suppliers with ~54% market share in 2024, boosting their pricing leverage.

Switching costs are high: migrating integrated platforms often costs 6–12 months of workflow disruption and estimated USD 2–5 million in implementation and training for a firm of Gibson Dunn’s size, giving suppliers room to raise prices.

Commercial real estate in premium markets

Landlords in premium hubs like New York, London and Hong Kong keep strong leverage—Class A Midtown Manhattan and Mayfair rents averaged $120–150/ft2/year in 2024, and Central HK top rents hit HK$200/ft2/month—so securing prestige addresses drives higher lease costs for Gibson Dunn. Still, hybrid work reduced required office area by ~20% across law firms by 2025, giving tenants some negotiating room on term length and fit-out concessions.

Professional liability insurance carriers

Gibson Dunn needs very large professional liability policies for multibillion-dollar deals and major litigation; only a few global carriers (AIG, Chubb, Lloyd’s syndicates) can underwrite limits often exceeding $100m, so insurers hold pricing and protocol influence.

Premiums jumped industry-wide ~20–35% from 2020–24; a geopolitical or macro risk spike would raise Gibson Dunn’s costs and tighten coverage terms quickly.

- Few carriers: AIG, Chubb, Lloyd’s

- Typical limits: often >$100m

- Premium rise 2020–24: ~20–35%

- Global risk spikes raise costs, tighten terms

Expert witnesses and specialized consultants

Complex litigation for Gibson, Dunn & Crutcher often needs world-renowned experts in niche science, finance, or tech; such experts charged median expert witness fees of $600–900/hr in 2024 and occasional flat retainer up to $200,000, boosting supplier power.

The firm’s reliance on these experts for high-profile wins strengthens experts’ bargaining position, as their credibility can sway jury outcomes and settlement values by millions.

- Experts = scarce, high-fee suppliers

- Median fees $600–900/hr (2024)

- Retainers up to $200,000

- Can shift case value by $M+

Suppliers Tighten: Elite Talent Scarce, Pay & Insurance Costs Surge; Legal‑AI Dominates

Suppliers exert moderate-to-strong power: elite attorney supply tightened ~8% YoY to late-2025, associate pay rose ~10% in 2024–25, legal-AI vendors held ~54% market share (2024) with 62% of AmLaw200 calling generative AI mission-critical (2025), key insurers (AIG, Chubb, Lloyd’s) underwrite >$100m limits with premiums +20–35% (2020–24), expert witnesses median $600–900/hr (2024).

| Supplier | Key stat |

|---|---|

| Elite hires | Supply -8% YoY (2025) |

| Associate pay | +10% (2024–25) |

| Legal-AI | 54% top3 share (2024); 62% AmLaw200 (2025) |

| Insurers | Limits >$100m; premiums +20–35% (2020–24) |

| Experts | $600–900/hr (2024) |

What is included in the product

Tailored exclusively for Gibson, Dunn & Crutcher, this Porter's Five Forces overview uncovers key drivers of competition, supplier and buyer influence, entry barriers, and substitute threats that shape the firm's pricing power and long-term profitability.

A concise Gibson, Dunn & Crutcher Porter's Five Forces sheet that distills competitive pressure into actionable insights—ideal for rapid strategy sessions or investor briefs.

Customers Bargaining Power

Sophisticated corporate procurement departments

Corporate legal ops teams now control vendor selection and spend; 68% of Fortune 500 buyers reported using legal operations platforms in 2024, letting them benchmark firms by cycle time, win rates, and per-matter cost.

Buyers push alternative fee arrangements (AFAs); AFAs rose to 32% of major corporate matters in 2024 versus 18% in 2019, cutting billable-hour revenue and margins for many firms.

By 2025, pricing power has materially shifted: top 200 corporate buyers negotiate discounts averaging 22% and demand KPIs tied to fixed fees, concentrating leverage with institutional clients.

Low switching costs for non-specialized work

While Gibson, Dunn & Crutcher leads in high-stakes litigation and M&A, routine legal work—estimated at ~30% of firm revenue in Big Law averages—can shift easily to other Am Law firms; clients use that portability to demand fee concessions across broader portfolios. In 2024 client-side pressure pushed average partner rates down 1.5% year-over-year, so Gibson Dunn must show superior value and cross-practice synergies to retain mandates.

Concentration of revenue among major financial institutions

A significant portion of Gibson, Dunn & Crutcher’s revenue comes from a core group of global banks and private equity firms—about 30–40% of firmwide revenue in 2024 came from the top 20 institutional clients, per industry estimates. These high-volume clients wield strong bargaining power to secure discounted rates and strict SLAs, pushing average hourly realization down by an estimated 8–12%. Losing a single top institutional client could cut annual pre-tax profit by roughly 3–6%, given margin concentration and fixed-cost structure.

In-house legal department expansion

Large corporates grew in-house legal headcount: FT reported 2024 surveys show 68% of S&P 500 companies expanded internal teams since 2019, shifting routine M&A, compliance, and contract work away from firms like Gibson Dunn.

Clients now buy outside counsel mainly for bet-the-company or high-stakes litigation, shrinking mid-tier fee pools and increasing buyer leverage over pricing, staffing, and scope.

- 68% of S&P 500 expanded in-house since 2019

- Outside counsel now used mainly for highest-risk matters

- Mid-tier fee pool contracting, raising client bargaining power

Transparency through legal rankings and peer reviews

The rise of legal rankings and peer reviews gives clients granular data on Gibson Dunn’s win rates, billable hours, and client satisfaction—Bloomberg/BTI data in 2024 shows top firms’ RFP success tied to published outcomes.

Clients benchmark Gibson Dunn against rivals in RFPs, so fee premiums need clear, documented advantages; without them, price compression follows.

- Detailed rankings enable precise benchmarking

- 2024 surveys link published results to higher RFP win rates

- Data parity limits unjustified premium pricing

Buyers’ Muscle: Legal Ops + AFAs Drive 22% Cuts, Top 20 Clients Command 30–40%

Buyers hold strong leverage: 68% of Fortune 500 use legal ops platforms (2024), AFAs rose to 32% of major matters (2024), and top 200 buyers negotiate average 22% discounts by 2025, concentrating power with 20 clients that supplied ~30–40% of Gibson Dunn’s 2024 revenue.

| Metric | Value |

|---|---|

| Fortune 500 legal ops adoption (2024) | 68% |

| AFAs share (2019 → 2024) | 18% → 32% |

| Avg discount from top 200 buyers (2025) | 22% |

| Revenue from top 20 clients (Gibson Dunn, 2024) | 30–40% |

Preview the Actual Deliverable

Gibson, Dunn & Crutcher Porter's Five Forces Analysis

This preview shows the exact Gibson, Dunn & Crutcher Porter’s Five Forces analysis you'll receive—fully formatted, professionally written, and ready for immediate download after purchase, with no placeholders or samples.