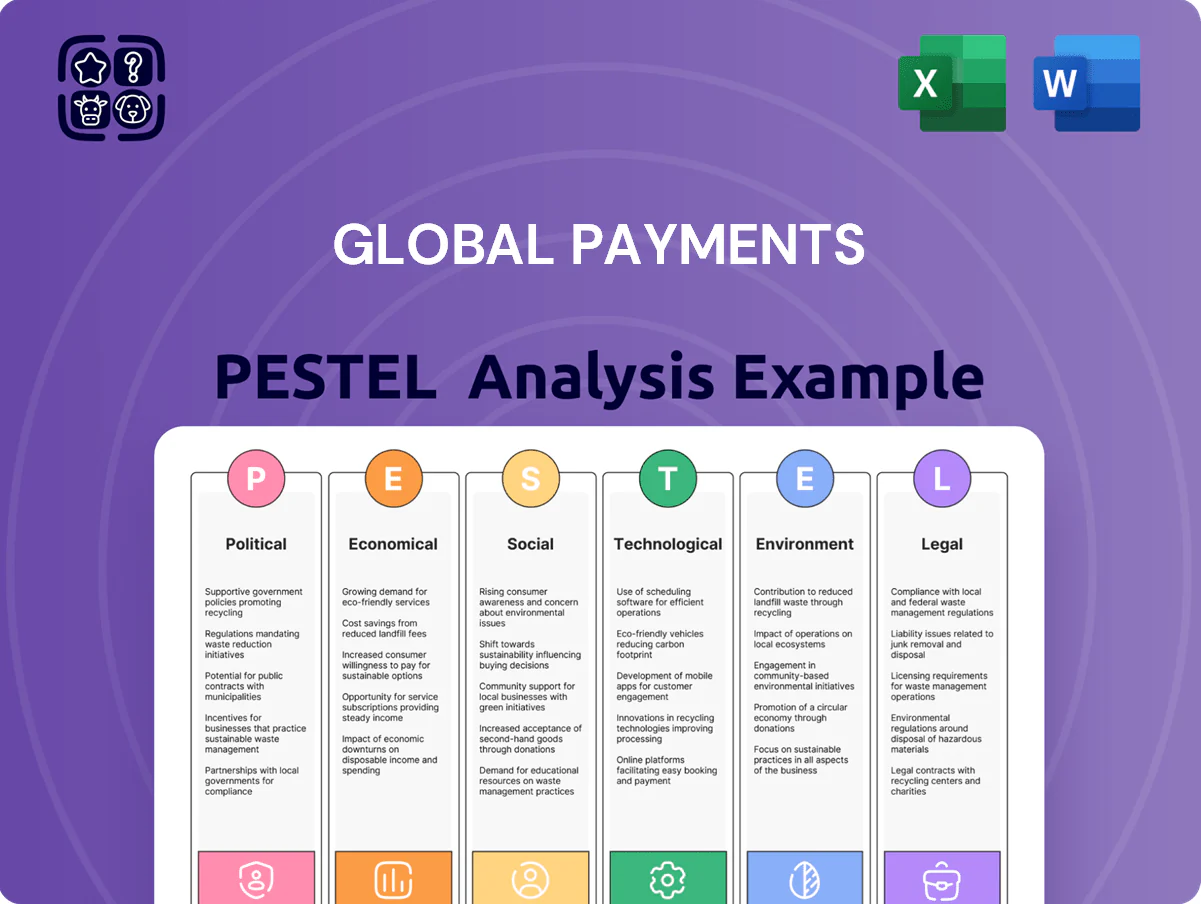

Global Payments PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and rapid fintech innovation are reshaping Global Payments' strategic outlook—our PESTLE distills these forces into concise, actionable insights. Purchase the full analysis for a complete breakdown of regulatory, social, and environmental risks and opportunities that investors, consultants, and executives rely on. Get instant access to ready-to-use findings and strengthen your strategic decisions today.

Political factors

Geopolitical instability and sanctions compliance

Ongoing geopolitical tensions in Eastern Europe and the Middle East through 2025 are reshaping trade corridors and sanctions regimes, with over 60 countries revising export controls and OFAC/UK sanctions lists expanding by ~12% in 2024; Global Payments must restrict services in sanctioned jurisdictions and adapt compliance controls. The firm faces heightened compliance costs—industry estimates suggest sanctions-related remediation can add 5–8% to operating expenses—and needs resilient risk frameworks. Sudden political shifts risk revenue disruption in high-exposure markets, where cross-border volumes fell ~7% year-over-year in affected corridors in 2024.

Government led digital payment initiatives

Many governments are pushing digital payments to cut shadow economies—India’s demonetization and UPI growth (UPI volumes rose to 83 billion transactions in 2024) improved tax compliance; similar mandates in Brazil and Indonesia expand real-time rails, requiring Global Payments to align tech and APIs with local specs.

Trade relations and cross border tariffs

Fluctuating trade relations among the US, China and EU directly affect cross-border volumes; global merchandise trade fell 0.9% in 2023 and recovered 2.7% in 2024, shifting payment flows and FX demand.

Tariff adjustments and new agreements change merchant net margins and cross-border fees—e.g., new EU digital services rules and US-China tariffs raised costs for some sectors by up to mid-single digits.

Global Payments must keep an agile footprint—diversifying processing hubs and issuer partnerships across regions to limit exposure to protectionist shocks and preserve transaction profitability.

National security and data sovereignty laws

National security and data sovereignty laws push countries to require that citizen financial data be stored and processed domestically, forcing Global Payments to deploy local data centers; estimates show data localization can raise CAPEX by 10–25% per market and increase operating costs by 5–15% annually.

Noncompliance risks license revocation and political backlash—recent 2024 actions in India and Brazil led to fines totaling over $120m across global payment firms—so adherence is essential to maintain market access.

- Data localization raises CAPEX 10–25% and OPEX 5–15%

- 2024 fines > $120m for noncompliance in major markets

- Local infrastructure increases operational complexity and regulatory oversight

Corporate tax policy shifts

Changes in corporate tax rates and treaties, including the OECD/G20 global minimum tax (Pillar Two) set at 15%, directly affect Global Payments’ net margins; Pillar Two compliance could raise its effective tax rate from recent levels (Global Payments reported an effective tax rate of ~17% in FY2024) and reduce EPS unless mitigated by credits.

As governments close deficits, tax burdens on high-growth fintechs are under review; over 140 jurisdictions had adopted or started implementing Pillar Two by end-2025, increasing compliance complexity and potential cash tax outflows.

Strategic tax planning, onshoring profits, and enhanced transparency in reporting are essential for Global Payments to manage its effective tax rate, sustain free cash flow (Global Payments generated $1.9bn operating cash flow in FY2024) and maintain investor confidence.

- OECD Pillar Two 15% global minimum tax impacts effective tax rates

- ~140 jurisdictions adopting Pillar Two by end-2025 raises compliance and cash tax risk

- Global Payments’ FY2024 effective tax rate ~17% and operating cash flow ~$1.9bn

- Strategic tax planning and transparent reporting critical to protect margins and investor trust

Political headwinds: rising sanctions, data-localization costs and Pillar Two squeeze margins

Political risks—sanctions expansion (~12% in 2024), data localization (CAPEX +10–25%, OPEX +5–15%), and Pillar Two (15%)—drive higher compliance costs, threaten market access (2024 fines >$120m) and pressure margins (effective tax ~17%, operating cash ~$1.9bn FY2024); Global Payments must diversify hubs, localize infrastructure, and strengthen tax and sanctions controls to sustain cross-border volumes (-7% in affected corridors 2024).

| Metric | Value |

|---|---|

| Sanctions expansion (2024) | ~12% |

| Data localization cost | CAPEX +10–25%, OPEX +5–15% |

| 2024 fines (payments firms) | >$120m |

| Pillar Two rate | 15% (adopted ~140 jurisdictions by end-2025) |

| Global Payments ETR FY2024 | ~17% |

What is included in the product

Explores how macro-environmental factors shape Global Payments across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights to identify risks and opportunities for executives, consultants, and investors.

A concise, visually segmented PESTLE summary for Global Payments that’s easy to drop into presentations or share across teams, enabling quick risk assessment, market positioning discussions, and customizable notes for region- or product-specific strategy sessions.

Economic factors

Global interest rate environment

By end-2025, stabilization of global policy rates around 4–5% in the US and 3–4% in major EMs raised weighted average cost of capital for fintech M&A and infrastructure, increasing financing costs by ~150–250 bps vs 2010s.

Higher rates lifted average US credit card APRs to ~20% (2025), dampening consumer discretionary spending and lowering Merchant Solutions volumes by an estimated 2–4% year-over-year in 2024–25.

Global Payments must optimize debt maturity profiles and cost of funds while allocating ~15–20% of annual EBITDA to reinvest in cloud, tokenization, and BNPL integrations to sustain growth.

Inflationary pressures on consumer spending

Persistent inflation in essentials—U.S. CPI at 3.4% y/y in 2025 and euro area HICP near 2.9%—squeezes discretionary spending, reducing retail and travel transaction volumes and pressuring Global Payments’ fee revenue.

Higher prices can lift nominal ticket sizes (average transaction value up 4–6% in 2024–25), but volume declines (retail footfall down ~2–5% in key markets) risk net revenue growth.

Global Payments tracks CPI, PCE and card-transaction volumes monthly to recalibrate pricing and roll out cost-focused merchant solutions for value-conscious clients.

Foreign exchange rate volatility

Ongoing FX volatility risks translating international earnings into US dollars: in 2024 FX moves widened reported revenue swings, with USD strength vs. EUR and GBP trimming cross-border net income by an estimated 1–3% for many global payment firms.

Expansion of the gig economy

The gig economy reached an estimated 162 million workers in the US and EU combined by 2024, driving demand for instant-payouts and payroll solutions; Global Payments’ Business and Consumer Solutions segment targets this need with APIs and pay-on-demand features that boost transaction volumes and ARR.

Serving non-traditional workers supports higher per-user software adoption and recurring fees—platform payouts and payroll services accounted for a growing share of merchant services revenue in 2024, reinforcing gig-driven growth.

- 162M gig workers (US+EU, 2024)

- Instant-payout demand raises transaction frequency and ARR

- Business & Consumer Solutions tailored to freelance payroll/APIs

Consolidation within the fintech sector

Economic pressures have driven fintech consolidation: venture funding to fintechs fell 56% in 2023 vs 2021 peak, pushing smaller firms to seek buyers while incumbents pursue tech acquisitions.

Global Payments targets strategic buys to bolster its software-led ecosystem, leveraging acquisitions to add payments, gateway and issuer services and drive cross-sell.

Consolidation yields economies of scale—Global Payments reported 2024 adjusted operating margin improvements after recent targets integration, expanding platform capabilities and reducing per-transaction costs.

- Fintech venture funding down 56% from 2021 peak

- Strategic acquisitions expand software and payment capabilities

- Economies of scale improve margins and lower transaction costs

Higher rates squeeze margins; gig boom fuels instant-payout demand

Rising policy rates (US ~4–5% 2025) and higher funding costs (+150–250bps vs 2010s) compress WACC; card APRs ~20% (2025) cut Merchant volumes 2–4% while nominal ticket sizes rose 4–6%; CPI: US 3.4% and euro area HICP 2.9% (2025); FX headwinds trimmed cross-border revenue ~1–3%; gig workforce ~162M (US+EU, 2024) boosts instant-payout demand.

| Metric | Value (2024–25) |

|---|---|

| US policy rate | 4–5% |

| Avg credit card APR | ~20% |

| US CPI | 3.4% y/y |

| Euro HICP | 2.9% y/y |

| Ticket size change | +4–6% |

| Volume change | -2–5% |

| Gig workers (US+EU) | 162M |

| Fintech VC funding drop vs 2021 | -56% |

Preview Before You Purchase

Global Payments PESTLE Analysis

The preview shown here is the exact Global Payments PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic cycles, and rapid fintech innovation are reshaping Global Payments' strategic outlook—our PESTLE distills these forces into concise, actionable insights. Purchase the full analysis for a complete breakdown of regulatory, social, and environmental risks and opportunities that investors, consultants, and executives rely on. Get instant access to ready-to-use findings and strengthen your strategic decisions today.

Political factors

Geopolitical instability and sanctions compliance

Ongoing geopolitical tensions in Eastern Europe and the Middle East through 2025 are reshaping trade corridors and sanctions regimes, with over 60 countries revising export controls and OFAC/UK sanctions lists expanding by ~12% in 2024; Global Payments must restrict services in sanctioned jurisdictions and adapt compliance controls. The firm faces heightened compliance costs—industry estimates suggest sanctions-related remediation can add 5–8% to operating expenses—and needs resilient risk frameworks. Sudden political shifts risk revenue disruption in high-exposure markets, where cross-border volumes fell ~7% year-over-year in affected corridors in 2024.

Government led digital payment initiatives

Many governments are pushing digital payments to cut shadow economies—India’s demonetization and UPI growth (UPI volumes rose to 83 billion transactions in 2024) improved tax compliance; similar mandates in Brazil and Indonesia expand real-time rails, requiring Global Payments to align tech and APIs with local specs.

Trade relations and cross border tariffs

Fluctuating trade relations among the US, China and EU directly affect cross-border volumes; global merchandise trade fell 0.9% in 2023 and recovered 2.7% in 2024, shifting payment flows and FX demand.

Tariff adjustments and new agreements change merchant net margins and cross-border fees—e.g., new EU digital services rules and US-China tariffs raised costs for some sectors by up to mid-single digits.

Global Payments must keep an agile footprint—diversifying processing hubs and issuer partnerships across regions to limit exposure to protectionist shocks and preserve transaction profitability.

National security and data sovereignty laws

National security and data sovereignty laws push countries to require that citizen financial data be stored and processed domestically, forcing Global Payments to deploy local data centers; estimates show data localization can raise CAPEX by 10–25% per market and increase operating costs by 5–15% annually.

Noncompliance risks license revocation and political backlash—recent 2024 actions in India and Brazil led to fines totaling over $120m across global payment firms—so adherence is essential to maintain market access.

- Data localization raises CAPEX 10–25% and OPEX 5–15%

- 2024 fines > $120m for noncompliance in major markets

- Local infrastructure increases operational complexity and regulatory oversight

Corporate tax policy shifts

Changes in corporate tax rates and treaties, including the OECD/G20 global minimum tax (Pillar Two) set at 15%, directly affect Global Payments’ net margins; Pillar Two compliance could raise its effective tax rate from recent levels (Global Payments reported an effective tax rate of ~17% in FY2024) and reduce EPS unless mitigated by credits.

As governments close deficits, tax burdens on high-growth fintechs are under review; over 140 jurisdictions had adopted or started implementing Pillar Two by end-2025, increasing compliance complexity and potential cash tax outflows.

Strategic tax planning, onshoring profits, and enhanced transparency in reporting are essential for Global Payments to manage its effective tax rate, sustain free cash flow (Global Payments generated $1.9bn operating cash flow in FY2024) and maintain investor confidence.

- OECD Pillar Two 15% global minimum tax impacts effective tax rates

- ~140 jurisdictions adopting Pillar Two by end-2025 raises compliance and cash tax risk

- Global Payments’ FY2024 effective tax rate ~17% and operating cash flow ~$1.9bn

- Strategic tax planning and transparent reporting critical to protect margins and investor trust

Political headwinds: rising sanctions, data-localization costs and Pillar Two squeeze margins

Political risks—sanctions expansion (~12% in 2024), data localization (CAPEX +10–25%, OPEX +5–15%), and Pillar Two (15%)—drive higher compliance costs, threaten market access (2024 fines >$120m) and pressure margins (effective tax ~17%, operating cash ~$1.9bn FY2024); Global Payments must diversify hubs, localize infrastructure, and strengthen tax and sanctions controls to sustain cross-border volumes (-7% in affected corridors 2024).

| Metric | Value |

|---|---|

| Sanctions expansion (2024) | ~12% |

| Data localization cost | CAPEX +10–25%, OPEX +5–15% |

| 2024 fines (payments firms) | >$120m |

| Pillar Two rate | 15% (adopted ~140 jurisdictions by end-2025) |

| Global Payments ETR FY2024 | ~17% |

What is included in the product

Explores how macro-environmental factors shape Global Payments across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights to identify risks and opportunities for executives, consultants, and investors.

A concise, visually segmented PESTLE summary for Global Payments that’s easy to drop into presentations or share across teams, enabling quick risk assessment, market positioning discussions, and customizable notes for region- or product-specific strategy sessions.

Economic factors

Global interest rate environment

By end-2025, stabilization of global policy rates around 4–5% in the US and 3–4% in major EMs raised weighted average cost of capital for fintech M&A and infrastructure, increasing financing costs by ~150–250 bps vs 2010s.

Higher rates lifted average US credit card APRs to ~20% (2025), dampening consumer discretionary spending and lowering Merchant Solutions volumes by an estimated 2–4% year-over-year in 2024–25.

Global Payments must optimize debt maturity profiles and cost of funds while allocating ~15–20% of annual EBITDA to reinvest in cloud, tokenization, and BNPL integrations to sustain growth.

Inflationary pressures on consumer spending

Persistent inflation in essentials—U.S. CPI at 3.4% y/y in 2025 and euro area HICP near 2.9%—squeezes discretionary spending, reducing retail and travel transaction volumes and pressuring Global Payments’ fee revenue.

Higher prices can lift nominal ticket sizes (average transaction value up 4–6% in 2024–25), but volume declines (retail footfall down ~2–5% in key markets) risk net revenue growth.

Global Payments tracks CPI, PCE and card-transaction volumes monthly to recalibrate pricing and roll out cost-focused merchant solutions for value-conscious clients.

Foreign exchange rate volatility

Ongoing FX volatility risks translating international earnings into US dollars: in 2024 FX moves widened reported revenue swings, with USD strength vs. EUR and GBP trimming cross-border net income by an estimated 1–3% for many global payment firms.

Expansion of the gig economy

The gig economy reached an estimated 162 million workers in the US and EU combined by 2024, driving demand for instant-payouts and payroll solutions; Global Payments’ Business and Consumer Solutions segment targets this need with APIs and pay-on-demand features that boost transaction volumes and ARR.

Serving non-traditional workers supports higher per-user software adoption and recurring fees—platform payouts and payroll services accounted for a growing share of merchant services revenue in 2024, reinforcing gig-driven growth.

- 162M gig workers (US+EU, 2024)

- Instant-payout demand raises transaction frequency and ARR

- Business & Consumer Solutions tailored to freelance payroll/APIs

Consolidation within the fintech sector

Economic pressures have driven fintech consolidation: venture funding to fintechs fell 56% in 2023 vs 2021 peak, pushing smaller firms to seek buyers while incumbents pursue tech acquisitions.

Global Payments targets strategic buys to bolster its software-led ecosystem, leveraging acquisitions to add payments, gateway and issuer services and drive cross-sell.

Consolidation yields economies of scale—Global Payments reported 2024 adjusted operating margin improvements after recent targets integration, expanding platform capabilities and reducing per-transaction costs.

- Fintech venture funding down 56% from 2021 peak

- Strategic acquisitions expand software and payment capabilities

- Economies of scale improve margins and lower transaction costs

Higher rates squeeze margins; gig boom fuels instant-payout demand

Rising policy rates (US ~4–5% 2025) and higher funding costs (+150–250bps vs 2010s) compress WACC; card APRs ~20% (2025) cut Merchant volumes 2–4% while nominal ticket sizes rose 4–6%; CPI: US 3.4% and euro area HICP 2.9% (2025); FX headwinds trimmed cross-border revenue ~1–3%; gig workforce ~162M (US+EU, 2024) boosts instant-payout demand.

| Metric | Value (2024–25) |

|---|---|

| US policy rate | 4–5% |

| Avg credit card APR | ~20% |

| US CPI | 3.4% y/y |

| Euro HICP | 2.9% y/y |

| Ticket size change | +4–6% |

| Volume change | -2–5% |

| Gig workers (US+EU) | 162M |

| Fintech VC funding drop vs 2021 | -56% |

Preview Before You Purchase

Global Payments PESTLE Analysis

The preview shown here is the exact Global Payments PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment decisions.