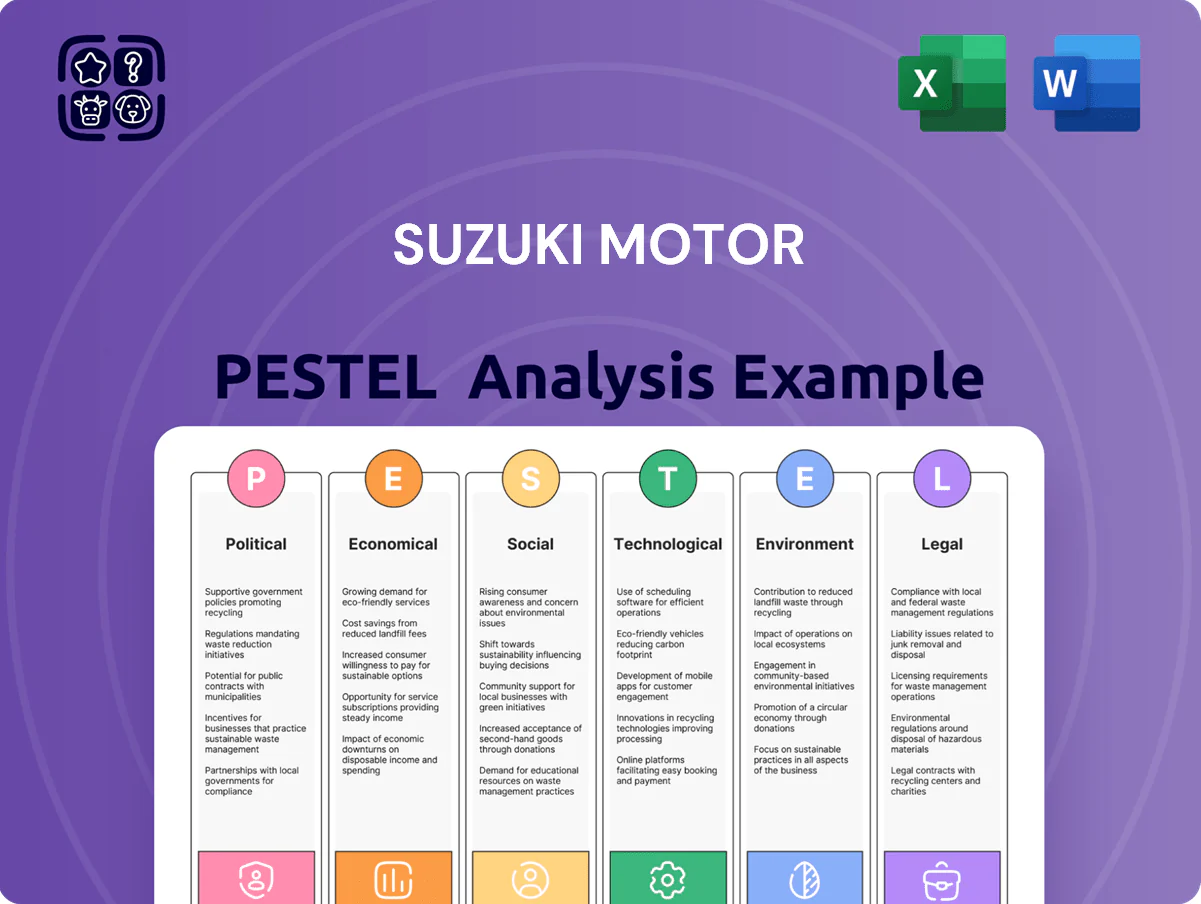

Suzuki Motor PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how political shifts, economic cycles, and technological innovation are shaping Suzuki Motor’s strategic outlook in our concise PESTLE snapshot — then unlock the full analysis for actionable insights, risk forecasts, and strategic recommendations tailored to investors and planners. Purchase the complete report to get the in-depth data and ready-to-use formats you need.

Political factors

Indo-Japanese strategic partnership

The deepening Indo-Japanese strategic partnership underpinned by 2023-25 agreements—including a 2023 $42.5 billion Japan-India investment corridor commitment—provides Suzuki stable geopolitical support for its India operations, notably Maruti Suzuki’s Gujarat and Suzuki Motor Gujarat (annual capacity ~750,000 units).

Geopolitical trade tensions

Rising protectionism and shifting trade alliances in Southeast Asia and Europe have pressured Suzuki’s export strategy, with ASEAN tariff negotiations and EU trade measures potentially affecting 30% of its FY2024 exports; EU auto tariffs discussions could raise costs by 2–4% per vehicle. Potential tariffs on imported components or finished vehicles force Suzuki to keep flexible supply chains and expand localized production—over 60% of Suzuki’s 2024 global production was already regional. Monitoring diplomatic ties between Japan and key partners (India, EU, ASEAN) is essential to sustain cost competitiveness and protect margins.

Indian regulatory environment

As Suzuki’s most critical market via Maruti Suzuki (FY2024 domestic market share ~49%), Indian federal and state policy shifts on automotive manufacturing directly affect production and margins; the PLI scheme (announced 2023, INR 25,938 crore for advanced auto components) and stricter local content rules increase capex and sourcing from local suppliers, impacting gross margins and ROIC, while India’s stable political environment supports execution of Suzuki’s Vision 2030 growth plans.

Global emission mandates

Global emission mandates push countries toward net-zero with EU ICE phase-out dates by 2035 and UK 2030 targets; Suzuki must reconcile these with markets like India, where ICE phase-out timelines are less defined.

EV subsidies and hybrid incentives—EU offering up to 9,000 euros in some markets and India reducing FAME subsidies—reshape margins and demand, affecting Suzuki’s R&D and pricing strategies.

- Suzuki faces divergent mandates: EU/UK strict (2030–2035) vs emerging markets slower

- EV subsidies vary: up to 9,000 euros in EU, FAME adjustments in India

- Policy shifts directly impact Suzuki’s product mix, CAPEX and competitive positioning

Regional stability in Africa

Suzuki is targeting Africa for growth, with vehicle sales in sub-Saharan Africa rising ~6% in 2024 and Nigeria/South Africa accounting for ~40% of regional auto demand, making political stability vital for investment returns.

Civil unrest, leadership changes, or sudden import-tariff hikes (Nigeria raised auto tariffs to 35% in 2023) can disrupt Suzuki’s distribution and increase landed costs.

Proactive engagement with governments, local partners, and risk monitoring is required to protect supply chains and a planned regional investment of ~$150–200 million over 2025–2027.

- Key risks: unrest, policy shifts, tariffs

- Exposure: Nigeria & South Africa ~40% regional demand

- Mitigation: local partnerships, government engagement, contingency funds

India-Japan $42.5B boost fuels Maruti/Suzuki growth; split EV/ICE play, Africa upside

Indo-Japan ties (2023 $42.5bn corridor) bolster Suzuki’s India capacity (~750k units at SMG); FY2024 Maruti domestic share ~49%. EU/UK ICE phase-outs (2030–2035) vs slower EM timelines force split EV/ICE strategy; FY2024 exports ~30% affected, potential tariff impact 2–4%/vehicle. Africa sales +6% (2024); Nigeria/South Africa ~40% regional demand. Planned regional capex $150–200m (2025–27).

| Metric | Value |

|---|---|

| Japan-India corridor | $42.5bn |

| SMG capacity | ~750,000 units |

| Maruti share FY2024 | ~49% |

| Exports affected | ~30% |

| Africa growth 2024 | +6% |

| Regional capex 2025–27 | $150–200m |

What is included in the product

Explores how external macro-environmental factors uniquely affect Suzuki Motor across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to highlight actionable threats and opportunities for executives, consultants, and investors.

A concise Suzuki Motor PESTLE snapshot that distills external risks and opportunities into actionable bullets for quick inclusion in presentations, shareable across teams, and editable with regional or business-specific notes.

Economic factors

Currency exchange fluctuations

As a Japanese multinational, Suzuki is highly sensitive to Yen volatility versus the US Dollar, Euro and Indian Rupee; a 10% Yen appreciation in 2024 would have reduced exporters' competitiveness, while in FY2024 Suzuki reported ¥1,200 billion exposure to foreign-currency translation risks. Significant currency swings affect imported component costs and export pricing—India operations (over 50% of group volumes) saw rupee volatility of ±6% in 2024. Suzuki uses forward contracts, options and natural hedges plus localized sourcing—India procurement rose to 78% local content in 2024—to buffer macroeconomic pressures.

Interest rate environment

Global central bank policies and fluctuating interest rates directly influence Suzuki's consumer purchasing power and vehicle financing costs; after 2022–2023 rate hikes, average auto loan rates in the US rose from ~5% to ~9% by 2024, tightening demand. High rates in key markets such as the EU and India can slow passenger car and motorcycle sales as monthly payments rise—Japan's household interest-sensitive auto purchases fell ~4% in 2024. Conversely, low-rate periods spur credit-driven retail growth and corporate fleet expansion, with global fleet orders up ~6% in 2023 when financing eased.

Inflation and raw material costs

Rising costs for steel, aluminum and platinum-group metals—steel up ~18% and aluminium ~14% in 2024 vs 2022, and palladium/platnium averaging a 22% year-on-year rise—are squeezing Suzuki’s margins, contributing to COGS pressure amid global commodity volatility.

Inflation elevated average manufacturing wage growth to roughly 6–8% in key hubs in 2024, forcing Suzuki to push continuous productivity gains and automation investments to offset labor-driven cost inflation.

To protect margins Suzuki faces the trade-off of modest retail price increases—recent regional hikes of 2–4%—while preserving its brand promise of affordability and value to avoid volume erosion.

Economic growth in India

- India GDP growth: 7.2% (FY2023–24), est 6.5%–7.0% (2024–25)

- Suzuki market share: ~50% of India PV market

- Per capita real GDP growth ~5% YoY (2023)

- Concentration risk: India-centric revenue exposure

Global supply chain resilience

Economic disruptions in global logistics and semiconductor shortages reduced Suzuki’s 2024 production by an estimated 5-7%, delaying deliveries and increasing lead times across key markets.

Suzuki’s inventory management and just-in-time processes are pivotal: maintaining buffer stocks lifted component availability to ~92% in FY2024 versus ~85% in 2022.

Strategic investments in supplier diversification and regional sourcing reduced localized bottleneck impact, trimming supply-related downtime by roughly 30% in 2024.

- 2024 production hit -5–7% from supply issues

- Component availability improved to ~92% in FY2024

- Diversification cut downtime ~30% in 2024

Suzuki margins squeezed: yen risk, commodity inflation & supply shocks force hedges

Yen volatility (¥1,200bn FX exposure FY2024), India-centered revenue (~50% PV share; GDP 7.2% FY23–24), commodity inflation (steel +18% vs 2022), higher financing costs (US loan rates ~9% 2024) and supply shocks (production -5–7% 2024) compress Suzuki margins, driving hedging, local sourcing (India local content 78%) and modest price rises (2–4%) to protect profitability.

| Metric | 2024 |

|---|---|

| FX exposure | ¥1,200bn |

| India GDP | 7.2% |

| India PV share | ~50% |

| Prod. impact | -5–7% |

Same Document Delivered

Suzuki Motor PESTLE Analysis

The preview shown here is the exact Suzuki Motor PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how political shifts, economic cycles, and technological innovation are shaping Suzuki Motor’s strategic outlook in our concise PESTLE snapshot — then unlock the full analysis for actionable insights, risk forecasts, and strategic recommendations tailored to investors and planners. Purchase the complete report to get the in-depth data and ready-to-use formats you need.

Political factors

Indo-Japanese strategic partnership

The deepening Indo-Japanese strategic partnership underpinned by 2023-25 agreements—including a 2023 $42.5 billion Japan-India investment corridor commitment—provides Suzuki stable geopolitical support for its India operations, notably Maruti Suzuki’s Gujarat and Suzuki Motor Gujarat (annual capacity ~750,000 units).

Geopolitical trade tensions

Rising protectionism and shifting trade alliances in Southeast Asia and Europe have pressured Suzuki’s export strategy, with ASEAN tariff negotiations and EU trade measures potentially affecting 30% of its FY2024 exports; EU auto tariffs discussions could raise costs by 2–4% per vehicle. Potential tariffs on imported components or finished vehicles force Suzuki to keep flexible supply chains and expand localized production—over 60% of Suzuki’s 2024 global production was already regional. Monitoring diplomatic ties between Japan and key partners (India, EU, ASEAN) is essential to sustain cost competitiveness and protect margins.

Indian regulatory environment

As Suzuki’s most critical market via Maruti Suzuki (FY2024 domestic market share ~49%), Indian federal and state policy shifts on automotive manufacturing directly affect production and margins; the PLI scheme (announced 2023, INR 25,938 crore for advanced auto components) and stricter local content rules increase capex and sourcing from local suppliers, impacting gross margins and ROIC, while India’s stable political environment supports execution of Suzuki’s Vision 2030 growth plans.

Global emission mandates

Global emission mandates push countries toward net-zero with EU ICE phase-out dates by 2035 and UK 2030 targets; Suzuki must reconcile these with markets like India, where ICE phase-out timelines are less defined.

EV subsidies and hybrid incentives—EU offering up to 9,000 euros in some markets and India reducing FAME subsidies—reshape margins and demand, affecting Suzuki’s R&D and pricing strategies.

- Suzuki faces divergent mandates: EU/UK strict (2030–2035) vs emerging markets slower

- EV subsidies vary: up to 9,000 euros in EU, FAME adjustments in India

- Policy shifts directly impact Suzuki’s product mix, CAPEX and competitive positioning

Regional stability in Africa

Suzuki is targeting Africa for growth, with vehicle sales in sub-Saharan Africa rising ~6% in 2024 and Nigeria/South Africa accounting for ~40% of regional auto demand, making political stability vital for investment returns.

Civil unrest, leadership changes, or sudden import-tariff hikes (Nigeria raised auto tariffs to 35% in 2023) can disrupt Suzuki’s distribution and increase landed costs.

Proactive engagement with governments, local partners, and risk monitoring is required to protect supply chains and a planned regional investment of ~$150–200 million over 2025–2027.

- Key risks: unrest, policy shifts, tariffs

- Exposure: Nigeria & South Africa ~40% regional demand

- Mitigation: local partnerships, government engagement, contingency funds

India-Japan $42.5B boost fuels Maruti/Suzuki growth; split EV/ICE play, Africa upside

Indo-Japan ties (2023 $42.5bn corridor) bolster Suzuki’s India capacity (~750k units at SMG); FY2024 Maruti domestic share ~49%. EU/UK ICE phase-outs (2030–2035) vs slower EM timelines force split EV/ICE strategy; FY2024 exports ~30% affected, potential tariff impact 2–4%/vehicle. Africa sales +6% (2024); Nigeria/South Africa ~40% regional demand. Planned regional capex $150–200m (2025–27).

| Metric | Value |

|---|---|

| Japan-India corridor | $42.5bn |

| SMG capacity | ~750,000 units |

| Maruti share FY2024 | ~49% |

| Exports affected | ~30% |

| Africa growth 2024 | +6% |

| Regional capex 2025–27 | $150–200m |

What is included in the product

Explores how external macro-environmental factors uniquely affect Suzuki Motor across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to highlight actionable threats and opportunities for executives, consultants, and investors.

A concise Suzuki Motor PESTLE snapshot that distills external risks and opportunities into actionable bullets for quick inclusion in presentations, shareable across teams, and editable with regional or business-specific notes.

Economic factors

Currency exchange fluctuations

As a Japanese multinational, Suzuki is highly sensitive to Yen volatility versus the US Dollar, Euro and Indian Rupee; a 10% Yen appreciation in 2024 would have reduced exporters' competitiveness, while in FY2024 Suzuki reported ¥1,200 billion exposure to foreign-currency translation risks. Significant currency swings affect imported component costs and export pricing—India operations (over 50% of group volumes) saw rupee volatility of ±6% in 2024. Suzuki uses forward contracts, options and natural hedges plus localized sourcing—India procurement rose to 78% local content in 2024—to buffer macroeconomic pressures.

Interest rate environment

Global central bank policies and fluctuating interest rates directly influence Suzuki's consumer purchasing power and vehicle financing costs; after 2022–2023 rate hikes, average auto loan rates in the US rose from ~5% to ~9% by 2024, tightening demand. High rates in key markets such as the EU and India can slow passenger car and motorcycle sales as monthly payments rise—Japan's household interest-sensitive auto purchases fell ~4% in 2024. Conversely, low-rate periods spur credit-driven retail growth and corporate fleet expansion, with global fleet orders up ~6% in 2023 when financing eased.

Inflation and raw material costs

Rising costs for steel, aluminum and platinum-group metals—steel up ~18% and aluminium ~14% in 2024 vs 2022, and palladium/platnium averaging a 22% year-on-year rise—are squeezing Suzuki’s margins, contributing to COGS pressure amid global commodity volatility.

Inflation elevated average manufacturing wage growth to roughly 6–8% in key hubs in 2024, forcing Suzuki to push continuous productivity gains and automation investments to offset labor-driven cost inflation.

To protect margins Suzuki faces the trade-off of modest retail price increases—recent regional hikes of 2–4%—while preserving its brand promise of affordability and value to avoid volume erosion.

Economic growth in India

- India GDP growth: 7.2% (FY2023–24), est 6.5%–7.0% (2024–25)

- Suzuki market share: ~50% of India PV market

- Per capita real GDP growth ~5% YoY (2023)

- Concentration risk: India-centric revenue exposure

Global supply chain resilience

Economic disruptions in global logistics and semiconductor shortages reduced Suzuki’s 2024 production by an estimated 5-7%, delaying deliveries and increasing lead times across key markets.

Suzuki’s inventory management and just-in-time processes are pivotal: maintaining buffer stocks lifted component availability to ~92% in FY2024 versus ~85% in 2022.

Strategic investments in supplier diversification and regional sourcing reduced localized bottleneck impact, trimming supply-related downtime by roughly 30% in 2024.

- 2024 production hit -5–7% from supply issues

- Component availability improved to ~92% in FY2024

- Diversification cut downtime ~30% in 2024

Suzuki margins squeezed: yen risk, commodity inflation & supply shocks force hedges

Yen volatility (¥1,200bn FX exposure FY2024), India-centered revenue (~50% PV share; GDP 7.2% FY23–24), commodity inflation (steel +18% vs 2022), higher financing costs (US loan rates ~9% 2024) and supply shocks (production -5–7% 2024) compress Suzuki margins, driving hedging, local sourcing (India local content 78%) and modest price rises (2–4%) to protect profitability.

| Metric | 2024 |

|---|---|

| FX exposure | ¥1,200bn |

| India GDP | 7.2% |

| India PV share | ~50% |

| Prod. impact | -5–7% |

Same Document Delivered

Suzuki Motor PESTLE Analysis

The preview shown here is the exact Suzuki Motor PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decision-making.