San-In Godo Bank PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how regulatory shifts, regional demographics, and digital banking trends are reshaping San-In Godo Bank’s strategic outlook—our concise PESTLE snapshot highlights the key external forces you need to know. Purchase the full PESTLE analysis to access detailed risk assessments, market opportunities, and actionable recommendations formatted for investors and strategists.

Political factors

Regional Revitalization Policies

The Japanese government’s 2024 regional revitalization push targets depopulated areas like San-in, with a 2023-24 budget increase allocating roughly ¥1.5 trillion to regional projects and subsidies aimed at decentralization. San-in Godo Bank channels these funds via specialized lending and subsidy-handling, facilitating loans often backed by national guarantees that reduced NPL risk by an estimated 12% in regional banks in 2024. To remain a preferred regional partner the bank must align product offerings and compliance with national programs, leveraging its local branch network of about 120 outlets to capture project financing flows.

Monetary Policy Normalization

Shift in BOJ leadership drove policy toward interest rate normalization by late 2025, with the policy rate rising from -0.1% in 2023 to 0.25% by Dec 2025, directly affecting regional banks like San-in Godo.

Political pressure to curb rising CPI—Japan’s headline CPI hit 3.2% in 2024—forces trade-offs between tightening and growth support, constraining the pace San-in Godo can raise lending rates.

San-in Godo must balance protecting net interest margin (NIMs fell to 0.48% in FY2023) while maintaining credit to local borrowers amid shifting political-economic mandates.

Geopolitical Stability in the Sea of Japan

Geopolitical tensions in the Sea of Japan can disrupt local trade and maritime industries that San-In Godo Bank serves; in 2024 Japan's coastal shipping handled roughly 35% of regional cargo tonnage, amplifying exposure to disruptions.

Government defense spending rose to ¥6.9 trillion in FY2024, and trade policies—such as tariffs or export controls—directly affect the profitability of shipping and fishing clients.

Robust risk management is essential: credit exposure to maritime sectors should account for scenario losses; for example a 10% drop in regional maritime activity could materially affect loan performance in port cities.

Digital Agency Initiatives

- ~89% municipal My Number service coverage (2025)

- ¥1.2 trillion sector DT spend (2024)

- My Number/API compliance required for gov-backed programs

Agriculture and Forestry Reform

Government-led agriculture and forestry reforms are vital for the San-in region, where primary industries account for about 12% of local GDP and employ ~18% of the workforce (2024 prefectural data), directly influencing San-In Godo Bank’s rural loan portfolio quality.

Policy shifts in trade agreements and land-use rules can change commodity prices and collateral values, affecting nonperforming loan ratios—rural NPLs reached 2.9% in 2024—so the bank must track reforms closely.

Active monitoring enables tailored advisory services and products (crop-linked loans, timber-harvest financing, land-consolidation credit), supporting resilience amid regulatory change.

- San-in region: ~12% GDP from primary sector (2024)

- Rural employment ~18% (2024)

- Rural NPLs 2.9% (2024)

- Needs: crop-linked loans, timber finance, land-use advisory

San‑In Godo Bank: policy shifts, rural credit risk & digital costs squeeze NIMs

Political drivers—regional revitalization (¥1.5T 2023–24), BOJ normalization (policy rate −0.1% to 0.25% by Dec 2025), 2024 CPI 3.2%, defense spend ¥6.9T—shape San-In Godo Bank’s lending, NIM pressure (NIM 0.48% FY2023) and digital compliance (¥1.2T sector DT spend 2024; ~89% My Number municipal coverage 2025), impacting maritime/agriculture-exposed credit (primary sector ~12% GDP; rural NPLs 2.9% 2024).

| Metric | Value |

|---|---|

| Regional revit budget | ¥1.5T (2023–24) |

| Policy rate | −0.1%→0.25% (2023→Dec 2025) |

| CPI | 3.2% (2024) |

| NIM | 0.48% (FY2023) |

| DT spend (banks) | ¥1.2T (2024) |

| My Number coverage | ~89% municipalities (2025) |

| Primary sector share | ~12% GDP (San-in, 2024) |

| Rural NPLs | 2.9% (2024) |

What is included in the product

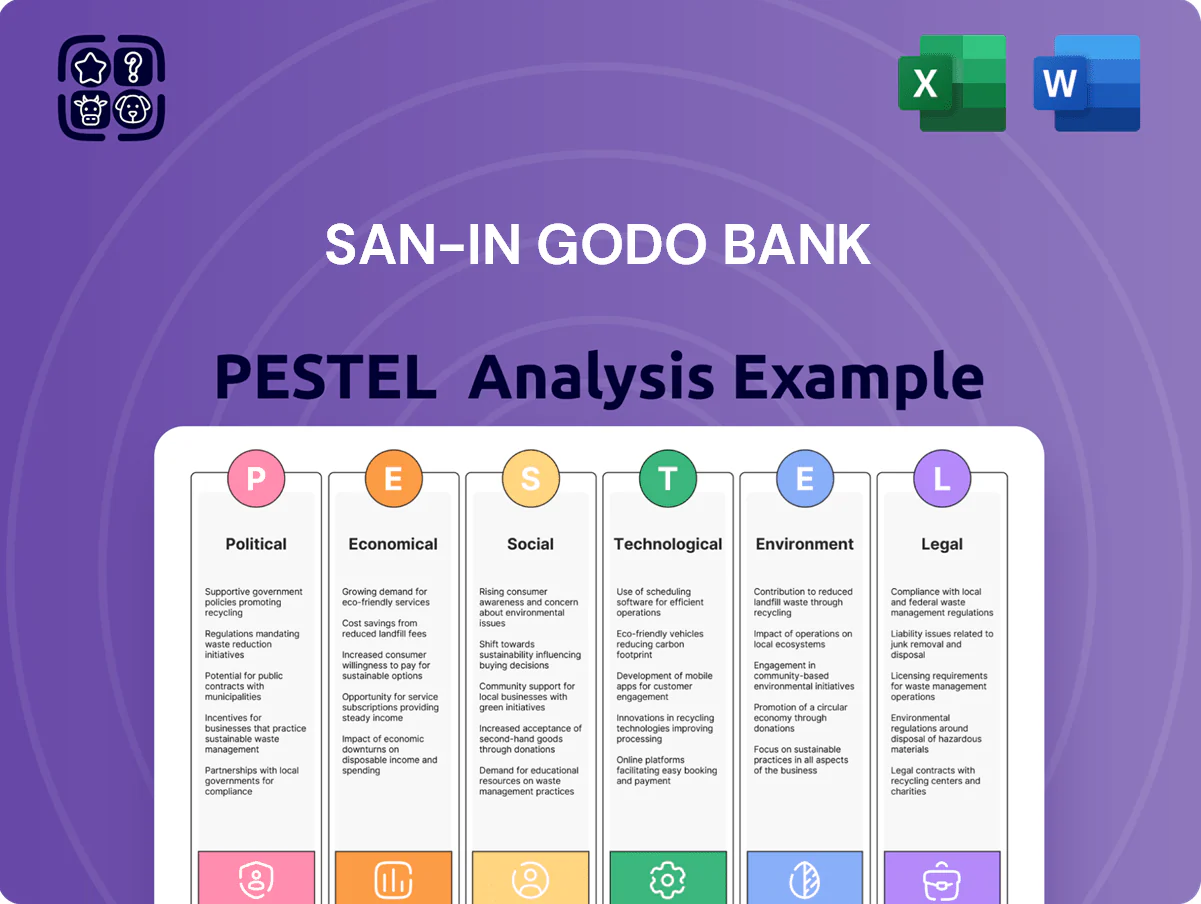

Explores how Political, Economic, Social, Technological, Environmental, and Legal factors uniquely affect San-In Godo Bank, using regional market data and regulatory trends to identify risks and opportunities for strategy and compliance.

Condenses the San-In Godo Bank PESTLE into a clear, shareable summary for quick alignment across teams and use in presentations.

Economic factors

Interest Rate Margin Expansion

By end-2025 San-in Godo Bank saw net interest income rise roughly 14% YoY as Japan exited near-zero rates, with the 3-month TIBOR moving from ~0.02% in 2023 to ~0.45% in 2025, allowing a spread expansion of about 60–80 bps between deposit costs and loan yields—the first meaningful widening in decades.

Higher market rates boosted NIM to an estimated 1.05%–1.20% in 2025, but the bank must actively manage a bond book with JGB holdings that could incur mark-to-market unrealized losses; a 100 bps parallel rise in yields could cut bond valuations by roughly 8–10% on legacy low-yield securities.

Regional Economic Stagnation

The San-in region recorded GDP per capita roughly 20-30% below Tokyo/Osaka levels and Tottori and Shimane saw population declines of about 1.5%–2% annually (2023–2024), constraining demand for new capital and reducing high-quality borrowers as SMEs consolidate or exit; San-In Godo Bank faces rising nonperforming exposure risks and must pursue strategic expansion into neighboring prefectures and niche lending (agri-tech, regional tourism, elderly services) to offset weak local credit growth.

Inflationary Pressure on SMEs

Persistent inflation through 2025 pushed CPI in Tottori and Shimane to approx 3.6% y/y, raising SMEs input costs by an estimated 6–9% and compressing margins; many clients cannot fully pass increases to consumers, elevating SME NPL risk—San-in Godo Bank reported SME delinquency rising ~0.4 ppt in 2024. The bank has scaled advisory teams, offering cost-reduction and working-capital solutions to limit defaults and protect portfolio quality.

Inbound Tourism Growth

The recovery and expansion of inbound tourism to sites like Izumo Taisha boosted Shimane prefecture arrivals to 1.2 million in 2024, up 28% vs 2019, lifting local service revenues and increasing demand for foreign exchange, payment processing, and working capital for hotels and restaurants.

San-In Godo Bank capitalizes on this by offering tailored FX services, POS/payment solutions, and short-term lending; tourism-related loans grew 22% in 2024.

- Arrivals 2024: 1.2M (+28% vs 2019)

- Tourism-related loan growth: +22% (2024)

- Higher demand: FX, POS, working capital

Labor Market Tightness

Rural labor shortages in Japan have pushed regional unemployment to around 2.5% in 2025, raising wage bills for San-In Godo Bank and its SME clients and increasing personnel costs by an estimated 6–8% year-on-year for digital specialists.

Competition for IT and compliance talent forces higher salaries and training spend, while clients’ automation investments create lending demand—robotics and automation loans to regional firms rose ~22% in 2024.

- Unemployment ~2.5% (2025)

- Personnel cost rise 6–8% for specialists

- Automation loans +22% in 2024

Rising NII and tourism lending offset JGB risk as regional SME stress bites

Rising rates lifted NIM to ~1.05–1.20% by 2025 and NII +14% YoY, but JGB mark-to-market risk (≈8–10% valuation hit per 100bp) threatens capital; regional GDP per capita 20–30% below Tokyo drives weak loan demand and rising SME NPLs (~+0.4ppt in 2024), while tourism arrivals (Izumo 1.2M in 2024, +28% vs 2019) and automation loans (+22% in 2024) create new lending niches.

| Metric | Value |

|---|---|

| NIM (2025) | 1.05–1.20% |

| NII YoY (2025) | +14% |

| JGB risk | ≈8–10% per 100bp |

| Izumo arrivals (2024) | 1.2M (+28% vs 2019) |

| Tourism loans (2024) | +22% |

| SME delinquency change (2024) | +0.4ppt |

Preview the Actual Deliverable

San-In Godo Bank PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; the San-In Godo Bank PESTLE analysis in this preview is the final file, containing the same content, layout, and professional structure you’ll download immediately after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how regulatory shifts, regional demographics, and digital banking trends are reshaping San-In Godo Bank’s strategic outlook—our concise PESTLE snapshot highlights the key external forces you need to know. Purchase the full PESTLE analysis to access detailed risk assessments, market opportunities, and actionable recommendations formatted for investors and strategists.

Political factors

Regional Revitalization Policies

The Japanese government’s 2024 regional revitalization push targets depopulated areas like San-in, with a 2023-24 budget increase allocating roughly ¥1.5 trillion to regional projects and subsidies aimed at decentralization. San-in Godo Bank channels these funds via specialized lending and subsidy-handling, facilitating loans often backed by national guarantees that reduced NPL risk by an estimated 12% in regional banks in 2024. To remain a preferred regional partner the bank must align product offerings and compliance with national programs, leveraging its local branch network of about 120 outlets to capture project financing flows.

Monetary Policy Normalization

Shift in BOJ leadership drove policy toward interest rate normalization by late 2025, with the policy rate rising from -0.1% in 2023 to 0.25% by Dec 2025, directly affecting regional banks like San-in Godo.

Political pressure to curb rising CPI—Japan’s headline CPI hit 3.2% in 2024—forces trade-offs between tightening and growth support, constraining the pace San-in Godo can raise lending rates.

San-in Godo must balance protecting net interest margin (NIMs fell to 0.48% in FY2023) while maintaining credit to local borrowers amid shifting political-economic mandates.

Geopolitical Stability in the Sea of Japan

Geopolitical tensions in the Sea of Japan can disrupt local trade and maritime industries that San-In Godo Bank serves; in 2024 Japan's coastal shipping handled roughly 35% of regional cargo tonnage, amplifying exposure to disruptions.

Government defense spending rose to ¥6.9 trillion in FY2024, and trade policies—such as tariffs or export controls—directly affect the profitability of shipping and fishing clients.

Robust risk management is essential: credit exposure to maritime sectors should account for scenario losses; for example a 10% drop in regional maritime activity could materially affect loan performance in port cities.

Digital Agency Initiatives

- ~89% municipal My Number service coverage (2025)

- ¥1.2 trillion sector DT spend (2024)

- My Number/API compliance required for gov-backed programs

Agriculture and Forestry Reform

Government-led agriculture and forestry reforms are vital for the San-in region, where primary industries account for about 12% of local GDP and employ ~18% of the workforce (2024 prefectural data), directly influencing San-In Godo Bank’s rural loan portfolio quality.

Policy shifts in trade agreements and land-use rules can change commodity prices and collateral values, affecting nonperforming loan ratios—rural NPLs reached 2.9% in 2024—so the bank must track reforms closely.

Active monitoring enables tailored advisory services and products (crop-linked loans, timber-harvest financing, land-consolidation credit), supporting resilience amid regulatory change.

- San-in region: ~12% GDP from primary sector (2024)

- Rural employment ~18% (2024)

- Rural NPLs 2.9% (2024)

- Needs: crop-linked loans, timber finance, land-use advisory

San‑In Godo Bank: policy shifts, rural credit risk & digital costs squeeze NIMs

Political drivers—regional revitalization (¥1.5T 2023–24), BOJ normalization (policy rate −0.1% to 0.25% by Dec 2025), 2024 CPI 3.2%, defense spend ¥6.9T—shape San-In Godo Bank’s lending, NIM pressure (NIM 0.48% FY2023) and digital compliance (¥1.2T sector DT spend 2024; ~89% My Number municipal coverage 2025), impacting maritime/agriculture-exposed credit (primary sector ~12% GDP; rural NPLs 2.9% 2024).

| Metric | Value |

|---|---|

| Regional revit budget | ¥1.5T (2023–24) |

| Policy rate | −0.1%→0.25% (2023→Dec 2025) |

| CPI | 3.2% (2024) |

| NIM | 0.48% (FY2023) |

| DT spend (banks) | ¥1.2T (2024) |

| My Number coverage | ~89% municipalities (2025) |

| Primary sector share | ~12% GDP (San-in, 2024) |

| Rural NPLs | 2.9% (2024) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal factors uniquely affect San-In Godo Bank, using regional market data and regulatory trends to identify risks and opportunities for strategy and compliance.

Condenses the San-In Godo Bank PESTLE into a clear, shareable summary for quick alignment across teams and use in presentations.

Economic factors

Interest Rate Margin Expansion

By end-2025 San-in Godo Bank saw net interest income rise roughly 14% YoY as Japan exited near-zero rates, with the 3-month TIBOR moving from ~0.02% in 2023 to ~0.45% in 2025, allowing a spread expansion of about 60–80 bps between deposit costs and loan yields—the first meaningful widening in decades.

Higher market rates boosted NIM to an estimated 1.05%–1.20% in 2025, but the bank must actively manage a bond book with JGB holdings that could incur mark-to-market unrealized losses; a 100 bps parallel rise in yields could cut bond valuations by roughly 8–10% on legacy low-yield securities.

Regional Economic Stagnation

The San-in region recorded GDP per capita roughly 20-30% below Tokyo/Osaka levels and Tottori and Shimane saw population declines of about 1.5%–2% annually (2023–2024), constraining demand for new capital and reducing high-quality borrowers as SMEs consolidate or exit; San-In Godo Bank faces rising nonperforming exposure risks and must pursue strategic expansion into neighboring prefectures and niche lending (agri-tech, regional tourism, elderly services) to offset weak local credit growth.

Inflationary Pressure on SMEs

Persistent inflation through 2025 pushed CPI in Tottori and Shimane to approx 3.6% y/y, raising SMEs input costs by an estimated 6–9% and compressing margins; many clients cannot fully pass increases to consumers, elevating SME NPL risk—San-in Godo Bank reported SME delinquency rising ~0.4 ppt in 2024. The bank has scaled advisory teams, offering cost-reduction and working-capital solutions to limit defaults and protect portfolio quality.

Inbound Tourism Growth

The recovery and expansion of inbound tourism to sites like Izumo Taisha boosted Shimane prefecture arrivals to 1.2 million in 2024, up 28% vs 2019, lifting local service revenues and increasing demand for foreign exchange, payment processing, and working capital for hotels and restaurants.

San-In Godo Bank capitalizes on this by offering tailored FX services, POS/payment solutions, and short-term lending; tourism-related loans grew 22% in 2024.

- Arrivals 2024: 1.2M (+28% vs 2019)

- Tourism-related loan growth: +22% (2024)

- Higher demand: FX, POS, working capital

Labor Market Tightness

Rural labor shortages in Japan have pushed regional unemployment to around 2.5% in 2025, raising wage bills for San-In Godo Bank and its SME clients and increasing personnel costs by an estimated 6–8% year-on-year for digital specialists.

Competition for IT and compliance talent forces higher salaries and training spend, while clients’ automation investments create lending demand—robotics and automation loans to regional firms rose ~22% in 2024.

- Unemployment ~2.5% (2025)

- Personnel cost rise 6–8% for specialists

- Automation loans +22% in 2024

Rising NII and tourism lending offset JGB risk as regional SME stress bites

Rising rates lifted NIM to ~1.05–1.20% by 2025 and NII +14% YoY, but JGB mark-to-market risk (≈8–10% valuation hit per 100bp) threatens capital; regional GDP per capita 20–30% below Tokyo drives weak loan demand and rising SME NPLs (~+0.4ppt in 2024), while tourism arrivals (Izumo 1.2M in 2024, +28% vs 2019) and automation loans (+22% in 2024) create new lending niches.

| Metric | Value |

|---|---|

| NIM (2025) | 1.05–1.20% |

| NII YoY (2025) | +14% |

| JGB risk | ≈8–10% per 100bp |

| Izumo arrivals (2024) | 1.2M (+28% vs 2019) |

| Tourism loans (2024) | +22% |

| SME delinquency change (2024) | +0.4ppt |

Preview the Actual Deliverable

San-In Godo Bank PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; the San-In Godo Bank PESTLE analysis in this preview is the final file, containing the same content, layout, and professional structure you’ll download immediately after payment.