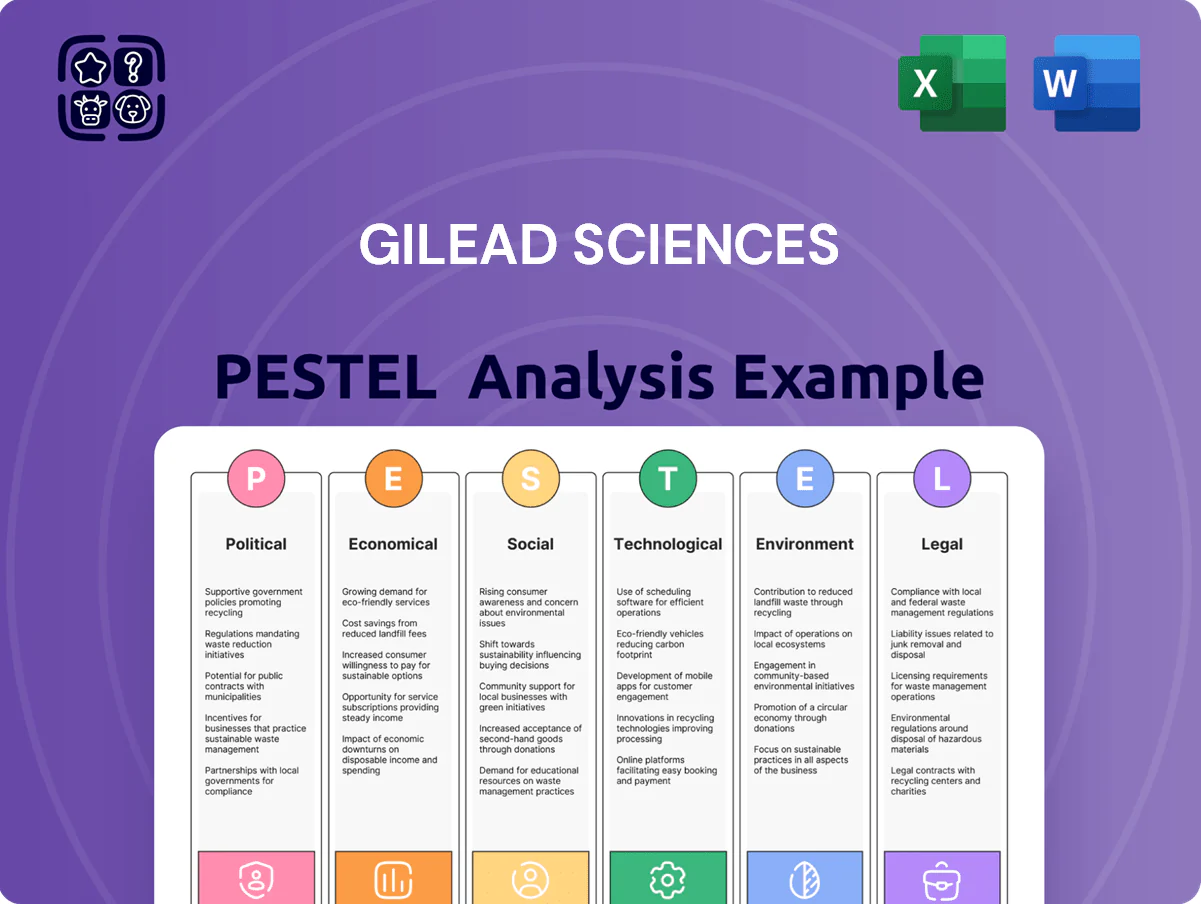

Gilead Sciences PESTLE Analysis

Skip the Research. Get the Strategy.

Gilead Sciences faces a complex external landscape—regulatory scrutiny, shifting drug-pricing debates, advancing biotech technologies, and growing ESG expectations—that could reshape its R&D and market strategies; our PESTLE distills these forces into actionable intelligence. Purchase the full analysis to get detailed risk scenarios, strategic implications, and ready-to-use slides to inform investment or corporate decisions.

Political factors

Drug Pricing Legislation and the Inflation Reduction Act

The ongoing implementation of the Inflation Reduction Act (IRA) is pressuring Gilead’s pricing strategy, as Medicare negotiation could target top antiviral drugs that accounted for roughly $13.5B of revenue in 2024; negotiated price caps may compress gross margins on established products.

Geopolitical Stability and Global Supply Chain Security

Trade tensions between the US, EU and China risk disrupting supply of APIs and intermediates; in 2024 global pharma trade volatility rose 12%, increasing procurement costs for firms like Gilead that sourced ~35% of APIs from Asia in 2023. Gilead’s network spans 20+ countries and remains sensitive to shifts in tariffs and export controls that can delay production. Strategic diversification—Gilead expanded capacity with a $500m investment in 2024 to add sites in Ireland and Singapore—mitigates regional political instability risks.

Government Funding for HIV and Hepatitis Initiatives

Public health budgets and programs like PEPFAR (FY2025 US appropriations ~$6.8bn) materially drive demand for Gilead antiviral sales, with PEPFAR and the Global Fund supporting procurement in >50 low- and middle-income countries.

Shifts in political leadership or fiscal priorities can cut yearly allocations—PEPFAR funding varied ±5–10% over past decade—creating revenue volatility for Gilead in key markets.

Maintaining access requires sustained advocacy and public-private partnerships; Gilead reported ~$1.2bn in global access investments in 2024 to secure procurement channels and tiered pricing.

Regulatory Alignment Across International Markets

Political cooperation on healthcare standards accelerates Gilead’s global launch of oncology and inflammation drugs; harmonized approvals cut time-to-market—EMA median approval 426 days vs FDA 303 days (2023), while China’s NMPA reforms reduced review times by ~20% in 2021–2023.

Divergent EU, US, China requirements raise compliance costs—Gilead reported R&D and licensing expenses of $6.2bn in FY2024—risking delayed revenue recognition and market fragmentation.

Gilead must align regulatory strategies across jurisdictions through parallel submissions and reliance pathways to optimize rollout and protect peak sales.

- FDA median approval 303 days (2023) vs EMA 426 days

- China NMPA review times down ~20% (2021–2023)

- Gilead R&D/licensing expenses $6.2bn FY2024

Taxation Policies and International Profit Repatriation

Corporate tax reforms in the US and the OECD two-pillar global minimum tax (15%) affect Gilead’s effective tax rate and cash repatriation strategies; Gilead reported a GAAP tax rate of 12% in 2024 but faces pressure to align with the 15% minimum, which could reduce tax planning opportunities and increase cash tax outflows.

Revisions to IP taxation—shift toward nexus-based and marketing-relief rules—can lower after-tax margins on overseas royalties; in 2024 Gilead booked ~30% of revenue outside the US, so changes materially affect net profitability by region.

Financial planners must model increased cash taxes and reduced BEPS-driven benefits when valuing Gilead; sensitivity scenarios shifting the effective tax rate by +3–6 percentage points can reduce FCFF and terminal value meaningfully for DCFs.

- 2024 GAAP tax rate: 12%

- OECD global minimum: 15%

- ~30% revenue from outside US (2024)

- Valuation sensitivity: +3–6 ppt tax rate → lower FCFF/terminal value

Gilead faces pricing, tax & supply risks—$13.5B antiviral revenue and margin pressure

Political actions—IRA Medicare negotiation, OECD 15% minimum tax, and trade/tariff shifts—threaten Gilead’s pricing, margins, and supply chain; IRA targets ~$13.5B antiviral revenue (2024), GAAP tax 12% vs OECD 15%, ~30% revenue outside US, and 35% APIs sourced from Asia (2023). Gilead’s $500m 2024 capacity spend and $1.2bn access investments partially mitigate risks while regulatory divergence raises R&D/compliance costs ($6.2bn FY2024).

| Metric | Value |

|---|---|

| Antiviral revenue at risk (2024) | $13.5B |

| GAAP tax rate (2024) | 12% |

| OECD minimum tax | 15% |

| Revenue outside US (2024) | ~30% |

| APIs from Asia (2023) | 35% |

| 2024 capacity investment | $500M |

| 2024 access investments | $1.2B |

| R&D/licensing expense (FY2024) | $6.2B |

What is included in the product

Explores how external macro-environmental factors uniquely affect Gilead Sciences across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform strategy, risk mitigation, and opportunity identification for executives and investors.

A concise, visually segmented PESTLE snapshot of Gilead Sciences that highlights regulatory, technological, and market risks for quick inclusion in decks or meeting briefs, with editable notes for regional or pipeline-specific context.

Economic factors

Impact of Global Interest Rate Environments

Persistent high US Federal Reserve rates (2024 year-end federal funds target 5.25–5.50%) and 10-year Treasury yields around 4.6% increase Gilead Sciences’ cost of debt, raising financing costs for oncology M&A and potentially reducing deal IRRs.

Higher rates make leverage pricier; Gilead’s net debt/EBITDA (about 1.5x FY2024) and $7–8bn annual cash flow projections shape its ability to fund acquisitions without excessive dilution.

Investors should monitor credit spreads and Fed guidance, as rate volatility can constrain deal size, push Gilead toward stock-based trades, or delay strategic expansion.

Currency Exchange Rate Volatility

With approximately 45% of 2024 revenue derived outside the US, Gilead faces material exposure to US dollar movements; a 10% dollar appreciation versus major currencies historically reduced reported international revenue by roughly 4–6% in prior periods.

Healthcare Budget Constraints and Payor Pressure

Economic downturns and 2024–25 austerity measures have tightened reimbursement: OECD government health spending growth slowed to 1.2% in 2024, prompting stricter payor reviews across Europe and parts of Asia.

Insurers now demand demonstrable long-term value; US private payors rejected or limited access to several high-cost cell therapies in 2024 after cost-effectiveness concerns.

Gilead must prove superior cost-effectiveness—health economic models showing lower lifetime costs or QALY gains versus standard care are increasingly required to secure coverage and favorable pricing.

Inflationary Pressure on Manufacturing and R&D Costs

Inflation has driven wages for specialized biotech talent up ~6-8% in 2024 and raw-material costs rise ~9% year-over-year, compressing Gilead’s operating margins unless drug prices or efficiency gains offset them.

The capital-intensive R&D budget is sensitive to inflation; a 5% CPI rise in 2024 can increase pipeline costs by hundreds of millions, affecting future approvals.

Operational efficiency and supply-chain optimization—including hedging energy and sourcing strategies—are essential to protect profitability.

- Specialized labor +6–8% (2024)

- Raw materials +9% YoY (2024)

- CPI impact ~5% raises pipeline costs materially

- Focus: supply-chain, energy hedging, operational efficiency

Consumer Purchasing Power in Emerging Markets

Rising middle classes in markets like India and Brazil—where middle-class consumption grew by ~3% CAGR 2015–2023 and middle-class populations reached ~300m and ~110m respectively in 2024—increase demand for Gilead’s antivirals and HIV treatments but affordability remains constrained.

Economic volatility, with 2023 GDP growth swings of ±2–4% in many EMs, can suppress uptake of high-cost chronic therapies, pressuring volumes and reimbursement timelines.

Tiered pricing and local manufacturing partnerships are essential; Gilead has used differential pricing in ~40+ LMICs and can expand such models to protect margins while boosting access.

- Rising middle class: India ~300m, Brazil ~110m (2024)

- EM GDP volatility: ±2–4% swings (2023)

- Tiered pricing used in 40+ LMICs

High US rates squeeze oncology M&A returns; FX and input inflation pressure growth

High US rates (Fed funds 5.25–5.50% end-2024) raise funding costs, pressuring oncology M&A returns; net debt/EBITDA ~1.5x and $7–8bn annual cash flow guide deal capacity. FX: ~45% revenue ex-US; a 10% USD appreciation cuts reported intl revenue ~4–6%. 2024: specialized labor +6–8%, raw materials +9% YoY; OECD health spending growth 1.2% tightening reimbursement; EM middle class: India ~300m, Brazil ~110m.

| Metric | 2024 Value |

|---|---|

| Fed funds | 5.25–5.50% |

| 10yr US Treasury | ~4.6% |

| Net debt/EBITDA | ~1.5x |

| Annual cash flow | $7–8bn |

| Revenue ex-US | ~45% |

| Labor inflation | +6–8% |

| Raw materials | +9% YoY |

| OECD health spend growth | 1.2% |

| India middle class | ~300m |

| Brazil middle class | ~110m |

Preview Before You Purchase

Gilead Sciences PESTLE Analysis

The preview shown here is the exact Gilead Sciences PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It includes the complete political, economic, social, technological, legal, and environmental assessment as displayed. No placeholders or teasers—this is the real, final document you’ll download immediately after payment. The content and structure are identical to the delivered file.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Gilead Sciences faces a complex external landscape—regulatory scrutiny, shifting drug-pricing debates, advancing biotech technologies, and growing ESG expectations—that could reshape its R&D and market strategies; our PESTLE distills these forces into actionable intelligence. Purchase the full analysis to get detailed risk scenarios, strategic implications, and ready-to-use slides to inform investment or corporate decisions.

Political factors

Drug Pricing Legislation and the Inflation Reduction Act

The ongoing implementation of the Inflation Reduction Act (IRA) is pressuring Gilead’s pricing strategy, as Medicare negotiation could target top antiviral drugs that accounted for roughly $13.5B of revenue in 2024; negotiated price caps may compress gross margins on established products.

Geopolitical Stability and Global Supply Chain Security

Trade tensions between the US, EU and China risk disrupting supply of APIs and intermediates; in 2024 global pharma trade volatility rose 12%, increasing procurement costs for firms like Gilead that sourced ~35% of APIs from Asia in 2023. Gilead’s network spans 20+ countries and remains sensitive to shifts in tariffs and export controls that can delay production. Strategic diversification—Gilead expanded capacity with a $500m investment in 2024 to add sites in Ireland and Singapore—mitigates regional political instability risks.

Government Funding for HIV and Hepatitis Initiatives

Public health budgets and programs like PEPFAR (FY2025 US appropriations ~$6.8bn) materially drive demand for Gilead antiviral sales, with PEPFAR and the Global Fund supporting procurement in >50 low- and middle-income countries.

Shifts in political leadership or fiscal priorities can cut yearly allocations—PEPFAR funding varied ±5–10% over past decade—creating revenue volatility for Gilead in key markets.

Maintaining access requires sustained advocacy and public-private partnerships; Gilead reported ~$1.2bn in global access investments in 2024 to secure procurement channels and tiered pricing.

Regulatory Alignment Across International Markets

Political cooperation on healthcare standards accelerates Gilead’s global launch of oncology and inflammation drugs; harmonized approvals cut time-to-market—EMA median approval 426 days vs FDA 303 days (2023), while China’s NMPA reforms reduced review times by ~20% in 2021–2023.

Divergent EU, US, China requirements raise compliance costs—Gilead reported R&D and licensing expenses of $6.2bn in FY2024—risking delayed revenue recognition and market fragmentation.

Gilead must align regulatory strategies across jurisdictions through parallel submissions and reliance pathways to optimize rollout and protect peak sales.

- FDA median approval 303 days (2023) vs EMA 426 days

- China NMPA review times down ~20% (2021–2023)

- Gilead R&D/licensing expenses $6.2bn FY2024

Taxation Policies and International Profit Repatriation

Corporate tax reforms in the US and the OECD two-pillar global minimum tax (15%) affect Gilead’s effective tax rate and cash repatriation strategies; Gilead reported a GAAP tax rate of 12% in 2024 but faces pressure to align with the 15% minimum, which could reduce tax planning opportunities and increase cash tax outflows.

Revisions to IP taxation—shift toward nexus-based and marketing-relief rules—can lower after-tax margins on overseas royalties; in 2024 Gilead booked ~30% of revenue outside the US, so changes materially affect net profitability by region.

Financial planners must model increased cash taxes and reduced BEPS-driven benefits when valuing Gilead; sensitivity scenarios shifting the effective tax rate by +3–6 percentage points can reduce FCFF and terminal value meaningfully for DCFs.

- 2024 GAAP tax rate: 12%

- OECD global minimum: 15%

- ~30% revenue from outside US (2024)

- Valuation sensitivity: +3–6 ppt tax rate → lower FCFF/terminal value

Gilead faces pricing, tax & supply risks—$13.5B antiviral revenue and margin pressure

Political actions—IRA Medicare negotiation, OECD 15% minimum tax, and trade/tariff shifts—threaten Gilead’s pricing, margins, and supply chain; IRA targets ~$13.5B antiviral revenue (2024), GAAP tax 12% vs OECD 15%, ~30% revenue outside US, and 35% APIs sourced from Asia (2023). Gilead’s $500m 2024 capacity spend and $1.2bn access investments partially mitigate risks while regulatory divergence raises R&D/compliance costs ($6.2bn FY2024).

| Metric | Value |

|---|---|

| Antiviral revenue at risk (2024) | $13.5B |

| GAAP tax rate (2024) | 12% |

| OECD minimum tax | 15% |

| Revenue outside US (2024) | ~30% |

| APIs from Asia (2023) | 35% |

| 2024 capacity investment | $500M |

| 2024 access investments | $1.2B |

| R&D/licensing expense (FY2024) | $6.2B |

What is included in the product

Explores how external macro-environmental factors uniquely affect Gilead Sciences across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform strategy, risk mitigation, and opportunity identification for executives and investors.

A concise, visually segmented PESTLE snapshot of Gilead Sciences that highlights regulatory, technological, and market risks for quick inclusion in decks or meeting briefs, with editable notes for regional or pipeline-specific context.

Economic factors

Impact of Global Interest Rate Environments

Persistent high US Federal Reserve rates (2024 year-end federal funds target 5.25–5.50%) and 10-year Treasury yields around 4.6% increase Gilead Sciences’ cost of debt, raising financing costs for oncology M&A and potentially reducing deal IRRs.

Higher rates make leverage pricier; Gilead’s net debt/EBITDA (about 1.5x FY2024) and $7–8bn annual cash flow projections shape its ability to fund acquisitions without excessive dilution.

Investors should monitor credit spreads and Fed guidance, as rate volatility can constrain deal size, push Gilead toward stock-based trades, or delay strategic expansion.

Currency Exchange Rate Volatility

With approximately 45% of 2024 revenue derived outside the US, Gilead faces material exposure to US dollar movements; a 10% dollar appreciation versus major currencies historically reduced reported international revenue by roughly 4–6% in prior periods.

Healthcare Budget Constraints and Payor Pressure

Economic downturns and 2024–25 austerity measures have tightened reimbursement: OECD government health spending growth slowed to 1.2% in 2024, prompting stricter payor reviews across Europe and parts of Asia.

Insurers now demand demonstrable long-term value; US private payors rejected or limited access to several high-cost cell therapies in 2024 after cost-effectiveness concerns.

Gilead must prove superior cost-effectiveness—health economic models showing lower lifetime costs or QALY gains versus standard care are increasingly required to secure coverage and favorable pricing.

Inflationary Pressure on Manufacturing and R&D Costs

Inflation has driven wages for specialized biotech talent up ~6-8% in 2024 and raw-material costs rise ~9% year-over-year, compressing Gilead’s operating margins unless drug prices or efficiency gains offset them.

The capital-intensive R&D budget is sensitive to inflation; a 5% CPI rise in 2024 can increase pipeline costs by hundreds of millions, affecting future approvals.

Operational efficiency and supply-chain optimization—including hedging energy and sourcing strategies—are essential to protect profitability.

- Specialized labor +6–8% (2024)

- Raw materials +9% YoY (2024)

- CPI impact ~5% raises pipeline costs materially

- Focus: supply-chain, energy hedging, operational efficiency

Consumer Purchasing Power in Emerging Markets

Rising middle classes in markets like India and Brazil—where middle-class consumption grew by ~3% CAGR 2015–2023 and middle-class populations reached ~300m and ~110m respectively in 2024—increase demand for Gilead’s antivirals and HIV treatments but affordability remains constrained.

Economic volatility, with 2023 GDP growth swings of ±2–4% in many EMs, can suppress uptake of high-cost chronic therapies, pressuring volumes and reimbursement timelines.

Tiered pricing and local manufacturing partnerships are essential; Gilead has used differential pricing in ~40+ LMICs and can expand such models to protect margins while boosting access.

- Rising middle class: India ~300m, Brazil ~110m (2024)

- EM GDP volatility: ±2–4% swings (2023)

- Tiered pricing used in 40+ LMICs

High US rates squeeze oncology M&A returns; FX and input inflation pressure growth

High US rates (Fed funds 5.25–5.50% end-2024) raise funding costs, pressuring oncology M&A returns; net debt/EBITDA ~1.5x and $7–8bn annual cash flow guide deal capacity. FX: ~45% revenue ex-US; a 10% USD appreciation cuts reported intl revenue ~4–6%. 2024: specialized labor +6–8%, raw materials +9% YoY; OECD health spending growth 1.2% tightening reimbursement; EM middle class: India ~300m, Brazil ~110m.

| Metric | 2024 Value |

|---|---|

| Fed funds | 5.25–5.50% |

| 10yr US Treasury | ~4.6% |

| Net debt/EBITDA | ~1.5x |

| Annual cash flow | $7–8bn |

| Revenue ex-US | ~45% |

| Labor inflation | +6–8% |

| Raw materials | +9% YoY |

| OECD health spend growth | 1.2% |

| India middle class | ~300m |

| Brazil middle class | ~110m |

Preview Before You Purchase

Gilead Sciences PESTLE Analysis

The preview shown here is the exact Gilead Sciences PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It includes the complete political, economic, social, technological, legal, and environmental assessment as displayed. No placeholders or teasers—this is the real, final document you’ll download immediately after payment. The content and structure are identical to the delivered file.