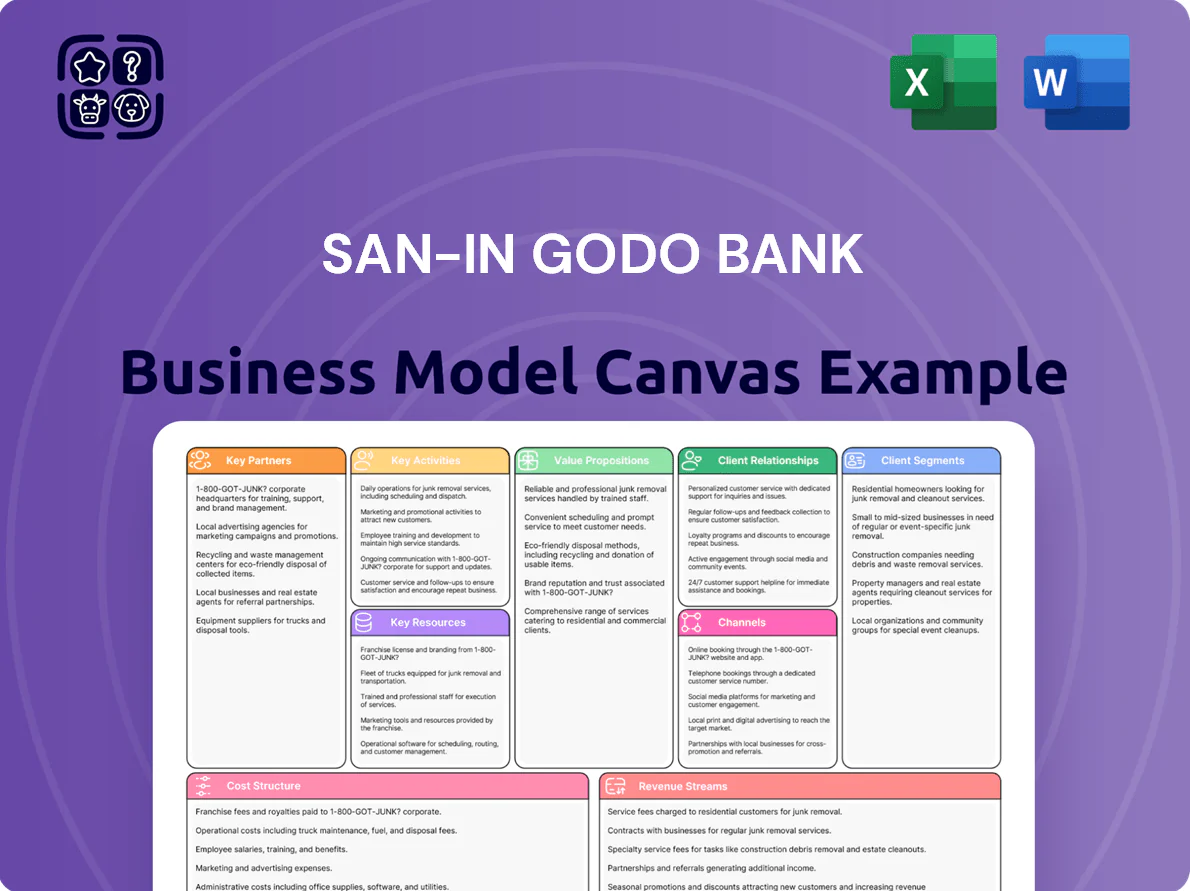

San-In Godo Bank Business Model Canvas

San-In Godo Bank: Actionable Business Model Canvas for Investors & Strategists

Unlock the full strategic blueprint behind San-In Godo Bank’s business model—this in-depth Business Model Canvas exposes how the bank creates customer value, leverages regional partnerships, and sustains profitability in a competitive market; ideal for investors, consultants, and entrepreneurs seeking actionable, ready-to-use insights to benchmark or adapt.

Partnerships

Strategic Alliance with Nomura Securities

The bank partners with Nomura Securities to deliver advanced asset management to the San-in region, leveraging Nomura’s national reach and San-In Godo Bank’s local branch network to serve wealthy clients; joint AUM reached about ¥45 billion as of Dec 2025, up 18% year-on-year.

Local Government and Municipalities

San-In Godo Bank partners with Shimane and Tottori prefectural governments as lead financier for regional revitalization, underwriting about ¥48.5 billion in public-sector loans and ¥6.2 billion in infrastructure bonds in FY2024, supporting projects from port upgrades to eldercare facilities; these ties secure roughly 22% of the bank’s fee and loan income and bolster its community standing and long-term stable cash flow.

Regional Revitalization Funds

The bank partners with private equity firms and local investment funds to inject equity and operational expertise into struggling SMEs and startups, co-investing in 48 projects worth ¥9.6 billion in 2024 to sustain jobs and supply chains in the San-In region.

Fintech and IT Solution Providers

San-In Godo Bank partners with fintechs and IT vendors to speed digital transformation, adding biometric login and robo-advisory tools to mobile banking and back-office systems; such deals cut digital service rollout from ~12 months to ~4 months and helped mobile active users grow 28% YoY to 210,000 in 2024.

These partnerships target younger customers—ages 20–39 made up 42% of new accounts in 2024—helping retention as 67% of that cohort prefer digital-first banking per the bank’s 2024 CX survey.

- Biometric auth: live 2024

- Robo-advice: pilot Q3 2024

- Digital rollout time: 12→4 months

- Mobile users: 210,000 (2024)

- New-account youth share: 42% (2024)

Credit Guarantee Corporations

Working with regional credit guarantee corporations lets San-In Godo Bank lend to SMEs with weak collateral by shifting default risk; guarantees covered about 40% of SME loan balances in the San-In region in 2024, cutting net charge-offs on guaranteed loans by roughly 60% year-over-year.

This partnership ensures local entrepreneurs get vital liquidity, aligns with the bank’s SME strategy targeting a 15% portfolio share by 2026, and supports credit growth while keeping CET1 ratios stable.

- Guarantees cover ~40% of SME loans (2024)

- Net charge-offs down ~60% on guaranteed loans

- SME portfolio target 15% by 2026

San-In Godo Bank boosts growth via Nomura wealth, prefectures, PE, fintech & guarantees

San-In Godo Bank leverages Nomura for wealth management (AUM ≈ ¥45bn, +18% YoY), prefectural ties for public-sector lending (¥48.5bn loans, ¥6.2bn bonds, ~22% income), PE/local funds for 48 co-investments (¥9.6bn), fintechs for digital (biometric live 2024; robo pilot Q3 2024; mobile users 210,000), and credit guarantees covering ~40% of SME loans (net charge-offs -60%).

| Partner | Key metric |

|---|---|

| Nomura | AUM ¥45bn |

| Prefectures | Loans ¥48.5bn |

| PE/funds | Co-invest ¥9.6bn |

| Fintechs | Mobile 210,000 |

| Guarantees | Cover 40% |

What is included in the product

A concise, pre-written Business Model Canvas for San-In Godo Bank outlining customer segments, channels, value propositions, revenue streams, key activities, resources, partnerships, cost structure and risk profile, reflecting real-world regional banking operations and strategic priorities for presentations, investor discussions and internal planning.

High-level view of San-In Godo Bank’s business model with editable cells to quickly pinpoint how regional banking services, fee income, and lending practices alleviate customer pain points and guide strategic decisions.

Activities

Retail and Corporate Lending

The bank focuses on housing loans to individuals and capital-investment loans to businesses, driving 72% of net interest income in FY2024 and supporting regional GDP via ¥125bn in new lending in 2024. By scoring credit risk with local-market data and keeping NPLs at 0.9% (2024), the portfolio stays healthy while funding housing and SME growth.

Wealth Management and Advisory

Following its 2024 alliance with Nomura, San-In Godo Bank shifted toward comprehensive wealth management, with staff offering personalized investment advice, inheritance planning, and asset-allocation strategies for HNW clients; fee income from wealth services rose to 18% of non-interest income in FY2024, helping reduce reliance on net interest margin, which fell to 0.65% in FY2024.

Digital Banking Transformation

San-In Godo Bank is upgrading digital infrastructure to deliver a seamless omnichannel experience, launching a redesigned mobile app in Q4 2025 and targeting 40% mobile active users by end-2026 (currently 22% in 2024); back-office automation via RPA and straight-through processing aims to cut processing costs 18–25% and reduce turnaround time by 60%, lowering operating expense ratio toward the regional peer median of ~45%.

Business Matching and Consulting

Risk Management and Compliance

San-In Godo Bank keeps financial stability by monitoring market volatility and credit exposure—daily VaR checks and quarterly stress tests; loan NPL ratio stood at 1.2% as of FY2024, and CET1-equivalent capital ratio was ~12.8% at 31 Dec 2024.

The bank spends ~¥1.5bn annually on compliance and IT security (2024), meeting AML and J-SOX requirements and implementing SOC2-like controls to protect depositor trust and regional stability.

- Daily VaR, quarterly stress tests

- NPL 1.2% (FY2024)

- CET1 ~12.8% (31‑Dec‑2024)

- Compliance/IT spend ≈ ¥1.5bn (2024)

Housing & SME lending fuels NII; digital push to double mobile users, CET1 ~12.8%

Focuses on housing and SME lending (¥125bn new loans in 2024) driving 72% of NII; wealth-management fees rose to 18% of non-interest income after 2024 Nomura tie-up; digital upgrades target 40% mobile users by end-2026 (22% in 2024) and 18–25% back-office cost cuts via RPA; NPL 1.2% and CET1 ~12.8% (31‑Dec‑2024).

| Metric | Value |

|---|---|

| New lending 2024 | ¥125bn |

| NII from loans | 72% |

| Wealth fees | 18% of non-interest income (2024) |

| Mobile users | 22% (2024), target 40% end‑2026 |

| NPL ratio | 1.2% (FY2024) |

| CET1-equivalent | ~12.8% (31‑Dec‑2024) |

| Compliance/IT spend | ≈ ¥1.5bn (2024) |

Full Document Unlocks After Purchase

Business Model Canvas

The preview shown here is the real San-In Godo Bank Business Model Canvas—not a mockup—and it reflects the exact document you will receive after purchase.

When you complete your order you’ll get full access to this same, professionally formatted file ready for editing, presenting, or sharing.

No placeholders or sample pages—what you see in this preview is the actual deliverable, delivered in its complete form.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

San-In Godo Bank: Actionable Business Model Canvas for Investors & Strategists

Unlock the full strategic blueprint behind San-In Godo Bank’s business model—this in-depth Business Model Canvas exposes how the bank creates customer value, leverages regional partnerships, and sustains profitability in a competitive market; ideal for investors, consultants, and entrepreneurs seeking actionable, ready-to-use insights to benchmark or adapt.

Partnerships

Strategic Alliance with Nomura Securities

The bank partners with Nomura Securities to deliver advanced asset management to the San-in region, leveraging Nomura’s national reach and San-In Godo Bank’s local branch network to serve wealthy clients; joint AUM reached about ¥45 billion as of Dec 2025, up 18% year-on-year.

Local Government and Municipalities

San-In Godo Bank partners with Shimane and Tottori prefectural governments as lead financier for regional revitalization, underwriting about ¥48.5 billion in public-sector loans and ¥6.2 billion in infrastructure bonds in FY2024, supporting projects from port upgrades to eldercare facilities; these ties secure roughly 22% of the bank’s fee and loan income and bolster its community standing and long-term stable cash flow.

Regional Revitalization Funds

The bank partners with private equity firms and local investment funds to inject equity and operational expertise into struggling SMEs and startups, co-investing in 48 projects worth ¥9.6 billion in 2024 to sustain jobs and supply chains in the San-In region.

Fintech and IT Solution Providers

San-In Godo Bank partners with fintechs and IT vendors to speed digital transformation, adding biometric login and robo-advisory tools to mobile banking and back-office systems; such deals cut digital service rollout from ~12 months to ~4 months and helped mobile active users grow 28% YoY to 210,000 in 2024.

These partnerships target younger customers—ages 20–39 made up 42% of new accounts in 2024—helping retention as 67% of that cohort prefer digital-first banking per the bank’s 2024 CX survey.

- Biometric auth: live 2024

- Robo-advice: pilot Q3 2024

- Digital rollout time: 12→4 months

- Mobile users: 210,000 (2024)

- New-account youth share: 42% (2024)

Credit Guarantee Corporations

Working with regional credit guarantee corporations lets San-In Godo Bank lend to SMEs with weak collateral by shifting default risk; guarantees covered about 40% of SME loan balances in the San-In region in 2024, cutting net charge-offs on guaranteed loans by roughly 60% year-over-year.

This partnership ensures local entrepreneurs get vital liquidity, aligns with the bank’s SME strategy targeting a 15% portfolio share by 2026, and supports credit growth while keeping CET1 ratios stable.

- Guarantees cover ~40% of SME loans (2024)

- Net charge-offs down ~60% on guaranteed loans

- SME portfolio target 15% by 2026

San-In Godo Bank boosts growth via Nomura wealth, prefectures, PE, fintech & guarantees

San-In Godo Bank leverages Nomura for wealth management (AUM ≈ ¥45bn, +18% YoY), prefectural ties for public-sector lending (¥48.5bn loans, ¥6.2bn bonds, ~22% income), PE/local funds for 48 co-investments (¥9.6bn), fintechs for digital (biometric live 2024; robo pilot Q3 2024; mobile users 210,000), and credit guarantees covering ~40% of SME loans (net charge-offs -60%).

| Partner | Key metric |

|---|---|

| Nomura | AUM ¥45bn |

| Prefectures | Loans ¥48.5bn |

| PE/funds | Co-invest ¥9.6bn |

| Fintechs | Mobile 210,000 |

| Guarantees | Cover 40% |

What is included in the product

A concise, pre-written Business Model Canvas for San-In Godo Bank outlining customer segments, channels, value propositions, revenue streams, key activities, resources, partnerships, cost structure and risk profile, reflecting real-world regional banking operations and strategic priorities for presentations, investor discussions and internal planning.

High-level view of San-In Godo Bank’s business model with editable cells to quickly pinpoint how regional banking services, fee income, and lending practices alleviate customer pain points and guide strategic decisions.

Activities

Retail and Corporate Lending

The bank focuses on housing loans to individuals and capital-investment loans to businesses, driving 72% of net interest income in FY2024 and supporting regional GDP via ¥125bn in new lending in 2024. By scoring credit risk with local-market data and keeping NPLs at 0.9% (2024), the portfolio stays healthy while funding housing and SME growth.

Wealth Management and Advisory

Following its 2024 alliance with Nomura, San-In Godo Bank shifted toward comprehensive wealth management, with staff offering personalized investment advice, inheritance planning, and asset-allocation strategies for HNW clients; fee income from wealth services rose to 18% of non-interest income in FY2024, helping reduce reliance on net interest margin, which fell to 0.65% in FY2024.

Digital Banking Transformation

San-In Godo Bank is upgrading digital infrastructure to deliver a seamless omnichannel experience, launching a redesigned mobile app in Q4 2025 and targeting 40% mobile active users by end-2026 (currently 22% in 2024); back-office automation via RPA and straight-through processing aims to cut processing costs 18–25% and reduce turnaround time by 60%, lowering operating expense ratio toward the regional peer median of ~45%.

Business Matching and Consulting

Risk Management and Compliance

San-In Godo Bank keeps financial stability by monitoring market volatility and credit exposure—daily VaR checks and quarterly stress tests; loan NPL ratio stood at 1.2% as of FY2024, and CET1-equivalent capital ratio was ~12.8% at 31 Dec 2024.

The bank spends ~¥1.5bn annually on compliance and IT security (2024), meeting AML and J-SOX requirements and implementing SOC2-like controls to protect depositor trust and regional stability.

- Daily VaR, quarterly stress tests

- NPL 1.2% (FY2024)

- CET1 ~12.8% (31‑Dec‑2024)

- Compliance/IT spend ≈ ¥1.5bn (2024)

Housing & SME lending fuels NII; digital push to double mobile users, CET1 ~12.8%

Focuses on housing and SME lending (¥125bn new loans in 2024) driving 72% of NII; wealth-management fees rose to 18% of non-interest income after 2024 Nomura tie-up; digital upgrades target 40% mobile users by end-2026 (22% in 2024) and 18–25% back-office cost cuts via RPA; NPL 1.2% and CET1 ~12.8% (31‑Dec‑2024).

| Metric | Value |

|---|---|

| New lending 2024 | ¥125bn |

| NII from loans | 72% |

| Wealth fees | 18% of non-interest income (2024) |

| Mobile users | 22% (2024), target 40% end‑2026 |

| NPL ratio | 1.2% (FY2024) |

| CET1-equivalent | ~12.8% (31‑Dec‑2024) |

| Compliance/IT spend | ≈ ¥1.5bn (2024) |

Full Document Unlocks After Purchase

Business Model Canvas

The preview shown here is the real San-In Godo Bank Business Model Canvas—not a mockup—and it reflects the exact document you will receive after purchase.

When you complete your order you’ll get full access to this same, professionally formatted file ready for editing, presenting, or sharing.

No placeholders or sample pages—what you see in this preview is the actual deliverable, delivered in its complete form.