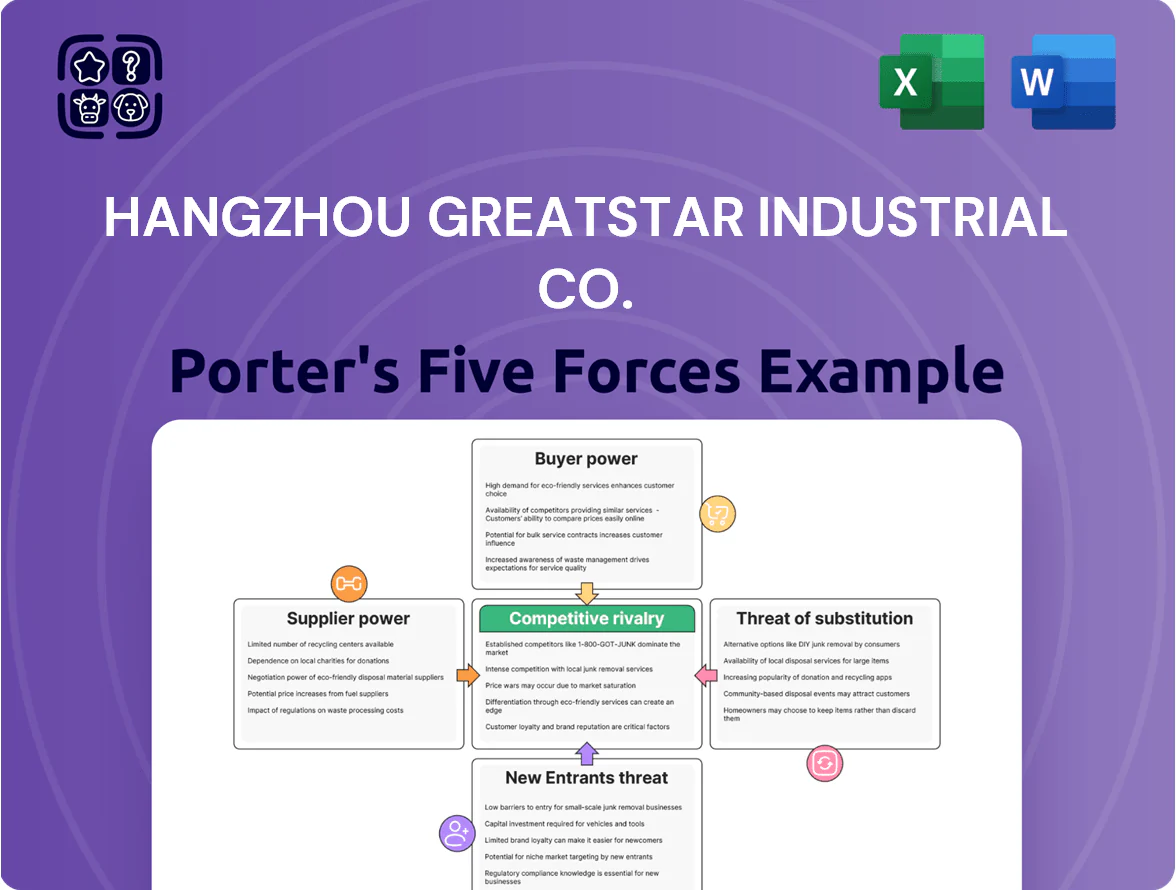

Hangzhou GreatStar Industrial Co. Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Hangzhou GreatStar faces moderate supplier leverage due to diversified component sourcing, intense rivalry from global toolmakers, and rising pressure from low-cost entrants and substitutes in hand and power tools.

Buyers wield significant power in professional and retail channels, while regulatory and tech shifts shape margins and product differentiation opportunities.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Hangzhou GreatStar Industrial Co.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Commodity Price Volatility

GreatStar depends on steel, plastic resins and lithium-ion cells; steel accounted for ~28% of COGS in 2024 and battery cells rose 35% YOY in 2024–25, pushing input cost pressure.

The firm buys from many suppliers and used scale to secure discounts—procurement saved an estimated $120M in 2024—yet remains exposed to systemic shocks in nickel, cobalt and petrochemical markets.

As of late 2025, LME nickel up 42% year-to-date and global resin tightness kept polymer prices ~18% above 2023 levels, so supplier power spikes can rapidly erode margins.

Fragmentation of the Chinese Manufacturing Base

A significant portion of GreatStar’s supply chain sits in China’s fragmented manufacturing clusters, where tens of thousands of small suppliers compete for volume; in 2024 Zhejiang province reported over 120,000 SMEs in metalworking, keeping individual supplier leverage low.

This fragmentation cuts supplier bargaining power as small vendors undercut each other for GreatStar’s high-volume orders, helping the company secure price concessions averaging 5–10% versus single-sourced contracts.

Maintaining a diverse supplier base—over 300 active component vendors in 2024—ensures no single supplier can dictate terms or halt production, lowering disruption risk and supporting stable gross margins around 28% in FY2024.

Strategic Vertical Integration Efforts

GreatStar has boosted vertical integration, acquiring manufacturing units and brands so in-house production rose to ~45% of component volume by 2025, cutting reliance on external vendors.

This shift trims supplier price exposure—internal sourcing saved an estimated CNY 320 million in input costs in 2024–25—and tightens quality control across the product lifecycle.

Logistics and International Shipping Constraints

- Top-10 carriers ≈80% capacity (2024)

- Long-term contracts ≈60% of volume (2024)

- Main export ports: Ningbo, Shanghai, Shenzhen

- Stabilized rates vs. 2021–22 peak but concentrated market

Technological Sophistication of Battery Suppliers

- High consolidation: ~6 firms >60% premium cells

- 2024 market: 72% premium-cell share in cordless tools

- Implication: higher input price sensitivity

- Mitigation: diversify cell partners, invest in cell-testing

GreatStar mitigates supplier concentration—45% vertical integration, 300+ vendors, 60% freight cover

Suppliers wield moderate power: commodity inputs (steel ~28% of COGS 2024) are fragmented and weak, but specialty lithium cells and global carriers are concentrated—nickel +42% YTD 2025; 6 firms >60% premium cells (2024); top-10 carriers ~80% capacity (2024)—GreatStar counters with 300+ vendors, 45% vertical integration (2025) and long-term freight contracts (~60% volume 2024).

| Metric | Value |

|---|---|

| Steel share of COGS | ~28% (2024) |

| Vertical integration | ~45% component volume (2025) |

| Active suppliers | 300+ (2024) |

| Premium cell concentration | 6 firms >60% (2024) |

| Nickel price move | +42% YTD (2025) |

| Top-10 carriers share | ~80% (2024) |

| Long-term freight cover | ~60% volume (2024) |

What is included in the product

Tailored exclusively for Hangzhou GreatStar Industrial Co., this Porter's Five Forces overview uncovers competitive drivers, buyer/supplier influence, entry barriers, substitute threats, and strategic levers shaping its industry position.

Concise Porter's Five Forces snapshot tailored for Hangzhou GreatStar—quickly spot supplier/buyer leverage, competitive rivalry, threats from new entrants/substitutes and regulatory pressure to guide strategic decisions.

Customers Bargaining Power

Concentration of Big-Box Retail Power

Low Switching Costs for DIY Consumers

Individual DIY users face low switching costs between hand-tool and basic power-tool brands, so GreatStar (Hangzhou GreatStar Industrial Co., founded 1999) must compete on price, ergonomics, and perceived value to retain buyers.

Global DIY tool market grew 3.8% in 2024 to $43.2B; with 60% of DIY purchases price-driven, many consumers pick the best immediate deal or feature set, increasing churn risk for GreatStar.

Growth of E-commerce and Direct Comparison

The rise of Amazon and marketplaces gives buyers instant price checks and peer reviews; global e-commerce GMV hit about 5.7 trillion USD in 2023 and marketplaces accounted for ~52% of that, so visibility depends on price and ratings.

GreatStar must keep competitive prices and >=4.0 ratings to appear in search algorithms and avoid Buy Box losses; a 1-star drop can cut conversion by ~16%.

Customers can switch fast to emerging brands—online private labels grew 18% YoY in 2024—so GreatStar’s reputation for quality and value is critical to retain share.

Rise of Private Label Brand Competition

Many of GreatStar’s top customers—large US and EU retailers—sell private-label tools that directly compete with GreatStar’s branded lines, capturing up to 20–30% gross margin advantage via lower price points and better shelf placement.

Retailers can prioritize house brands in promotions and displays, pressuring GreatStar’s volumes and margins; in 2024 private-label penetration in hand tools rose ~4 percentage points in key markets.

GreatStar counters through R&D on product features, and by leveraging acquisitions—Arrow (2019) and SK Professional Tools (2020)—to defend pricing and justify premium listings.

- Private-label can undercut by 20–30% on price

- Retailer promo control reduces branded shelf share

- 2024 private-label hand-tool share +4 ppt in core markets

- Acquired brands (Arrow, SK) used to defend premium positioning

Professional User Loyalty and Technical Requirements

Professional tradespeople show higher brand loyalty than DIY buyers but demand superior performance; industry surveys in 2024 report 62% of pros recommend brands based on durability and warranty terms.

These users shape market trends via preference for specialized features—torque, ergonomics, IP ratings—forcing GreatStar to spend more on R&D; GreatStar reported R&D up 18% in 2023 to ¥120 million (≈$16.5M).

Endorsement from pros drives long-term brand equity and resale channels, so losing pro support would materially hit sales in pro segments, which made ~38% of China tool market revenue in 2023.

- Pros = higher loyalty, higher expectations

- 62% of pros recommend on durability (2024)

- GreatStar R&D +18% to ¥120M in 2023

- Pro segment ≈38% of China tool revenue (2023)

Retailer power squeezes margins; R&D & M&A defend brands amid fierce marketplace pricing

| Metric | 2023–2024 |

|---|---|

| Retailer share of sales | 25–35% |

| Gross margin | ~29% (2023) |

| R&D spend | ¥120M (+18% 2023) |

| Marketplace share (GMV) | ~52% of $5.7T (2023) |

| Pro recommendation | 62% (2024) |

Preview Before You Purchase

Hangzhou GreatStar Industrial Co. Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Hangzhou GreatStar Industrial Co. you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted, professionally written, and ready for download and use the moment you buy. It contains the complete assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry tailored to GreatStar.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Hangzhou GreatStar faces moderate supplier leverage due to diversified component sourcing, intense rivalry from global toolmakers, and rising pressure from low-cost entrants and substitutes in hand and power tools.

Buyers wield significant power in professional and retail channels, while regulatory and tech shifts shape margins and product differentiation opportunities.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Hangzhou GreatStar Industrial Co.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Commodity Price Volatility

GreatStar depends on steel, plastic resins and lithium-ion cells; steel accounted for ~28% of COGS in 2024 and battery cells rose 35% YOY in 2024–25, pushing input cost pressure.

The firm buys from many suppliers and used scale to secure discounts—procurement saved an estimated $120M in 2024—yet remains exposed to systemic shocks in nickel, cobalt and petrochemical markets.

As of late 2025, LME nickel up 42% year-to-date and global resin tightness kept polymer prices ~18% above 2023 levels, so supplier power spikes can rapidly erode margins.

Fragmentation of the Chinese Manufacturing Base

A significant portion of GreatStar’s supply chain sits in China’s fragmented manufacturing clusters, where tens of thousands of small suppliers compete for volume; in 2024 Zhejiang province reported over 120,000 SMEs in metalworking, keeping individual supplier leverage low.

This fragmentation cuts supplier bargaining power as small vendors undercut each other for GreatStar’s high-volume orders, helping the company secure price concessions averaging 5–10% versus single-sourced contracts.

Maintaining a diverse supplier base—over 300 active component vendors in 2024—ensures no single supplier can dictate terms or halt production, lowering disruption risk and supporting stable gross margins around 28% in FY2024.

Strategic Vertical Integration Efforts

GreatStar has boosted vertical integration, acquiring manufacturing units and brands so in-house production rose to ~45% of component volume by 2025, cutting reliance on external vendors.

This shift trims supplier price exposure—internal sourcing saved an estimated CNY 320 million in input costs in 2024–25—and tightens quality control across the product lifecycle.

Logistics and International Shipping Constraints

- Top-10 carriers ≈80% capacity (2024)

- Long-term contracts ≈60% of volume (2024)

- Main export ports: Ningbo, Shanghai, Shenzhen

- Stabilized rates vs. 2021–22 peak but concentrated market

Technological Sophistication of Battery Suppliers

- High consolidation: ~6 firms >60% premium cells

- 2024 market: 72% premium-cell share in cordless tools

- Implication: higher input price sensitivity

- Mitigation: diversify cell partners, invest in cell-testing

GreatStar mitigates supplier concentration—45% vertical integration, 300+ vendors, 60% freight cover

Suppliers wield moderate power: commodity inputs (steel ~28% of COGS 2024) are fragmented and weak, but specialty lithium cells and global carriers are concentrated—nickel +42% YTD 2025; 6 firms >60% premium cells (2024); top-10 carriers ~80% capacity (2024)—GreatStar counters with 300+ vendors, 45% vertical integration (2025) and long-term freight contracts (~60% volume 2024).

| Metric | Value |

|---|---|

| Steel share of COGS | ~28% (2024) |

| Vertical integration | ~45% component volume (2025) |

| Active suppliers | 300+ (2024) |

| Premium cell concentration | 6 firms >60% (2024) |

| Nickel price move | +42% YTD (2025) |

| Top-10 carriers share | ~80% (2024) |

| Long-term freight cover | ~60% volume (2024) |

What is included in the product

Tailored exclusively for Hangzhou GreatStar Industrial Co., this Porter's Five Forces overview uncovers competitive drivers, buyer/supplier influence, entry barriers, substitute threats, and strategic levers shaping its industry position.

Concise Porter's Five Forces snapshot tailored for Hangzhou GreatStar—quickly spot supplier/buyer leverage, competitive rivalry, threats from new entrants/substitutes and regulatory pressure to guide strategic decisions.

Customers Bargaining Power

Concentration of Big-Box Retail Power

Low Switching Costs for DIY Consumers

Individual DIY users face low switching costs between hand-tool and basic power-tool brands, so GreatStar (Hangzhou GreatStar Industrial Co., founded 1999) must compete on price, ergonomics, and perceived value to retain buyers.

Global DIY tool market grew 3.8% in 2024 to $43.2B; with 60% of DIY purchases price-driven, many consumers pick the best immediate deal or feature set, increasing churn risk for GreatStar.

Growth of E-commerce and Direct Comparison

The rise of Amazon and marketplaces gives buyers instant price checks and peer reviews; global e-commerce GMV hit about 5.7 trillion USD in 2023 and marketplaces accounted for ~52% of that, so visibility depends on price and ratings.

GreatStar must keep competitive prices and >=4.0 ratings to appear in search algorithms and avoid Buy Box losses; a 1-star drop can cut conversion by ~16%.

Customers can switch fast to emerging brands—online private labels grew 18% YoY in 2024—so GreatStar’s reputation for quality and value is critical to retain share.

Rise of Private Label Brand Competition

Many of GreatStar’s top customers—large US and EU retailers—sell private-label tools that directly compete with GreatStar’s branded lines, capturing up to 20–30% gross margin advantage via lower price points and better shelf placement.

Retailers can prioritize house brands in promotions and displays, pressuring GreatStar’s volumes and margins; in 2024 private-label penetration in hand tools rose ~4 percentage points in key markets.

GreatStar counters through R&D on product features, and by leveraging acquisitions—Arrow (2019) and SK Professional Tools (2020)—to defend pricing and justify premium listings.

- Private-label can undercut by 20–30% on price

- Retailer promo control reduces branded shelf share

- 2024 private-label hand-tool share +4 ppt in core markets

- Acquired brands (Arrow, SK) used to defend premium positioning

Professional User Loyalty and Technical Requirements

Professional tradespeople show higher brand loyalty than DIY buyers but demand superior performance; industry surveys in 2024 report 62% of pros recommend brands based on durability and warranty terms.

These users shape market trends via preference for specialized features—torque, ergonomics, IP ratings—forcing GreatStar to spend more on R&D; GreatStar reported R&D up 18% in 2023 to ¥120 million (≈$16.5M).

Endorsement from pros drives long-term brand equity and resale channels, so losing pro support would materially hit sales in pro segments, which made ~38% of China tool market revenue in 2023.

- Pros = higher loyalty, higher expectations

- 62% of pros recommend on durability (2024)

- GreatStar R&D +18% to ¥120M in 2023

- Pro segment ≈38% of China tool revenue (2023)

Retailer power squeezes margins; R&D & M&A defend brands amid fierce marketplace pricing

| Metric | 2023–2024 |

|---|---|

| Retailer share of sales | 25–35% |

| Gross margin | ~29% (2023) |

| R&D spend | ¥120M (+18% 2023) |

| Marketplace share (GMV) | ~52% of $5.7T (2023) |

| Pro recommendation | 62% (2024) |

Preview Before You Purchase

Hangzhou GreatStar Industrial Co. Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Hangzhou GreatStar Industrial Co. you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted, professionally written, and ready for download and use the moment you buy. It contains the complete assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry tailored to GreatStar.