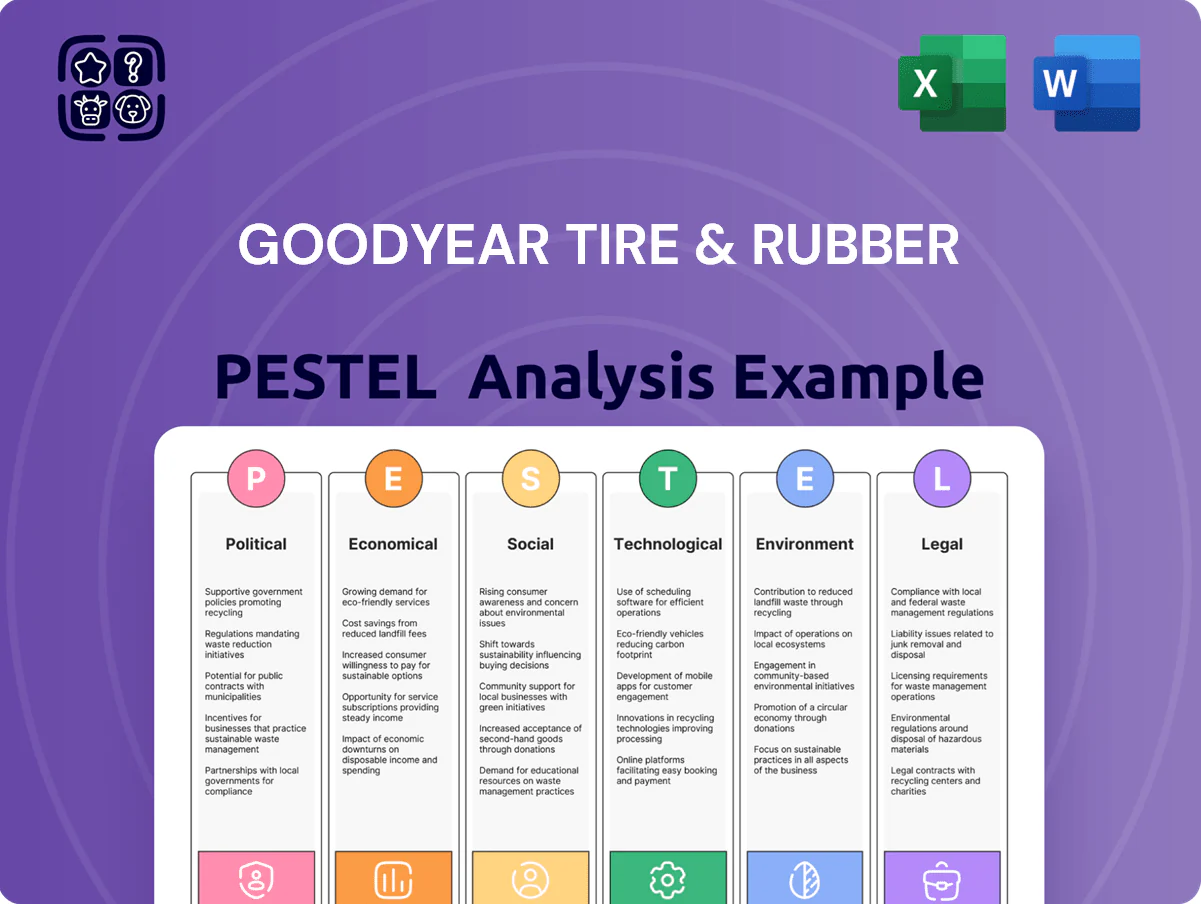

Goodyear Tire & Rubber PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Our PESTLE Analysis of Goodyear Tire & Rubber reveals how regulatory shifts, supply-chain inflation, evolving consumer mobility, and accelerating tire tech converge to reshape strategy and risk—insights investors and strategists can act on immediately; buy the full report to access detailed, editable findings and actionable recommendations.

Political factors

Trade Policy and Tariffs

Global trade tensions, notably US-China tariffs and a 15% average tariff on some imported tires into the US in recent years, raised Goodyear’s input costs—natural rubber and synthetic polymers—contributing to 2024 raw material inflation of ~12% year-over-year that pressured gross margins.

Shifting tariff regimes risk supply-chain disruption and price pass-through limits in North America, where Goodyear reported 2024 revenue of $14.5bn; abrupt duty changes could force margin compression or local price increases.

Goodyear’s response includes lobbying for tariff relief and expanding regional production—over 30 North American facilities—reducing import exposure and aiming to stabilize costs and pricing flexibility.

Government EV Mandates

Legislative pushes for EV adoption in Europe and North America — e.g., EU targets to cut new ICE sales by 2035 and US federal incentives under the Inflation Reduction Act — force mandatory shifts in tire design toward low rolling resistance; Goodyear estimates EV tire demand growing ~15–20% CAGR to 2030. The company secured >$100m in recent subsidies/grants for EV tire R&D, improving range by up to 5–7% in tests. Varying regional ICE phase-out timelines, however, require Goodyear to sustain capital flexibility and invest hundreds of millions in R&D and manufacturing upgrades to ensure compliance.

Geopolitical Stability in Sourcing Regions

Political unrest in Southeast Asia, which supplied about 70% of global natural rubber pre-2024, risks disrupting Goodyear’s raw-material access and contributed to a 28% YoY rubber price spike in 2022–23, pressuring gross margins.

Goodyear actively monitors conflicts and diplomatic ties across Malaysia, Thailand, and Indonesia to mitigate sudden export bans or port blockages that could delay shipments and increase logistics costs.

The board prioritizes diversifying rubber sourcing; by 2025 Goodyear aims to increase non-ASEAN supply share to 25% through new plantations and strategic contracts to stabilize procurement and cap volatility.

Labor Union Relations

Goodyear operates in regions with strong unions (US UAW, EU unions), where political shifts can raise collective bargaining power and wage mandates; in 2024 labor costs rose ~6% in North America for the sector, pressuring margins.

Changes in labor laws on safety and benefits (e.g., EU 2024 worker protection updates) increase manufacturing OPEX and capital compliance spend, measurable against Goodyear’s $3.3B 2024 cost of sales.

Collaborative union relations are vital to avoid strikes—previous tyre-industry strikes in 2022–24 caused multiweek shutdowns that trimmed industry output by estimated 4–7%, risking Goodyear’s market share.

- 2024 North America labor cost +6% (sector)

- Goodyear 2024 cost of sales $3.3B

- Industry strike-related output loss 4–7% (2022–24)

National Security and Aviation Contracts

As a major supplier to defense and aviation, Goodyear faces strict government vetting and ITAR-like national security regulations; defense contracts represented an estimated $200–300m of segment revenues in recent years (2024 filings show specialized products growth of ~5%).

Political decisions on US defense spending—FY2025 baseline defense budget ~$858bn—directly affect the long-term pipeline for military-grade and high-altitude aviation tires.

Administrative changes can re-prioritize procurement, shifting contract awards and R&D focus toward different aircraft programs and readiness levels.

- Defense-related revenue estimate: $200–300m

- 2025 US defense budget: ~$858bn

- Specialized products growth ~5% in 2024

Geopolitics, tariffs and supply shocks reshape Goodyear’s costs, sourcing and strategy

Political risks—tariffs (US avg ~15% on some imported tires), EV policy shifts (EU 2035 ICE phase-out; IRA incentives), SE Asia instability (70% pre-2024 rubber supply; 28% rubber price spike 2022–23), union pressure (NA labor costs +6% in 2024), and defense procurement volatility (defense-related revenue $200–300m)—drive Goodyear’s sourcing, pricing, labor and R&D strategies.

| Metric | Value |

|---|---|

| 2014–24 rubber supply source (pre-2024) | ~70% SE Asia |

| Rubber price spike | +28% (2022–23) |

| NA labor cost change (2024) | +6% |

| Goodyear 2024 revenue | $14.5bn |

| Cost of sales (2024) | $3.3bn |

| Defense-related revenue | $200–300m |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Goodyear Tire & Rubber, with data-driven trends and region-specific examples to identify risks and opportunities for executives, investors, and strategists.

A concise, PESTLE-sorted summary of Goodyear Tire & Rubber that highlights external risks and opportunities for quick inclusion in presentations or planning sessions.

Economic factors

Raw Material Price Volatility

The profitability of Goodyear is highly sensitive to swings in natural rubber, synthetic rubber and oil-based chemical costs; rubber prices rose about 18% in 2024, squeezing industry margins when not passed to buyers. Economic instability in commodity markets can cause rapid margin compression—Goodyear reported raw material cost headwinds of roughly $400 million in 2023–2024. Robust hedging and scaling bio-based rubber alternatives (R&D spend approx. $200–250 million annually) are critical to stabilize the bottom line.

Global Interest Rate Trends

Global interest rates remaining elevated—US Fed funds at 5.25–5.50% in 2024 and ECB rates around 3.25%—have curtailed auto sales and fleet financing, pushing consumers to delay new vehicle purchases and favor replacement tires. For Goodyear, this boosts replacement-market demand but reduces original-equipment volumes; FY2024 replacement sales rose mid-single digits industry-wide. The company must manage leverage—Goodyear’s net debt was about $4.3bn at end-2024—to preserve liquidity amid higher borrowing costs.

Automotive Industry Cycles

Goodyear performance tracks the cyclical global auto industry and vehicle miles traveled; global light-vehicle sales fell 5% in 2023 to ~70.6M units, pressuring replacement tire volumes and revenue.

Economic downturns cut freight activity—U.S. intermodal volumes dropped ~4% Y/Y in 2023—reducing demand for commercial truck tires and fleet maintenance services.

During expansions, higher-margin aviation and luxury segments boost margins: Goodyear’s aerospace sales rose ~8% in 2024 while premium OE fits supported ASP improvements reported in its 2024 10-K.

Inflationary Pressure on Logistics

Persistent inflation in energy and transport—fuel prices rose ~18% YoY in 2024—raises distribution costs for Goodyear’s heavy tire shipments across North America and global lanes, squeezing margins.

Goodyear leverages advanced logistics software and regional warehousing, cutting route miles and improving fill rates; efficiency gains helped lower per-unit freight by an estimated 6% in 2024.

Controlling these overheads is vital to keep retail and OE pricing competitive versus low-cost entrants from emerging markets increasing North American share.

- Fuel/energy inflation ~18% YoY (2024)

- Per-unit freight reduced ~6% via logistics/warehousing (2024)

- Pressure from low-cost emerging-market manufacturers in North America

Currency Exchange Fluctuations

As a multinational, Goodyear faces translation risk converting 2025 international earnings into USD; a 5% Euro decline versus the dollar could reduce reported quarterly revenue by roughly 2–3%, given Euro-denominated sales exposure.

Volatility in the Euro, Chinese yuan and Brazilian real drove a 2024 FX headwind of about $60–90 million to adjusted operating income; swings in these currencies cause material quarterly net income variance.

Goodyear’s treasury uses forwards, options and cross-currency swaps; as of FY2024 the company reported hedges covering a significant portion of near-term cash flows, mitigating but not eliminating FX translation impacts.

- 2024 FX headwind: ~$60–90M to adjusted operating income

- 5% Euro move ≈ 2–3% revenue swing

- Hedging tools: forwards, options, cross-currency swaps

Goodyear hit by $400M material headwind, rising rates, FX and freight pressures

Goodyear faces raw-material cost volatility (rubber +18% in 2024; ~$400M headwind 2023–24), higher borrowing costs (net debt ~$4.3B end-2024; Fed 5.25–5.50% in 2024), FX swings (2024 FX headwind ~$60–90M; 5% EUR move ≈2–3% revenue), and freight inflation (fuel +18% 2024; per-unit freight down ~6% via logistics).

| Metric | 2024/2024–25 |

|---|---|

| Rubber price change | +18% |

| Raw-material headwind | $~400M |

| Net debt | $4.3B |

| FX headwind | $60–90M |

| Freight change | -6% per-unit |

What You See Is What You Get

Goodyear Tire & Rubber PESTLE Analysis

The preview shown here is the exact Goodyear Tire & Rubber PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategy or investment analysis.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Our PESTLE Analysis of Goodyear Tire & Rubber reveals how regulatory shifts, supply-chain inflation, evolving consumer mobility, and accelerating tire tech converge to reshape strategy and risk—insights investors and strategists can act on immediately; buy the full report to access detailed, editable findings and actionable recommendations.

Political factors

Trade Policy and Tariffs

Global trade tensions, notably US-China tariffs and a 15% average tariff on some imported tires into the US in recent years, raised Goodyear’s input costs—natural rubber and synthetic polymers—contributing to 2024 raw material inflation of ~12% year-over-year that pressured gross margins.

Shifting tariff regimes risk supply-chain disruption and price pass-through limits in North America, where Goodyear reported 2024 revenue of $14.5bn; abrupt duty changes could force margin compression or local price increases.

Goodyear’s response includes lobbying for tariff relief and expanding regional production—over 30 North American facilities—reducing import exposure and aiming to stabilize costs and pricing flexibility.

Government EV Mandates

Legislative pushes for EV adoption in Europe and North America — e.g., EU targets to cut new ICE sales by 2035 and US federal incentives under the Inflation Reduction Act — force mandatory shifts in tire design toward low rolling resistance; Goodyear estimates EV tire demand growing ~15–20% CAGR to 2030. The company secured >$100m in recent subsidies/grants for EV tire R&D, improving range by up to 5–7% in tests. Varying regional ICE phase-out timelines, however, require Goodyear to sustain capital flexibility and invest hundreds of millions in R&D and manufacturing upgrades to ensure compliance.

Geopolitical Stability in Sourcing Regions

Political unrest in Southeast Asia, which supplied about 70% of global natural rubber pre-2024, risks disrupting Goodyear’s raw-material access and contributed to a 28% YoY rubber price spike in 2022–23, pressuring gross margins.

Goodyear actively monitors conflicts and diplomatic ties across Malaysia, Thailand, and Indonesia to mitigate sudden export bans or port blockages that could delay shipments and increase logistics costs.

The board prioritizes diversifying rubber sourcing; by 2025 Goodyear aims to increase non-ASEAN supply share to 25% through new plantations and strategic contracts to stabilize procurement and cap volatility.

Labor Union Relations

Goodyear operates in regions with strong unions (US UAW, EU unions), where political shifts can raise collective bargaining power and wage mandates; in 2024 labor costs rose ~6% in North America for the sector, pressuring margins.

Changes in labor laws on safety and benefits (e.g., EU 2024 worker protection updates) increase manufacturing OPEX and capital compliance spend, measurable against Goodyear’s $3.3B 2024 cost of sales.

Collaborative union relations are vital to avoid strikes—previous tyre-industry strikes in 2022–24 caused multiweek shutdowns that trimmed industry output by estimated 4–7%, risking Goodyear’s market share.

- 2024 North America labor cost +6% (sector)

- Goodyear 2024 cost of sales $3.3B

- Industry strike-related output loss 4–7% (2022–24)

National Security and Aviation Contracts

As a major supplier to defense and aviation, Goodyear faces strict government vetting and ITAR-like national security regulations; defense contracts represented an estimated $200–300m of segment revenues in recent years (2024 filings show specialized products growth of ~5%).

Political decisions on US defense spending—FY2025 baseline defense budget ~$858bn—directly affect the long-term pipeline for military-grade and high-altitude aviation tires.

Administrative changes can re-prioritize procurement, shifting contract awards and R&D focus toward different aircraft programs and readiness levels.

- Defense-related revenue estimate: $200–300m

- 2025 US defense budget: ~$858bn

- Specialized products growth ~5% in 2024

Geopolitics, tariffs and supply shocks reshape Goodyear’s costs, sourcing and strategy

Political risks—tariffs (US avg ~15% on some imported tires), EV policy shifts (EU 2035 ICE phase-out; IRA incentives), SE Asia instability (70% pre-2024 rubber supply; 28% rubber price spike 2022–23), union pressure (NA labor costs +6% in 2024), and defense procurement volatility (defense-related revenue $200–300m)—drive Goodyear’s sourcing, pricing, labor and R&D strategies.

| Metric | Value |

|---|---|

| 2014–24 rubber supply source (pre-2024) | ~70% SE Asia |

| Rubber price spike | +28% (2022–23) |

| NA labor cost change (2024) | +6% |

| Goodyear 2024 revenue | $14.5bn |

| Cost of sales (2024) | $3.3bn |

| Defense-related revenue | $200–300m |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Goodyear Tire & Rubber, with data-driven trends and region-specific examples to identify risks and opportunities for executives, investors, and strategists.

A concise, PESTLE-sorted summary of Goodyear Tire & Rubber that highlights external risks and opportunities for quick inclusion in presentations or planning sessions.

Economic factors

Raw Material Price Volatility

The profitability of Goodyear is highly sensitive to swings in natural rubber, synthetic rubber and oil-based chemical costs; rubber prices rose about 18% in 2024, squeezing industry margins when not passed to buyers. Economic instability in commodity markets can cause rapid margin compression—Goodyear reported raw material cost headwinds of roughly $400 million in 2023–2024. Robust hedging and scaling bio-based rubber alternatives (R&D spend approx. $200–250 million annually) are critical to stabilize the bottom line.

Global Interest Rate Trends

Global interest rates remaining elevated—US Fed funds at 5.25–5.50% in 2024 and ECB rates around 3.25%—have curtailed auto sales and fleet financing, pushing consumers to delay new vehicle purchases and favor replacement tires. For Goodyear, this boosts replacement-market demand but reduces original-equipment volumes; FY2024 replacement sales rose mid-single digits industry-wide. The company must manage leverage—Goodyear’s net debt was about $4.3bn at end-2024—to preserve liquidity amid higher borrowing costs.

Automotive Industry Cycles

Goodyear performance tracks the cyclical global auto industry and vehicle miles traveled; global light-vehicle sales fell 5% in 2023 to ~70.6M units, pressuring replacement tire volumes and revenue.

Economic downturns cut freight activity—U.S. intermodal volumes dropped ~4% Y/Y in 2023—reducing demand for commercial truck tires and fleet maintenance services.

During expansions, higher-margin aviation and luxury segments boost margins: Goodyear’s aerospace sales rose ~8% in 2024 while premium OE fits supported ASP improvements reported in its 2024 10-K.

Inflationary Pressure on Logistics

Persistent inflation in energy and transport—fuel prices rose ~18% YoY in 2024—raises distribution costs for Goodyear’s heavy tire shipments across North America and global lanes, squeezing margins.

Goodyear leverages advanced logistics software and regional warehousing, cutting route miles and improving fill rates; efficiency gains helped lower per-unit freight by an estimated 6% in 2024.

Controlling these overheads is vital to keep retail and OE pricing competitive versus low-cost entrants from emerging markets increasing North American share.

- Fuel/energy inflation ~18% YoY (2024)

- Per-unit freight reduced ~6% via logistics/warehousing (2024)

- Pressure from low-cost emerging-market manufacturers in North America

Currency Exchange Fluctuations

As a multinational, Goodyear faces translation risk converting 2025 international earnings into USD; a 5% Euro decline versus the dollar could reduce reported quarterly revenue by roughly 2–3%, given Euro-denominated sales exposure.

Volatility in the Euro, Chinese yuan and Brazilian real drove a 2024 FX headwind of about $60–90 million to adjusted operating income; swings in these currencies cause material quarterly net income variance.

Goodyear’s treasury uses forwards, options and cross-currency swaps; as of FY2024 the company reported hedges covering a significant portion of near-term cash flows, mitigating but not eliminating FX translation impacts.

- 2024 FX headwind: ~$60–90M to adjusted operating income

- 5% Euro move ≈ 2–3% revenue swing

- Hedging tools: forwards, options, cross-currency swaps

Goodyear hit by $400M material headwind, rising rates, FX and freight pressures

Goodyear faces raw-material cost volatility (rubber +18% in 2024; ~$400M headwind 2023–24), higher borrowing costs (net debt ~$4.3B end-2024; Fed 5.25–5.50% in 2024), FX swings (2024 FX headwind ~$60–90M; 5% EUR move ≈2–3% revenue), and freight inflation (fuel +18% 2024; per-unit freight down ~6% via logistics).

| Metric | 2024/2024–25 |

|---|---|

| Rubber price change | +18% |

| Raw-material headwind | $~400M |

| Net debt | $4.3B |

| FX headwind | $60–90M |

| Freight change | -6% per-unit |

What You See Is What You Get

Goodyear Tire & Rubber PESTLE Analysis

The preview shown here is the exact Goodyear Tire & Rubber PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategy or investment analysis.