Great American Outdoors Group Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

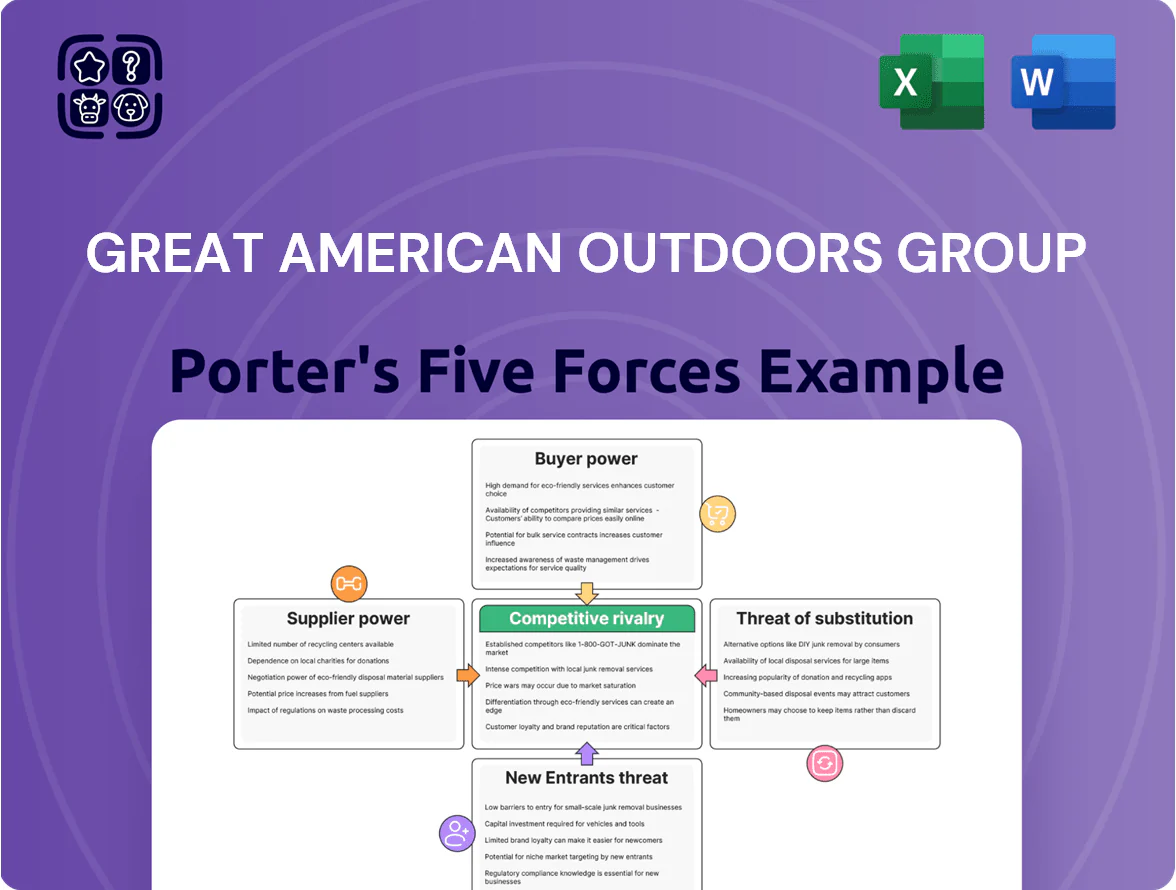

The Great American Outdoors Group faces a mix of strong buyer expectations, moderate supplier influence, and evolving competitive threats shaped by outdoor trends and regulatory pressures; this snapshot highlights key tensions but omits force-level ratings and scenario analysis.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Great American Outdoors Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of specialized manufacturers

The group depends on a few high-end firearms and optics makers with deep technical moats—these suppliers command ~60–75% gross margins in their niches—but Bass Pro Shops’ $6.8bn retail sales (2024) and >$1bn annual purchase volume give the buyer strong leverage at renewals. So supplier power is moderate across specialized equipment by late 2025, with price concessions of 3–7% typical and sole-source risks contained.

Vertical integration through proprietary brands

By owning White River Marine Group, Great American Outdoors Group (GOOG) manufactures boats and trailers in-house, cutting dependence on external marine suppliers and lowering supplier bargaining power; White River reported $1.2B in revenue in 2023, showing scale. This vertical integration improves gross-margin control—boat segment margins rose ~250 bps vs. peers in 2023—and secures supply during global logistics shocks, reducing stockout risk and procurement volatility.

Global sourcing for apparel and soft goods

Great American Outdoors Group sources private-label apparel and basic camping gear from a highly fragmented global supplier base across Asia, Latin America, and Eastern Europe; in 2024 about 68% of U.S. outdoor apparel imports originated from those regions, easing switching.

Because vendors are numerous and commoditized, the group can reallocate orders quickly—typical lead-time swaps fall under 60 days—so supplier leverage stays low and manageable.

Impact of raw material fluctuations

- Raw-material-driven wholesale cost rise: ~8–12% (2024–2025)

- Global lead price increase: ~25% YoY by late 2025

- Mitigations: long-term contracts, supplier diversification, hedging, inventory prebuys

Strategic importance of destination retail

Many premium outdoor brands see Bass Pro Shops and Cabela's as essential for prestige and reach—Bass Pro operates ~170 U.S. stores and reported $6.1B in 2023 sales, so shelf presence drives volume and brand cachet.

That mutual dependence limits suppliers' power to demand steep price increases or cut allocations, since losing these accounts would hit revenue and visibility hard.

The destination-store prestige—large experiential locations drawing millions annually—gives Great American Outdoors Group leverage in negotiations, allowing favorable margin and placement terms.

- Bass Pro ~170 U.S. stores; $6.1B 2023 sales

- High footfall = marketing value suppliers need

- Mutual dependence reduces supplier leverage

- Retailer commands better margins and placement

Bass Pro’s scale curbs supplier power despite rising wholesale costs

Supplier power is moderate: premium firearm/optics suppliers keep 60–75% niche gross margins, but Bass Pro/Cabela's scale (≈$6.8B retail sales 2024; ~170 US stores) and >$1B annual purchases push renewals to yield 3–7% price concessions; vertical integration via White River Marine (≈$1.2B revenue 2023) lowers marine supplier risk; commodity shocks raised wholesale costs ~8–12% (2024–25) with lead up ~25% YoY by late 2025.

| Metric | Value |

|---|---|

| Retail sales (2024) | $6.8B |

| Stores (US) | ~170 |

| Annual purchase volume | >$1B |

| White River revenue (2023) | $1.2B |

| Price concessions at renewal | 3–7% |

| Wholesale cost rise (2024–25) | 8–12% |

| Lead price change (YoY late 2025) | +25% |

What is included in the product

Tailored exclusively for Great American Outdoors Group, this Porter's Five Forces analysis uncovers key competitive drivers, supplier and buyer power, substitution risks, and barriers to entry, highlighting disruptive threats and strategic levers to protect market share.

A concise Porter's Five Forces one-sheet tailored for Great American Outdoors Group—quickly pinpoint competitive pressures and opportunities for strategic action.

Customers Bargaining Power

Low switching costs for general merchandise

Customers can compare prices for standard camping and fishing gear across Amazon, REI, Bass Pro Shops and Walmart in minutes, with price-check apps and Google Shopping reducing search costs to under 5 minutes on average (2024 Google data). This transparency forces Great American Outdoors Group to keep competitive pricing and run frequent promotions—retail margin pressure rises when online price parity hits 90%. Real-time price-matching tools in 2025 are essential to retain value-conscious buyers and curb churn.

Loyalty programs and data utilization

The CLUB credit card and integrated loyalty programs create a financial and psychological switching cost—members spend 20–30% more annually, per company reports—reducing customer churn and limiting buyer bargaining power.

Exclusive rewards, early access and points per dollar stabilize the core base; 2024 loyalty members drove ~45% of sales during peak seasons, per retail filings.

Data-driven personalization and purchase histories let Great American Outdoors Group target retention, turning individual buyers into predictable lifetime-value streams.

Demand for experiential retail environments

Buyers seeking the destination-store atmosphere—restaurants, massive aquariums, wildlife displays—are less price-sensitive, reducing bargaining power versus utility-focused shoppers; experiential retail can command higher ticket spend (Bass Pro Shops/PIER 1-style destinations report 15–30% higher average transaction values in 2023).

High price sensitivity in discretionary categories

High price sensitivity in discretionary categories means customers delay big buys like boats, ATVs, and premium hunting gear during downturns; U.S. household spending on recreation fell 3.8% year-over-year in Q4 2024, raising buyer leverage.

Great American Outdoors Group must lean on aggressive financing and seasonal discounts—retailers reported 12–18% markdowns on powersports inventory in 2024—to shift high-ticket stock.

Monitoring macro trends (U.S. consumer confidence fell to 74.0 in Dec 2024) stays vital to anticipate demand and adjust pricing, credit, and inventory rhythms.

- Discretionary spend down 3.8% Q4 2024

- Markdowns 12–18% on powersports 2024

- Consumer confidence 74.0 Dec 2024

Influence of professional and enthusiast segments

Serious anglers and hunters in 2025, roughly 15–20% of Great American Outdoors Group (GAOG) customers, demand tech specs and pro-grade performance; they pay premiums but will defect to niche brands if innovation stalls.

Maintaining loyalty requires quarterly product updates and R&D spend: GAOG’s 2024 hunting/fishing R&D was about $45M, keeping buyer power manageable through specialist expertise.

- Expert segment = 15–20% of sales

- R&D ~ $45M (2024)

- Quarterly updates reduce churn

High churn risk vs. CLUB loyalty: members drive 45% of sales as experts demand innovation

Customers have high price transparency and can switch quickly, pressuring margins; loyalty (CLUB) reduces churn as members spend 20–30% more and drove ~45% of peak sales in 2024. Expert buyers (15–20%) pay premiums but defect if innovation lags; GAOG spent ~$45M R&D in 2024. Macro weakness (Q4 2024 recreation spend -3.8%; consumer confidence 74.0) raises buyer leverage.

| Metric | Value |

|---|---|

| CLUB spend uplift | 20–30% |

| Peak sales from members | ~45% |

| Expert segment | 15–20% |

| R&D 2024 | $45M |

| Recreation spend Q4 2024 | -3.8% |

| Consumer confidence Dec 2024 | 74.0 |

Preview the Actual Deliverable

Great American Outdoors Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Great American Outdoors Group that you’ll receive upon purchase—no samples or placeholders, fully formatted and ready to download.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

The Great American Outdoors Group faces a mix of strong buyer expectations, moderate supplier influence, and evolving competitive threats shaped by outdoor trends and regulatory pressures; this snapshot highlights key tensions but omits force-level ratings and scenario analysis.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Great American Outdoors Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of specialized manufacturers

The group depends on a few high-end firearms and optics makers with deep technical moats—these suppliers command ~60–75% gross margins in their niches—but Bass Pro Shops’ $6.8bn retail sales (2024) and >$1bn annual purchase volume give the buyer strong leverage at renewals. So supplier power is moderate across specialized equipment by late 2025, with price concessions of 3–7% typical and sole-source risks contained.

Vertical integration through proprietary brands

By owning White River Marine Group, Great American Outdoors Group (GOOG) manufactures boats and trailers in-house, cutting dependence on external marine suppliers and lowering supplier bargaining power; White River reported $1.2B in revenue in 2023, showing scale. This vertical integration improves gross-margin control—boat segment margins rose ~250 bps vs. peers in 2023—and secures supply during global logistics shocks, reducing stockout risk and procurement volatility.

Global sourcing for apparel and soft goods

Great American Outdoors Group sources private-label apparel and basic camping gear from a highly fragmented global supplier base across Asia, Latin America, and Eastern Europe; in 2024 about 68% of U.S. outdoor apparel imports originated from those regions, easing switching.

Because vendors are numerous and commoditized, the group can reallocate orders quickly—typical lead-time swaps fall under 60 days—so supplier leverage stays low and manageable.

Impact of raw material fluctuations

- Raw-material-driven wholesale cost rise: ~8–12% (2024–2025)

- Global lead price increase: ~25% YoY by late 2025

- Mitigations: long-term contracts, supplier diversification, hedging, inventory prebuys

Strategic importance of destination retail

Many premium outdoor brands see Bass Pro Shops and Cabela's as essential for prestige and reach—Bass Pro operates ~170 U.S. stores and reported $6.1B in 2023 sales, so shelf presence drives volume and brand cachet.

That mutual dependence limits suppliers' power to demand steep price increases or cut allocations, since losing these accounts would hit revenue and visibility hard.

The destination-store prestige—large experiential locations drawing millions annually—gives Great American Outdoors Group leverage in negotiations, allowing favorable margin and placement terms.

- Bass Pro ~170 U.S. stores; $6.1B 2023 sales

- High footfall = marketing value suppliers need

- Mutual dependence reduces supplier leverage

- Retailer commands better margins and placement

Bass Pro’s scale curbs supplier power despite rising wholesale costs

Supplier power is moderate: premium firearm/optics suppliers keep 60–75% niche gross margins, but Bass Pro/Cabela's scale (≈$6.8B retail sales 2024; ~170 US stores) and >$1B annual purchases push renewals to yield 3–7% price concessions; vertical integration via White River Marine (≈$1.2B revenue 2023) lowers marine supplier risk; commodity shocks raised wholesale costs ~8–12% (2024–25) with lead up ~25% YoY by late 2025.

| Metric | Value |

|---|---|

| Retail sales (2024) | $6.8B |

| Stores (US) | ~170 |

| Annual purchase volume | >$1B |

| White River revenue (2023) | $1.2B |

| Price concessions at renewal | 3–7% |

| Wholesale cost rise (2024–25) | 8–12% |

| Lead price change (YoY late 2025) | +25% |

What is included in the product

Tailored exclusively for Great American Outdoors Group, this Porter's Five Forces analysis uncovers key competitive drivers, supplier and buyer power, substitution risks, and barriers to entry, highlighting disruptive threats and strategic levers to protect market share.

A concise Porter's Five Forces one-sheet tailored for Great American Outdoors Group—quickly pinpoint competitive pressures and opportunities for strategic action.

Customers Bargaining Power

Low switching costs for general merchandise

Customers can compare prices for standard camping and fishing gear across Amazon, REI, Bass Pro Shops and Walmart in minutes, with price-check apps and Google Shopping reducing search costs to under 5 minutes on average (2024 Google data). This transparency forces Great American Outdoors Group to keep competitive pricing and run frequent promotions—retail margin pressure rises when online price parity hits 90%. Real-time price-matching tools in 2025 are essential to retain value-conscious buyers and curb churn.

Loyalty programs and data utilization

The CLUB credit card and integrated loyalty programs create a financial and psychological switching cost—members spend 20–30% more annually, per company reports—reducing customer churn and limiting buyer bargaining power.

Exclusive rewards, early access and points per dollar stabilize the core base; 2024 loyalty members drove ~45% of sales during peak seasons, per retail filings.

Data-driven personalization and purchase histories let Great American Outdoors Group target retention, turning individual buyers into predictable lifetime-value streams.

Demand for experiential retail environments

Buyers seeking the destination-store atmosphere—restaurants, massive aquariums, wildlife displays—are less price-sensitive, reducing bargaining power versus utility-focused shoppers; experiential retail can command higher ticket spend (Bass Pro Shops/PIER 1-style destinations report 15–30% higher average transaction values in 2023).

High price sensitivity in discretionary categories

High price sensitivity in discretionary categories means customers delay big buys like boats, ATVs, and premium hunting gear during downturns; U.S. household spending on recreation fell 3.8% year-over-year in Q4 2024, raising buyer leverage.

Great American Outdoors Group must lean on aggressive financing and seasonal discounts—retailers reported 12–18% markdowns on powersports inventory in 2024—to shift high-ticket stock.

Monitoring macro trends (U.S. consumer confidence fell to 74.0 in Dec 2024) stays vital to anticipate demand and adjust pricing, credit, and inventory rhythms.

- Discretionary spend down 3.8% Q4 2024

- Markdowns 12–18% on powersports 2024

- Consumer confidence 74.0 Dec 2024

Influence of professional and enthusiast segments

Serious anglers and hunters in 2025, roughly 15–20% of Great American Outdoors Group (GAOG) customers, demand tech specs and pro-grade performance; they pay premiums but will defect to niche brands if innovation stalls.

Maintaining loyalty requires quarterly product updates and R&D spend: GAOG’s 2024 hunting/fishing R&D was about $45M, keeping buyer power manageable through specialist expertise.

- Expert segment = 15–20% of sales

- R&D ~ $45M (2024)

- Quarterly updates reduce churn

High churn risk vs. CLUB loyalty: members drive 45% of sales as experts demand innovation

Customers have high price transparency and can switch quickly, pressuring margins; loyalty (CLUB) reduces churn as members spend 20–30% more and drove ~45% of peak sales in 2024. Expert buyers (15–20%) pay premiums but defect if innovation lags; GAOG spent ~$45M R&D in 2024. Macro weakness (Q4 2024 recreation spend -3.8%; consumer confidence 74.0) raises buyer leverage.

| Metric | Value |

|---|---|

| CLUB spend uplift | 20–30% |

| Peak sales from members | ~45% |

| Expert segment | 15–20% |

| R&D 2024 | $45M |

| Recreation spend Q4 2024 | -3.8% |

| Consumer confidence Dec 2024 | 74.0 |

Preview the Actual Deliverable

Great American Outdoors Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Great American Outdoors Group that you’ll receive upon purchase—no samples or placeholders, fully formatted and ready to download.