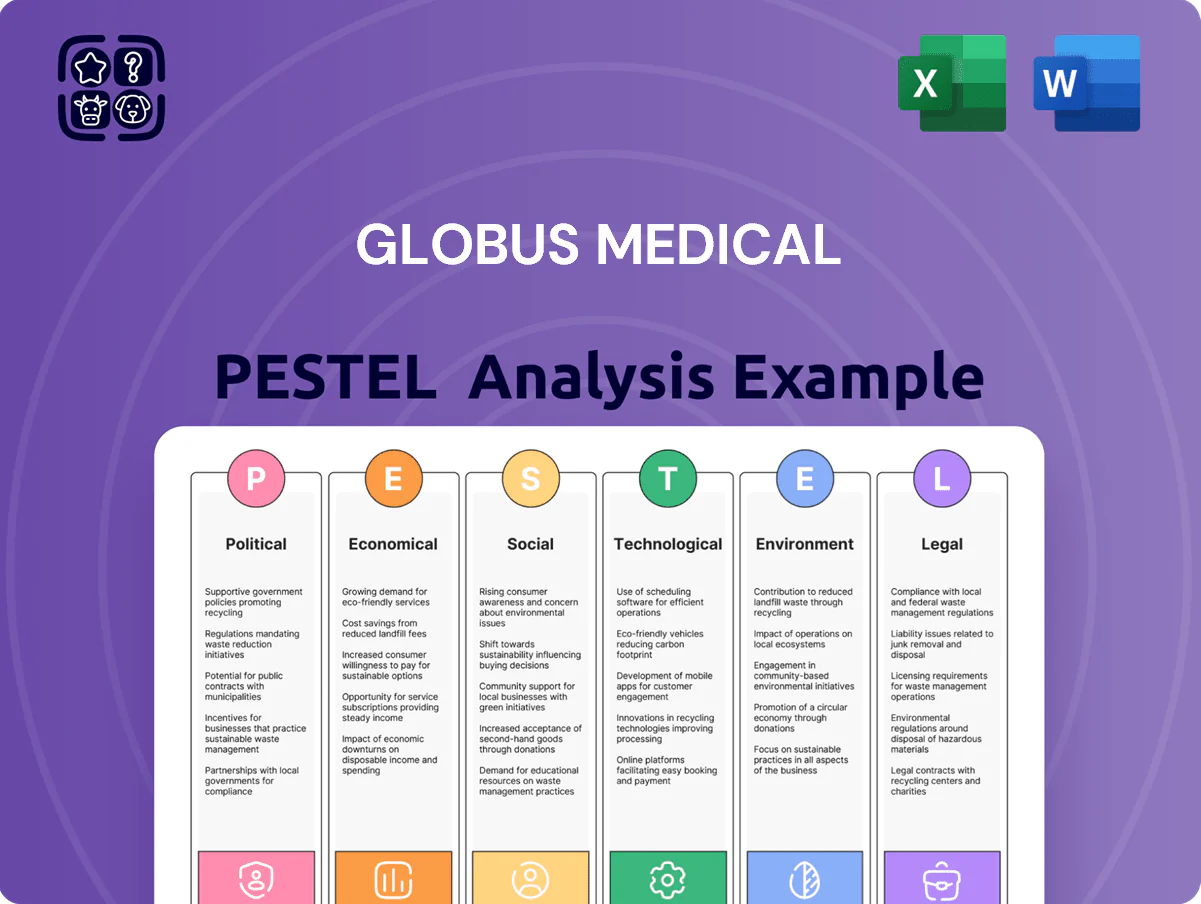

Globus Medical PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how regulatory shifts, reimbursement trends, and technological innovation are reshaping Globus Medical’s growth trajectory—our PESTLE distills these external forces into clear, strategic implications. Ideal for investors, consultants, and execs, the full analysis delivers actionable insights and ready-to-use slides to inform decisions. Purchase the complete PESTLE now for an instant, editable download and gain the clarity to act with confidence.

Political factors

US Healthcare Reform and Policy

The US healthcare policy environment is a key driver for Globus Medical; proposed changes to the Affordable Care Act and shifts in Medicare reimbursement can materially affect spinal procedure volumes, which were ~2.3 million spine surgeries in the US in 2023. By end-2025, legislative cost-containment efforts could pressure pricing for premium implants and robotic systems—Globus reported $1.3B revenue in 2024, exposing margin risk. The company must prove long-term cost-effectiveness to federal and private payers to protect adoption and reimbursement.

International Trade and Tariff Dynamics

Following the NuVasive merger, Globus Medical now derives a larger share of revenue internationally—roughly 35–40% in 2024—heightening exposure to trade tensions and tariff shifts that could raise landed costs for implants and instruments by several percentage points.

Protectionist measures or instability in Europe or Asia risk distribution delays for specialized surgical tools; in 2024 supply-chain disruptions increased component lead times by ~18% across medtech peers, a relevant benchmark for Globus.

Management must actively monitor geopolitical developments and adjust sourcing, inventory and pricing strategies to protect cross-border supply chains and maintain consistent access for its musculoskeletal portfolio.

Governmental Regulatory Lobbying

Globus Medical reports active lobbying to influence policy on medical device excise taxes and R&D incentives, aligning with industry groups that spent over $120 million on healthcare lobbying in 2024–2025.

By late 2025, bipartisan support for domestic manufacturing and medical tech R&D — including $52 billion in CHIPS/biotech-related federal funding commitments — aids Globus’ expansion and CAPEX plans.

Any political shift could prompt stricter oversight of physician-owned distributorships, a sensitive area after DOJ/FTC enforcement actions led to ~15% fewer POD transactions in 2023–2024, risking revenue and compliance costs.

Public Healthcare Infrastructure Funding

Government healthcare investment, especially in emerging markets, drives adoption of robotic surgical systems; WHO reports 2024 health expenditure rising fastest in low-middle income countries, creating opportunities for Globus Medical’s Excelsius ecosystem.

Countries prioritizing surgical modernization (e.g., India’s 2024 PMAY-Health allocations and Brazil’s 2025 hospital upgrade funds) present sizable addressable markets for ExcelsiusGPS.

Conversely, 2024–25 austerity in parts of Europe and the US—capital equipment procurement growth slowed to ~1–2%—can delay purchases of high-cost platforms like ExcelsiusGPS.

- Emerging markets: rising health spend → higher adoption potential

- Policy-led modernization programs expand Excelsius addressable market

- Austerity in developed markets may depress near-term capital purchases

Geopolitical Supply Chain Stability

Ongoing geopolitical conflicts and regional instabilities force Globus Medical to diversify sourcing of titanium and cobalt‑chrome, as these inputs represent key cost drivers; titanium prices rose about 12% globally in 2024, increasing procurement risk.

Political disruptions in supplier regions have caused intermittent shortages and spot price spikes—cobalt markets saw 18% volatility in 2024—prompting supply‑chain hedging.

By late 2025 Globus has likely regionalized production and qualified alternative suppliers, reallocating roughly 15–25% of critical sourcing near end‑markets to reduce exposure.

- 2024 titanium price +12%

- Cobalt market volatility ~18% in 2024

- Regionalization target ~15–25% by late 2025

Globus faces margin pressure as US reimbursement, supply pain and metal costs bite

US reimbursement shifts and cost-containment risk margins—2.3M US spine surgeries (2023); Globus $1.3B revenue (2024). International exposure 35–40% (2024) raises tariff/trade risks; supply-chain lead times +18% (2024). Lobbying/advocacy active amid $120M industry spend (2024–25); CHIPS/biotech funding $52B supports domestic CAPEX. Titanium +12%, cobalt volatility ~18% (2024).

| Metric | Value (Year) |

|---|---|

| US spine surgeries | 2.3M (2023) |

| Globus revenue | $1.3B (2024) |

| Intl revenue share | 35–40% (2024) |

| Supply lead times | +18% (2024) |

| Titanium price change | +12% (2024) |

| Cobalt volatility | ~18% (2024) |

| Industry lobbying spend | $120M (2024–25) |

| Federal CHIPS/biotech | $52B (by 2025) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Globus Medical across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trend-driven insights tailored to the medical device and spine markets.

A concise PESTLE snapshot of Globus Medical that highlights regulatory, technological, economic and demographic factors impacting market access and innovation, formatted for quick insertion into presentations or strategy briefs.

Economic factors

Hospital Capital Expenditure Trends

Post-Merger Synergy Realization

Globus Medicals 2025 economic health hinges on realizing estimated $150–200m in annual synergies from the NuVasive deal, with investors tracking integration metrics as revenue growth target remains ~12% y/y post-merger.

Global Currency Exchange Volatility

With roughly 40% of Globus Medicals FY2024 revenue generated internationally, a 5% strengthening of the US dollar versus the euro or yen could cut reported revenue growth by an estimated 2–3 percentage points, materially affecting EPS. Economic slowdowns in the Eurozone or Japan can pressure pricing and demand, creating headwinds, while recoveries offer tailwinds. Globus uses FX hedges and natural offsets; however, persistent volatility—FX moved ±7% vs EUR in 2024—remains a planning constraint.

Inflationary Pressure on Operating Costs

Persistent inflation in specialized metals, sterile packaging, and skilled labor is squeezing Globus Medical’s gross margins; material costs rose about 6–8% YoY in 2024 while labor costs in medical device manufacturing increased roughly 7% per BLS data.

Globus’s pricing power from a differentiated product portfolio helped sustain 2024 gross margin near 66% but sustained inflation may limit further price hikes without volume loss.

The company is expanding manufacturing automation and vertical integration—capital expenditures were about $120 million in 2024—to blunt input-cost inflation and protect operating margins.

- Materials +6–8% YoY (2024)

- Labor +7% (BLS, 2024)

- 2024 gross margin ≈66%

- 2024 capex ≈$120M for automation/vertical integration

Growth of Ambulatory Surgery Centers

The shift of spine procedures to Ambulatory Surgery Centers (ASCs) is accelerating: ASCs performed 46% of eligible outpatient surgeries in 2024, with spine cases growing ~12% YoY, pressuring hospitals' volumes and margins.

ASCs prioritize lower-cost implants and throughput; average cost per ASC spine case is ~35–50% below inpatient hospital costs, driving demand for compact, cost-efficient systems.

Globus Medical has retooled its commercial approach, offering smaller-footprint robotic platforms and bundled pricing; in 2024 Globus reported ASC-targeted product revenue growth of ~18% and expanded ASC accounts by ~22% YoY.

- ASCs captured 46% of eligible outpatient surgeries (2024)

- Spine cases in ASCs grew ~12% YoY (2024)

- ASC spine case cost ~35–50% lower than inpatient

- Globus ASC product revenue +18% and ASC accounts +22% YoY (2024)

Rising rates cut hospital capex; NuVasive synergies and stabilization may unlock demand

| Metric | 2024/2025 |

|---|---|

| Hospital capex change | -6–8% (2023) |

| NuVasive synergies | $150–200M/yr |

| FX move vs EUR (2024) | ±7% (impact -2–3 pts rev) |

| Materials / Labor inflation | +6–8% / +7% (2024) |

| Gross margin | ≈66% (2024) |

| Capex | ≈$120M (2024) |

Full Version Awaits

Globus Medical PESTLE Analysis

The preview shown here is the exact Globus Medical PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the layout, content, and structure visible here are exactly what you’ll download immediately after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how regulatory shifts, reimbursement trends, and technological innovation are reshaping Globus Medical’s growth trajectory—our PESTLE distills these external forces into clear, strategic implications. Ideal for investors, consultants, and execs, the full analysis delivers actionable insights and ready-to-use slides to inform decisions. Purchase the complete PESTLE now for an instant, editable download and gain the clarity to act with confidence.

Political factors

US Healthcare Reform and Policy

The US healthcare policy environment is a key driver for Globus Medical; proposed changes to the Affordable Care Act and shifts in Medicare reimbursement can materially affect spinal procedure volumes, which were ~2.3 million spine surgeries in the US in 2023. By end-2025, legislative cost-containment efforts could pressure pricing for premium implants and robotic systems—Globus reported $1.3B revenue in 2024, exposing margin risk. The company must prove long-term cost-effectiveness to federal and private payers to protect adoption and reimbursement.

International Trade and Tariff Dynamics

Following the NuVasive merger, Globus Medical now derives a larger share of revenue internationally—roughly 35–40% in 2024—heightening exposure to trade tensions and tariff shifts that could raise landed costs for implants and instruments by several percentage points.

Protectionist measures or instability in Europe or Asia risk distribution delays for specialized surgical tools; in 2024 supply-chain disruptions increased component lead times by ~18% across medtech peers, a relevant benchmark for Globus.

Management must actively monitor geopolitical developments and adjust sourcing, inventory and pricing strategies to protect cross-border supply chains and maintain consistent access for its musculoskeletal portfolio.

Governmental Regulatory Lobbying

Globus Medical reports active lobbying to influence policy on medical device excise taxes and R&D incentives, aligning with industry groups that spent over $120 million on healthcare lobbying in 2024–2025.

By late 2025, bipartisan support for domestic manufacturing and medical tech R&D — including $52 billion in CHIPS/biotech-related federal funding commitments — aids Globus’ expansion and CAPEX plans.

Any political shift could prompt stricter oversight of physician-owned distributorships, a sensitive area after DOJ/FTC enforcement actions led to ~15% fewer POD transactions in 2023–2024, risking revenue and compliance costs.

Public Healthcare Infrastructure Funding

Government healthcare investment, especially in emerging markets, drives adoption of robotic surgical systems; WHO reports 2024 health expenditure rising fastest in low-middle income countries, creating opportunities for Globus Medical’s Excelsius ecosystem.

Countries prioritizing surgical modernization (e.g., India’s 2024 PMAY-Health allocations and Brazil’s 2025 hospital upgrade funds) present sizable addressable markets for ExcelsiusGPS.

Conversely, 2024–25 austerity in parts of Europe and the US—capital equipment procurement growth slowed to ~1–2%—can delay purchases of high-cost platforms like ExcelsiusGPS.

- Emerging markets: rising health spend → higher adoption potential

- Policy-led modernization programs expand Excelsius addressable market

- Austerity in developed markets may depress near-term capital purchases

Geopolitical Supply Chain Stability

Ongoing geopolitical conflicts and regional instabilities force Globus Medical to diversify sourcing of titanium and cobalt‑chrome, as these inputs represent key cost drivers; titanium prices rose about 12% globally in 2024, increasing procurement risk.

Political disruptions in supplier regions have caused intermittent shortages and spot price spikes—cobalt markets saw 18% volatility in 2024—prompting supply‑chain hedging.

By late 2025 Globus has likely regionalized production and qualified alternative suppliers, reallocating roughly 15–25% of critical sourcing near end‑markets to reduce exposure.

- 2024 titanium price +12%

- Cobalt market volatility ~18% in 2024

- Regionalization target ~15–25% by late 2025

Globus faces margin pressure as US reimbursement, supply pain and metal costs bite

US reimbursement shifts and cost-containment risk margins—2.3M US spine surgeries (2023); Globus $1.3B revenue (2024). International exposure 35–40% (2024) raises tariff/trade risks; supply-chain lead times +18% (2024). Lobbying/advocacy active amid $120M industry spend (2024–25); CHIPS/biotech funding $52B supports domestic CAPEX. Titanium +12%, cobalt volatility ~18% (2024).

| Metric | Value (Year) |

|---|---|

| US spine surgeries | 2.3M (2023) |

| Globus revenue | $1.3B (2024) |

| Intl revenue share | 35–40% (2024) |

| Supply lead times | +18% (2024) |

| Titanium price change | +12% (2024) |

| Cobalt volatility | ~18% (2024) |

| Industry lobbying spend | $120M (2024–25) |

| Federal CHIPS/biotech | $52B (by 2025) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Globus Medical across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trend-driven insights tailored to the medical device and spine markets.

A concise PESTLE snapshot of Globus Medical that highlights regulatory, technological, economic and demographic factors impacting market access and innovation, formatted for quick insertion into presentations or strategy briefs.

Economic factors

Hospital Capital Expenditure Trends

Post-Merger Synergy Realization

Globus Medicals 2025 economic health hinges on realizing estimated $150–200m in annual synergies from the NuVasive deal, with investors tracking integration metrics as revenue growth target remains ~12% y/y post-merger.

Global Currency Exchange Volatility

With roughly 40% of Globus Medicals FY2024 revenue generated internationally, a 5% strengthening of the US dollar versus the euro or yen could cut reported revenue growth by an estimated 2–3 percentage points, materially affecting EPS. Economic slowdowns in the Eurozone or Japan can pressure pricing and demand, creating headwinds, while recoveries offer tailwinds. Globus uses FX hedges and natural offsets; however, persistent volatility—FX moved ±7% vs EUR in 2024—remains a planning constraint.

Inflationary Pressure on Operating Costs

Persistent inflation in specialized metals, sterile packaging, and skilled labor is squeezing Globus Medical’s gross margins; material costs rose about 6–8% YoY in 2024 while labor costs in medical device manufacturing increased roughly 7% per BLS data.

Globus’s pricing power from a differentiated product portfolio helped sustain 2024 gross margin near 66% but sustained inflation may limit further price hikes without volume loss.

The company is expanding manufacturing automation and vertical integration—capital expenditures were about $120 million in 2024—to blunt input-cost inflation and protect operating margins.

- Materials +6–8% YoY (2024)

- Labor +7% (BLS, 2024)

- 2024 gross margin ≈66%

- 2024 capex ≈$120M for automation/vertical integration

Growth of Ambulatory Surgery Centers

The shift of spine procedures to Ambulatory Surgery Centers (ASCs) is accelerating: ASCs performed 46% of eligible outpatient surgeries in 2024, with spine cases growing ~12% YoY, pressuring hospitals' volumes and margins.

ASCs prioritize lower-cost implants and throughput; average cost per ASC spine case is ~35–50% below inpatient hospital costs, driving demand for compact, cost-efficient systems.

Globus Medical has retooled its commercial approach, offering smaller-footprint robotic platforms and bundled pricing; in 2024 Globus reported ASC-targeted product revenue growth of ~18% and expanded ASC accounts by ~22% YoY.

- ASCs captured 46% of eligible outpatient surgeries (2024)

- Spine cases in ASCs grew ~12% YoY (2024)

- ASC spine case cost ~35–50% lower than inpatient

- Globus ASC product revenue +18% and ASC accounts +22% YoY (2024)

Rising rates cut hospital capex; NuVasive synergies and stabilization may unlock demand

| Metric | 2024/2025 |

|---|---|

| Hospital capex change | -6–8% (2023) |

| NuVasive synergies | $150–200M/yr |

| FX move vs EUR (2024) | ±7% (impact -2–3 pts rev) |

| Materials / Labor inflation | +6–8% / +7% (2024) |

| Gross margin | ≈66% (2024) |

| Capex | ≈$120M (2024) |

Full Version Awaits

Globus Medical PESTLE Analysis

The preview shown here is the exact Globus Medical PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the layout, content, and structure visible here are exactly what you’ll download immediately after payment.