InterGlobe Aviation Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

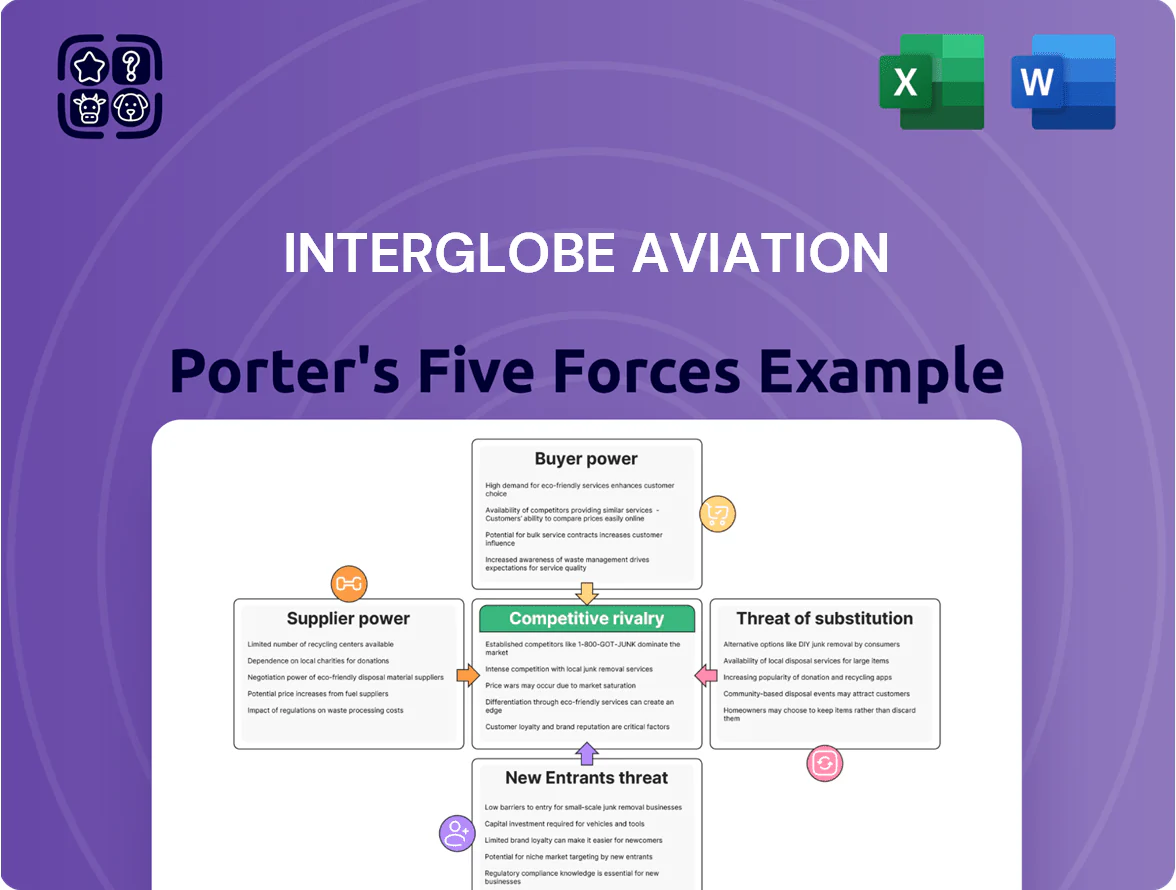

InterGlobe Aviation faces intense rivalry, regulatory headwinds, and capital-hungry suppliers, while buyer power and substitutes exert mixed pressure on margins—this snapshot highlights key competitive tensions shaping its strategy.

Suppliers Bargaining Power

Concentrated Aircraft Manufacturing Duopoly

The global commercial-aircraft market is a Boeing-Airbus duopoly, leaving IndiGo with few procurement alternatives; as of late 2025 IndiGo’s fleet is ~99% Airbus A320 family with ~430 A320neo-family orders outstanding, constraining its bargaining options.

Engine Manufacturer Technical Dependencies

IndiGo suffered major disruptions from 2016–2018 Pratt & Whitney PW1100G issues, costing estimated revenue losses of ~INR 3.5–4.0 billion in 2016–17 and grounding rates spiking 15–20%—showing clear supplier power.

Shift to CFM International LEAP engines for A320neo deliveries reduced exposure, but certified-provider scarcity creates lock-in for spares and shop visits.

By end-2025 only two OEMs (Pratt & Whitney, CFM) dominate certified narrowbody engines, keeping bargaining power high over maintenance pricing and MTBUR (mean time between unplanned removals) guarantees.

Volatility of Aviation Turbine Fuel Providers

Fuel is IndiGo's largest operating cost, accounting for about 28% of total expenses in FY2024 (InterGlobe Aviation), and supply is concentrated among a few state and private oil marketers in India, giving suppliers strong leverage.

Jet fuel prices track global crude benchmarks plus local duties, so IndiGo is a price taker with little control over base costs; jet fuel averaged ~USD 90–100/bbl in 2024, pushing jet-fuel bill above INR 25,000 crore.

With no scalable alternative energy for narrow-body jets by 2025, suppliers retain dominant bargaining power, raising IndiGo's exposure to oil-price swings and policy-driven tax shifts.

Airport Infrastructure and Slot Constraints

Major hubs Delhi, Mumbai and Bengaluru are run by a handful of private operators or the Airports Authority of India, creating localized monopolies for ground services that raise switching costs for carriers.

India saw a record 210 million domestic passengers in 2025, pushing peak-hour slot scarcity; prime slots command higher aeronautical fees, giving airports leverage in negotiations.

IndiGo (InterGlobe Aviation) must accept higher fees to keep network density and its high-frequency schedule—core to market share and unit-cost advantage.

- Localized monopoly at major hubs

- 210 million domestic fliers in 2025

- Slot scarcity raises aeronautical fees

- IndiGo obliged to pay to protect frequency

Shortage of Specialized Technical Labor

The rapid expansion of Indian aviation has created intense demand for pilots, cabin crew, and A&P (airframe and powerplant) engineers; training lead times of 12–24 months and strict DGCA (Directorate General of Civil Aviation) certification give unions and institutes leverage.

By Dec 2025, Air India’s hiring surge raised market wages: average pilot pay for captains rose ~18% YoY and airline personnel costs climbed ~9% of operating expenses, boosting suppliers’ bargaining power.

- 12–24 month training lead time

- DGCA certification bottleneck

- Captain pay +18% YoY (2025)

- Personnel costs +~9% of OPEX (2025)

Suppliers Tighten the Noose on IndiGo: Fleet, Fuel, Slots & Crew Drive Costs Up

Suppliers hold strong leverage over IndiGo: aircraft (Airbus duopoly, ~99% A320 family, ~430 A320neo orders outstanding), engines (CFM/Pratt dominance), fuel (28% of FY2024 costs; jet fuel ~USD 90–100/bbl in 2024; fuel bill >INR 25,000 crore), airports/slots (210m domestic fliers in 2025) and crew/training (12–24m lead, captain pay +18% YoY 2025).

| Item | Key stat (2024–25) |

|---|---|

| Fleet concentration | ~99% A320 family; ~430 neo orders |

| Fuel | 28% Opex; ~USD90–100/bbl; >INR25,000cr |

| Passengers | 210m domestic (2025) |

| Pilot pay | Captain +18% YoY (2025) |

What is included in the product

Tailored exclusively for InterGlobe Aviation, this Porter's Five Forces overview uncovers competitive drivers, supplier and buyer influence, entry barriers, and substitutes to evaluate pricing power, profitability risks, and strategic positioning within the Indian aviation market.

Concise Porter's Five Forces for InterGlobe Aviation—one-sheet view to spot competitive intensity and relief points for pricing, capacity, and supplier pressure.

Customers Bargaining Power

High Price Sensitivity of Indian Travelers

The Indian market is highly price-sensitive: a 1–2% domestic fare rise can cut load factors several percentage points, and 2024 average domestic yield for IndiGo (InterGlobe Aviation) was near INR 3.2/km, forcing tight pricing.

Passengers treat flights as commodities, chasing lowest fares; IndiGo’s market share hit ~60% in 2024, but loyalty is weak so promo pricing drives volumes.

To compete, IndiGo kept unit cost per ASK around INR 2.9 in 2024, preserving low fares to retain mass-market demand through 2025.

Information Transparency via Digital Aggregators

Information transparency from OTAs and meta-search engines lets travelers compare fares and schedules across carriers in seconds, removing info asymmetry so IndiGo cannot conceal premium pricing on busy routes; in 2024 OTAs accounted for ~45% of Indian airline bookings, rising toward 50% by end-2025 per industry estimates.

Low Switching Costs for Domestic Passengers

Leverage of Large Corporate and Government Accounts

Corporate travel departments and government agencies account for roughly 25–30% of IndiGo’s high-frequency bookings and deliver steadier yield than leisure segments, reducing revenue volatility in 2025.

These bulk buyers extract discounted corporate fares, flexible cancellation windows, and seat guarantees, pressuring margins and ancillary upsell.

Given institutional travel spend estimated at $1.2–1.6 billion on IndiGo in 2024–25, these clients can dictate contract terms and service levels.

- 25–30% of high-frequency bookings

- $1.2–1.6B estimated institutional spend (2024–25)

- Discounts, flexible cancellations, preferred seating

- Material leverage over contract terms

Impact of Social Media on Brand Reputation

In the digital age, individual customers wield indirect power via social media where service failures go viral; IndiGo saw a 22% rise in negative online mentions after major delays in 2023, hitting brand sentiment scores by 8 points.

Perceived declines in punctuality or service are amplified instantly, affecting future bookings—IndiGo’s on-time performance fell to 80% in late 2023 vs 87% in 2022, correlating with a 3% dip in quarterly load factor.

By 2025 the collective consumer voice is a strong operational check, with consumer complaints on platforms rising 15% year-over-year and directly linked to faster policy changes.

- Social reach amplifies single incidents into reputational hits

- 2023: 22% more negative mentions; sentiment down 8 points

- On-time performance drop (87%→80%) tied to 3% load-factor dip

- 2024–25: 15% YoY rise in public complaints, prompting quicker fixes

IndiGo squeezed: strong customer leverage, tight yields, rising corporate and social pressure

Customers hold strong bargaining power: price sensitivity, easy switching, and OTA transparency force IndiGo into tight pricing (yield ~INR 3.2/km; unit cost ~INR 2.9/ASK in 2024) while corporates (25–30% bookings; $1.2–1.6B spend 2024–25) extract discounts and terms; social media amplifies service failures (22% more negative mentions in 2023) accelerating policy responses.

| Metric | Value (2024) |

|---|---|

| Yield | INR 3.2/km |

| Unit cost/ASK | INR 2.9 |

| Market share | ~60% |

| Corporate bookings | 25–30% |

| Institutional spend | $1.2–1.6B |

| OTA bookings | ~45% |

| Negative mentions rise | 22% |

Same Document Delivered

InterGlobe Aviation Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of InterGlobe Aviation you'll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

InterGlobe Aviation faces intense rivalry, regulatory headwinds, and capital-hungry suppliers, while buyer power and substitutes exert mixed pressure on margins—this snapshot highlights key competitive tensions shaping its strategy.

Suppliers Bargaining Power

Concentrated Aircraft Manufacturing Duopoly

The global commercial-aircraft market is a Boeing-Airbus duopoly, leaving IndiGo with few procurement alternatives; as of late 2025 IndiGo’s fleet is ~99% Airbus A320 family with ~430 A320neo-family orders outstanding, constraining its bargaining options.

Engine Manufacturer Technical Dependencies

IndiGo suffered major disruptions from 2016–2018 Pratt & Whitney PW1100G issues, costing estimated revenue losses of ~INR 3.5–4.0 billion in 2016–17 and grounding rates spiking 15–20%—showing clear supplier power.

Shift to CFM International LEAP engines for A320neo deliveries reduced exposure, but certified-provider scarcity creates lock-in for spares and shop visits.

By end-2025 only two OEMs (Pratt & Whitney, CFM) dominate certified narrowbody engines, keeping bargaining power high over maintenance pricing and MTBUR (mean time between unplanned removals) guarantees.

Volatility of Aviation Turbine Fuel Providers

Fuel is IndiGo's largest operating cost, accounting for about 28% of total expenses in FY2024 (InterGlobe Aviation), and supply is concentrated among a few state and private oil marketers in India, giving suppliers strong leverage.

Jet fuel prices track global crude benchmarks plus local duties, so IndiGo is a price taker with little control over base costs; jet fuel averaged ~USD 90–100/bbl in 2024, pushing jet-fuel bill above INR 25,000 crore.

With no scalable alternative energy for narrow-body jets by 2025, suppliers retain dominant bargaining power, raising IndiGo's exposure to oil-price swings and policy-driven tax shifts.

Airport Infrastructure and Slot Constraints

Major hubs Delhi, Mumbai and Bengaluru are run by a handful of private operators or the Airports Authority of India, creating localized monopolies for ground services that raise switching costs for carriers.

India saw a record 210 million domestic passengers in 2025, pushing peak-hour slot scarcity; prime slots command higher aeronautical fees, giving airports leverage in negotiations.

IndiGo (InterGlobe Aviation) must accept higher fees to keep network density and its high-frequency schedule—core to market share and unit-cost advantage.

- Localized monopoly at major hubs

- 210 million domestic fliers in 2025

- Slot scarcity raises aeronautical fees

- IndiGo obliged to pay to protect frequency

Shortage of Specialized Technical Labor

The rapid expansion of Indian aviation has created intense demand for pilots, cabin crew, and A&P (airframe and powerplant) engineers; training lead times of 12–24 months and strict DGCA (Directorate General of Civil Aviation) certification give unions and institutes leverage.

By Dec 2025, Air India’s hiring surge raised market wages: average pilot pay for captains rose ~18% YoY and airline personnel costs climbed ~9% of operating expenses, boosting suppliers’ bargaining power.

- 12–24 month training lead time

- DGCA certification bottleneck

- Captain pay +18% YoY (2025)

- Personnel costs +~9% of OPEX (2025)

Suppliers Tighten the Noose on IndiGo: Fleet, Fuel, Slots & Crew Drive Costs Up

Suppliers hold strong leverage over IndiGo: aircraft (Airbus duopoly, ~99% A320 family, ~430 A320neo orders outstanding), engines (CFM/Pratt dominance), fuel (28% of FY2024 costs; jet fuel ~USD 90–100/bbl in 2024; fuel bill >INR 25,000 crore), airports/slots (210m domestic fliers in 2025) and crew/training (12–24m lead, captain pay +18% YoY 2025).

| Item | Key stat (2024–25) |

|---|---|

| Fleet concentration | ~99% A320 family; ~430 neo orders |

| Fuel | 28% Opex; ~USD90–100/bbl; >INR25,000cr |

| Passengers | 210m domestic (2025) |

| Pilot pay | Captain +18% YoY (2025) |

What is included in the product

Tailored exclusively for InterGlobe Aviation, this Porter's Five Forces overview uncovers competitive drivers, supplier and buyer influence, entry barriers, and substitutes to evaluate pricing power, profitability risks, and strategic positioning within the Indian aviation market.

Concise Porter's Five Forces for InterGlobe Aviation—one-sheet view to spot competitive intensity and relief points for pricing, capacity, and supplier pressure.

Customers Bargaining Power

High Price Sensitivity of Indian Travelers

The Indian market is highly price-sensitive: a 1–2% domestic fare rise can cut load factors several percentage points, and 2024 average domestic yield for IndiGo (InterGlobe Aviation) was near INR 3.2/km, forcing tight pricing.

Passengers treat flights as commodities, chasing lowest fares; IndiGo’s market share hit ~60% in 2024, but loyalty is weak so promo pricing drives volumes.

To compete, IndiGo kept unit cost per ASK around INR 2.9 in 2024, preserving low fares to retain mass-market demand through 2025.

Information Transparency via Digital Aggregators

Information transparency from OTAs and meta-search engines lets travelers compare fares and schedules across carriers in seconds, removing info asymmetry so IndiGo cannot conceal premium pricing on busy routes; in 2024 OTAs accounted for ~45% of Indian airline bookings, rising toward 50% by end-2025 per industry estimates.

Low Switching Costs for Domestic Passengers

Leverage of Large Corporate and Government Accounts

Corporate travel departments and government agencies account for roughly 25–30% of IndiGo’s high-frequency bookings and deliver steadier yield than leisure segments, reducing revenue volatility in 2025.

These bulk buyers extract discounted corporate fares, flexible cancellation windows, and seat guarantees, pressuring margins and ancillary upsell.

Given institutional travel spend estimated at $1.2–1.6 billion on IndiGo in 2024–25, these clients can dictate contract terms and service levels.

- 25–30% of high-frequency bookings

- $1.2–1.6B estimated institutional spend (2024–25)

- Discounts, flexible cancellations, preferred seating

- Material leverage over contract terms

Impact of Social Media on Brand Reputation

In the digital age, individual customers wield indirect power via social media where service failures go viral; IndiGo saw a 22% rise in negative online mentions after major delays in 2023, hitting brand sentiment scores by 8 points.

Perceived declines in punctuality or service are amplified instantly, affecting future bookings—IndiGo’s on-time performance fell to 80% in late 2023 vs 87% in 2022, correlating with a 3% dip in quarterly load factor.

By 2025 the collective consumer voice is a strong operational check, with consumer complaints on platforms rising 15% year-over-year and directly linked to faster policy changes.

- Social reach amplifies single incidents into reputational hits

- 2023: 22% more negative mentions; sentiment down 8 points

- On-time performance drop (87%→80%) tied to 3% load-factor dip

- 2024–25: 15% YoY rise in public complaints, prompting quicker fixes

IndiGo squeezed: strong customer leverage, tight yields, rising corporate and social pressure

Customers hold strong bargaining power: price sensitivity, easy switching, and OTA transparency force IndiGo into tight pricing (yield ~INR 3.2/km; unit cost ~INR 2.9/ASK in 2024) while corporates (25–30% bookings; $1.2–1.6B spend 2024–25) extract discounts and terms; social media amplifies service failures (22% more negative mentions in 2023) accelerating policy responses.

| Metric | Value (2024) |

|---|---|

| Yield | INR 3.2/km |

| Unit cost/ASK | INR 2.9 |

| Market share | ~60% |

| Corporate bookings | 25–30% |

| Institutional spend | $1.2–1.6B |

| OTA bookings | ~45% |

| Negative mentions rise | 22% |

Same Document Delivered

InterGlobe Aviation Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of InterGlobe Aviation you'll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for use.