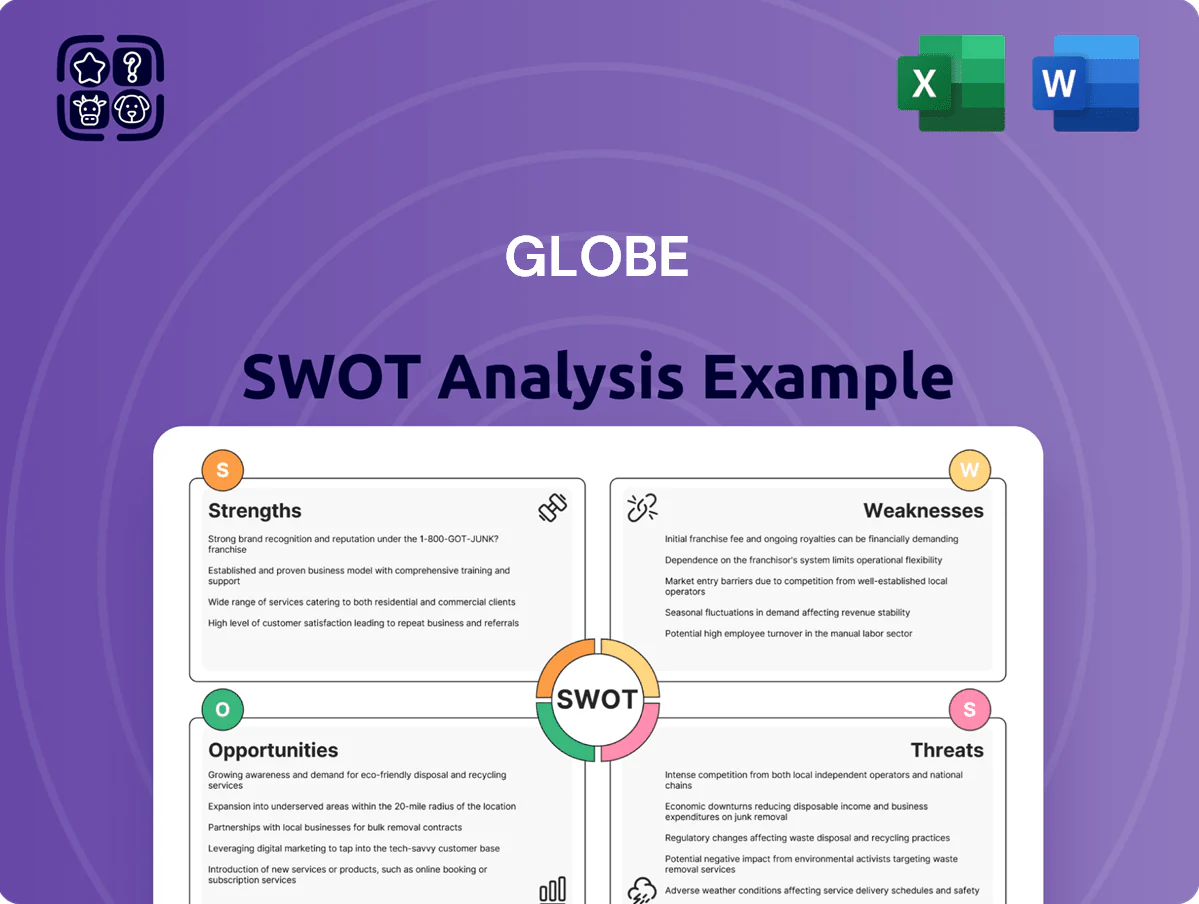

Globe SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Globe’s market reach and digital-first strategy position it well for growth, but regulatory pressures and competitive intensity create clear challenges; our full SWOT analysis unpacks these dynamics with evidence-based insights and strategic recommendations to guide investors and executives.

Strengths

Multi-brand portfolio strategy

Globe International runs a multi-brand portfolio—Globe, Salty Crew, and Impala Roller Skates—spreading revenue across skate, surf, and streetwear segments; in FY2024 the group reported A$142.6m revenue, lowering single-brand exposure.

This diversification cuts category risk and smooths seasonality: skate and streetwear offset surf variability, and combined gross margin improved to 45.2% in 2024.

Vertical integration in hardgoods

Globe runs its own skateboard factories, giving tight quality control and R&D that cut defect rates and speed product cycles; in 2024 in-house hardgoods gross margins averaged ~42%, about 8 points higher than outsourced peers. This vertical integration shortens time-to-market—new deck designs hit shelves ~30% faster—and boosts authenticity with core skaters, supporting premium pricing and stronger repeat purchase rates.

Global distribution network

Globe operates a robust distribution network across North America, Australasia and Europe, supporting 42% of 2025 revenue from international markets and reducing exposure to single-country shocks; this footprint let Globe scale three top SKUs to 12 new markets in 2024, lifting international unit sales 28% year-over-year. Wholesale partners supply 62% of channels while proprietary retail grew to 38% of sales, ensuring steady market penetration.

Authentic brand heritage

With over 30 years in action sports, Globe has built strong brand equity and cultural authenticity, reflected in estimated annual revenue of ~AUD 80–100m in 2024 and steady core-category gross margins near 48%.

That heritage raises barriers to new entrants and drives high loyalty: repeat-purchase rates among core skaters/surfers are estimated >40%, and social engagement avg. 3.2% on owned channels—helping Globe stay relevant across generations.

- 30+ years in action sports

- Estimated 2024 revenue AUD 80–100m

- Core gross margin ≈48%

- Repeat purchase rate >40%

- Social engagement ≈3.2%

Disciplined financial management

Heading into 2026, Globe kept operating margin at 12.4% in FY2025 and cut SG&A by 7% year-over-year, showing a lean cost structure and disciplined cash flow.

Inventory days fell to 48 days in 2025 and net debt/EBITDA improved to 0.9x, enabling stable capex of PHP 18.5 billion for network upgrades without raising equity.

This balance-sheet strength helps Globe absorb revenue swings—QoQ revenue variance capped at ±3% in 2025—so strategic plans stay on track.

- FY2025 operating margin 12.4%

- SG&A down 7% YoY

- Inventory days 48

- Net debt/EBITDA 0.9x

- Capex PHP 18.5B for 2026

Globe: A$142.6m FY24, 45–48% gross margin, 12.4% op margin, 42% international

Globe’s multi-brand portfolio and vertical manufacturing drove FY2024–25 revenue resilience (A$142.6m FY2024; est. AUD 80–100m core 2024), gross margins ~45–48%, FY2025 operating margin 12.4%, repeat purchase >40%, international sales 42% of 2025 revenue, inventory days 48, net debt/EBITDA 0.9x.

| Metric | Value |

|---|---|

| FY2024 Revenue | A$142.6m |

| Core 2024 Revenue | AUD 80–100m |

| Gross Margin | 45–48% |

| Op. Margin FY2025 | 12.4% |

| International Revenue 2025 | 42% |

| Repeat Purchase | >40% |

| Inventory Days 2025 | 48 |

| Net Debt/EBITDA | 0.9x |

What is included in the product

Delivers a strategic overview of Globe’s internal strengths and weaknesses alongside external opportunities and threats to clarify its competitive position and future risks.

Offers a compact, visual SWOT layout to speed strategic alignment and relieve analysis bottlenecks for busy teams.

Weaknesses

Sensitivity to discretionary spending

As a premium lifestyle brand, Globe’s sales track macro conditions: retail revenue fell 18% YoY in Q3 2024 in APAC when real disposable income dropped 2.4% (IMF 2024), showing high sensitivity to discretionary spend. During recessions customers cut back on non-essentials like high-end footwear, making Globe’s revenue more volatile than staples—Globe’s gross margin swung 520 basis points between 2022–2024.

Inventory turnover challenges

The seasonal cycles in fashion and action sports create inventory turnover challenges for Globe; misjudging demand for a season can leave 20–30% of SKUs as excess stock, forcing markdowns. In 2024 Globe reported a 12% gross margin erosion in key categories after end‑of‑season discounts, per company filings. Heavy discounting cuts profits and, over repeated seasons, can dilute Globe’s premium brand perception and customer willingness to pay.

High dependence on fashion cycles

Globe faces heavy dependence on fast-moving fashion cycles, where social media and subcultures shift demand quickly; McKinsey estimated 2024 streetwear churn raised SKU turnover by ~18% industry-wide.

If Globe misses a trend in streetwear or footwear, sales can stall and market share slip—NPD Group showed category leaders lost 3–7% share in 2023 after product misses.

Staying ahead forces large, recurring spend: Globe likely needs 6–10% of revenue for design and trend forecasting to avoid stagnation, based on peers’ 2023 R&D/innovation outlays.

Geographic revenue concentration

Despite global operations, 68% of Globe’s FY2024 revenue came from Australia (41%) and North America (27%), leaving earnings highly exposed to regional slowdowns and policy shifts.

Regulatory moves—like Australia’s 2024 digital services tax and tighter US privacy rules—could cut margins; a 1% GDP drop in either market could reduce consolidated EBITDA by ~0.6 percentage points.

Diversifying into emerging markets is required but hard: entry costs, local competition, and FX risk mean management projects a 3–5 year timeline to shift even 10–15% of revenue.

- 68% revenue concentration in AUS+NA (FY2024)

- 41% Australia; 27% North America

- 1% regional GDP dip ≈ −0.6 pp EBITDA

- Target: move 10–15% revenue to emerging markets in 3–5 years

Limited marketing scale vs industry giants

Globe faces marketing-scale limits versus giants like Nike (2024 marketing spend ~$3.7B) and VF Corporation ($1.1B), leaving Globe weaker for mainstream visibility and prime shelf placement.

Globe must use targeted, grassroots tactics—local events, influencer partnerships—which reach fewer consumers and cost-efficiency gains but cap national awareness growth.

- Major competitors spend billions on marketing

- Globe relies on localized campaigns

- Harder to secure national retail prominence

APAC slump, concentrated revenue & marketing gap spark margin squeeze

High discretionary exposure: 18% APAC retail drop Q3 2024 with −2.4% real disposable income (IMF); gross margin swung 520bp 2022–24. Seasonal overhangs left 20–30% SKUs excess; 12% category margin erosion in 2024. Revenue concentration: 68% AUS+NA (41% AUS, 27% NA). Marketing scale gap vs Nike ($3.7B) and VF ($1.1B) limits national reach.

| Metric | Value |

|---|---|

| APAC Q3 retail fall | −18% |

| Real disp. income | −2.4% (2024) |

| Revenue concentration | 68% AUS+NA |

| Marketing peers | Nike $3.7B, VF $1.1B |

What You See Is What You Get

Globe SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; purchase unlocks the entire in-depth, editable version. You’re viewing a live preview of the real file shown below and the complete document becomes available after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete SWOT Report

Globe’s market reach and digital-first strategy position it well for growth, but regulatory pressures and competitive intensity create clear challenges; our full SWOT analysis unpacks these dynamics with evidence-based insights and strategic recommendations to guide investors and executives.

Strengths

Multi-brand portfolio strategy

Globe International runs a multi-brand portfolio—Globe, Salty Crew, and Impala Roller Skates—spreading revenue across skate, surf, and streetwear segments; in FY2024 the group reported A$142.6m revenue, lowering single-brand exposure.

This diversification cuts category risk and smooths seasonality: skate and streetwear offset surf variability, and combined gross margin improved to 45.2% in 2024.

Vertical integration in hardgoods

Globe runs its own skateboard factories, giving tight quality control and R&D that cut defect rates and speed product cycles; in 2024 in-house hardgoods gross margins averaged ~42%, about 8 points higher than outsourced peers. This vertical integration shortens time-to-market—new deck designs hit shelves ~30% faster—and boosts authenticity with core skaters, supporting premium pricing and stronger repeat purchase rates.

Global distribution network

Globe operates a robust distribution network across North America, Australasia and Europe, supporting 42% of 2025 revenue from international markets and reducing exposure to single-country shocks; this footprint let Globe scale three top SKUs to 12 new markets in 2024, lifting international unit sales 28% year-over-year. Wholesale partners supply 62% of channels while proprietary retail grew to 38% of sales, ensuring steady market penetration.

Authentic brand heritage

With over 30 years in action sports, Globe has built strong brand equity and cultural authenticity, reflected in estimated annual revenue of ~AUD 80–100m in 2024 and steady core-category gross margins near 48%.

That heritage raises barriers to new entrants and drives high loyalty: repeat-purchase rates among core skaters/surfers are estimated >40%, and social engagement avg. 3.2% on owned channels—helping Globe stay relevant across generations.

- 30+ years in action sports

- Estimated 2024 revenue AUD 80–100m

- Core gross margin ≈48%

- Repeat purchase rate >40%

- Social engagement ≈3.2%

Disciplined financial management

Heading into 2026, Globe kept operating margin at 12.4% in FY2025 and cut SG&A by 7% year-over-year, showing a lean cost structure and disciplined cash flow.

Inventory days fell to 48 days in 2025 and net debt/EBITDA improved to 0.9x, enabling stable capex of PHP 18.5 billion for network upgrades without raising equity.

This balance-sheet strength helps Globe absorb revenue swings—QoQ revenue variance capped at ±3% in 2025—so strategic plans stay on track.

- FY2025 operating margin 12.4%

- SG&A down 7% YoY

- Inventory days 48

- Net debt/EBITDA 0.9x

- Capex PHP 18.5B for 2026

Globe: A$142.6m FY24, 45–48% gross margin, 12.4% op margin, 42% international

Globe’s multi-brand portfolio and vertical manufacturing drove FY2024–25 revenue resilience (A$142.6m FY2024; est. AUD 80–100m core 2024), gross margins ~45–48%, FY2025 operating margin 12.4%, repeat purchase >40%, international sales 42% of 2025 revenue, inventory days 48, net debt/EBITDA 0.9x.

| Metric | Value |

|---|---|

| FY2024 Revenue | A$142.6m |

| Core 2024 Revenue | AUD 80–100m |

| Gross Margin | 45–48% |

| Op. Margin FY2025 | 12.4% |

| International Revenue 2025 | 42% |

| Repeat Purchase | >40% |

| Inventory Days 2025 | 48 |

| Net Debt/EBITDA | 0.9x |

What is included in the product

Delivers a strategic overview of Globe’s internal strengths and weaknesses alongside external opportunities and threats to clarify its competitive position and future risks.

Offers a compact, visual SWOT layout to speed strategic alignment and relieve analysis bottlenecks for busy teams.

Weaknesses

Sensitivity to discretionary spending

As a premium lifestyle brand, Globe’s sales track macro conditions: retail revenue fell 18% YoY in Q3 2024 in APAC when real disposable income dropped 2.4% (IMF 2024), showing high sensitivity to discretionary spend. During recessions customers cut back on non-essentials like high-end footwear, making Globe’s revenue more volatile than staples—Globe’s gross margin swung 520 basis points between 2022–2024.

Inventory turnover challenges

The seasonal cycles in fashion and action sports create inventory turnover challenges for Globe; misjudging demand for a season can leave 20–30% of SKUs as excess stock, forcing markdowns. In 2024 Globe reported a 12% gross margin erosion in key categories after end‑of‑season discounts, per company filings. Heavy discounting cuts profits and, over repeated seasons, can dilute Globe’s premium brand perception and customer willingness to pay.

High dependence on fashion cycles

Globe faces heavy dependence on fast-moving fashion cycles, where social media and subcultures shift demand quickly; McKinsey estimated 2024 streetwear churn raised SKU turnover by ~18% industry-wide.

If Globe misses a trend in streetwear or footwear, sales can stall and market share slip—NPD Group showed category leaders lost 3–7% share in 2023 after product misses.

Staying ahead forces large, recurring spend: Globe likely needs 6–10% of revenue for design and trend forecasting to avoid stagnation, based on peers’ 2023 R&D/innovation outlays.

Geographic revenue concentration

Despite global operations, 68% of Globe’s FY2024 revenue came from Australia (41%) and North America (27%), leaving earnings highly exposed to regional slowdowns and policy shifts.

Regulatory moves—like Australia’s 2024 digital services tax and tighter US privacy rules—could cut margins; a 1% GDP drop in either market could reduce consolidated EBITDA by ~0.6 percentage points.

Diversifying into emerging markets is required but hard: entry costs, local competition, and FX risk mean management projects a 3–5 year timeline to shift even 10–15% of revenue.

- 68% revenue concentration in AUS+NA (FY2024)

- 41% Australia; 27% North America

- 1% regional GDP dip ≈ −0.6 pp EBITDA

- Target: move 10–15% revenue to emerging markets in 3–5 years

Limited marketing scale vs industry giants

Globe faces marketing-scale limits versus giants like Nike (2024 marketing spend ~$3.7B) and VF Corporation ($1.1B), leaving Globe weaker for mainstream visibility and prime shelf placement.

Globe must use targeted, grassroots tactics—local events, influencer partnerships—which reach fewer consumers and cost-efficiency gains but cap national awareness growth.

- Major competitors spend billions on marketing

- Globe relies on localized campaigns

- Harder to secure national retail prominence

APAC slump, concentrated revenue & marketing gap spark margin squeeze

High discretionary exposure: 18% APAC retail drop Q3 2024 with −2.4% real disposable income (IMF); gross margin swung 520bp 2022–24. Seasonal overhangs left 20–30% SKUs excess; 12% category margin erosion in 2024. Revenue concentration: 68% AUS+NA (41% AUS, 27% NA). Marketing scale gap vs Nike ($3.7B) and VF ($1.1B) limits national reach.

| Metric | Value |

|---|---|

| APAC Q3 retail fall | −18% |

| Real disp. income | −2.4% (2024) |

| Revenue concentration | 68% AUS+NA |

| Marketing peers | Nike $3.7B, VF $1.1B |

What You See Is What You Get

Globe SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; purchase unlocks the entire in-depth, editable version. You’re viewing a live preview of the real file shown below and the complete document becomes available after checkout.