Green Plains Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

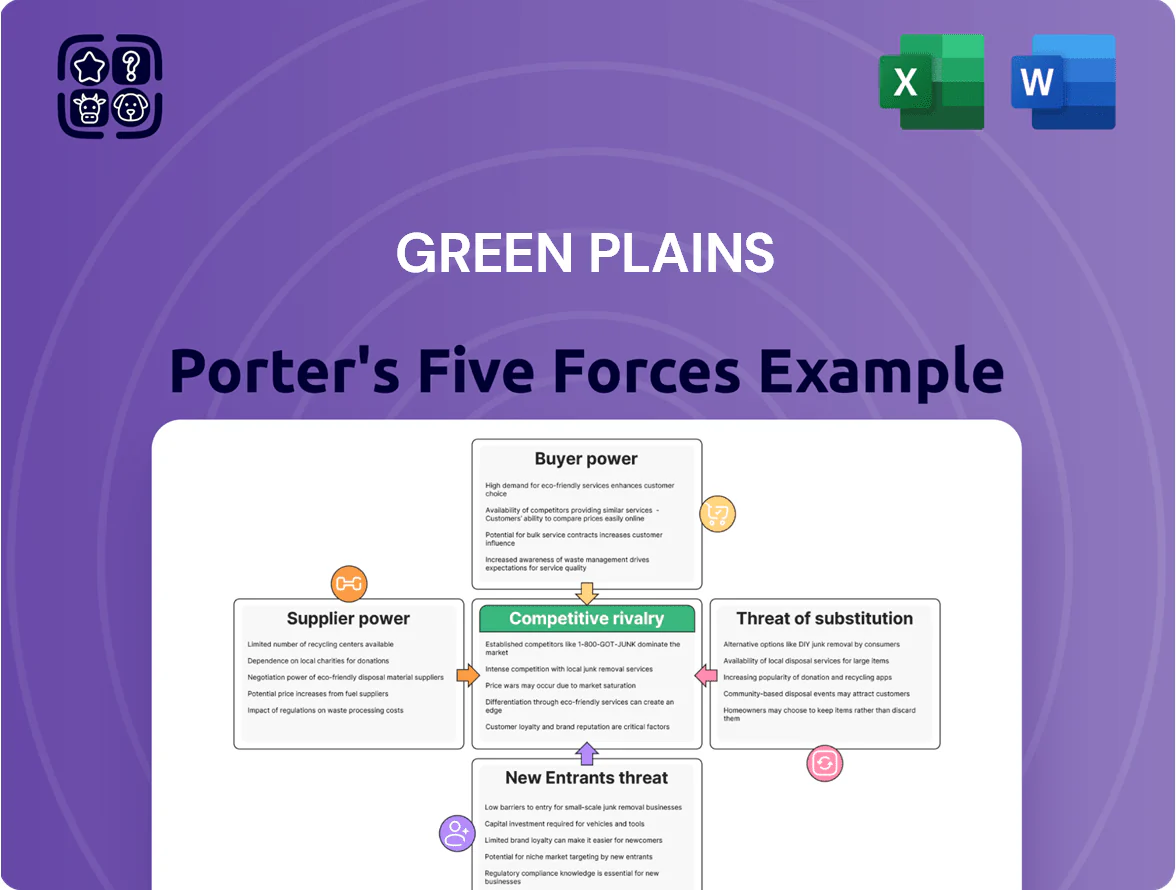

Green Plains operates in a capital‑intensive, commodity‑driven sector where buyer bargaining and substitute threats are moderate, supplier power fluctuates with feedstock availability, entry barriers are high due to scale and regulation, and rivalry is intense among margin‑sensitive players—this snapshot hints at strategic pressure points and resilience factors.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Green Plains’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility of Corn Feedstock Prices

Corn is Green Plains’ main feedstock, bought from fragmented US farmers and grain elevators; global corn futures (Dec 2025) traded near $5.80/bushel, set by weather, demand, and geopolitics, not by Green Plains.

Because corn is a globally traded commodity, price spikes after poor US harvests or Black Sea export disruptions force Green Plains to pay market rates, raising supplier bargaining power and input cost volatility.

Energy and Natural Gas Requirements

Biorefining is energy-intensive and Green Plains relies heavily on natural gas for heat and power; U.S. industrial natural gas prices averaged about 3.80 USD/MMBtu in 2024, so fuel swings hit margins directly.

Green Plains is a price taker in energy markets and reported energy expense volatility that pressured 2024 gross margins; hedging reduces but doesn’t eliminate exposure.

With few regional utility providers, suppliers hold leverage over fixed operating costs, making utility contract terms and 3–5 year price trends critical to profitability.

Logistics and Transportation Providers

Rail, truck, and barge moves nearly all corn to Green Plains and ethanol out; Class I railroads (BNSF, UP, CN, CSX) wield strong leverage because long‑haul substitutes are scarce.

In 2025, U.S. rail labor talks and chokepoints raised freight rates ~8–12% YoY and caused shipment delays averaging 3–5 days, keeping supplier pressure high on margins.

Specialized Technology and Enzyme Providers

The shift to high-value ingredients forces Green Plains to rely on a handful of biotech firms supplying specialized enzymes and yeast strains, many protected by patents; these suppliers can command price premia—industry reports show enzyme costs can be 5–15% of bioprocessing OPEX.

Switching suppliers risks batch failures and weeks of recalibration, and may cut protein yields by 10–25% during transition, hurting margins and time-to-market.

Fragmentation of Agricultural Producers

Individual farmers have little negotiating power, but the collective Midwest corn belt controls feedstock volume; U.S. corn harvested area fell 1.2% in 2024 to 83.2 million acres, tightening availability for Green Plains.

Green Plains lowers risk by placing plants in high-yield counties—average 2024 county yields were 183.4 bu/acre versus national 172.0 bu/acre—but remains exposed if planting shifts to soybeans.

By end-2025, acreage competition between biofuel feedstock and food crops is a key constraint; USDA projected 2025 corn planted area at ~82–84 million acres, keeping supply-side pressure.

- Farmers weak individually; region decisive

- Green Plains sites in high-yield counties (183.4 bu/acre avg)

- 2024 U.S. corn harvested 83.2M acres (-1.2%)

- USDA 2025 corn plantings ~82–84M acres → continued supply risk

Supplier leverage high: commodity feed, energy volatility, and IP‑tied enzyme risk

Suppliers hold moderate‑high leverage: corn is a global commodity (Dec 2025 futures ~5.80 USD/bu) so feedstock price shocks raise costs; natural gas averaged ~3.80 USD/MMBtu in 2024, adding energy volatility; rail and utilities are regional bottlenecks; biotech enzyme/strain suppliers (5–15% OPEX) are concentrated and IP‑locked, making switching costly (10–25% yield risk).

| Metric | Value |

|---|---|

| Corn futures (Dec 2025) | ~5.80 USD/bu |

| NatGas (2024 avg) | ~3.80 USD/MMBtu |

| U.S. harvested acres 2024 | 83.2M (-1.2%) |

| Enzyme OPEX share | 5–15% |

| Switch yield risk | 10–25% |

What is included in the product

Concise Porter's Five Forces analysis of Green Plains evaluating competitive rivalry, supplier and buyer power, entry barriers, and substitute threats to reveal strategic risks, pricing influence, and opportunities to defend or expand market position.

A concise Porter's Five Forces one-sheet for Green Plains—instantly spot where margin pressure or opportunity lies and paste directly into decks for faster, confident decision-making.

Customers Bargaining Power

Concentration of Oil Majors and Blenders

The primary customers for ethanol—large integrated oil companies and fuel blenders—are highly concentrated, with the top 10 U.S. refiners and blenders accounting for roughly 60% of gasoline demand in 2024, giving them strong volume leverage to push prices down. Ethanol trades as a commodity (RINs fungibility adds to price focus), so buyers routinely shift suppliers to capture spot discounts; Green Plains reported 2024 average sales volumes of ~1.2 billion gallons, exposing it to buyer-driven margin pressure.

Livestock Producer Sensitivity to Feed Costs

Regulatory Influence on Demand Volume

Regulatory demand drives ethanol sales: the US Renewable Fuel Standard (RFS) set 2023-24 total renewable fuel volumes near 20.63 billion gallons, creating a demand floor for Green Plains’ ethanol. Still, buyers purchase to meet compliance only, capping upside and increasing price sensitivity. If 2025 blending targets fall—as tracked in policy proposals—buyers gain leverage to push for lower prices, pressuring margins and volumes.

Demand for High-Protein Ingredients

Price Transparency in Commodity Markets

Price transparency for ethanol and corn oil on public exchanges means buyers see spot margins, so Green Plains (ticker: GPRE) can rarely command premiums without clear product differentiation.

In 2025, visible spot ethanol spreads averaged about 0.12–0.18 USD/gal vs. wholesale costs, and buyers used that data to push margins down when industry inventory rose to ~24–26 million barrels.

- Public spot spreads: 0.12–0.18 USD/gal (2025)

- Industry inventory: ~24–26 million barrels (2025)

- Result: limited pricing power without differentiation

Customers Hold the Cards: Top Buyers Dominate Demand, Price-Sensitive DGs & Niche Buyers

The bargaining power of Green Plains’ customers is high: top 10 refiners/blenders = ~60% gasoline demand (2024), distillers grains price-sensitive (DGs $180/ton vs corn $220/ton, 2024), RFS volumes ~20.63 bg (2023-24) cap upside, specialized pet/aqua buyers = ~40% of ingredient purchases (2024) but switching cost premium ~10–15%.

| Metric | Value |

|---|---|

| Top-10 buyer share | ~60% (2024) |

| DGs vs corn | $180/ton vs $220/ton (2024) |

| RFS volume | 20.63 billion gal (2023-24) |

| Pet/aqua buyer share | ~40% (2024) |

| Spot ethanol spread | $0.12–0.18/gal (2025) |

What You See Is What You Get

Green Plains Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Green Plains you’ll receive—no placeholders or samples—fully formatted and ready for immediate download after purchase.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Green Plains operates in a capital‑intensive, commodity‑driven sector where buyer bargaining and substitute threats are moderate, supplier power fluctuates with feedstock availability, entry barriers are high due to scale and regulation, and rivalry is intense among margin‑sensitive players—this snapshot hints at strategic pressure points and resilience factors.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Green Plains’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility of Corn Feedstock Prices

Corn is Green Plains’ main feedstock, bought from fragmented US farmers and grain elevators; global corn futures (Dec 2025) traded near $5.80/bushel, set by weather, demand, and geopolitics, not by Green Plains.

Because corn is a globally traded commodity, price spikes after poor US harvests or Black Sea export disruptions force Green Plains to pay market rates, raising supplier bargaining power and input cost volatility.

Energy and Natural Gas Requirements

Biorefining is energy-intensive and Green Plains relies heavily on natural gas for heat and power; U.S. industrial natural gas prices averaged about 3.80 USD/MMBtu in 2024, so fuel swings hit margins directly.

Green Plains is a price taker in energy markets and reported energy expense volatility that pressured 2024 gross margins; hedging reduces but doesn’t eliminate exposure.

With few regional utility providers, suppliers hold leverage over fixed operating costs, making utility contract terms and 3–5 year price trends critical to profitability.

Logistics and Transportation Providers

Rail, truck, and barge moves nearly all corn to Green Plains and ethanol out; Class I railroads (BNSF, UP, CN, CSX) wield strong leverage because long‑haul substitutes are scarce.

In 2025, U.S. rail labor talks and chokepoints raised freight rates ~8–12% YoY and caused shipment delays averaging 3–5 days, keeping supplier pressure high on margins.

Specialized Technology and Enzyme Providers

The shift to high-value ingredients forces Green Plains to rely on a handful of biotech firms supplying specialized enzymes and yeast strains, many protected by patents; these suppliers can command price premia—industry reports show enzyme costs can be 5–15% of bioprocessing OPEX.

Switching suppliers risks batch failures and weeks of recalibration, and may cut protein yields by 10–25% during transition, hurting margins and time-to-market.

Fragmentation of Agricultural Producers

Individual farmers have little negotiating power, but the collective Midwest corn belt controls feedstock volume; U.S. corn harvested area fell 1.2% in 2024 to 83.2 million acres, tightening availability for Green Plains.

Green Plains lowers risk by placing plants in high-yield counties—average 2024 county yields were 183.4 bu/acre versus national 172.0 bu/acre—but remains exposed if planting shifts to soybeans.

By end-2025, acreage competition between biofuel feedstock and food crops is a key constraint; USDA projected 2025 corn planted area at ~82–84 million acres, keeping supply-side pressure.

- Farmers weak individually; region decisive

- Green Plains sites in high-yield counties (183.4 bu/acre avg)

- 2024 U.S. corn harvested 83.2M acres (-1.2%)

- USDA 2025 corn plantings ~82–84M acres → continued supply risk

Supplier leverage high: commodity feed, energy volatility, and IP‑tied enzyme risk

Suppliers hold moderate‑high leverage: corn is a global commodity (Dec 2025 futures ~5.80 USD/bu) so feedstock price shocks raise costs; natural gas averaged ~3.80 USD/MMBtu in 2024, adding energy volatility; rail and utilities are regional bottlenecks; biotech enzyme/strain suppliers (5–15% OPEX) are concentrated and IP‑locked, making switching costly (10–25% yield risk).

| Metric | Value |

|---|---|

| Corn futures (Dec 2025) | ~5.80 USD/bu |

| NatGas (2024 avg) | ~3.80 USD/MMBtu |

| U.S. harvested acres 2024 | 83.2M (-1.2%) |

| Enzyme OPEX share | 5–15% |

| Switch yield risk | 10–25% |

What is included in the product

Concise Porter's Five Forces analysis of Green Plains evaluating competitive rivalry, supplier and buyer power, entry barriers, and substitute threats to reveal strategic risks, pricing influence, and opportunities to defend or expand market position.

A concise Porter's Five Forces one-sheet for Green Plains—instantly spot where margin pressure or opportunity lies and paste directly into decks for faster, confident decision-making.

Customers Bargaining Power

Concentration of Oil Majors and Blenders

The primary customers for ethanol—large integrated oil companies and fuel blenders—are highly concentrated, with the top 10 U.S. refiners and blenders accounting for roughly 60% of gasoline demand in 2024, giving them strong volume leverage to push prices down. Ethanol trades as a commodity (RINs fungibility adds to price focus), so buyers routinely shift suppliers to capture spot discounts; Green Plains reported 2024 average sales volumes of ~1.2 billion gallons, exposing it to buyer-driven margin pressure.

Livestock Producer Sensitivity to Feed Costs

Regulatory Influence on Demand Volume

Regulatory demand drives ethanol sales: the US Renewable Fuel Standard (RFS) set 2023-24 total renewable fuel volumes near 20.63 billion gallons, creating a demand floor for Green Plains’ ethanol. Still, buyers purchase to meet compliance only, capping upside and increasing price sensitivity. If 2025 blending targets fall—as tracked in policy proposals—buyers gain leverage to push for lower prices, pressuring margins and volumes.

Demand for High-Protein Ingredients

Price Transparency in Commodity Markets

Price transparency for ethanol and corn oil on public exchanges means buyers see spot margins, so Green Plains (ticker: GPRE) can rarely command premiums without clear product differentiation.

In 2025, visible spot ethanol spreads averaged about 0.12–0.18 USD/gal vs. wholesale costs, and buyers used that data to push margins down when industry inventory rose to ~24–26 million barrels.

- Public spot spreads: 0.12–0.18 USD/gal (2025)

- Industry inventory: ~24–26 million barrels (2025)

- Result: limited pricing power without differentiation

Customers Hold the Cards: Top Buyers Dominate Demand, Price-Sensitive DGs & Niche Buyers

The bargaining power of Green Plains’ customers is high: top 10 refiners/blenders = ~60% gasoline demand (2024), distillers grains price-sensitive (DGs $180/ton vs corn $220/ton, 2024), RFS volumes ~20.63 bg (2023-24) cap upside, specialized pet/aqua buyers = ~40% of ingredient purchases (2024) but switching cost premium ~10–15%.

| Metric | Value |

|---|---|

| Top-10 buyer share | ~60% (2024) |

| DGs vs corn | $180/ton vs $220/ton (2024) |

| RFS volume | 20.63 billion gal (2023-24) |

| Pet/aqua buyer share | ~40% (2024) |

| Spot ethanol spread | $0.12–0.18/gal (2025) |

What You See Is What You Get

Green Plains Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Green Plains you’ll receive—no placeholders or samples—fully formatted and ready for immediate download after purchase.