Gaming & Leisure Properties Business Model Canvas

Asset-Light REIT Blueprint: Gaming & Leisure Properties’ Growth, Leases & Capital Recycling

Explore Gaming & Leisure Properties’ asset-light REIT model: strategic property acquisitions, long-term lease income from leading operators, and capital recycling that fuels growth and shareholder returns.

Unlock the full Business Model Canvas to see detailed customer segments, revenue drivers, cost structure, and partnership dynamics—perfect for investors, analysts, and strategists seeking a ready-to-use, actionable blueprint.

Partnerships

PENN Entertainment Strategic Alliance

PENN Entertainment, as GLPI’s primary tenant and former parent, remains the most critical partner, generating about $1.1 billion in rent and tenant-related revenue through 2024 and underpinning GLPI’s dividend coverage.

By year-end 2025 the alliance still features joint asset-management initiatives and options for co-development across PENN’s ~40 regional properties, sustaining predictable cash flow and growth optionality for GLPI.

Regional Gaming Operators

GLPI partners with regional casino operators such as Boyd Gaming and Casino Queen to diversify tenants beyond its 2013 spin‑off roots; as of Q3 2025 GLPI leased 98 properties and reported 2024 AFFO of $1.39 per share, showing scale from diversified operator relationships.

These partnerships let GLPI enter localized markets with varied regulation and demand, supporting lease renewals and sourcing acquisitions—GLPI closed $750m in acquisitions in 2024, underscoring the value of operator ties for long‑term growth.

Financial and Lending Institutions

Gaming & Leisure Properties relies on investment banks and credit providers to maintain liquidity and fund acquisitions, using these partners to issue senior unsecured notes and manage a $1.5 billion revolving credit facility (renewed 2024) that underpins capital deployment.

By late 2025 the firm leverages these relationships to trim its weighted average cost of capital to about 6.1% amid rising rates, refinancing $800 million of debt in 2024–25 to extend maturities and lower coupon costs.

State Gaming Regulatory Commissions

GLPI maintains active contacts with state gaming regulatory commissions in all states where it owns casinos (24 states as of Dec 31, 2025), since regulators vet landlord suitability and lease compliance to state gambling laws; proactive engagement reduces the risk of tenant license suspensions that could halt operations and cut rental income (GLPI reported $1.6B in rent and management income in 2024).

- Regulatory coverage: 24 states (2025)

- Risk mitigant: prevents license-driven revenue loss

- Financial stake: $1.6B rent & management income (2024)

Construction and Development Firms

GLPI funds tenant improvements and master-plan expansions with specialized construction partners to lift rent yields and asset value, targeting 5–8% uplift per project based on recent redevelopments that averaged $25–40M capex each in 2023–2024.

By 2025 these builds prioritize non-gaming amenities—hotels and convention space—to boost NOI diversification and attract higher lease rates from operators.

- Average redevelopment capex: $25–40M (2023–24)

- Estimated rent-yield uplift per project: 5–8%

- 2025 focus: hotels + convention spaces to diversify NOI

GLPI: $1.6B rent, $750M 2024 buys, $1.5B revolver, WACC ≈6.1% — 24-state regulatory moat

GLPI’s key partners—PENN Entertainment (≈$1.1B rent through 2024), Boyd Gaming, Casino Queen and other operators—drive stable rent from 98 leases and enabled $750M acquisitions in 2024; banks and a $1.5B revolver (renewed 2024) funded $800M refinancings, trimming WACC to ~6.1% by 2025 while 24-state regulatory ties protect $1.6B rent exposure.

| Metric | Value |

|---|---|

| PENN rent (through 2024) | $1.1B |

| Total rent & management (2024) | $1.6B |

| Leased properties (Q3 2025) | 98 |

| Acquisitions (2024) | $750M |

| Revolver | $1.5B (2024 renewed) |

| Refinanced debt (2024–25) | $800M |

| WACC (est. 2025) | ≈6.1% |

| States with regulatory coverage (2025) | 24 |

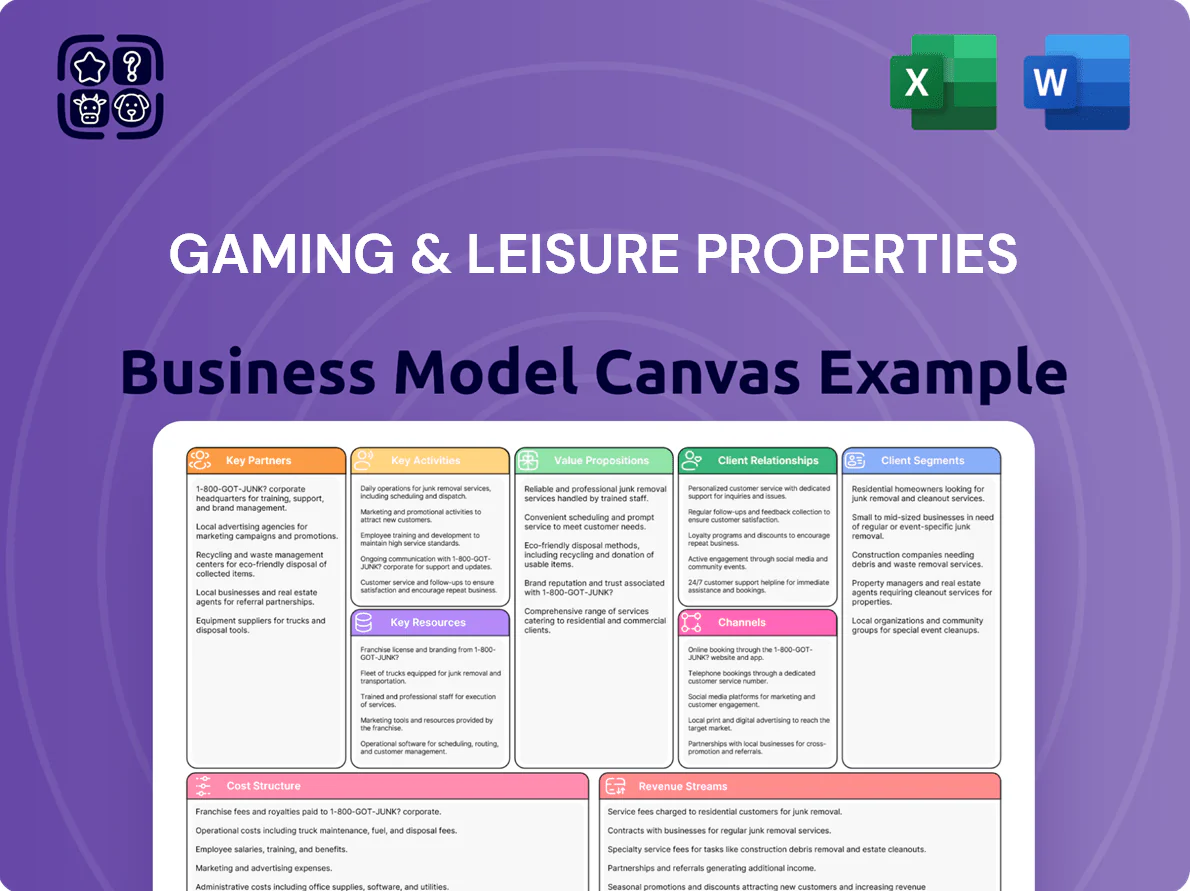

What is included in the product

A concise Business Model Canvas for Gaming & Leisure Properties, detailing customer segments, value propositions, channels, revenue streams, key activities, resources, partners, cost structure, and governance tailored to a casino-focused REIT; structured for investor presentations with competitive analysis, SWOT-linked insights, and actionable recommendations for capital allocation and portfolio optimization.

High-level view of Gaming & Leisure Properties’ business model with editable cells to quickly map REIT revenue streams, tenant relationships, and capital allocation.

Activities

Strategic Property Acquisition

GLPI targets and acquires high-quality gaming real estate that fits its risk-return profile, focusing on markets with limited competition and long-term foot traffic; since 2023 GLPI completed $2.1B in acquisitions supporting portfolio diversification.

Each deal is screened for tenant creditworthiness, lease structure, and location viability—metrics that drove AFFO per share growth of 3.8% in 2024 and funded $450M of shareholder returns.

Lease Underwriting and Management

GLPI negotiates and manages triple-net leases (tenant pays taxes, insurance, maintenance), targeting escalators of 2–3% and lease terms averaging 15–20 years to lock stable cashflows; as of Q4 2025 GLPI held 58 consolidated properties and reported $1.1B annualized rent, so escalators materially boost NOI. Management runs quarterly tenant credit reviews and KPI tracking (revPAR/EBITDAR margins) to catch early distress and trigger cure rights or cash collateral to protect rent streams.

Capital Structure Optimization

As a REIT, Gaming & Leisure Properties (GLPI) must distribute at least 90% of taxable income while funding growth via equity and debt; management actively mixes follow-on equity (e.g., $1.2B raised in 2023–24) with bond and bank issuances to preserve liquidity. A primary 2025 activity is refinancing roughly $1.8B of maturing debt at competitive rates to protect dividend yield, which averaged about 5.6% in 2024.

Portfolio Diversification and Expansion

Management reduces tenant concentration risk by acquiring properties from a broader set of gaming operators and evaluating entries into new U.S. states and selected international jurisdictions; as of YE 2025 GLPI held ~38% revenue with its top tenant, down from 46% in 2021, and added 12 properties across three new states in 2024–25.

Diversification includes testing gaming-adjacent leisure assets—e.g., 2025 pilot leases for hotels and F&B venues—to buffer against local downturns and operator-specific shocks.

- Top-tenant revenue ~38% (YE 2025)

- 12 properties added in 2024–25 across 3 new states

- Pilot leisure leases launched in 2025 (hotels, F&B)

Compliance and Regulatory Monitoring

GLPI allocates substantial legal and compliance headcount and spent roughly $18.5M on compliance-related SG&A in 2024, running continuous internal audits and legal reviews of leases and tenant deals to preserve REIT tax status and gaming licenses.

Regulatory monitoring tracks state and federal rule changes—affecting ~100 operating licenses across 15 states—so the company updates policies and files license renewals proactively to avoid disruptions.

- 2024 compliance SG&A: $18.5M

- ~100 gaming licenses in 15 states

- Routine internal audits and lease/legal reviews

GLPI strengthens cash flows with $2.1B in NNN gaming deals, 12 properties, top-tenant risk down

GLPI acquires and manages triple-net gaming real estate, secures long-term leases (15–20 yrs) with 2–3% escalators, and runs tenant credit/KPI monitoring to protect cashflows; portfolio actions (2023–25) added 12 properties, $2.1B acquisitions, and cut top-tenant revenue to ~38% (YE 2025).

| Metric | Value |

|---|---|

| Acquisitions 2023–25 | $2.1B |

| Properties added 2024–25 | 12 |

| Top-tenant revenue (YE 2025) | ~38% |

| Annualized rent (Q4 2025) | $1.1B |

| Compliance SG&A 2024 | $18.5M |

Full Document Unlocks After Purchase

Business Model Canvas

The document previewed here is the actual Gaming & Leisure Properties Business Model Canvas you will receive—no mockups or samples. Upon purchase you’ll instantly download this exact, fully editable file, formatted and structured the same way as shown. It’s ready for presentation, analysis, or customization, with all sections included and no surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Asset-Light REIT Blueprint: Gaming & Leisure Properties’ Growth, Leases & Capital Recycling

Explore Gaming & Leisure Properties’ asset-light REIT model: strategic property acquisitions, long-term lease income from leading operators, and capital recycling that fuels growth and shareholder returns.

Unlock the full Business Model Canvas to see detailed customer segments, revenue drivers, cost structure, and partnership dynamics—perfect for investors, analysts, and strategists seeking a ready-to-use, actionable blueprint.

Partnerships

PENN Entertainment Strategic Alliance

PENN Entertainment, as GLPI’s primary tenant and former parent, remains the most critical partner, generating about $1.1 billion in rent and tenant-related revenue through 2024 and underpinning GLPI’s dividend coverage.

By year-end 2025 the alliance still features joint asset-management initiatives and options for co-development across PENN’s ~40 regional properties, sustaining predictable cash flow and growth optionality for GLPI.

Regional Gaming Operators

GLPI partners with regional casino operators such as Boyd Gaming and Casino Queen to diversify tenants beyond its 2013 spin‑off roots; as of Q3 2025 GLPI leased 98 properties and reported 2024 AFFO of $1.39 per share, showing scale from diversified operator relationships.

These partnerships let GLPI enter localized markets with varied regulation and demand, supporting lease renewals and sourcing acquisitions—GLPI closed $750m in acquisitions in 2024, underscoring the value of operator ties for long‑term growth.

Financial and Lending Institutions

Gaming & Leisure Properties relies on investment banks and credit providers to maintain liquidity and fund acquisitions, using these partners to issue senior unsecured notes and manage a $1.5 billion revolving credit facility (renewed 2024) that underpins capital deployment.

By late 2025 the firm leverages these relationships to trim its weighted average cost of capital to about 6.1% amid rising rates, refinancing $800 million of debt in 2024–25 to extend maturities and lower coupon costs.

State Gaming Regulatory Commissions

GLPI maintains active contacts with state gaming regulatory commissions in all states where it owns casinos (24 states as of Dec 31, 2025), since regulators vet landlord suitability and lease compliance to state gambling laws; proactive engagement reduces the risk of tenant license suspensions that could halt operations and cut rental income (GLPI reported $1.6B in rent and management income in 2024).

- Regulatory coverage: 24 states (2025)

- Risk mitigant: prevents license-driven revenue loss

- Financial stake: $1.6B rent & management income (2024)

Construction and Development Firms

GLPI funds tenant improvements and master-plan expansions with specialized construction partners to lift rent yields and asset value, targeting 5–8% uplift per project based on recent redevelopments that averaged $25–40M capex each in 2023–2024.

By 2025 these builds prioritize non-gaming amenities—hotels and convention space—to boost NOI diversification and attract higher lease rates from operators.

- Average redevelopment capex: $25–40M (2023–24)

- Estimated rent-yield uplift per project: 5–8%

- 2025 focus: hotels + convention spaces to diversify NOI

GLPI: $1.6B rent, $750M 2024 buys, $1.5B revolver, WACC ≈6.1% — 24-state regulatory moat

GLPI’s key partners—PENN Entertainment (≈$1.1B rent through 2024), Boyd Gaming, Casino Queen and other operators—drive stable rent from 98 leases and enabled $750M acquisitions in 2024; banks and a $1.5B revolver (renewed 2024) funded $800M refinancings, trimming WACC to ~6.1% by 2025 while 24-state regulatory ties protect $1.6B rent exposure.

| Metric | Value |

|---|---|

| PENN rent (through 2024) | $1.1B |

| Total rent & management (2024) | $1.6B |

| Leased properties (Q3 2025) | 98 |

| Acquisitions (2024) | $750M |

| Revolver | $1.5B (2024 renewed) |

| Refinanced debt (2024–25) | $800M |

| WACC (est. 2025) | ≈6.1% |

| States with regulatory coverage (2025) | 24 |

What is included in the product

A concise Business Model Canvas for Gaming & Leisure Properties, detailing customer segments, value propositions, channels, revenue streams, key activities, resources, partners, cost structure, and governance tailored to a casino-focused REIT; structured for investor presentations with competitive analysis, SWOT-linked insights, and actionable recommendations for capital allocation and portfolio optimization.

High-level view of Gaming & Leisure Properties’ business model with editable cells to quickly map REIT revenue streams, tenant relationships, and capital allocation.

Activities

Strategic Property Acquisition

GLPI targets and acquires high-quality gaming real estate that fits its risk-return profile, focusing on markets with limited competition and long-term foot traffic; since 2023 GLPI completed $2.1B in acquisitions supporting portfolio diversification.

Each deal is screened for tenant creditworthiness, lease structure, and location viability—metrics that drove AFFO per share growth of 3.8% in 2024 and funded $450M of shareholder returns.

Lease Underwriting and Management

GLPI negotiates and manages triple-net leases (tenant pays taxes, insurance, maintenance), targeting escalators of 2–3% and lease terms averaging 15–20 years to lock stable cashflows; as of Q4 2025 GLPI held 58 consolidated properties and reported $1.1B annualized rent, so escalators materially boost NOI. Management runs quarterly tenant credit reviews and KPI tracking (revPAR/EBITDAR margins) to catch early distress and trigger cure rights or cash collateral to protect rent streams.

Capital Structure Optimization

As a REIT, Gaming & Leisure Properties (GLPI) must distribute at least 90% of taxable income while funding growth via equity and debt; management actively mixes follow-on equity (e.g., $1.2B raised in 2023–24) with bond and bank issuances to preserve liquidity. A primary 2025 activity is refinancing roughly $1.8B of maturing debt at competitive rates to protect dividend yield, which averaged about 5.6% in 2024.

Portfolio Diversification and Expansion

Management reduces tenant concentration risk by acquiring properties from a broader set of gaming operators and evaluating entries into new U.S. states and selected international jurisdictions; as of YE 2025 GLPI held ~38% revenue with its top tenant, down from 46% in 2021, and added 12 properties across three new states in 2024–25.

Diversification includes testing gaming-adjacent leisure assets—e.g., 2025 pilot leases for hotels and F&B venues—to buffer against local downturns and operator-specific shocks.

- Top-tenant revenue ~38% (YE 2025)

- 12 properties added in 2024–25 across 3 new states

- Pilot leisure leases launched in 2025 (hotels, F&B)

Compliance and Regulatory Monitoring

GLPI allocates substantial legal and compliance headcount and spent roughly $18.5M on compliance-related SG&A in 2024, running continuous internal audits and legal reviews of leases and tenant deals to preserve REIT tax status and gaming licenses.

Regulatory monitoring tracks state and federal rule changes—affecting ~100 operating licenses across 15 states—so the company updates policies and files license renewals proactively to avoid disruptions.

- 2024 compliance SG&A: $18.5M

- ~100 gaming licenses in 15 states

- Routine internal audits and lease/legal reviews

GLPI strengthens cash flows with $2.1B in NNN gaming deals, 12 properties, top-tenant risk down

GLPI acquires and manages triple-net gaming real estate, secures long-term leases (15–20 yrs) with 2–3% escalators, and runs tenant credit/KPI monitoring to protect cashflows; portfolio actions (2023–25) added 12 properties, $2.1B acquisitions, and cut top-tenant revenue to ~38% (YE 2025).

| Metric | Value |

|---|---|

| Acquisitions 2023–25 | $2.1B |

| Properties added 2024–25 | 12 |

| Top-tenant revenue (YE 2025) | ~38% |

| Annualized rent (Q4 2025) | $1.1B |

| Compliance SG&A 2024 | $18.5M |

Full Document Unlocks After Purchase

Business Model Canvas

The document previewed here is the actual Gaming & Leisure Properties Business Model Canvas you will receive—no mockups or samples. Upon purchase you’ll instantly download this exact, fully editable file, formatted and structured the same way as shown. It’s ready for presentation, analysis, or customization, with all sections included and no surprises.