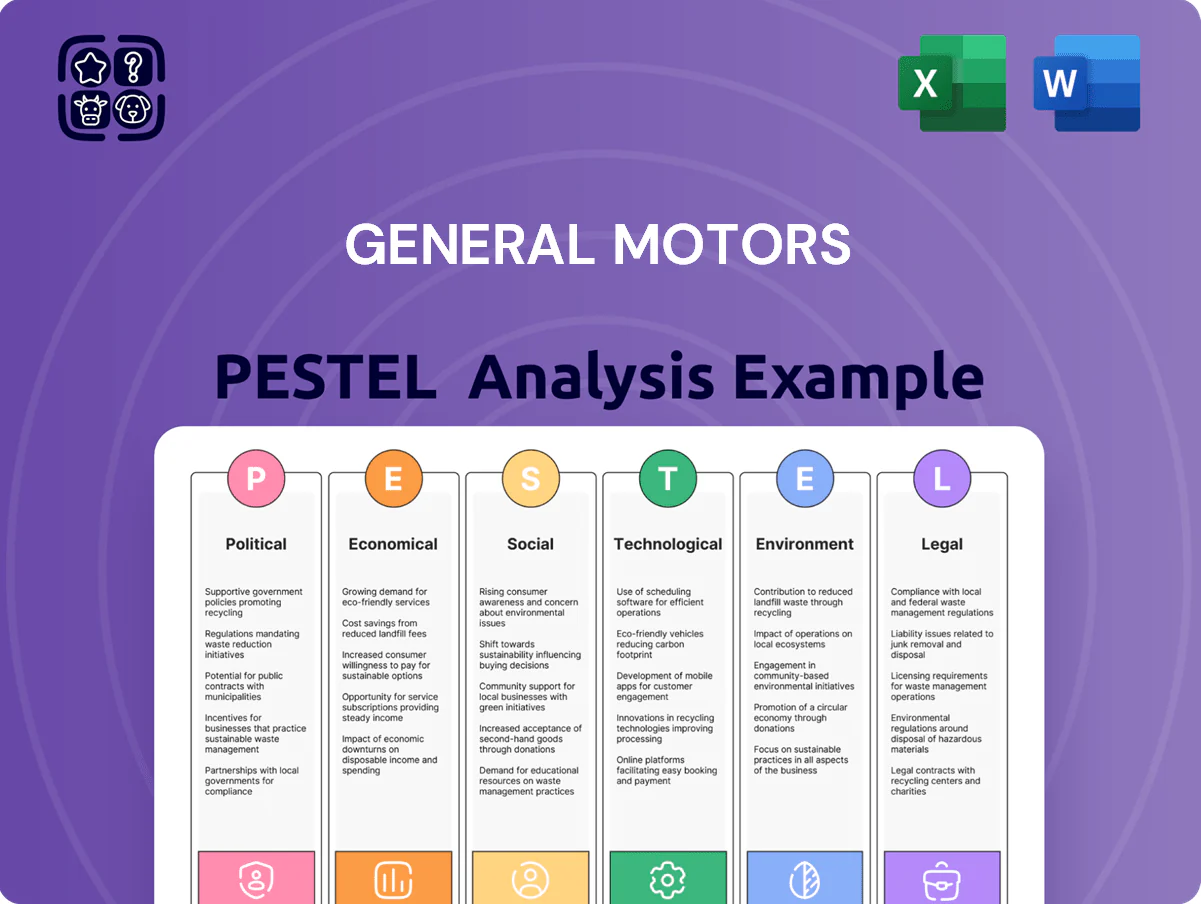

General Motors PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and rapid technological change are reshaping General Motors’ strategy and risk profile—our concise PESTLE snapshot highlights the forces that matter most to investors and strategists; purchase the full PESTLE to unlock actionable insights, detailed drivers, and mitigation tactics you can use immediately.

Political factors

Trade Policy and International Relations

The ongoing US-China trade tensions materially affect General Motors, which sold 2.9 million vehicles in China in 2023 (about 40% of global sales), exposing GM to tariff risks and regulatory shifts. Tariffs on components and raw materials could raise production costs—China-sourced parts comprised an estimated 28% of GM’s global supply-chain inputs in 2024—squeezing margins. Management must steer geopolitical complexity to preserve profitability in GM’s largest international market.

Government Subsidies and EV Incentives

Federal and state incentives, notably the Inflation Reduction Act's EV tax credits worth up to 7,500 USD, are pivotal in boosting U.S. EV adoption and helped GM report 2024 EV retail growth of roughly 30% year-over-year to support its goal of 1 million annual EV deliveries by 2025.

Labor Union Relations and Domestic Policy

The United Auto Workers' political clout drove GM's 2023-24 contract settlements, raising average hourly wages ~20% for many UAW-represented workers and adding estimated annual labor costs near $1.2–1.5 billion for GM in 2024, pressuring margins. Recent UAW-backed legislation and federal support for domestic manufacturing increase expectations for domestic production and job retention, constraining GM's offshoring options. Balancing political compliance with competitiveness vs non-union peers requires operational efficiency and automation investments to offset elevated labor costs.

Infrastructure Investment for Charging Networks

- 7.5 billion USD federal funding through 2026

- Target: 500,000 public chargers by 2030

- GM lobbying for grants, tax credits and corridor chargers

Geopolitical Stability in Mineral Sourcing

Political instability in lithium- and cobalt-producing regions (e.g., DRC supplies ~70% of cobalt) threatens GM production timelines for EVs and Ultium batteries, risking cost spikes and delays.

GM must pursue strategic diplomacy and multi-year offtake deals—global EV battery contracts reached $30–40 billion in 2024—to secure input flows.

U.S. and allied reshoring incentives (IRA tax credits, $10+ billion in battery processing grants by 2025) are critical to lower dependence on volatile foreign regimes.

- DRC ~70% cobalt supply; Chile/Argentina ~60% lithium brine share

- 2024–25 battery offtake market: $30–40B

- U.S. battery processing grants ≈ $10B+ under IRA by 2025

GM faces China risk, rising UAW costs, IRA EV boost and cobalt supply tension

US-China trade tensions, with China accounting for ~40% of GM global sales (2.9M vehicles in 2023), raise tariff and supply risks; China-sourced parts ~28% of inputs in 2024. IRA EV tax credits (up to $7,500) and $7.5B charging funds through 2026 boost U.S. EV demand; UAW wage rises (~20%, ~$1.2–1.5B annual cost) pressure margins; DRC ~70% cobalt, 2024–25 battery offtake market $30–40B.

| Factor | Key Data |

|---|---|

| China sales | 2.9M (40%) |

| China parts | ~28% |

| IRA credit | up to $7,500 |

| Charging funds | $7.5B (to 2026) |

| UAW cost | ~$1.2–1.5B |

| Cobalt supply | DRC ~70% |

What is included in the product

Explores how external macro-environmental factors uniquely affect General Motors across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify risks and opportunities for executives, consultants, and investors.

A concise PESTLE summary of General Motors, segmented by factor for quick reference, that teams can drop into presentations or strategy packs to streamline risk discussions, enable regional/custom notes, and accelerate alignment across departments.

Economic factors

Interest Rates and Financing Costs

High US interest rates raised average new-vehicle APRs to about 7.5% in 2024, pressuring GM Financial and contributing to a 5–7% decline in retail sales vs. 2023; GM has tightened promotional terms while offering targeted 0.9–3.9% deals to protect margins. Fed tightening increased GM’s weighted average cost of capital, raising financing costs for CAPEX—GM’s 2024 net automotive debt remained ~44 billion USD, heightening sensitivity to rate shifts.

Inflation and Raw Material Volatility

Rising prices for steel (+18% YoY in 2024), aluminum (+12% YoY) and battery-grade lithium/hydroxide (battery chemicals up ~40% since 2022) have driven strong inflationary pressure on GM’s manufacturing costs.

GM leverages hedging and multi-year supply agreements—capital spending on supply contracts rose to $7.5B in 2024—to stabilize input prices.

Despite these measures, sustained inflation risks forcing MSRP increases; GM reported average transaction prices up ~6% in 2024 as it balanced margins and affordability.

Global GDP Growth and Consumer Spending

General Motors' sales are highly cyclical and track global GDP and consumer confidence; global GDP growth slowed to 2.5% in 2024 from 3.4% in 2021, pressuring demand for new SUVs and trucks and contributing to GM's 2024 North America wholesale vehicle unit decline of about 7% year-over-year.

Currency Exchange Rate Fluctuations

As a global automaker, GM faces currency volatility, notably USD/CNY and USD/EUR; a 10% appreciation of the dollar versus the yuan in 2024 would reduce reported RMB revenues by roughly 9–11% after translation, pressuring margins in China where GM earned about $20B in 2024 revenue from joint ventures.

Exchange swings also affect export competitiveness—Euro weakness versus USD in 2025 widened pricing gaps in Europe—while hedging costs rose as GM reported $1.2B in net FX losses in FY2024.

GM treasury uses forwards, FX swaps and options to hedge transactional and translational exposure, with derivatives notional positions exceeding $25B at end-2024 to smooth P&L volatility.

- USD/CNY and USD/EUR moves materially affect translated earnings and export pricing

- ~$20B 2024 China-related revenue sensitive to FX shifts

- $1.2B FX losses reported in FY2024 highlight exposure

- Derivatives notional >$25B end-2024 for hedging

Market Saturation in Mature Economies

The North American and European auto markets are nearing saturation, with light-vehicle sales growth around 1–2% annually and inventory pressures intensifying price competition, reducing organic growth for GM.

GM is reallocating capital into brand differentiation and high-margin segments—luxury EVs and heavy-duty trucks—after 2024 EV margins improved by mid-single digits versus ICE models.

To offset stagnating vehicle volumes, GM is expanding software and autonomous ride-hailing revenue streams via Cruise and OnStar, targeting recurring revenue to lift services share above the current mid-single-digit percent of total revenue.

- North America/Europe sales growth ~1–2% yearly

- 2024 EV margins ~mid-single digits higher vs ICE

- Focus: luxury EVs, heavy-duty trucks, software, Cruise/OnStar

Higher rates, rising input costs and FX hit auto margins; GM leans on hedges & heavy debt

Rising rates (avg new-vehicle APR ~7.5% in 2024) and WACC increases tightened financing; input inflation (steel +18%, aluminum +12%, battery chemicals +~40% since 2022) raised costs; FX volatility (USD strength; $1.2B FY2024 FX losses) and slower global GDP (2.5% in 2024) pressured volumes; GM used >$25B derivatives, $7.5B supply contracts and $44B net automotive debt to hedge and stabilize margins.

| Metric | 2024 |

|---|---|

| New-vehicle APR | ~7.5% |

| Steel price YoY | +18% |

| FX losses | $1.2B |

| Derivatives notional | >$25B |

| Net auto debt | $44B |

What You See Is What You Get

General Motors PESTLE Analysis

The preview shown here is the exact General Motors PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment decisions. The content, layout, and analysis visible are identical to the downloadable file provided upon payment, with no placeholders or surprises. Rely on this complete, final document for immediate application.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and rapid technological change are reshaping General Motors’ strategy and risk profile—our concise PESTLE snapshot highlights the forces that matter most to investors and strategists; purchase the full PESTLE to unlock actionable insights, detailed drivers, and mitigation tactics you can use immediately.

Political factors

Trade Policy and International Relations

The ongoing US-China trade tensions materially affect General Motors, which sold 2.9 million vehicles in China in 2023 (about 40% of global sales), exposing GM to tariff risks and regulatory shifts. Tariffs on components and raw materials could raise production costs—China-sourced parts comprised an estimated 28% of GM’s global supply-chain inputs in 2024—squeezing margins. Management must steer geopolitical complexity to preserve profitability in GM’s largest international market.

Government Subsidies and EV Incentives

Federal and state incentives, notably the Inflation Reduction Act's EV tax credits worth up to 7,500 USD, are pivotal in boosting U.S. EV adoption and helped GM report 2024 EV retail growth of roughly 30% year-over-year to support its goal of 1 million annual EV deliveries by 2025.

Labor Union Relations and Domestic Policy

The United Auto Workers' political clout drove GM's 2023-24 contract settlements, raising average hourly wages ~20% for many UAW-represented workers and adding estimated annual labor costs near $1.2–1.5 billion for GM in 2024, pressuring margins. Recent UAW-backed legislation and federal support for domestic manufacturing increase expectations for domestic production and job retention, constraining GM's offshoring options. Balancing political compliance with competitiveness vs non-union peers requires operational efficiency and automation investments to offset elevated labor costs.

Infrastructure Investment for Charging Networks

- 7.5 billion USD federal funding through 2026

- Target: 500,000 public chargers by 2030

- GM lobbying for grants, tax credits and corridor chargers

Geopolitical Stability in Mineral Sourcing

Political instability in lithium- and cobalt-producing regions (e.g., DRC supplies ~70% of cobalt) threatens GM production timelines for EVs and Ultium batteries, risking cost spikes and delays.

GM must pursue strategic diplomacy and multi-year offtake deals—global EV battery contracts reached $30–40 billion in 2024—to secure input flows.

U.S. and allied reshoring incentives (IRA tax credits, $10+ billion in battery processing grants by 2025) are critical to lower dependence on volatile foreign regimes.

- DRC ~70% cobalt supply; Chile/Argentina ~60% lithium brine share

- 2024–25 battery offtake market: $30–40B

- U.S. battery processing grants ≈ $10B+ under IRA by 2025

GM faces China risk, rising UAW costs, IRA EV boost and cobalt supply tension

US-China trade tensions, with China accounting for ~40% of GM global sales (2.9M vehicles in 2023), raise tariff and supply risks; China-sourced parts ~28% of inputs in 2024. IRA EV tax credits (up to $7,500) and $7.5B charging funds through 2026 boost U.S. EV demand; UAW wage rises (~20%, ~$1.2–1.5B annual cost) pressure margins; DRC ~70% cobalt, 2024–25 battery offtake market $30–40B.

| Factor | Key Data |

|---|---|

| China sales | 2.9M (40%) |

| China parts | ~28% |

| IRA credit | up to $7,500 |

| Charging funds | $7.5B (to 2026) |

| UAW cost | ~$1.2–1.5B |

| Cobalt supply | DRC ~70% |

What is included in the product

Explores how external macro-environmental factors uniquely affect General Motors across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify risks and opportunities for executives, consultants, and investors.

A concise PESTLE summary of General Motors, segmented by factor for quick reference, that teams can drop into presentations or strategy packs to streamline risk discussions, enable regional/custom notes, and accelerate alignment across departments.

Economic factors

Interest Rates and Financing Costs

High US interest rates raised average new-vehicle APRs to about 7.5% in 2024, pressuring GM Financial and contributing to a 5–7% decline in retail sales vs. 2023; GM has tightened promotional terms while offering targeted 0.9–3.9% deals to protect margins. Fed tightening increased GM’s weighted average cost of capital, raising financing costs for CAPEX—GM’s 2024 net automotive debt remained ~44 billion USD, heightening sensitivity to rate shifts.

Inflation and Raw Material Volatility

Rising prices for steel (+18% YoY in 2024), aluminum (+12% YoY) and battery-grade lithium/hydroxide (battery chemicals up ~40% since 2022) have driven strong inflationary pressure on GM’s manufacturing costs.

GM leverages hedging and multi-year supply agreements—capital spending on supply contracts rose to $7.5B in 2024—to stabilize input prices.

Despite these measures, sustained inflation risks forcing MSRP increases; GM reported average transaction prices up ~6% in 2024 as it balanced margins and affordability.

Global GDP Growth and Consumer Spending

General Motors' sales are highly cyclical and track global GDP and consumer confidence; global GDP growth slowed to 2.5% in 2024 from 3.4% in 2021, pressuring demand for new SUVs and trucks and contributing to GM's 2024 North America wholesale vehicle unit decline of about 7% year-over-year.

Currency Exchange Rate Fluctuations

As a global automaker, GM faces currency volatility, notably USD/CNY and USD/EUR; a 10% appreciation of the dollar versus the yuan in 2024 would reduce reported RMB revenues by roughly 9–11% after translation, pressuring margins in China where GM earned about $20B in 2024 revenue from joint ventures.

Exchange swings also affect export competitiveness—Euro weakness versus USD in 2025 widened pricing gaps in Europe—while hedging costs rose as GM reported $1.2B in net FX losses in FY2024.

GM treasury uses forwards, FX swaps and options to hedge transactional and translational exposure, with derivatives notional positions exceeding $25B at end-2024 to smooth P&L volatility.

- USD/CNY and USD/EUR moves materially affect translated earnings and export pricing

- ~$20B 2024 China-related revenue sensitive to FX shifts

- $1.2B FX losses reported in FY2024 highlight exposure

- Derivatives notional >$25B end-2024 for hedging

Market Saturation in Mature Economies

The North American and European auto markets are nearing saturation, with light-vehicle sales growth around 1–2% annually and inventory pressures intensifying price competition, reducing organic growth for GM.

GM is reallocating capital into brand differentiation and high-margin segments—luxury EVs and heavy-duty trucks—after 2024 EV margins improved by mid-single digits versus ICE models.

To offset stagnating vehicle volumes, GM is expanding software and autonomous ride-hailing revenue streams via Cruise and OnStar, targeting recurring revenue to lift services share above the current mid-single-digit percent of total revenue.

- North America/Europe sales growth ~1–2% yearly

- 2024 EV margins ~mid-single digits higher vs ICE

- Focus: luxury EVs, heavy-duty trucks, software, Cruise/OnStar

Higher rates, rising input costs and FX hit auto margins; GM leans on hedges & heavy debt

Rising rates (avg new-vehicle APR ~7.5% in 2024) and WACC increases tightened financing; input inflation (steel +18%, aluminum +12%, battery chemicals +~40% since 2022) raised costs; FX volatility (USD strength; $1.2B FY2024 FX losses) and slower global GDP (2.5% in 2024) pressured volumes; GM used >$25B derivatives, $7.5B supply contracts and $44B net automotive debt to hedge and stabilize margins.

| Metric | 2024 |

|---|---|

| New-vehicle APR | ~7.5% |

| Steel price YoY | +18% |

| FX losses | $1.2B |

| Derivatives notional | >$25B |

| Net auto debt | $44B |

What You See Is What You Get

General Motors PESTLE Analysis

The preview shown here is the exact General Motors PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment decisions. The content, layout, and analysis visible are identical to the downloadable file provided upon payment, with no placeholders or surprises. Rely on this complete, final document for immediate application.