Gran Tierra Energy Porter's Five Forces Analysis

Don't Miss the Bigger Picture

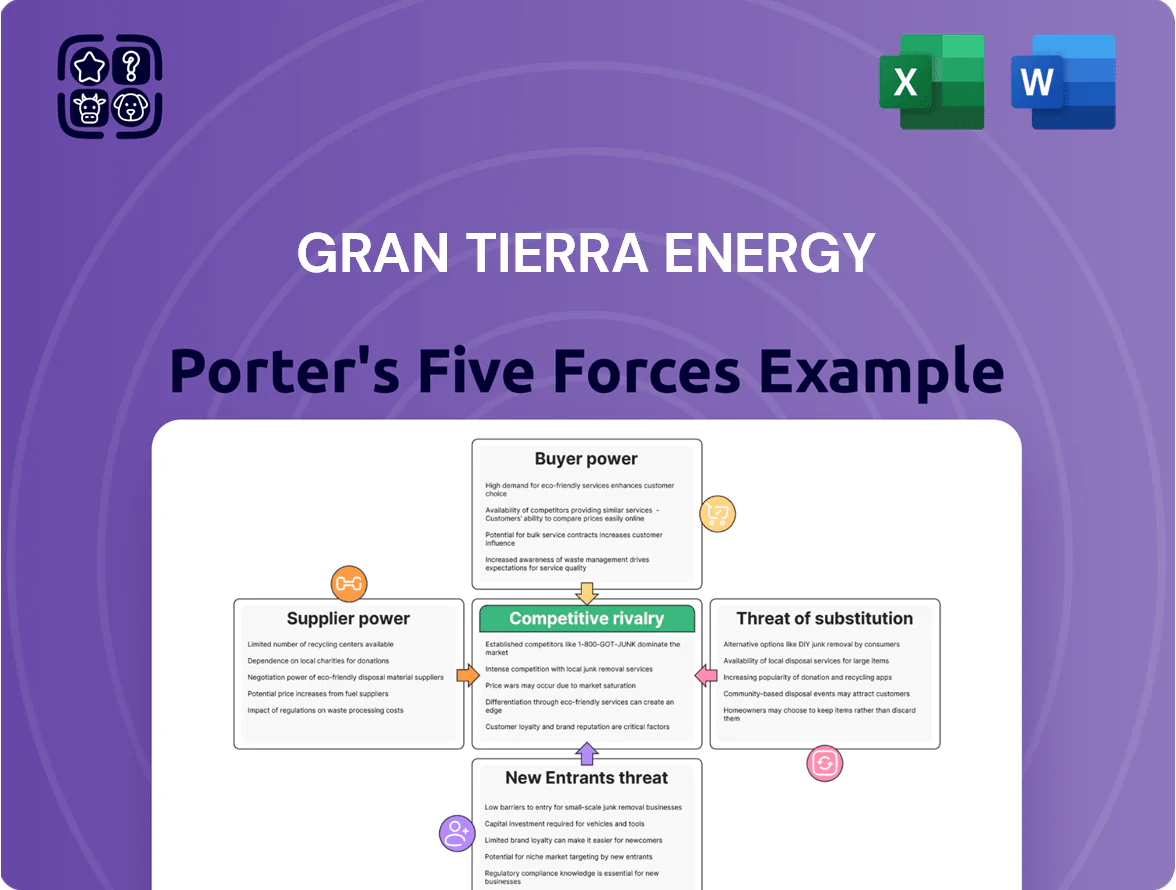

Gran Tierra Energy faces high competitive intensity from established E&P players, moderate supplier leverage due to service concentration, and variable buyer power tied to oil price volatility and offtake contracts.

Regulatory and environmental pressures raise barriers that both shield incumbents and elevate capital requirements, while substitutes and new entrants pose limited near-term threats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Gran Tierra Energy’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Specialized Oilfield Services

The market for high-tech drilling and completion services in Colombia is dominated by a few global players, notably SLB (Schlumberger) and Halliburton, which together held an estimated 60–70% share of service revenues in 2024 in the Andean region. As Gran Tierra scales projects in Putumayo and Llanos, its reliance on these suppliers rises, raising procurement risk. This supplier concentration lets providers sustain firm pricing—dayrates rose ~18% in 2024 during the crude rally—squeezing operator margins.

Local Community and Social License Demands

In Colombia local communities and indigenous groups act as critical suppliers of the social license to operate, giving them high bargaining power over Gran Tierra Energy; 2023 data shows social conflicts halted or delayed ~8% of national oil projects. They can disrupt operations via protests or legal challenges if demands for jobs and infrastructure go unmet, raising project risk and costs. Gran Tierra spent about $25–30 million on social programs and community investment in 2024 to secure access and reduce interruptions.

Rig Availability and Technical Equipment

The supply of high-spec drilling rigs for Putumayo Basin is tight; as of 2025 there were roughly 6–8 rigs regionally capable of ultra-deep or directional work, creating scarcity when activity rises.

Scarcity drives day rates up—regional premium rigs saw average rates rise 20–35% in 2024–25 to about USD 45,000–70,000/day—and contractors push for multi-year commitments.

Gran Tierra’s exploration pace and well count hinge on securing these constrained rigs at competitive rates; a single rig-week cost swing of USD 100k+ materially alters project IRR and cashflow timing.

Regulatory and Governmental Licensing

The Colombian National Hydrocarbons Agency (ANH) and environmental regulators act as near-monopolistic suppliers of exploration and production rights, setting work programs, royalty rates (Colombia royalties range 8–20% depending on field and contract), and strict environmental compliance with little room for negotiation.

Policy shifts or permit delays—ANH license backlogs rose ~15% in 2024—can push timelines, raise capex and operating costs, and hurt Gran Tierra Energy’s cash flow and reserve development plans.

- ANH controls access and terms

- Royalties typically 8–20%

- 2024 ANH backlog +15%

- Permit delays raise capex and slow production

Midstream Infrastructure and Pipeline Access

Gran Tierra relies on third-party pipelines and trucking to move crude to export points; in 2025 roughly 60–70% of its Colombian volumes use midstream routes including the Trans-Andean Pipeline (OTA).

Few pipeline alternatives give midstream operators pricing power; OTA bottlenecks let providers push tariff hikes that shave $2–8/boe from realized netbacks in stress periods.

Disruptions or rate increases directly cut cash flow and raise lifting breakeven per barrel.

- ~60–70% volumes via OTA

- $2–8/boe impact on netback

- Limited route alternatives → high supplier leverage

Service giants tighten grip: dayrates surge, royalties & midstream squeeze margins

Suppliers hold strong power: global service firms (SLB, Halliburton) captured ~60–70% Andean service revenue in 2024, driving dayrates +18% in 2024 and +20–35% for premium rigs into 2025 (USD 45k–70k/day). Local communities halted ~8% projects in 2023; Gran Tierra spent ~$25–30M on social programs in 2024. ANH sets royalties (8–20%) and permit backlogs +15% in 2024. Midstream (OTA) carries ~60–70% volumes, costing $2–8/boe in stress.

| Metric | Value |

|---|---|

| Service market share (SLB+Halliburton) | 60–70% (2024) |

| Premium rig rates | USD 45k–70k/day (2024–25) |

| Dayrate change | +18% (2024) |

| Community project halts | ~8% (2023) |

| Gran Tierra social spend | USD 25–30M (2024) |

| ANH royalty range | 8–20% |

| ANH backlog change | +15% (2024) |

| Volumes via OTA | 60–70% (2025) |

| Netback hit from midstream | USD 2–8/boe |

What is included in the product

Tailored exclusively for Gran Tierra Energy, this Porter's Five Forces overview uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and emerging threats shaping its profitability and strategic positioning.

One-sheet Porter's Five Forces tailored to Gran Tierra Energy—quickly spot upstream oil & gas risks and relief points for investment or strategy decisions.

Customers Bargaining Power

Dominance of State-Owned Refining Entities

Ecopetrol, owning about 75% of Colombia’s refining capacity as of 2025, functions as a near-monopsony for domestic crude, letting the state refiner set delivery schedules and benchmark-linked prices that squeeze upstream margins. Gran Tierra’s local sales are therefore tied to Ecopetrol’s operational needs and posted formulas, forcing the company to accept timing and quality adjustments and exposing it to refinery downtime risk and formula price volatility.

Global Commodity Market Price-Taking

As an independent producer, Gran Tierra Energy is a price-taker in the Brent crude market, so buyers pay benchmark prices and seldom pay a premium; in 2025 Brent averaged about $84/bbl, directly shaping company revenues. The firm’s cash flow tracks international benchmarks, leaving it exposed to shifts in refinery demand and trading-house flows—Brent volatility was ~32% annualized in 2024. Lacking pricing power, Gran Tierra must drive operational efficiency—2024 lifting costs were roughly $14–16/boe—to protect margins regardless of buyer identity.

Refining Requirements for Heavy Crude

Infrastructure-Driven Customer Lock-in

The physical tie to specific pipelines and export terminals constrains Gran Tierra Energy’s customer universe; in 2024 about 85% of its Ecuador and Colombia volumes flowed through two main corridors, limiting route options and price leverage.

That geographic lock-in lowers Gran Tierra’s ability to switch buyers for spot premiums, so terminal and pipeline owners can insist on firmer terms and longer tenors; negotiated discounts of $1–3/bbl versus Brent were common in 2024.

- ~85% volumes via two corridors (2024)

- Switching cost: limited alternate routes

- Buyers/terminals hold negotiating leverage

- Typical discount: $1–3 per barrel vs Brent (2024)

International Trading House Influence

Ecopetrol’s dominance squeezes Gran Tierra: heavy discounts and weak negotiating power

Customers hold strong bargaining power: Ecopetrol’s near-monopsony (≈75% domestic refining, 2025) and trader control (>60% exports, 2025) force Gran Tierra to accept posted formulas, timing, and discounts; heavy-sour differentials ran $10–18/bbl (2024–25) and pipeline lock-in sent common discounts $1–3/bbl (2024), while Gran Tierra’s ~35,000 boe/d (2024) scale and $14–16/boe lifting cost limit its negotiating leverage.

| Metric | Value |

|---|---|

| Ecopetrol refinery share (2025) | ≈75% |

| Traders' export control (2025) | >60% |

| GTE production (2024) | ≈35,000 boe/d |

| Heavy-sour differential (2024–25) | $10–18/bbl |

| Common pipeline/terminal discount (2024) | $1–3/bbl |

| Lifting cost (2024) | $14–16/boe |

Preview the Actual Deliverable

Gran Tierra Energy Porter's Five Forces Analysis

This preview shows the exact Gran Tierra Energy Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or samples.

The document displayed here is the full, professionally formatted analysis ready for download and use the moment you buy.

No mockups: this is the same complete file you’ll get instantly after payment, prepared for immediate application.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Gran Tierra Energy faces high competitive intensity from established E&P players, moderate supplier leverage due to service concentration, and variable buyer power tied to oil price volatility and offtake contracts.

Regulatory and environmental pressures raise barriers that both shield incumbents and elevate capital requirements, while substitutes and new entrants pose limited near-term threats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Gran Tierra Energy’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Specialized Oilfield Services

The market for high-tech drilling and completion services in Colombia is dominated by a few global players, notably SLB (Schlumberger) and Halliburton, which together held an estimated 60–70% share of service revenues in 2024 in the Andean region. As Gran Tierra scales projects in Putumayo and Llanos, its reliance on these suppliers rises, raising procurement risk. This supplier concentration lets providers sustain firm pricing—dayrates rose ~18% in 2024 during the crude rally—squeezing operator margins.

Local Community and Social License Demands

In Colombia local communities and indigenous groups act as critical suppliers of the social license to operate, giving them high bargaining power over Gran Tierra Energy; 2023 data shows social conflicts halted or delayed ~8% of national oil projects. They can disrupt operations via protests or legal challenges if demands for jobs and infrastructure go unmet, raising project risk and costs. Gran Tierra spent about $25–30 million on social programs and community investment in 2024 to secure access and reduce interruptions.

Rig Availability and Technical Equipment

The supply of high-spec drilling rigs for Putumayo Basin is tight; as of 2025 there were roughly 6–8 rigs regionally capable of ultra-deep or directional work, creating scarcity when activity rises.

Scarcity drives day rates up—regional premium rigs saw average rates rise 20–35% in 2024–25 to about USD 45,000–70,000/day—and contractors push for multi-year commitments.

Gran Tierra’s exploration pace and well count hinge on securing these constrained rigs at competitive rates; a single rig-week cost swing of USD 100k+ materially alters project IRR and cashflow timing.

Regulatory and Governmental Licensing

The Colombian National Hydrocarbons Agency (ANH) and environmental regulators act as near-monopolistic suppliers of exploration and production rights, setting work programs, royalty rates (Colombia royalties range 8–20% depending on field and contract), and strict environmental compliance with little room for negotiation.

Policy shifts or permit delays—ANH license backlogs rose ~15% in 2024—can push timelines, raise capex and operating costs, and hurt Gran Tierra Energy’s cash flow and reserve development plans.

- ANH controls access and terms

- Royalties typically 8–20%

- 2024 ANH backlog +15%

- Permit delays raise capex and slow production

Midstream Infrastructure and Pipeline Access

Gran Tierra relies on third-party pipelines and trucking to move crude to export points; in 2025 roughly 60–70% of its Colombian volumes use midstream routes including the Trans-Andean Pipeline (OTA).

Few pipeline alternatives give midstream operators pricing power; OTA bottlenecks let providers push tariff hikes that shave $2–8/boe from realized netbacks in stress periods.

Disruptions or rate increases directly cut cash flow and raise lifting breakeven per barrel.

- ~60–70% volumes via OTA

- $2–8/boe impact on netback

- Limited route alternatives → high supplier leverage

Service giants tighten grip: dayrates surge, royalties & midstream squeeze margins

Suppliers hold strong power: global service firms (SLB, Halliburton) captured ~60–70% Andean service revenue in 2024, driving dayrates +18% in 2024 and +20–35% for premium rigs into 2025 (USD 45k–70k/day). Local communities halted ~8% projects in 2023; Gran Tierra spent ~$25–30M on social programs in 2024. ANH sets royalties (8–20%) and permit backlogs +15% in 2024. Midstream (OTA) carries ~60–70% volumes, costing $2–8/boe in stress.

| Metric | Value |

|---|---|

| Service market share (SLB+Halliburton) | 60–70% (2024) |

| Premium rig rates | USD 45k–70k/day (2024–25) |

| Dayrate change | +18% (2024) |

| Community project halts | ~8% (2023) |

| Gran Tierra social spend | USD 25–30M (2024) |

| ANH royalty range | 8–20% |

| ANH backlog change | +15% (2024) |

| Volumes via OTA | 60–70% (2025) |

| Netback hit from midstream | USD 2–8/boe |

What is included in the product

Tailored exclusively for Gran Tierra Energy, this Porter's Five Forces overview uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and emerging threats shaping its profitability and strategic positioning.

One-sheet Porter's Five Forces tailored to Gran Tierra Energy—quickly spot upstream oil & gas risks and relief points for investment or strategy decisions.

Customers Bargaining Power

Dominance of State-Owned Refining Entities

Ecopetrol, owning about 75% of Colombia’s refining capacity as of 2025, functions as a near-monopsony for domestic crude, letting the state refiner set delivery schedules and benchmark-linked prices that squeeze upstream margins. Gran Tierra’s local sales are therefore tied to Ecopetrol’s operational needs and posted formulas, forcing the company to accept timing and quality adjustments and exposing it to refinery downtime risk and formula price volatility.

Global Commodity Market Price-Taking

As an independent producer, Gran Tierra Energy is a price-taker in the Brent crude market, so buyers pay benchmark prices and seldom pay a premium; in 2025 Brent averaged about $84/bbl, directly shaping company revenues. The firm’s cash flow tracks international benchmarks, leaving it exposed to shifts in refinery demand and trading-house flows—Brent volatility was ~32% annualized in 2024. Lacking pricing power, Gran Tierra must drive operational efficiency—2024 lifting costs were roughly $14–16/boe—to protect margins regardless of buyer identity.

Refining Requirements for Heavy Crude

Infrastructure-Driven Customer Lock-in

The physical tie to specific pipelines and export terminals constrains Gran Tierra Energy’s customer universe; in 2024 about 85% of its Ecuador and Colombia volumes flowed through two main corridors, limiting route options and price leverage.

That geographic lock-in lowers Gran Tierra’s ability to switch buyers for spot premiums, so terminal and pipeline owners can insist on firmer terms and longer tenors; negotiated discounts of $1–3/bbl versus Brent were common in 2024.

- ~85% volumes via two corridors (2024)

- Switching cost: limited alternate routes

- Buyers/terminals hold negotiating leverage

- Typical discount: $1–3 per barrel vs Brent (2024)

International Trading House Influence

Ecopetrol’s dominance squeezes Gran Tierra: heavy discounts and weak negotiating power

Customers hold strong bargaining power: Ecopetrol’s near-monopsony (≈75% domestic refining, 2025) and trader control (>60% exports, 2025) force Gran Tierra to accept posted formulas, timing, and discounts; heavy-sour differentials ran $10–18/bbl (2024–25) and pipeline lock-in sent common discounts $1–3/bbl (2024), while Gran Tierra’s ~35,000 boe/d (2024) scale and $14–16/boe lifting cost limit its negotiating leverage.

| Metric | Value |

|---|---|

| Ecopetrol refinery share (2025) | ≈75% |

| Traders' export control (2025) | >60% |

| GTE production (2024) | ≈35,000 boe/d |

| Heavy-sour differential (2024–25) | $10–18/bbl |

| Common pipeline/terminal discount (2024) | $1–3/bbl |

| Lifting cost (2024) | $14–16/boe |

Preview the Actual Deliverable

Gran Tierra Energy Porter's Five Forces Analysis

This preview shows the exact Gran Tierra Energy Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or samples.

The document displayed here is the full, professionally formatted analysis ready for download and use the moment you buy.

No mockups: this is the same complete file you’ll get instantly after payment, prepared for immediate application.