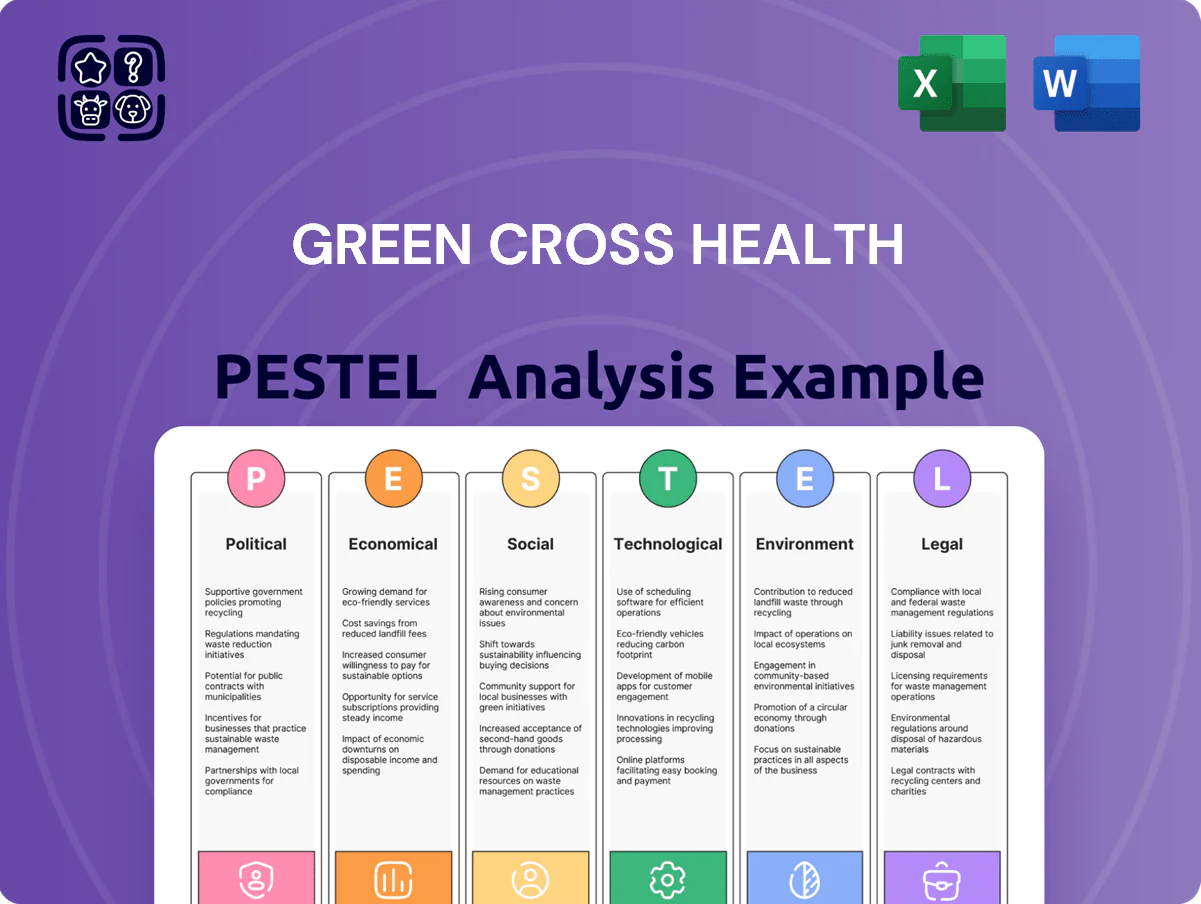

Green Cross Health PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how regulatory shifts, technology adoption, and changing consumer health trends are reshaping Green Cross Health’s strategic outlook—our concise PESTLE highlights risks and opportunities you need now. Purchase the full PESTLE to access the comprehensive, actionable analysis investors and strategists rely on and download immediately for use in forecasts, pitches, or boardroom decisions.

Political factors

Government Health Funding Policies

The New Zealand government’s health budget of NZD 22.0 billion for 2024/25 directly affects Green Cross Health’s pharmacy subsidies and primary care funding, with pharmacy funding representing ~18% of its FY2024 revenue mix; shifts to Te Whatu Ora’s funding model could compress margins at community medical centers where Green Cross operates. Investors should watch fiscal policy moves—any reallocation toward hospital-centric spending risks reducing community-based care reimbursements and lowering operating EBITDA by an estimated 3–6%.

Public Health Sector Reforms

The 2023–25 NZ health sector consolidation, including the 2022 creation of Te Whatu Ora and Te Aka Whai Ora, centralizes procurement, altering how Green Cross Health (revenue NZD 863m FY2024) negotiates contracts for home health and disability support services.

Centralized decision-making compresses regional autonomy, increasing competition for fixed national budgets—Home and Community Support Services funding was NZD 1.2b in 2024—so contract terms are more standardized.

Strategic alignment with national priorities, such as the 2024 emphasis on integrated community care and reducing acute admissions, is critical for Green Cross to secure multi-year service agreements and revenue stability.

Pharmacy Ownership Regulations

Political debates on pharmacy ownership deregulation in New Zealand risk opening markets to large international retailers, threatening Green Cross Health’s Unichem and Life Pharmacy networks which currently benefit from pharmacist-led ownership protections covering roughly 950 pharmacies nationwide.

International Trade Agreements

Trade policies affecting importation of active pharmaceutical ingredients and retail goods directly impact Green Cross Health’s supply-chain stability; in 2024 NZ imported NZD 6.8b of pharmaceuticals, exposing margins to border policy shifts.

Tariffs or non-tariff barriers can raise costs for OTC and medical supplies— a 5% tariff on imports could increase product costs materially versus FY2024 gross margins of ~27%.

Monitoring New Zealand’s trade relations, especially with Australia, China and ASEAN (top partners), is vital to forecast procurement costs and preserve retail margins amid 2024–25 volatility.

- NZ pharmaceutical imports NZD 6.8b (2024)

- FY2024 Green Cross Health gross margin ~27%

- Top trade partners: Australia, China, ASEAN — watch tariff/NTB changes

- Estimated 5% tariff could notably compress retail margins

Immigration Policies for Healthcare Workers

Government settings on work visas and residency pathways for pharmacists, nurses, and doctors directly affect Green Cross Health’s ability to address labor shortages; in New Zealand, health sector skilled visa approvals fell 12% in 2024, intensifying recruitment pressure.

Restrictive immigration policies can drive wage inflation—healthcare median wage growth hit 6.8% in 2024—and create operational bottlenecks across medical centers and community pharmacies.

Green Cross Health depends on favorable political stances toward skilled migration to sustain its professional workforce and limit agency staffing costs that erode margins.

- 2024 NZ health skilled visa approvals down 12%

- Healthcare wage growth 6.8% in 2024

- Higher agency staffing increases operating costs and margins pressure

NZ health budget squeeze: Green Cross margins hit by subsidies, wages and visa cuts

Political factors: NZ health budget NZD 22.0b (2024/25) affects pharmacy subsidies; FY2024 Green Cross revenue NZD 863m with ~18% from pharmacy. Centralized Te Whatu Ora procurement and sector consolidation standardize contracts; HCSS funding NZD 1.2b (2024). Skilled visa approvals -12% (2024) and healthcare wage growth 6.8% raise staffing costs and margin pressure.

| Metric | 2024 value |

|---|---|

| NZ health budget | NZD 22.0b |

| Green Cross revenue | NZD 863m |

| Pharmacy share | ~18% |

| Pharma imports | NZD 6.8b |

| Skilled visa approvals | -12% |

What is included in the product

Explores how macro-environmental factors uniquely affect Green Cross Health across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific examples to identify threats and opportunities for executives and investors.

Condenses Green Cross Health's PESTLE into a clear, shareable summary that highlights external risks and opportunities for rapid alignment in strategy sessions or investor updates.

Economic factors

Interest Rate Environment

As of late 2025, New Zealand OCR at 5.5% keeps borrowing costs elevated, raising debt servicing for Green Cross Health’s capital projects—each 100m NZD debt carries ~5.5m NZD annual interest vs ~3m at a 3% OCR. High rates constrain expansion and M&A, particularly for medical center upgrades. A stabilizing OCR would lower financing costs, enabling larger investments across pharmacy and community health portfolios.

Consumer Spending and Inflation

Persistent inflation—New Zealand CPI rose 6.7% y/y in 2023 and 4.7% y/y in Dec 2024—tightens household budgets, reducing spend in Life Pharmacy and Unichem retail categories; prescription volumes remain price-inelastic but high-end beauty and wellness sales are down versus pre-inflation levels. Green Cross Health must calibrate pricing and promotions to protect retail volumes while preserving margins, noting pharmacy gross margins averaged ~28% in FY2024.

Labor Market Costs

Wage growth in New Zealand's healthcare sector reached about 4.5% in 2024, driven by inflation and collective bargaining, significantly increasing operating expenses for providers like Green Cross Health.

To retain specialized clinicians and pharmacists, Green Cross Health must offer market-competitive salaries; pharmacist median pay rose ~6% to NZD 85,000 in 2024, pressuring payroll budgets.

Managing the labor cost-to-revenue ratio—which averaged ~48% across community healthcare in 2024—is a primary focus to protect Green Cross Health’s profitability.

Currency Exchange Rate Fluctuations

The NZD fell about 6% vs USD in 2024, raising landed costs for imported retail products and medical equipment for Green Cross Health and risking margin compression if rises cannot be passed to consumers.

Management reported hedging coverage of roughly 60% of 2024 FX exposure; without hedges a 5% NZD depreciation could cut gross margin by ~0.8–1.2ppt on import-heavy lines.

- NZD -6% vs USD in 2024

- ~60% hedging coverage reported

- 5% NZD depreciation ≈ 0.8–1.2ppt margin hit

Real Estate and Lease Costs

With over 200 pharmacies and medical centres, Green Cross Health is sensitive to NZ commercial property trends; national retail vacancy rose to 6.5% in 2024, putting upward pressure on prime precinct rents.

Lease renewals in high-footfall suburban and CBD sites can raise fixed overheads materially—rent-to-revenue ratios exceeding 8% can erode margins in pharmacy retail.

Strategic site selection, portfolio-wide lease renegotiation and use of sale-and-leaseback or turnover-based rent models are key to cost control and division sustainability.

- Network scale: ~200 locations (2025)

- Retail vacancy: 6.5% (2024)

- Target rent/revenue sensitivity: >8% risks margin pressure

- Mitigants: lease renegotiation, turnover rents, sale-and-leaseback

Higher OCR, slower CPI, wage pressure and FX drag squeeze pharmacist margins

Elevated OCR (5.5% late-2025) raises funding costs; NZ CPI slowed from 6.7% (2023) to 4.7% (Dec 2024) compresses discretionary retail spend; wage inflation (~4.5% sector, pharmacist median NZD85,000 in 2024) boosts payroll; NZD -6% vs USD (2024) increases imported costs—~60% hedged.

| Metric | Value |

|---|---|

| OCR | 5.5% |

| CPI (Dec 2024) | 4.7% |

| Pharmacist pay (median) | NZD85,000 |

| NZD vs USD (2024) | -6% |

| Hedge cover | ~60% |

Same Document Delivered

Green Cross Health PESTLE Analysis

The preview shown here is the exact Green Cross Health PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic analysis and decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how regulatory shifts, technology adoption, and changing consumer health trends are reshaping Green Cross Health’s strategic outlook—our concise PESTLE highlights risks and opportunities you need now. Purchase the full PESTLE to access the comprehensive, actionable analysis investors and strategists rely on and download immediately for use in forecasts, pitches, or boardroom decisions.

Political factors

Government Health Funding Policies

The New Zealand government’s health budget of NZD 22.0 billion for 2024/25 directly affects Green Cross Health’s pharmacy subsidies and primary care funding, with pharmacy funding representing ~18% of its FY2024 revenue mix; shifts to Te Whatu Ora’s funding model could compress margins at community medical centers where Green Cross operates. Investors should watch fiscal policy moves—any reallocation toward hospital-centric spending risks reducing community-based care reimbursements and lowering operating EBITDA by an estimated 3–6%.

Public Health Sector Reforms

The 2023–25 NZ health sector consolidation, including the 2022 creation of Te Whatu Ora and Te Aka Whai Ora, centralizes procurement, altering how Green Cross Health (revenue NZD 863m FY2024) negotiates contracts for home health and disability support services.

Centralized decision-making compresses regional autonomy, increasing competition for fixed national budgets—Home and Community Support Services funding was NZD 1.2b in 2024—so contract terms are more standardized.

Strategic alignment with national priorities, such as the 2024 emphasis on integrated community care and reducing acute admissions, is critical for Green Cross to secure multi-year service agreements and revenue stability.

Pharmacy Ownership Regulations

Political debates on pharmacy ownership deregulation in New Zealand risk opening markets to large international retailers, threatening Green Cross Health’s Unichem and Life Pharmacy networks which currently benefit from pharmacist-led ownership protections covering roughly 950 pharmacies nationwide.

International Trade Agreements

Trade policies affecting importation of active pharmaceutical ingredients and retail goods directly impact Green Cross Health’s supply-chain stability; in 2024 NZ imported NZD 6.8b of pharmaceuticals, exposing margins to border policy shifts.

Tariffs or non-tariff barriers can raise costs for OTC and medical supplies— a 5% tariff on imports could increase product costs materially versus FY2024 gross margins of ~27%.

Monitoring New Zealand’s trade relations, especially with Australia, China and ASEAN (top partners), is vital to forecast procurement costs and preserve retail margins amid 2024–25 volatility.

- NZ pharmaceutical imports NZD 6.8b (2024)

- FY2024 Green Cross Health gross margin ~27%

- Top trade partners: Australia, China, ASEAN — watch tariff/NTB changes

- Estimated 5% tariff could notably compress retail margins

Immigration Policies for Healthcare Workers

Government settings on work visas and residency pathways for pharmacists, nurses, and doctors directly affect Green Cross Health’s ability to address labor shortages; in New Zealand, health sector skilled visa approvals fell 12% in 2024, intensifying recruitment pressure.

Restrictive immigration policies can drive wage inflation—healthcare median wage growth hit 6.8% in 2024—and create operational bottlenecks across medical centers and community pharmacies.

Green Cross Health depends on favorable political stances toward skilled migration to sustain its professional workforce and limit agency staffing costs that erode margins.

- 2024 NZ health skilled visa approvals down 12%

- Healthcare wage growth 6.8% in 2024

- Higher agency staffing increases operating costs and margins pressure

NZ health budget squeeze: Green Cross margins hit by subsidies, wages and visa cuts

Political factors: NZ health budget NZD 22.0b (2024/25) affects pharmacy subsidies; FY2024 Green Cross revenue NZD 863m with ~18% from pharmacy. Centralized Te Whatu Ora procurement and sector consolidation standardize contracts; HCSS funding NZD 1.2b (2024). Skilled visa approvals -12% (2024) and healthcare wage growth 6.8% raise staffing costs and margin pressure.

| Metric | 2024 value |

|---|---|

| NZ health budget | NZD 22.0b |

| Green Cross revenue | NZD 863m |

| Pharmacy share | ~18% |

| Pharma imports | NZD 6.8b |

| Skilled visa approvals | -12% |

What is included in the product

Explores how macro-environmental factors uniquely affect Green Cross Health across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific examples to identify threats and opportunities for executives and investors.

Condenses Green Cross Health's PESTLE into a clear, shareable summary that highlights external risks and opportunities for rapid alignment in strategy sessions or investor updates.

Economic factors

Interest Rate Environment

As of late 2025, New Zealand OCR at 5.5% keeps borrowing costs elevated, raising debt servicing for Green Cross Health’s capital projects—each 100m NZD debt carries ~5.5m NZD annual interest vs ~3m at a 3% OCR. High rates constrain expansion and M&A, particularly for medical center upgrades. A stabilizing OCR would lower financing costs, enabling larger investments across pharmacy and community health portfolios.

Consumer Spending and Inflation

Persistent inflation—New Zealand CPI rose 6.7% y/y in 2023 and 4.7% y/y in Dec 2024—tightens household budgets, reducing spend in Life Pharmacy and Unichem retail categories; prescription volumes remain price-inelastic but high-end beauty and wellness sales are down versus pre-inflation levels. Green Cross Health must calibrate pricing and promotions to protect retail volumes while preserving margins, noting pharmacy gross margins averaged ~28% in FY2024.

Labor Market Costs

Wage growth in New Zealand's healthcare sector reached about 4.5% in 2024, driven by inflation and collective bargaining, significantly increasing operating expenses for providers like Green Cross Health.

To retain specialized clinicians and pharmacists, Green Cross Health must offer market-competitive salaries; pharmacist median pay rose ~6% to NZD 85,000 in 2024, pressuring payroll budgets.

Managing the labor cost-to-revenue ratio—which averaged ~48% across community healthcare in 2024—is a primary focus to protect Green Cross Health’s profitability.

Currency Exchange Rate Fluctuations

The NZD fell about 6% vs USD in 2024, raising landed costs for imported retail products and medical equipment for Green Cross Health and risking margin compression if rises cannot be passed to consumers.

Management reported hedging coverage of roughly 60% of 2024 FX exposure; without hedges a 5% NZD depreciation could cut gross margin by ~0.8–1.2ppt on import-heavy lines.

- NZD -6% vs USD in 2024

- ~60% hedging coverage reported

- 5% NZD depreciation ≈ 0.8–1.2ppt margin hit

Real Estate and Lease Costs

With over 200 pharmacies and medical centres, Green Cross Health is sensitive to NZ commercial property trends; national retail vacancy rose to 6.5% in 2024, putting upward pressure on prime precinct rents.

Lease renewals in high-footfall suburban and CBD sites can raise fixed overheads materially—rent-to-revenue ratios exceeding 8% can erode margins in pharmacy retail.

Strategic site selection, portfolio-wide lease renegotiation and use of sale-and-leaseback or turnover-based rent models are key to cost control and division sustainability.

- Network scale: ~200 locations (2025)

- Retail vacancy: 6.5% (2024)

- Target rent/revenue sensitivity: >8% risks margin pressure

- Mitigants: lease renegotiation, turnover rents, sale-and-leaseback

Higher OCR, slower CPI, wage pressure and FX drag squeeze pharmacist margins

Elevated OCR (5.5% late-2025) raises funding costs; NZ CPI slowed from 6.7% (2023) to 4.7% (Dec 2024) compresses discretionary retail spend; wage inflation (~4.5% sector, pharmacist median NZD85,000 in 2024) boosts payroll; NZD -6% vs USD (2024) increases imported costs—~60% hedged.

| Metric | Value |

|---|---|

| OCR | 5.5% |

| CPI (Dec 2024) | 4.7% |

| Pharmacist pay (median) | NZD85,000 |

| NZD vs USD (2024) | -6% |

| Hedge cover | ~60% |

Same Document Delivered

Green Cross Health PESTLE Analysis

The preview shown here is the exact Green Cross Health PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic analysis and decision-making.