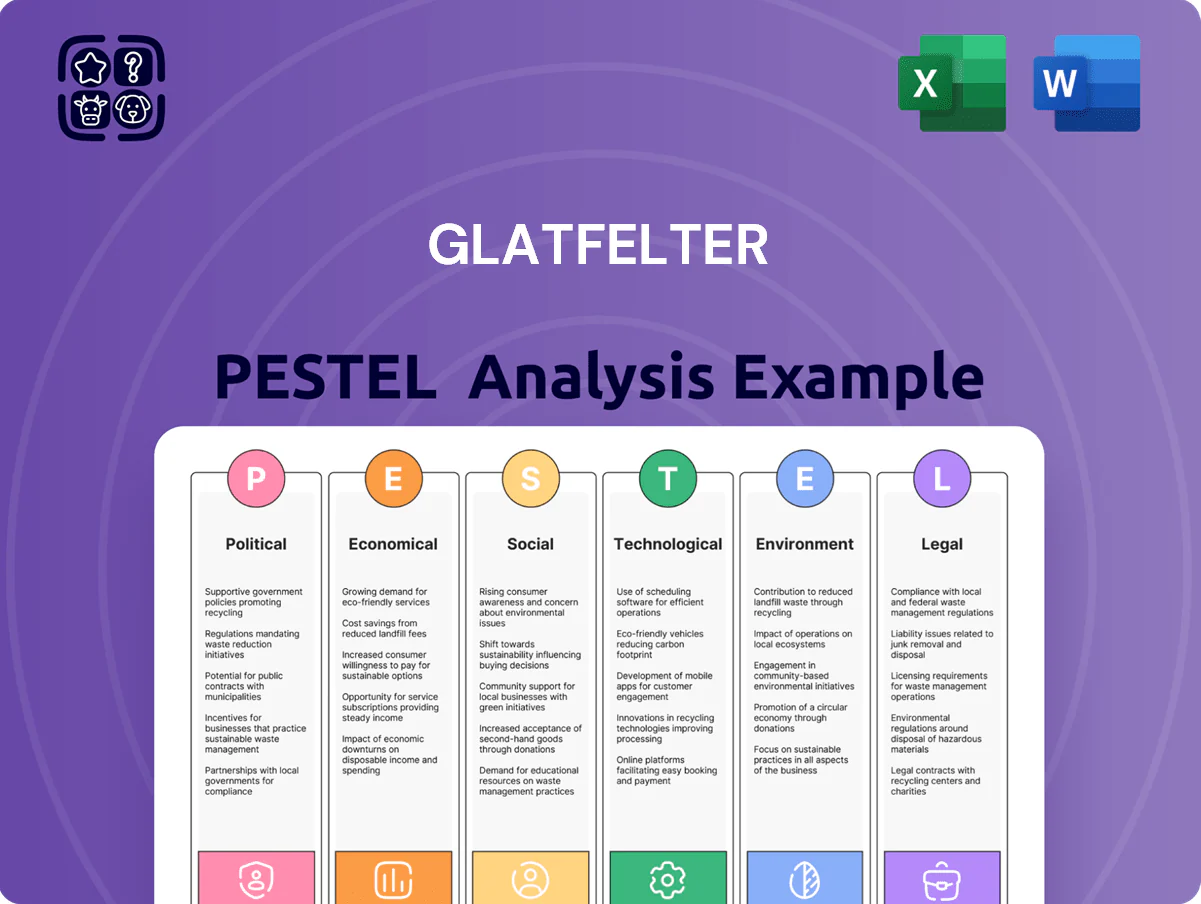

Glatfelter PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, supply-chain pressures, and rising sustainability standards are reshaping Glatfelter’s prospects—our concise PESTLE highlights the external forces investors and strategists must track; purchase the full, editable analysis for a complete, actionable roadmap you can use immediately.

Political factors

Global Trade Policy and Tariffs

Changes in US-EU-Asia trade agreements and tariffs affect Glatfelter’s export costs for specialty materials; US tariffs on certain paper/nonwoven inputs rose to 7.5–10% in 2024, lifting landed costs and squeezing margins.

As a global supplier, Glatfelter must navigate protectionist measures—2024 local-content rules in parts of Asia increased domestic sourcing by an estimated 5–8% for buyers, pressuring cross-border sales.

Analysts track these policy shifts to quantify potential cost inflation and supply-chain disruption risk; a 2024 scenario analysis by sell-side firms shows EBITDA downside of 3–6% under sustained tariff hikes.

Geopolitical Stability in Key Regions

Government Green Subsidies and Incentives

Post-Merger Regulatory Scrutiny

Post-merger scrutiny of Magnera after Glatfelter’s combination with Berry Global’s specialty business has drawn attention from antitrust authorities, with US and EU agencies reviewing market shares where Magnera now holds an estimated 18–22% share in select engineered materials segments as of 2025.

Ongoing political concern over concentration may constrain future M&A, given regulators have challenged deals exceeding 30% local market share and imposed remedies in 2023–2024 industrial transactions.

Executives must keep transparent regulator engagement, maintain compliance programs and provide timely divestiture or behavioral remedies to preserve operational freedom and avoid fines that in similar cases reached $50–200 million.

- Regulatory review: US and EU scrutiny active

- Market share: ~18–22% in key segments (2025)

- M&A constraints: heightened when deals push >30% share

- Risk: potential fines $50–200M; need for compliance

Public Health Policy Integration

Government mandates on hygiene and medical stockpiling drive steady demand for Glatfelter’s filtration and nonwoven hygiene products; U.S. federal stockpile expansions and EU procurement plans boosted medical material purchases by an estimated 8–12% in 2024, favoring suppliers with certified medical-grade capacity.

As governments prioritize pandemic preparedness, Glatfelter can pursue multi-year public contracts—U.S. government healthcare procurement exceeded $95 billion in 2024—creating predictable revenue streams for specialized nonwovens used in masks, gowns, and filters.

These policies establish a demand floor for healthcare-grade nonwovens, supporting Glatfelter’s capacity utilization and pricing power amid rising global healthcare spending, which reached about 10% of GDP on average across OECD countries in 2024.

- Government procurement growth 8–12% (2024)

- U.S. healthcare procurement ≈ $95B (2024)

- OECD average healthcare spend ≈ 10% of GDP (2024)

Tariffs, input shocks and subsidies squeeze EBITDA; Magnera at 18–22%—M&A risk if >30%

US/EU/Asia tariffs and local-content rules raised landed costs 7.5–10% (tariffs) and forced 5–8% domestic sourcing (2024), squeezing EBITDA by 3–6% in downside scenarios; Europe gas +28% YoY (2024) and pulp +22% (2023–24) raised input volatility. Subsidies/R&D credits ($45B+ programs 2024–25) lower transition CAPEX burden; Magnera holds ~18–22% share in segments (2025), M&A scrutiny tight if >30%—fines $50–200M.

| Metric | 2023–25 |

|---|---|

| Tariff increase | 7.5–10% |

| Local-content impact | +5–8% |

| Europe gas price change | +28% YoY (2024) |

| Pulp price change | +22% (2023–24) |

| Subsidy pool | $45B+ (2024–25) |

| Market share (Magnera) | 18–22% (2025) |

| M&A concern threshold | >30% market share |

| Potential fines | $50–200M |

What is included in the product

Explores how macro-environmental forces uniquely impact Glatfelter across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking scenarios to identify risks, opportunities, and strategic responses for executives, investors, and consultants.

Condenses Glatfelter's full PESTLE into a clean, shareable summary that’s visually segmented for quick interpretation, easily dropped into presentations, annotated for local context, and ideal for cross-team alignment during strategy or risk discussions.

Economic factors

Raw Material Price Volatility

Raw material price volatility—notably wood pulp, synthetic fibers, and resins—drives cost risk for Glatfelter; wood pulp rose about 22% year-over-year in 2024 while key resin prices surged 18% amid supply-chain bottlenecks, squeezing margins if costs cannot be passed on. Analysts monitor the S&P Global Pulp & Paper index and resin commodity indices to model input inflation impacts; a 10% input shock could cut adjusted operating margin by roughly 150–250 basis points based on 2024 cost structure.

Currency Exchange Rate Fluctuations

Operating across North America, Europe and Asia exposes Glatfelter to volatility in the USD, EUR and GBP; a 10% USD appreciation versus the EUR in 2023-24 would have reduced reported euro-denominated revenue by roughly 9% on cross-border sales. A stronger dollar raises export prices abroad and can compress international margins while revaluing foreign earnings downward. Robust hedging—forwards, options and natural hedges—remains essential to stabilize cash flows amid FX swings.

Interest Rate Impacts on Corporate Debt

Glatfelter's capital-intensive manufacturing and the substantial debt taken on during its 2024 merger make it highly sensitive to central bank moves; a 100 bps rise in rates would raise annual interest expense materially on its roughly $700 million of gross debt (2025 estimate). Higher rates compress free cash flow by increasing debt servicing and can delay investments in automation and deinking tech. Investors track Glatfelter's debt-to-equity (~1.1x in 2024) and interest coverage (EBIT/interest ~3.2x in 2024) to gauge resilience in a higher-rate regime.

Consumer Spending on Essential Goods

Consumer spending on essential goods like hygiene and food packaging is relatively recession-resistant, but during severe downturns consumers often trade down to private-label or lower-cost formats; US private-label penetration rose to 19.3% in 2023, signaling substitution risk for premium nonwoven demand.

Emerging-market GDP growth—IMF forecast 4.2% in 2024–25 for EMs—drives premium hygiene uptake, offering Glatfelter upside in specialty nonwovens used in higher-margin products.

Analysts track global GDP and consumer staples volumes; global GDP growth slowed to 3.1% in 2023, implying moderating but still positive demand outlook for specialty materials.

- Recession-resistant but vulnerable to trade-down (US private-label 19.3% in 2023)

- EM GDP ~4.2% (2024–25) supports premium hygiene adoption

- Global GDP 3.1% in 2023 moderates specialty nonwoven volume growth

Energy Cost Fluctuations in Manufacturing

Glatfelter's specialty papers and nonwovens are energy-intensive; in 2024 European electricity prices averaged about €120/MWh and TTF gas prices saw spikes to €60/MWh-equivalent, materially raising manufacturing unit costs.

Energy market shifts in Europe can change plant margins quickly; Glatfelter reported energy and raw material cost pressures contributing to margin compression in 2024.

Investing in efficiency—LEDs, heat recovery, CHP—reduces exposure; typical paybacks in the sector range 3–6 years, lowering sensitivity to volatile utility markets.

- High energy intensity makes costs a key margin driver

- 2024 EU power ~€120/MWh, gas surge to ~€60/MWh-eq

- Efficiency investments = 3–6 year payback, cut volatility risk

Cost, FX & Rate Pressures vs. EM Demand: Pulp +22%, Resins +18%, Debt ~$700M

Economic factors: input-cost volatility (wood pulp +22% YoY 2024; resins +18%), FX sensitivity (USD strength cuts EUR revenue ~9% per 10% move), rate exposure (≈$700M debt; debt/equity ~1.1x; interest coverage ~3.2x in 2024), resilient but trade-down risk (US private-label 19.3% 2023); EM GDP ~4.2% (2024–25) supports premium demand; EU power ~€120/MWh 2024.

| Metric | Value |

|---|---|

| Wood pulp (2024) | +22% YoY |

| Resins (2024) | +18% YoY |

| Debt (est) | $700M |

| Debt/Equity (2024) | ~1.1x |

| Interest coverage (2024) | ~3.2x |

| US private-label (2023) | 19.3% |

| EM GDP (2024–25) | ~4.2% |

| EU power (2024) | ~€120/MWh |

What You See Is What You Get

Glatfelter PESTLE Analysis

The preview shown here is the exact Glatfelter PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use without edits.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how political shifts, supply-chain pressures, and rising sustainability standards are reshaping Glatfelter’s prospects—our concise PESTLE highlights the external forces investors and strategists must track; purchase the full, editable analysis for a complete, actionable roadmap you can use immediately.

Political factors

Global Trade Policy and Tariffs

Changes in US-EU-Asia trade agreements and tariffs affect Glatfelter’s export costs for specialty materials; US tariffs on certain paper/nonwoven inputs rose to 7.5–10% in 2024, lifting landed costs and squeezing margins.

As a global supplier, Glatfelter must navigate protectionist measures—2024 local-content rules in parts of Asia increased domestic sourcing by an estimated 5–8% for buyers, pressuring cross-border sales.

Analysts track these policy shifts to quantify potential cost inflation and supply-chain disruption risk; a 2024 scenario analysis by sell-side firms shows EBITDA downside of 3–6% under sustained tariff hikes.

Geopolitical Stability in Key Regions

Government Green Subsidies and Incentives

Post-Merger Regulatory Scrutiny

Post-merger scrutiny of Magnera after Glatfelter’s combination with Berry Global’s specialty business has drawn attention from antitrust authorities, with US and EU agencies reviewing market shares where Magnera now holds an estimated 18–22% share in select engineered materials segments as of 2025.

Ongoing political concern over concentration may constrain future M&A, given regulators have challenged deals exceeding 30% local market share and imposed remedies in 2023–2024 industrial transactions.

Executives must keep transparent regulator engagement, maintain compliance programs and provide timely divestiture or behavioral remedies to preserve operational freedom and avoid fines that in similar cases reached $50–200 million.

- Regulatory review: US and EU scrutiny active

- Market share: ~18–22% in key segments (2025)

- M&A constraints: heightened when deals push >30% share

- Risk: potential fines $50–200M; need for compliance

Public Health Policy Integration

Government mandates on hygiene and medical stockpiling drive steady demand for Glatfelter’s filtration and nonwoven hygiene products; U.S. federal stockpile expansions and EU procurement plans boosted medical material purchases by an estimated 8–12% in 2024, favoring suppliers with certified medical-grade capacity.

As governments prioritize pandemic preparedness, Glatfelter can pursue multi-year public contracts—U.S. government healthcare procurement exceeded $95 billion in 2024—creating predictable revenue streams for specialized nonwovens used in masks, gowns, and filters.

These policies establish a demand floor for healthcare-grade nonwovens, supporting Glatfelter’s capacity utilization and pricing power amid rising global healthcare spending, which reached about 10% of GDP on average across OECD countries in 2024.

- Government procurement growth 8–12% (2024)

- U.S. healthcare procurement ≈ $95B (2024)

- OECD average healthcare spend ≈ 10% of GDP (2024)

Tariffs, input shocks and subsidies squeeze EBITDA; Magnera at 18–22%—M&A risk if >30%

US/EU/Asia tariffs and local-content rules raised landed costs 7.5–10% (tariffs) and forced 5–8% domestic sourcing (2024), squeezing EBITDA by 3–6% in downside scenarios; Europe gas +28% YoY (2024) and pulp +22% (2023–24) raised input volatility. Subsidies/R&D credits ($45B+ programs 2024–25) lower transition CAPEX burden; Magnera holds ~18–22% share in segments (2025), M&A scrutiny tight if >30%—fines $50–200M.

| Metric | 2023–25 |

|---|---|

| Tariff increase | 7.5–10% |

| Local-content impact | +5–8% |

| Europe gas price change | +28% YoY (2024) |

| Pulp price change | +22% (2023–24) |

| Subsidy pool | $45B+ (2024–25) |

| Market share (Magnera) | 18–22% (2025) |

| M&A concern threshold | >30% market share |

| Potential fines | $50–200M |

What is included in the product

Explores how macro-environmental forces uniquely impact Glatfelter across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking scenarios to identify risks, opportunities, and strategic responses for executives, investors, and consultants.

Condenses Glatfelter's full PESTLE into a clean, shareable summary that’s visually segmented for quick interpretation, easily dropped into presentations, annotated for local context, and ideal for cross-team alignment during strategy or risk discussions.

Economic factors

Raw Material Price Volatility

Raw material price volatility—notably wood pulp, synthetic fibers, and resins—drives cost risk for Glatfelter; wood pulp rose about 22% year-over-year in 2024 while key resin prices surged 18% amid supply-chain bottlenecks, squeezing margins if costs cannot be passed on. Analysts monitor the S&P Global Pulp & Paper index and resin commodity indices to model input inflation impacts; a 10% input shock could cut adjusted operating margin by roughly 150–250 basis points based on 2024 cost structure.

Currency Exchange Rate Fluctuations

Operating across North America, Europe and Asia exposes Glatfelter to volatility in the USD, EUR and GBP; a 10% USD appreciation versus the EUR in 2023-24 would have reduced reported euro-denominated revenue by roughly 9% on cross-border sales. A stronger dollar raises export prices abroad and can compress international margins while revaluing foreign earnings downward. Robust hedging—forwards, options and natural hedges—remains essential to stabilize cash flows amid FX swings.

Interest Rate Impacts on Corporate Debt

Glatfelter's capital-intensive manufacturing and the substantial debt taken on during its 2024 merger make it highly sensitive to central bank moves; a 100 bps rise in rates would raise annual interest expense materially on its roughly $700 million of gross debt (2025 estimate). Higher rates compress free cash flow by increasing debt servicing and can delay investments in automation and deinking tech. Investors track Glatfelter's debt-to-equity (~1.1x in 2024) and interest coverage (EBIT/interest ~3.2x in 2024) to gauge resilience in a higher-rate regime.

Consumer Spending on Essential Goods

Consumer spending on essential goods like hygiene and food packaging is relatively recession-resistant, but during severe downturns consumers often trade down to private-label or lower-cost formats; US private-label penetration rose to 19.3% in 2023, signaling substitution risk for premium nonwoven demand.

Emerging-market GDP growth—IMF forecast 4.2% in 2024–25 for EMs—drives premium hygiene uptake, offering Glatfelter upside in specialty nonwovens used in higher-margin products.

Analysts track global GDP and consumer staples volumes; global GDP growth slowed to 3.1% in 2023, implying moderating but still positive demand outlook for specialty materials.

- Recession-resistant but vulnerable to trade-down (US private-label 19.3% in 2023)

- EM GDP ~4.2% (2024–25) supports premium hygiene adoption

- Global GDP 3.1% in 2023 moderates specialty nonwoven volume growth

Energy Cost Fluctuations in Manufacturing

Glatfelter's specialty papers and nonwovens are energy-intensive; in 2024 European electricity prices averaged about €120/MWh and TTF gas prices saw spikes to €60/MWh-equivalent, materially raising manufacturing unit costs.

Energy market shifts in Europe can change plant margins quickly; Glatfelter reported energy and raw material cost pressures contributing to margin compression in 2024.

Investing in efficiency—LEDs, heat recovery, CHP—reduces exposure; typical paybacks in the sector range 3–6 years, lowering sensitivity to volatile utility markets.

- High energy intensity makes costs a key margin driver

- 2024 EU power ~€120/MWh, gas surge to ~€60/MWh-eq

- Efficiency investments = 3–6 year payback, cut volatility risk

Cost, FX & Rate Pressures vs. EM Demand: Pulp +22%, Resins +18%, Debt ~$700M

Economic factors: input-cost volatility (wood pulp +22% YoY 2024; resins +18%), FX sensitivity (USD strength cuts EUR revenue ~9% per 10% move), rate exposure (≈$700M debt; debt/equity ~1.1x; interest coverage ~3.2x in 2024), resilient but trade-down risk (US private-label 19.3% 2023); EM GDP ~4.2% (2024–25) supports premium demand; EU power ~€120/MWh 2024.

| Metric | Value |

|---|---|

| Wood pulp (2024) | +22% YoY |

| Resins (2024) | +18% YoY |

| Debt (est) | $700M |

| Debt/Equity (2024) | ~1.1x |

| Interest coverage (2024) | ~3.2x |

| US private-label (2023) | 19.3% |

| EM GDP (2024–25) | ~4.2% |

| EU power (2024) | ~€120/MWh |

What You See Is What You Get

Glatfelter PESTLE Analysis

The preview shown here is the exact Glatfelter PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use without edits.