Green Cross Health Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

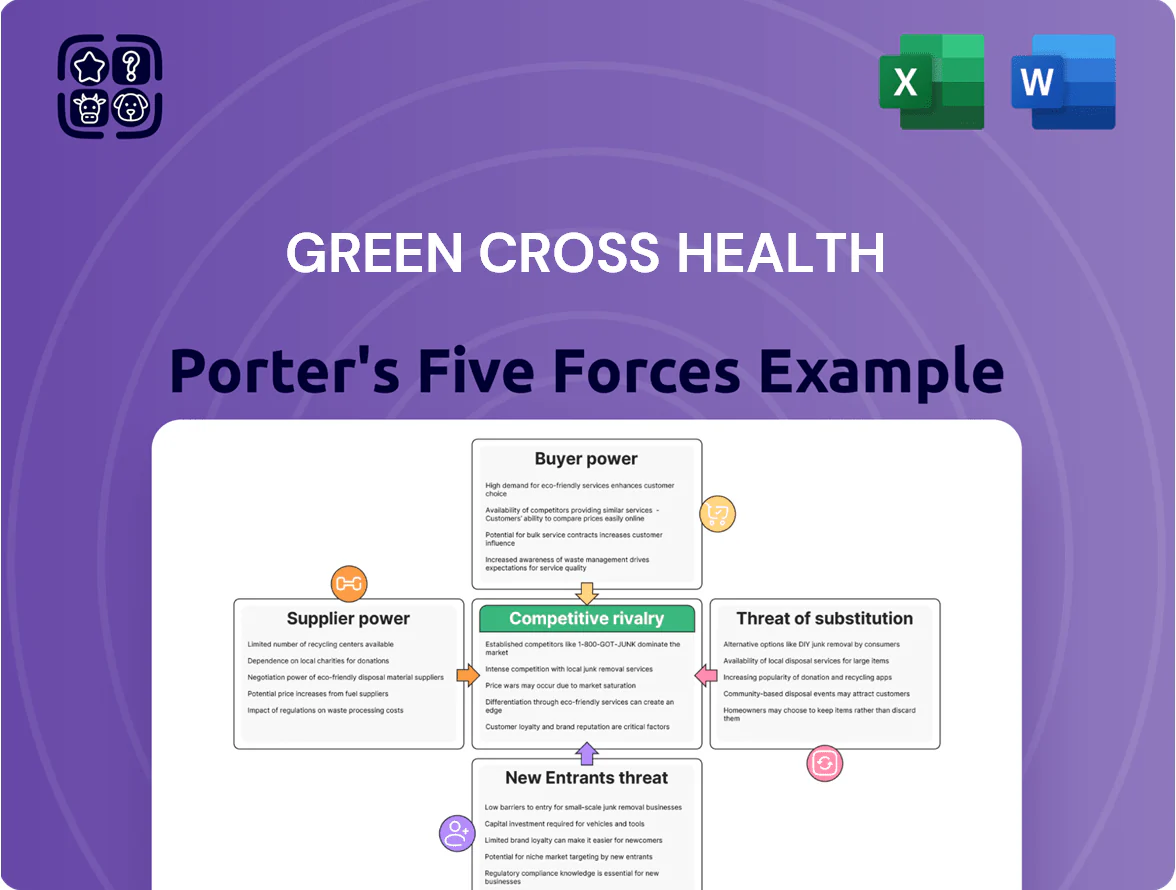

Green Cross Health faces moderate buyer power, intensifying competition from national pharmacy chains, and regulatory pressures that shape margins and growth avenues; supplier leverage and digital disruption add tactical complexity to its community-focused model.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Green Cross Health’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Pharmac Procurement Centralization

Pharmac, New Zealand’s pharmaceutical procurement agency, centralizes purchases for ~95% of subsidised medicines, cutting suppliers’ bargaining power and limiting manufacturers’ ability to price above set rates.

Because Pharmac sets subsidies and prices, Green Cross Health faces stable drug costs—retail cost inflation for subsidised drugs has averaged under 2% annually since 2019—protecting it from global price shocks.

That protection reduces margin risk but narrows brand choice in stores: a 2024 Ministry of Health review found formulary consolidation reduced listed brands by ~18%, constraining retail differentiation.

Wholesale Distribution Concentration

Green Cross Health depends on a few large wholesalers—notably EBOS Group (NZX:EBOS), which held ~28% market share in Australasian healthcare distribution in 2024—giving suppliers leverage over delivery timing and service fees for Unichem and Life Pharmacy.

In 2024 EBOS reported NZD 4.8bn revenue and 4.6% EBIT margin, so a 5% price rise or a 3‑day logistics delay could cut pharmacy margins by ~0.5–1.2 percentage points and disrupt inventory turnover.

Qualified Workforce Scarcity

The supply of registered pharmacists and specialized nurses in New Zealand remained tight in late 2025, with pharmacist vacancy rates near 6% and nursing shortages adding ~4% to locum costs, giving staff strong bargaining power.

Rising wage expectations—pharmacist median pay up ~8% year-on-year to NZD 95,000 in 2025—and richer benefits push Green Cross Health’s operating expenses higher.

Green Cross Health needs ongoing investment in recruitment, retention, and training; failing that, clinic staffing gaps risk regulatory non-compliance and lost revenue.

Specialized Technology Providers

Specialized vendors for clinical management software and secure patient-data platforms give Green Cross Health rising supplier power because switching costs and workflow disruption are high; 2024 NZ Health IT surveys show 62% of GP practices cite integration cost as main barrier to change.

As primary care shifts to integrated digital records, these suppliers command premiums—cybersecurity and interoperability add 8–15% to vendor fees per contract, per 2023 NZ procurement reports.

- Dependence: core clinical software

- High switching cost: 62% practices

- Premiums: +8–15% for security/interop

- Risk: vendor lock-in, pricing leverage

Global Product Diversification

Suppliers of premium beauty and wellness brands exert moderate power over Life Pharmacy due to exclusivity; a major brand exit or shift to direct-to-consumer could cut store footfall by an estimated 3–7% based on NZ retail cosmetics trends in 2024.

Green Cross Health limits supplier power via a diversified supplier mix across 150+ Life Pharmacy stores and group procurement, so no single brand can set network-wide terms.

- Moderate supplier power: exclusivity drives leverage

- Risk: 3–7% potential footfall loss if major brand exits

- Mitigation: 150+ stores, broad supplier portfolio, group buying

Pharmac caps drug pricing; EBOS & IT vendors retain delivery, wage and lock‑in leverage

Pharmac’s central purchasing (~95% subsidised drugs) caps suppliers’ pricing power, keeping subsidised drug inflation <2% pa since 2019 and protecting margins; EBOS (28% Australasian distribution share, NZD 4.8bn revenue in 2024) and clinical IT vendors (62% practices cite high switch cost) still wield delivery, wage (pharmacist median NZD 95,000 in 2025) and lock‑in leverage.

| Metric | Value |

|---|---|

| Pharmac coverage | ~95% |

| Subsidised drug inflation | <2% pa (since 2019) |

| EBOS 2024 revenue | NZD 4.8bn (28% share) |

| Pharmacist median pay 2025 | NZD 95,000 |

| High switch-cost IT practices | 62% |

What is included in the product

Tailored Porter's Five Forces for Green Cross Health, uncovering key competitive drivers, buyer and supplier power, substitute threats, and entry barriers to assess pricing influence, profitability risks, and strategic defenses.

One-sheet Porter's Five Forces for Green Cross Health—quickly spot competitive threats and relief strategies to guide pharmacy and primary-care decisions.

Customers Bargaining Power

Government Funding Dominance

The primary customer for Green Cross Health is the New Zealand government via Te Whatu Ora, which funded about NZD 2.2 billion in primary care subsidies in FY2024, creating a monopsony-like market where the state sets GP and dispensing reimbursement rates.

That pricing power limits Green Cross Health’s ability to raise fees; its medical and community health revenue—around NZD 300m in FY2024—is highly sensitive to public health policy and budget shifts.

Retail Consumer Price Sensitivity

In retail pharmacy, customer bargaining power is high: 72% of New Zealand shoppers compare pharmacy prices online in 2024, pressuring margins on vitamins, skincare and OTCs.

Easy price comparison and online alternatives force Green Cross Health to use Living Rewards and targeted discounts to retain customers and sustain premium pricing on 15–20% of SKU lines.

Increased Patient Mobility

Urban patients can choose among 4,000+ clinics and 3,200+ community pharmacies in New Zealand, so Green Cross Health faces high switching risk if wait times or service fall; a 2024 survey found 42% of urban patients would change providers after one poor visit. Digital booking and e-prescription platforms grew 28% in 2023, making cross-network switching easier, so Green Cross must prioritize faster access, seamless digital booking, and prescription continuity to retain volumes and revenue.

Growth of Private Health Insurance

As private health insurance uptake in New Zealand rose to about 34% of the population by 2024, insurers gained leverage to steer members toward contracted providers, pressuring prices for specialist and rehab services.

Insurers negotiate bulk rates and preferred-provider deals that can compress Green Cross Health margins; aligning services and reporting to insurer requirements is key to capture higher-paying insured patients.

- ~34% insured (2024)

- Insurer-negotiated bulk rates reduce margins

- Preferred-provider status drives patient volumes

- Align offerings/reporting to win high-value patients

Digital Literacy and Self-Care

Consumers increasingly self-diagnose and buy health products online, with 78% of NZ adults using digital health info in 2024, shifting purchase power from pharmacists to shoppers.

Customers now request specific brands and OTC remedies after online research, reducing reliance on pharmacist advice and pressuring margins.

Green Cross Health must adopt consultative, personalized services—telehealth, targeted advice, loyalty data—to add value beyond transactions.

- 78% NZ adults used digital health info (2024)

- Higher SKU-request rate lowers add-on sales

- Telehealth + loyalty raises retention

Pricing pressure and digital shift force Green Cross Health into loyalty, telehealth, insurer ties

Customers (mainly Te Whatu Ora) have strong pricing power—NZD 2.2bn primary care subsidies in FY2024—limiting fee growth; retail shoppers and insurers (34% insured in 2024) further compress margins via price comparison and preferred-provider deals; digital self-diagnosis (78% of adults in 2024) shifts purchase power online, raising switching risk and forcing Green Cross Health toward loyalty, telehealth, and insurer-aligned reporting to protect volumes.

| Metric | 2024 value |

|---|---|

| Government primary care subsidies | NZD 2.2bn |

| Green Cross medical/community revenue | ~NZD 300m |

| Private insurance uptake | 34% |

| Adults using digital health info | 78% |

| Urban patient switching after one poor visit | 42% |

Same Document Delivered

Green Cross Health Porter's Five Forces Analysis

This preview shows the exact Green Cross Health Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders, fully formatted and ready for use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Green Cross Health faces moderate buyer power, intensifying competition from national pharmacy chains, and regulatory pressures that shape margins and growth avenues; supplier leverage and digital disruption add tactical complexity to its community-focused model.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Green Cross Health’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Pharmac Procurement Centralization

Pharmac, New Zealand’s pharmaceutical procurement agency, centralizes purchases for ~95% of subsidised medicines, cutting suppliers’ bargaining power and limiting manufacturers’ ability to price above set rates.

Because Pharmac sets subsidies and prices, Green Cross Health faces stable drug costs—retail cost inflation for subsidised drugs has averaged under 2% annually since 2019—protecting it from global price shocks.

That protection reduces margin risk but narrows brand choice in stores: a 2024 Ministry of Health review found formulary consolidation reduced listed brands by ~18%, constraining retail differentiation.

Wholesale Distribution Concentration

Green Cross Health depends on a few large wholesalers—notably EBOS Group (NZX:EBOS), which held ~28% market share in Australasian healthcare distribution in 2024—giving suppliers leverage over delivery timing and service fees for Unichem and Life Pharmacy.

In 2024 EBOS reported NZD 4.8bn revenue and 4.6% EBIT margin, so a 5% price rise or a 3‑day logistics delay could cut pharmacy margins by ~0.5–1.2 percentage points and disrupt inventory turnover.

Qualified Workforce Scarcity

The supply of registered pharmacists and specialized nurses in New Zealand remained tight in late 2025, with pharmacist vacancy rates near 6% and nursing shortages adding ~4% to locum costs, giving staff strong bargaining power.

Rising wage expectations—pharmacist median pay up ~8% year-on-year to NZD 95,000 in 2025—and richer benefits push Green Cross Health’s operating expenses higher.

Green Cross Health needs ongoing investment in recruitment, retention, and training; failing that, clinic staffing gaps risk regulatory non-compliance and lost revenue.

Specialized Technology Providers

Specialized vendors for clinical management software and secure patient-data platforms give Green Cross Health rising supplier power because switching costs and workflow disruption are high; 2024 NZ Health IT surveys show 62% of GP practices cite integration cost as main barrier to change.

As primary care shifts to integrated digital records, these suppliers command premiums—cybersecurity and interoperability add 8–15% to vendor fees per contract, per 2023 NZ procurement reports.

- Dependence: core clinical software

- High switching cost: 62% practices

- Premiums: +8–15% for security/interop

- Risk: vendor lock-in, pricing leverage

Global Product Diversification

Suppliers of premium beauty and wellness brands exert moderate power over Life Pharmacy due to exclusivity; a major brand exit or shift to direct-to-consumer could cut store footfall by an estimated 3–7% based on NZ retail cosmetics trends in 2024.

Green Cross Health limits supplier power via a diversified supplier mix across 150+ Life Pharmacy stores and group procurement, so no single brand can set network-wide terms.

- Moderate supplier power: exclusivity drives leverage

- Risk: 3–7% potential footfall loss if major brand exits

- Mitigation: 150+ stores, broad supplier portfolio, group buying

Pharmac caps drug pricing; EBOS & IT vendors retain delivery, wage and lock‑in leverage

Pharmac’s central purchasing (~95% subsidised drugs) caps suppliers’ pricing power, keeping subsidised drug inflation <2% pa since 2019 and protecting margins; EBOS (28% Australasian distribution share, NZD 4.8bn revenue in 2024) and clinical IT vendors (62% practices cite high switch cost) still wield delivery, wage (pharmacist median NZD 95,000 in 2025) and lock‑in leverage.

| Metric | Value |

|---|---|

| Pharmac coverage | ~95% |

| Subsidised drug inflation | <2% pa (since 2019) |

| EBOS 2024 revenue | NZD 4.8bn (28% share) |

| Pharmacist median pay 2025 | NZD 95,000 |

| High switch-cost IT practices | 62% |

What is included in the product

Tailored Porter's Five Forces for Green Cross Health, uncovering key competitive drivers, buyer and supplier power, substitute threats, and entry barriers to assess pricing influence, profitability risks, and strategic defenses.

One-sheet Porter's Five Forces for Green Cross Health—quickly spot competitive threats and relief strategies to guide pharmacy and primary-care decisions.

Customers Bargaining Power

Government Funding Dominance

The primary customer for Green Cross Health is the New Zealand government via Te Whatu Ora, which funded about NZD 2.2 billion in primary care subsidies in FY2024, creating a monopsony-like market where the state sets GP and dispensing reimbursement rates.

That pricing power limits Green Cross Health’s ability to raise fees; its medical and community health revenue—around NZD 300m in FY2024—is highly sensitive to public health policy and budget shifts.

Retail Consumer Price Sensitivity

In retail pharmacy, customer bargaining power is high: 72% of New Zealand shoppers compare pharmacy prices online in 2024, pressuring margins on vitamins, skincare and OTCs.

Easy price comparison and online alternatives force Green Cross Health to use Living Rewards and targeted discounts to retain customers and sustain premium pricing on 15–20% of SKU lines.

Increased Patient Mobility

Urban patients can choose among 4,000+ clinics and 3,200+ community pharmacies in New Zealand, so Green Cross Health faces high switching risk if wait times or service fall; a 2024 survey found 42% of urban patients would change providers after one poor visit. Digital booking and e-prescription platforms grew 28% in 2023, making cross-network switching easier, so Green Cross must prioritize faster access, seamless digital booking, and prescription continuity to retain volumes and revenue.

Growth of Private Health Insurance

As private health insurance uptake in New Zealand rose to about 34% of the population by 2024, insurers gained leverage to steer members toward contracted providers, pressuring prices for specialist and rehab services.

Insurers negotiate bulk rates and preferred-provider deals that can compress Green Cross Health margins; aligning services and reporting to insurer requirements is key to capture higher-paying insured patients.

- ~34% insured (2024)

- Insurer-negotiated bulk rates reduce margins

- Preferred-provider status drives patient volumes

- Align offerings/reporting to win high-value patients

Digital Literacy and Self-Care

Consumers increasingly self-diagnose and buy health products online, with 78% of NZ adults using digital health info in 2024, shifting purchase power from pharmacists to shoppers.

Customers now request specific brands and OTC remedies after online research, reducing reliance on pharmacist advice and pressuring margins.

Green Cross Health must adopt consultative, personalized services—telehealth, targeted advice, loyalty data—to add value beyond transactions.

- 78% NZ adults used digital health info (2024)

- Higher SKU-request rate lowers add-on sales

- Telehealth + loyalty raises retention

Pricing pressure and digital shift force Green Cross Health into loyalty, telehealth, insurer ties

Customers (mainly Te Whatu Ora) have strong pricing power—NZD 2.2bn primary care subsidies in FY2024—limiting fee growth; retail shoppers and insurers (34% insured in 2024) further compress margins via price comparison and preferred-provider deals; digital self-diagnosis (78% of adults in 2024) shifts purchase power online, raising switching risk and forcing Green Cross Health toward loyalty, telehealth, and insurer-aligned reporting to protect volumes.

| Metric | 2024 value |

|---|---|

| Government primary care subsidies | NZD 2.2bn |

| Green Cross medical/community revenue | ~NZD 300m |

| Private insurance uptake | 34% |

| Adults using digital health info | 78% |

| Urban patient switching after one poor visit | 42% |

Same Document Delivered

Green Cross Health Porter's Five Forces Analysis

This preview shows the exact Green Cross Health Porter’s Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders, fully formatted and ready for use.