GrainCorp Boston Consulting Group Matrix

Actionable Strategy Starts Here

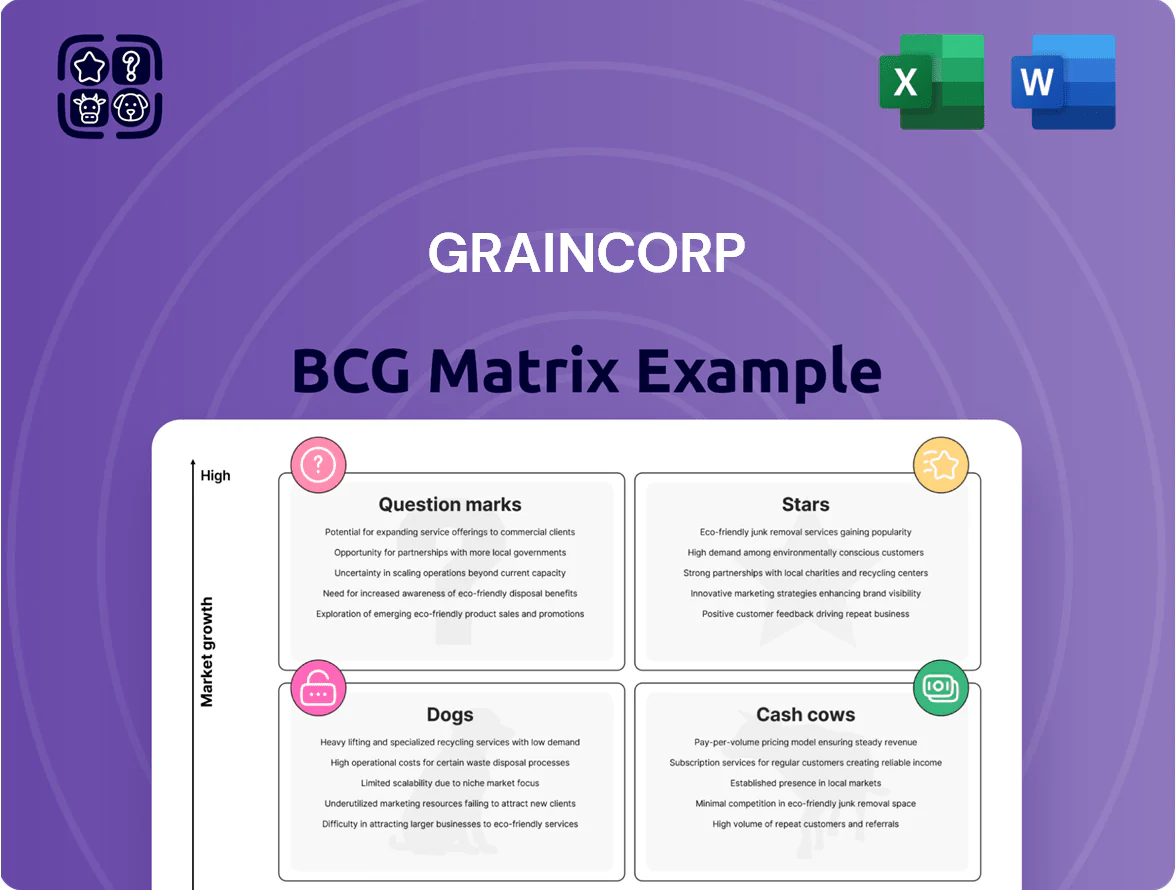

GrainCorp’s BCG Matrix snapshot shows a mix of stable cash-generating grain handling assets and high-potential value-added offerings facing competitive pressure—insightful for portfolio prioritization and capital allocation.

Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Oilseed Crushing and Renewable Fuel Feedstocks

GrainCorp hit record oilseed crush volumes of 557,000 tonnes in FY25, cementing its Australian market-leader position and driving higher processing margins.

The unit is rapidly moving into renewable fuels, supplying feedstocks for Sustainable Aviation Fuel (SAF) and biodiesel and capturing growth from global decarbonization mandates.

Demand is expanding: SAF and biodiesel volumes are forecast to grow double digits annually to 2030, and GrainCorp benefits from policy support like the A$250 million federal grant for domestic refining projects.

Animal Nutrition and Feed Solutions

Animal Nutrition and Feed Solutions: volumes jumped to 713,000 tonnes in FY25 from 517,000 tonnes in FY24, a 38% rise driven by record Australian cattle-on-feed and stronger New Zealand dairy demand; segment revenue growth outpaced GrainCorp average, with FY25 EBITDA margin expanding ~220 basis points after integrating XFA; the XFA deal boosted high-value nutritional consulting and speciality feed sales, adding cross-sell opportunities and higher ASPs.

AgTech and Digital Supply Chain Services

GrainCorp’s $30 million corporate venture fund, launched 2023, backs AgTech and digital supply-chain startups to modernize the value chain, targeting supply-chain transparency, carbon tracking, and on-farm productivity tools.

These initiatives align with a 2024 industry shift: 42% CAGR in farm-management software adoption in APAC (2021–24), and carbon-tracking demand up 60% in 2023, positioning GrainCorp’s platforms as first-to-market.

Early results: pilot deployments across 1200 farms in 2024 drove a 15% uptake in premium market access and contributed to a 3–5% revenue uplift in participating grain origination hubs.

Low-Carbon Canola Supply Chain

GrainCorp Next entered year two in 2025, delivering an end-to-end low-carbon canola chain that achieved ISCC certification for 120,000 tonnes, capturing roughly 35% of GrainCorp’s specialty export volume to the EU and earning a 5–8% price premium versus standard canola.

This positions GrainCorp as a green-transition leader: low-carbon supply reduces Scope 3 risk, supports EU renewable mandates, and drove an estimated A$18–24m incremental EBITDA in 2025 from premium sales and new long-term offtake contracts.

- ISCC-certified 120,000 t in 2025

- ~35% share of specialty export market

- 5–8% price premium; A$18–24m EBITDA uplift

- Strengthens export access to EU renewable/feedstock rules

Specialty Chickpea and Pulse Programs

In FY25 GrainCorp’s Agribusiness saw a 28% EBITDA uplift from high-margin chickpea and pulse programs, driven by a 15% YoY rise in global pulse demand as plant-based protein; exports from its East Coast network grew 32% and captured an estimated 45% share of Australia’s chickpea export flow.

The broader grain market is mature, but specialty pulses rank as a BCG Star for the international trade desk—high growth and high market share, with pulse revenue up to AUD 210m in FY25 and margins ~18%.

- FY25 pulse revenue AUD 210m

- EBITDA uplift +28%

- Export volume +32% YoY

- Estimated 45% export market share

- Average margin ~18%

GrainCorp drives margin surge: ISCC canola, animal feed & pulses power FY25 growth

GrainCorp’s Stars: oilseed crush 557,000t FY25, animal feed 713,000t (+38% YoY), ISCC low‑carbon canola 120,000t (35% specialty export share, A$18–24m EBITDA uplift), pulses revenue A$210m (+28% EBITDA, 32% export vol). High growth segments + market leadership drive margin expansion and premium access to EU renewables.

| Metric | FY25 |

|---|---|

| Oilseed crush | 557,000 t |

| Animal feed volumes | 713,000 t |

| ISCC canola | 120,000 t |

| Pulse revenue | A$210m |

| Pulse margin | ~18% |

| Pulse export share | ~45% |

| ISCC EBITDA uplift | A$18–24m |

What is included in the product

BCG Matrix mapping of GrainCorp’s units with quadrant-specific strategies, investment recommendations, and trend-driven risks and opportunities.

One-page GrainCorp BCG Matrix placing each business unit in a quadrant for quick strategic clarity.

Cash Cows

East Coast Australia (ECA) Storage and Handling

GrainCorp’s East Coast Australia (ECA) Storage and Handling is a Cash Cow, holding ~40% share of eastern Australia grain production and handling 31.6 million tonnes in FY25, producing steady EBITDA margins near 18% and strong operating cash flow. The mature silo and rail network needs relatively low incremental capex (≈A$85–95m annual maintenance in FY25), funding dividends and investments into higher-growth renewables like biofuels.

Port Terminal Services and Bulk Materials

GrainCorp’s seven East Coast bulk port terminals are high-barrier-to-entry infrastructure that secure a durable competitive moat.

In FY25 the bulk materials program handled 3.0 million tonnes of non-grain cargo and delivered a record contribution margin of $41 million.

These ports generate steady cash through long-term contracts and diversified commodity flows—woodchips, cement, fertilizer—reducing revenue volatility.

Human Nutrition and Edible Oil Refining

As the largest refiner of edible fats and oils in Australia and New Zealand, GrainCorp’s Human Nutrition and Edible Oil Refining holds a commanding market share in a stable, mature food industry, supplying about 40–45% of regional refined oil volumes in 2024. Despite cyclical margin pressure—refining EBIT margins averaged ~6% in FY2024—the segment delivers steady revenue (≈A$420m in FY2024) by selling essential inputs to major food manufacturers and bakeries. It runs at high operational efficiency with utilization rates near 92% and requires maintenance-level capex (~A$15–20m annually), supporting GrainCorp’s corporate liquidity.

Domestic Grain Marketing and Distribution

GrainCorp’s domestic marketing arm links Australian growers to local flour millers, feed lots, and industrial users, holding a dominant share of internal grain trade in a mature market with stable logistics and low promo spend.

Domestic outloads reached 6.5 million tonnes in FY25, generating steady cash flows that underpin GrainCorp’s 48-cent-per-share dividend and fund capex for storage and rail upgrades.

- FY25 domestic outloads: 6.5 Mt

- Market: mature, low promo spend

- Customers: flour mills, feedlots, industrial users

- Supports dividend: 48c/share

- Uses: cash for capex, working capital

Tallow and Used Cooking Oil Collection

The collection and aggregation of tallow and used cooking oil is a mature, high-market-share cash cow in GrainCorp’s Nutrition & Energy segment, delivering steady margins—estimated EBITDA margin ~18–22% in FY2025—backed by Australia’s ~8.6 million annual cattle and sheep slaughter throughput.

Established collection networks and long-term supplier contracts secure feedstock volumes of ~200–300 ktpa, supplying low-cost inputs that fund GrainCorp’s investment into renewable fuel Stars (renewable diesel and SAF projects targeting 150 ML diesel equivalent by 2027).

These operations generate predictable free cash flow used for capex and R&D, lowering project financing needs and de‑risking transition to higher-growth biofuel assets.

- EBITDA margin: ~18–22% FY2025

- Feedstock: ~200–300 ktpa

- Domestic slaughter support: ~8.6M head/yr

- Target renewable output: 150 ML by 2027

GrainCorp: High-margin storage & oils fueling dividends and 150ML growth target

GrainCorp Cash Cows: ECA storage (31.6 Mt FY25, ~40% regional share, EBITDA ~18%, maintenance capex A$85–95m); 7 bulk ports (3.0 Mt non-grain, margin A$41m FY25); Edible oils (≈A$420m revenue FY24, utilization ~92%, EBIT ~6%); Domestic marketing (6.5 Mt FY25, funds 48c dividend); Tallow/UCO (200–300 ktpa, EBITDA 18–22%, supports 150 ML target by 2027).

| Asset | FY24/25 |

|---|---|

| ECA storage | 31.6 Mt; EBITDA ~18% |

| Ports | 3.0 Mt non-grain; A$41m |

| Edible oils | ≈A$420m; util 92% |

| Domestic | 6.5 Mt; 48c div |

| Tallow/UCO | 200–300 ktpa; EBITDA 18–22% |

Full Transparency, Always

GrainCorp BCG Matrix

The file you're previewing on this page is the exact GrainCorp BCG Matrix report you'll receive after purchase—no watermarks, no placeholders—just a fully formatted, analysis-ready document for strategic use.

This preview mirrors the final delivery, crafted with market-backed insights and clear visuals so the full file you download is presentation-ready and immediately actionable.

Upon purchase you’ll get the same editable file sent to your inbox, suitable for printing, team reviews, or client presentations without further edits.

Designed by strategy experts for clarity and decision-making, this GrainCorp BCG Matrix is ready to plug into your planning, reporting, or investor materials.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

GrainCorp’s BCG Matrix snapshot shows a mix of stable cash-generating grain handling assets and high-potential value-added offerings facing competitive pressure—insightful for portfolio prioritization and capital allocation.

Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Oilseed Crushing and Renewable Fuel Feedstocks

GrainCorp hit record oilseed crush volumes of 557,000 tonnes in FY25, cementing its Australian market-leader position and driving higher processing margins.

The unit is rapidly moving into renewable fuels, supplying feedstocks for Sustainable Aviation Fuel (SAF) and biodiesel and capturing growth from global decarbonization mandates.

Demand is expanding: SAF and biodiesel volumes are forecast to grow double digits annually to 2030, and GrainCorp benefits from policy support like the A$250 million federal grant for domestic refining projects.

Animal Nutrition and Feed Solutions

Animal Nutrition and Feed Solutions: volumes jumped to 713,000 tonnes in FY25 from 517,000 tonnes in FY24, a 38% rise driven by record Australian cattle-on-feed and stronger New Zealand dairy demand; segment revenue growth outpaced GrainCorp average, with FY25 EBITDA margin expanding ~220 basis points after integrating XFA; the XFA deal boosted high-value nutritional consulting and speciality feed sales, adding cross-sell opportunities and higher ASPs.

AgTech and Digital Supply Chain Services

GrainCorp’s $30 million corporate venture fund, launched 2023, backs AgTech and digital supply-chain startups to modernize the value chain, targeting supply-chain transparency, carbon tracking, and on-farm productivity tools.

These initiatives align with a 2024 industry shift: 42% CAGR in farm-management software adoption in APAC (2021–24), and carbon-tracking demand up 60% in 2023, positioning GrainCorp’s platforms as first-to-market.

Early results: pilot deployments across 1200 farms in 2024 drove a 15% uptake in premium market access and contributed to a 3–5% revenue uplift in participating grain origination hubs.

Low-Carbon Canola Supply Chain

GrainCorp Next entered year two in 2025, delivering an end-to-end low-carbon canola chain that achieved ISCC certification for 120,000 tonnes, capturing roughly 35% of GrainCorp’s specialty export volume to the EU and earning a 5–8% price premium versus standard canola.

This positions GrainCorp as a green-transition leader: low-carbon supply reduces Scope 3 risk, supports EU renewable mandates, and drove an estimated A$18–24m incremental EBITDA in 2025 from premium sales and new long-term offtake contracts.

- ISCC-certified 120,000 t in 2025

- ~35% share of specialty export market

- 5–8% price premium; A$18–24m EBITDA uplift

- Strengthens export access to EU renewable/feedstock rules

Specialty Chickpea and Pulse Programs

In FY25 GrainCorp’s Agribusiness saw a 28% EBITDA uplift from high-margin chickpea and pulse programs, driven by a 15% YoY rise in global pulse demand as plant-based protein; exports from its East Coast network grew 32% and captured an estimated 45% share of Australia’s chickpea export flow.

The broader grain market is mature, but specialty pulses rank as a BCG Star for the international trade desk—high growth and high market share, with pulse revenue up to AUD 210m in FY25 and margins ~18%.

- FY25 pulse revenue AUD 210m

- EBITDA uplift +28%

- Export volume +32% YoY

- Estimated 45% export market share

- Average margin ~18%

GrainCorp drives margin surge: ISCC canola, animal feed & pulses power FY25 growth

GrainCorp’s Stars: oilseed crush 557,000t FY25, animal feed 713,000t (+38% YoY), ISCC low‑carbon canola 120,000t (35% specialty export share, A$18–24m EBITDA uplift), pulses revenue A$210m (+28% EBITDA, 32% export vol). High growth segments + market leadership drive margin expansion and premium access to EU renewables.

| Metric | FY25 |

|---|---|

| Oilseed crush | 557,000 t |

| Animal feed volumes | 713,000 t |

| ISCC canola | 120,000 t |

| Pulse revenue | A$210m |

| Pulse margin | ~18% |

| Pulse export share | ~45% |

| ISCC EBITDA uplift | A$18–24m |

What is included in the product

BCG Matrix mapping of GrainCorp’s units with quadrant-specific strategies, investment recommendations, and trend-driven risks and opportunities.

One-page GrainCorp BCG Matrix placing each business unit in a quadrant for quick strategic clarity.

Cash Cows

East Coast Australia (ECA) Storage and Handling

GrainCorp’s East Coast Australia (ECA) Storage and Handling is a Cash Cow, holding ~40% share of eastern Australia grain production and handling 31.6 million tonnes in FY25, producing steady EBITDA margins near 18% and strong operating cash flow. The mature silo and rail network needs relatively low incremental capex (≈A$85–95m annual maintenance in FY25), funding dividends and investments into higher-growth renewables like biofuels.

Port Terminal Services and Bulk Materials

GrainCorp’s seven East Coast bulk port terminals are high-barrier-to-entry infrastructure that secure a durable competitive moat.

In FY25 the bulk materials program handled 3.0 million tonnes of non-grain cargo and delivered a record contribution margin of $41 million.

These ports generate steady cash through long-term contracts and diversified commodity flows—woodchips, cement, fertilizer—reducing revenue volatility.

Human Nutrition and Edible Oil Refining

As the largest refiner of edible fats and oils in Australia and New Zealand, GrainCorp’s Human Nutrition and Edible Oil Refining holds a commanding market share in a stable, mature food industry, supplying about 40–45% of regional refined oil volumes in 2024. Despite cyclical margin pressure—refining EBIT margins averaged ~6% in FY2024—the segment delivers steady revenue (≈A$420m in FY2024) by selling essential inputs to major food manufacturers and bakeries. It runs at high operational efficiency with utilization rates near 92% and requires maintenance-level capex (~A$15–20m annually), supporting GrainCorp’s corporate liquidity.

Domestic Grain Marketing and Distribution

GrainCorp’s domestic marketing arm links Australian growers to local flour millers, feed lots, and industrial users, holding a dominant share of internal grain trade in a mature market with stable logistics and low promo spend.

Domestic outloads reached 6.5 million tonnes in FY25, generating steady cash flows that underpin GrainCorp’s 48-cent-per-share dividend and fund capex for storage and rail upgrades.

- FY25 domestic outloads: 6.5 Mt

- Market: mature, low promo spend

- Customers: flour mills, feedlots, industrial users

- Supports dividend: 48c/share

- Uses: cash for capex, working capital

Tallow and Used Cooking Oil Collection

The collection and aggregation of tallow and used cooking oil is a mature, high-market-share cash cow in GrainCorp’s Nutrition & Energy segment, delivering steady margins—estimated EBITDA margin ~18–22% in FY2025—backed by Australia’s ~8.6 million annual cattle and sheep slaughter throughput.

Established collection networks and long-term supplier contracts secure feedstock volumes of ~200–300 ktpa, supplying low-cost inputs that fund GrainCorp’s investment into renewable fuel Stars (renewable diesel and SAF projects targeting 150 ML diesel equivalent by 2027).

These operations generate predictable free cash flow used for capex and R&D, lowering project financing needs and de‑risking transition to higher-growth biofuel assets.

- EBITDA margin: ~18–22% FY2025

- Feedstock: ~200–300 ktpa

- Domestic slaughter support: ~8.6M head/yr

- Target renewable output: 150 ML by 2027

GrainCorp: High-margin storage & oils fueling dividends and 150ML growth target

GrainCorp Cash Cows: ECA storage (31.6 Mt FY25, ~40% regional share, EBITDA ~18%, maintenance capex A$85–95m); 7 bulk ports (3.0 Mt non-grain, margin A$41m FY25); Edible oils (≈A$420m revenue FY24, utilization ~92%, EBIT ~6%); Domestic marketing (6.5 Mt FY25, funds 48c dividend); Tallow/UCO (200–300 ktpa, EBITDA 18–22%, supports 150 ML target by 2027).

| Asset | FY24/25 |

|---|---|

| ECA storage | 31.6 Mt; EBITDA ~18% |

| Ports | 3.0 Mt non-grain; A$41m |

| Edible oils | ≈A$420m; util 92% |

| Domestic | 6.5 Mt; 48c div |

| Tallow/UCO | 200–300 ktpa; EBITDA 18–22% |

Full Transparency, Always

GrainCorp BCG Matrix

The file you're previewing on this page is the exact GrainCorp BCG Matrix report you'll receive after purchase—no watermarks, no placeholders—just a fully formatted, analysis-ready document for strategic use.

This preview mirrors the final delivery, crafted with market-backed insights and clear visuals so the full file you download is presentation-ready and immediately actionable.

Upon purchase you’ll get the same editable file sent to your inbox, suitable for printing, team reviews, or client presentations without further edits.

Designed by strategy experts for clarity and decision-making, this GrainCorp BCG Matrix is ready to plug into your planning, reporting, or investor materials.