Global Industrial PESTLE Analysis

Skip the Research. Get the Strategy.

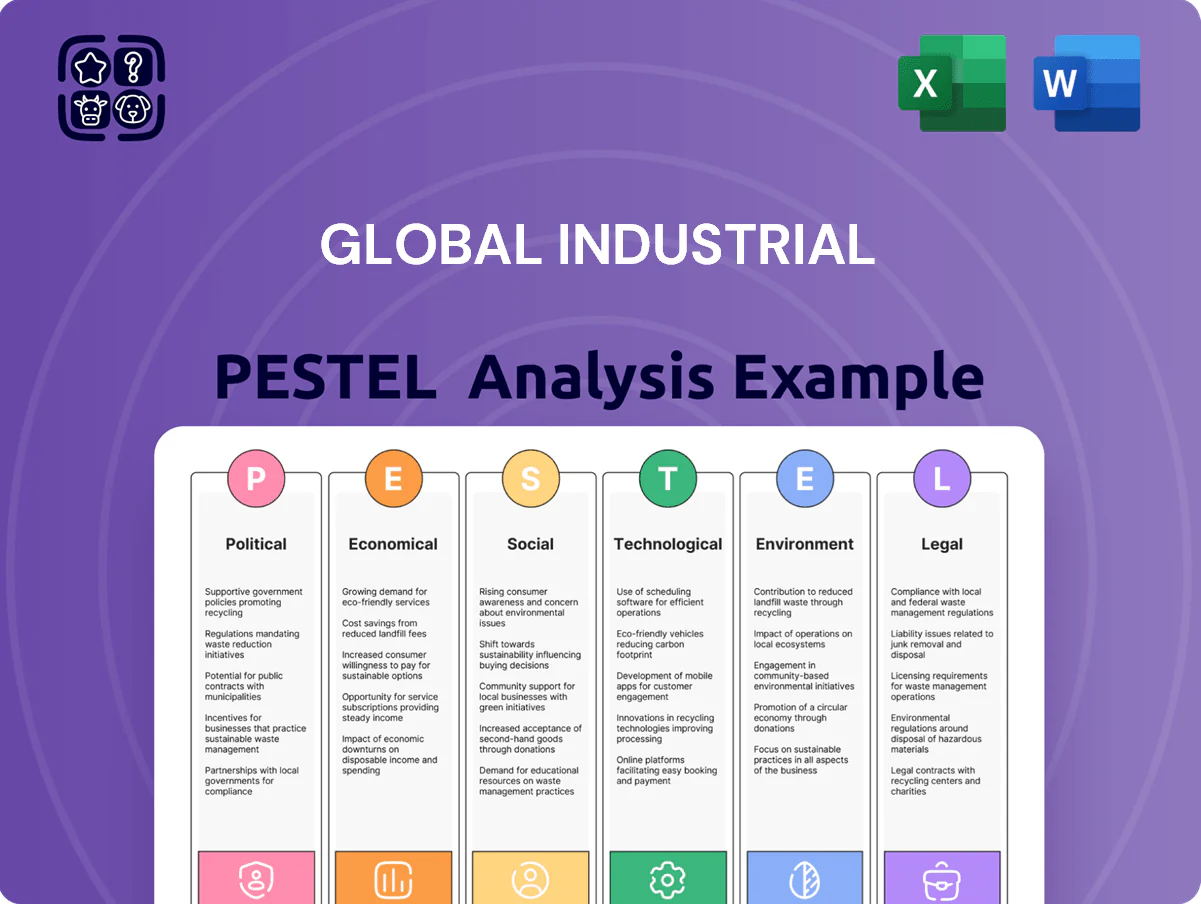

Navigate the forces reshaping Global Industrial with our concise PESTLE snapshot—covering political, economic, social, technological, legal, and environmental drivers that could alter its trajectory; purchase the full, editable PESTLE to access actionable insights, risk scenarios, and strategic recommendations tailored for investors and decision-makers.

Political factors

Trade Policy and Tariffs

The 2025 trade landscape shows volatile relations between Asia, EU and North American markets, with US steel tariffs at 25% and semiconductor-related duties up to 15% raising COGS for Global Industrial by an estimated 3–6% year-over-year.

Complex tariff schedules on imported electronics and industrial components have pushed input costs, prompting procurement to seek supplier diversification; 42% of firms report nearshoring plans for 2025 to reduce exposure.

Geopolitical friction and rising protectionism have increased supply-chain premium costs, squeezing margins and making tariff-aware sourcing and duty optimization critical to preserve EBITDA.

Infrastructure Investment Legislation

Government infrastructure spending, including the 2021 Bipartisan Infrastructure Law and $110B+ in 2024–2025 federal transportation allocations, continues to boost industrial distribution demand for material handling and safety equipment.

Late-stage implementation of projects through end-2025 keeps procurement cycles active; construction equipment orders rose ~8% YoY in 2024, sustaining aftermarket parts and safety gear demand.

State and federal allocations toward roads, bridges, and grid upgrades—estimated $200B+ in committed projects by 2025—create predictable multi-year revenue streams for suppliers in the sector.

Reshoring and Nearshoring Initiatives

Geopolitical Supply Chain Stability

Regional conflicts in the Red Sea and South China Sea have increased shipping insurance premiums by up to 40% in 2024, pressuring timely delivery across key maritime corridors and raising supply-risk for industrial inventory.

Political instability in major lanes forces higher inventory carrying costs—industry estimates show safety-stock increases of 12–18%—to preserve service levels for B2B customers of million-plus SKU catalogs.

Continuous monitoring of international relations is essential: container congestion spikes and rerouting in 2023–24 caused transit-time variances of 7–21 days, creating potential bottlenecks for large industrial assortments.

- Insurance premia +40% (2024)

- Safety-stock +12–18%

- Transit delays +7–21 days (2023–24)

- Million+ SKU catalogs require proactive geopolitical monitoring

Corporate Tax and Incentive Programs

Changes in corporate tax and green incentive policies at end-2025 shift capex: OECD average statutory corporate tax fell to 23.8% in 2025, while 45 countries expanded industrial green credits, boosting Global Industrial demand for HVAC and racking upgrades.

Tax credits for modernization raise reorder sizes—industrial HVAC and storage orders rose 12% YoY in 2025—while fiscal tightening risks a near-term 6–9% pullback in discretionary MRO spend.

- OECD avg tax rate 23.8% (2025)

- 45 countries expanded green credits (end-2025)

- HVAC/storage orders +12% YoY (2025)

- MRO discretionary spend risk −6–9% if tightened

Tariffs, insurance spikes and onshoring lift COGS, safety stock and MRO growth

Political risks—25% US steel tariffs, 15% semiconductor duties, 40% shipping insurance spike—have raised COGS ~3–6% and safety-stock +12–18%, while $200B+ infrastructure and $200–250B onshoring projects through 2025 sustain 6–8% regional MRO growth; OECD tax rate 23.8% and 45 countries' green credits drive HVAC/storage orders +12% YoY.

| Metric | Value |

|---|---|

| US steel tariff | 25% |

| Semiconductor duties | up to 15% |

| Insurance premia | +40% (2024) |

| Safety-stock | +12–18% |

| Infrastructure spend | $200B+ |

| Onshoring projects | $200–250B |

| OECD tax rate | 23.8% (2025) |

| HVAC/storage orders | +12% YoY (2025) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely shape the Global Industrial sector, with each category supported by current data and trend-driven sub-points to identify risks and opportunities.

A concise, visually segmented Global Industrial PESTLE summary that’s easy to drop into presentations or share across teams, enabling quick alignment on external risks and market positioning during planning sessions.

Economic factors

Industrial Production Trends

Industrial production rose 2.8% year-on-year through Q3 2025, signaling stronger MRO demand as manufacturing PMI averages climbed to 51.7 globally; higher output typically increases consumption of consumables and replacement parts across Global Industrial’s catalog.

Inflation and Pricing Power

Interest Rate Environment

The tightening interest rate environment at end-2025 — with global policy rates averaging about 4.5% and US Fed funds near 5.25% — raises SME borrowing costs, reducing affordability for large equipment purchases. Higher financing costs push some customers toward leasing or extending asset life via repairs; global leasing penetration rose ~6% in 2024–25 in logistics sectors. Global Industrial must shift sales to quantify multi-year ROI, TCO reductions, and financing alternatives to preserve demand.

Labor Market Costs

Rising wage expectations—US warehouse wages rose ~7% in 2024 versus 2021, with median hourly pay near $17—push operating expenses higher as competition for skilled logistics staff tightens globally.

Automation investment (robotics, sortation) is increasingly required: capital expenditure can cut labor hours per order by 30–50%, improving fulfillment speed and offsetting 8–12% annual wage inflation in tight markets.

Efficient human-capital management—cross-training, temp labor, and hybrid automation—remains critical to scale e-commerce while preserving margins amid labor shortages and rising personnel costs.

- Warehouse median hourly pay ≈ $17 (US, 2024)

- Wage growth ~7% since 2021

- Automation cuts labor hours/order 30–50%

- Typical wage inflation pressure 8–12% annually in tight markets

B2B E-commerce Growth

The shift to digital procurement is accelerating, with global B2B e-commerce sales projected to reach about $25 trillion in 2025, outpacing traditional channels; Global Industrial’s investment in its digital platform has driven double-digit online sales growth and greater market share. This reduces manual order-processing overhead—cutting fulfillment costs by an estimated 15–20%—and enables expansion into new geographies via scalable digital channels.

- Global B2B e-commerce ≈ $25T in 2025

- Global Industrial online sales growing double digits

- Fulfillment cost reductions ~15–20%

- Digital platform enables geographic expansion

Industrial growth, rising steel/petrochemicals, $25T B2B & automation slashing labor costs

Industrial output +2.8% YoY (Q3 2025); steel +18% and petrochemicals +22% (2024); input-driven COGS volatility +12% (2024); policy rates ~4.5% global, US Fed 5.25% (end-2025); US warehouse pay ≈ $17/hr, wages +7% since 2021; global B2B e-commerce ≈ $25T (2025); automation cuts labor/hr 30–50%.

| Metric | Value |

|---|---|

| Industrial output | +2.8% YoY |

| Steel | +18% YoY (2024) |

| Policy rates | ~4.5% global |

| B2B e‑commerce | $25T (2025) |

What You See Is What You Get

Global Industrial PESTLE Analysis

The preview shown here is the exact Global Industrial PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and insights visible in this preview are the same file you’ll download immediately after payment.

What you see is the finished product—actionable political, economic, social, technological, legal, and environmental analysis for strategic decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Navigate the forces reshaping Global Industrial with our concise PESTLE snapshot—covering political, economic, social, technological, legal, and environmental drivers that could alter its trajectory; purchase the full, editable PESTLE to access actionable insights, risk scenarios, and strategic recommendations tailored for investors and decision-makers.

Political factors

Trade Policy and Tariffs

The 2025 trade landscape shows volatile relations between Asia, EU and North American markets, with US steel tariffs at 25% and semiconductor-related duties up to 15% raising COGS for Global Industrial by an estimated 3–6% year-over-year.

Complex tariff schedules on imported electronics and industrial components have pushed input costs, prompting procurement to seek supplier diversification; 42% of firms report nearshoring plans for 2025 to reduce exposure.

Geopolitical friction and rising protectionism have increased supply-chain premium costs, squeezing margins and making tariff-aware sourcing and duty optimization critical to preserve EBITDA.

Infrastructure Investment Legislation

Government infrastructure spending, including the 2021 Bipartisan Infrastructure Law and $110B+ in 2024–2025 federal transportation allocations, continues to boost industrial distribution demand for material handling and safety equipment.

Late-stage implementation of projects through end-2025 keeps procurement cycles active; construction equipment orders rose ~8% YoY in 2024, sustaining aftermarket parts and safety gear demand.

State and federal allocations toward roads, bridges, and grid upgrades—estimated $200B+ in committed projects by 2025—create predictable multi-year revenue streams for suppliers in the sector.

Reshoring and Nearshoring Initiatives

Geopolitical Supply Chain Stability

Regional conflicts in the Red Sea and South China Sea have increased shipping insurance premiums by up to 40% in 2024, pressuring timely delivery across key maritime corridors and raising supply-risk for industrial inventory.

Political instability in major lanes forces higher inventory carrying costs—industry estimates show safety-stock increases of 12–18%—to preserve service levels for B2B customers of million-plus SKU catalogs.

Continuous monitoring of international relations is essential: container congestion spikes and rerouting in 2023–24 caused transit-time variances of 7–21 days, creating potential bottlenecks for large industrial assortments.

- Insurance premia +40% (2024)

- Safety-stock +12–18%

- Transit delays +7–21 days (2023–24)

- Million+ SKU catalogs require proactive geopolitical monitoring

Corporate Tax and Incentive Programs

Changes in corporate tax and green incentive policies at end-2025 shift capex: OECD average statutory corporate tax fell to 23.8% in 2025, while 45 countries expanded industrial green credits, boosting Global Industrial demand for HVAC and racking upgrades.

Tax credits for modernization raise reorder sizes—industrial HVAC and storage orders rose 12% YoY in 2025—while fiscal tightening risks a near-term 6–9% pullback in discretionary MRO spend.

- OECD avg tax rate 23.8% (2025)

- 45 countries expanded green credits (end-2025)

- HVAC/storage orders +12% YoY (2025)

- MRO discretionary spend risk −6–9% if tightened

Tariffs, insurance spikes and onshoring lift COGS, safety stock and MRO growth

Political risks—25% US steel tariffs, 15% semiconductor duties, 40% shipping insurance spike—have raised COGS ~3–6% and safety-stock +12–18%, while $200B+ infrastructure and $200–250B onshoring projects through 2025 sustain 6–8% regional MRO growth; OECD tax rate 23.8% and 45 countries' green credits drive HVAC/storage orders +12% YoY.

| Metric | Value |

|---|---|

| US steel tariff | 25% |

| Semiconductor duties | up to 15% |

| Insurance premia | +40% (2024) |

| Safety-stock | +12–18% |

| Infrastructure spend | $200B+ |

| Onshoring projects | $200–250B |

| OECD tax rate | 23.8% (2025) |

| HVAC/storage orders | +12% YoY (2025) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely shape the Global Industrial sector, with each category supported by current data and trend-driven sub-points to identify risks and opportunities.

A concise, visually segmented Global Industrial PESTLE summary that’s easy to drop into presentations or share across teams, enabling quick alignment on external risks and market positioning during planning sessions.

Economic factors

Industrial Production Trends

Industrial production rose 2.8% year-on-year through Q3 2025, signaling stronger MRO demand as manufacturing PMI averages climbed to 51.7 globally; higher output typically increases consumption of consumables and replacement parts across Global Industrial’s catalog.

Inflation and Pricing Power

Interest Rate Environment

The tightening interest rate environment at end-2025 — with global policy rates averaging about 4.5% and US Fed funds near 5.25% — raises SME borrowing costs, reducing affordability for large equipment purchases. Higher financing costs push some customers toward leasing or extending asset life via repairs; global leasing penetration rose ~6% in 2024–25 in logistics sectors. Global Industrial must shift sales to quantify multi-year ROI, TCO reductions, and financing alternatives to preserve demand.

Labor Market Costs

Rising wage expectations—US warehouse wages rose ~7% in 2024 versus 2021, with median hourly pay near $17—push operating expenses higher as competition for skilled logistics staff tightens globally.

Automation investment (robotics, sortation) is increasingly required: capital expenditure can cut labor hours per order by 30–50%, improving fulfillment speed and offsetting 8–12% annual wage inflation in tight markets.

Efficient human-capital management—cross-training, temp labor, and hybrid automation—remains critical to scale e-commerce while preserving margins amid labor shortages and rising personnel costs.

- Warehouse median hourly pay ≈ $17 (US, 2024)

- Wage growth ~7% since 2021

- Automation cuts labor hours/order 30–50%

- Typical wage inflation pressure 8–12% annually in tight markets

B2B E-commerce Growth

The shift to digital procurement is accelerating, with global B2B e-commerce sales projected to reach about $25 trillion in 2025, outpacing traditional channels; Global Industrial’s investment in its digital platform has driven double-digit online sales growth and greater market share. This reduces manual order-processing overhead—cutting fulfillment costs by an estimated 15–20%—and enables expansion into new geographies via scalable digital channels.

- Global B2B e-commerce ≈ $25T in 2025

- Global Industrial online sales growing double digits

- Fulfillment cost reductions ~15–20%

- Digital platform enables geographic expansion

Industrial growth, rising steel/petrochemicals, $25T B2B & automation slashing labor costs

Industrial output +2.8% YoY (Q3 2025); steel +18% and petrochemicals +22% (2024); input-driven COGS volatility +12% (2024); policy rates ~4.5% global, US Fed 5.25% (end-2025); US warehouse pay ≈ $17/hr, wages +7% since 2021; global B2B e-commerce ≈ $25T (2025); automation cuts labor/hr 30–50%.

| Metric | Value |

|---|---|

| Industrial output | +2.8% YoY |

| Steel | +18% YoY (2024) |

| Policy rates | ~4.5% global |

| B2B e‑commerce | $25T (2025) |

What You See Is What You Get

Global Industrial PESTLE Analysis

The preview shown here is the exact Global Industrial PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and insights visible in this preview are the same file you’ll download immediately after payment.

What you see is the finished product—actionable political, economic, social, technological, legal, and environmental analysis for strategic decision-making.