Green Cross Health SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Green Cross Health sits at the intersection of trusted pharmacy services and expanding primary care, with resilient retail networks and strong community trust—but faces margin pressure, regulatory complexity, and digital disruption risks. Discover the full SWOT analysis for granular financial context, strategic implications, and an editable Word + Excel package to support investment, planning, or pitch-ready recommendations.

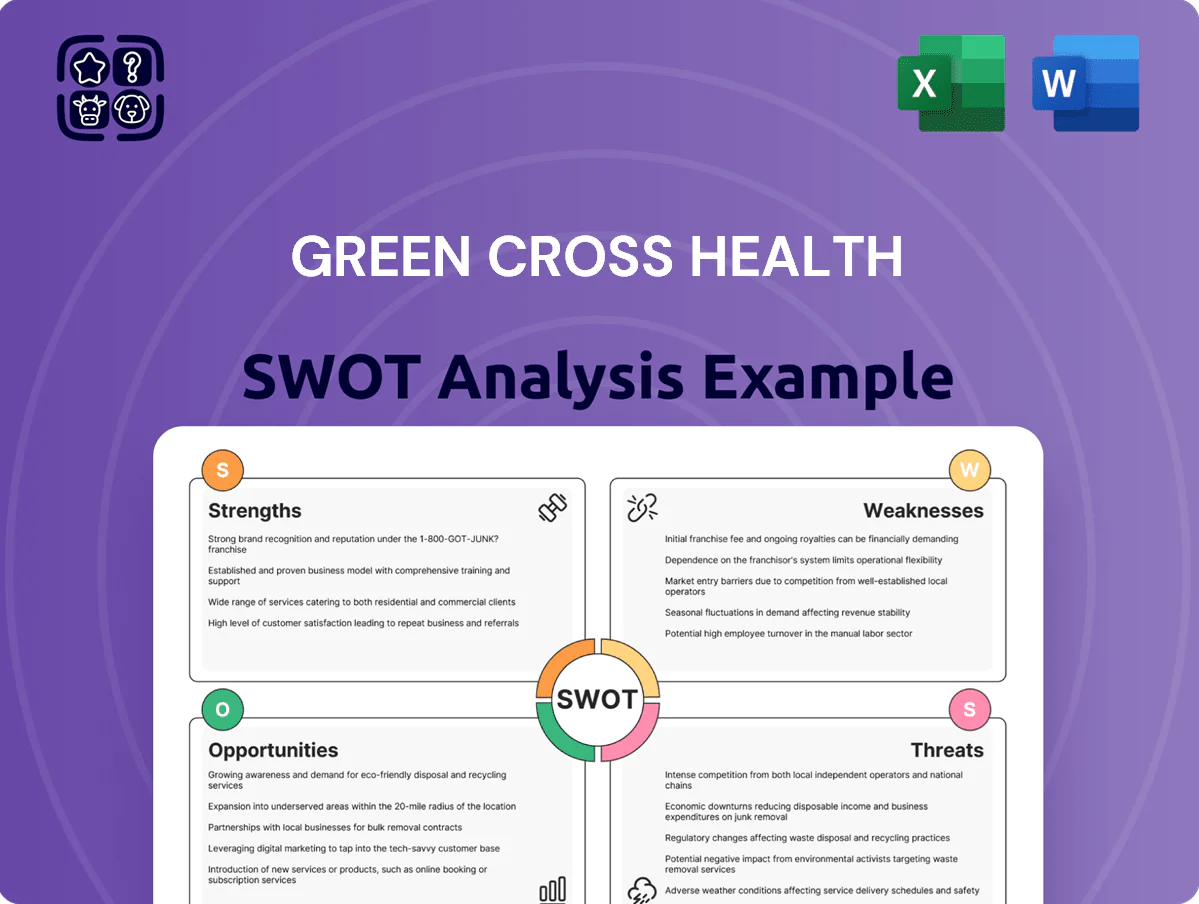

Strengths

Dominant Market Leadership in Pharmacy

Green Cross Health operates New Zealand’s largest pharmacy network via Unichem and Life Pharmacy, totaling about 400 sites as of Dec 2025; that scale drove NZD 1.1bn retail prescription sales in FY2024. The wide physical footprint yields procurement and distribution economies — supplier rebates and lower per‑unit logistics costs — that smaller independents cannot match. This network scale sustained a strong barrier to entry through 2025, protecting gross margins and same‑store sales.

Integrated Healthcare Service Model

Green Cross Health operates an integrated model across pharmacies, GP clinics and community services, covering about 900 sites and serving ~1.2 million patients in 2025, which supports coordinated care and better outcomes.

This vertical integration creates multiple touchpoints in the patient journey, lifting cross-referral rates—GP-to-pharmacy referrals rose 18% in FY2024—and boosting same-patient revenue per year by an estimated NZD 65 per patient.

Leveraging synergy reduced duplicate admin and inventory costs, improving group EBITDA margin to 11.8% in H1 2025 and shortening referral-to-treatment time by 22%.

Strong Brand Equity and Trust

The Unichem and Life Pharmacy brands are household names in New Zealand, known for professional health advice and reliability, driving a 2024/25 like-for-like sales uplift of 6.8% in retail pharmacy; this trust boosts patient choice in healthcare where reputation matters most. Green Cross Health has leveraged brand equity to grow private-pay health and wellness revenue to NZD 112.4m in FY2025, a 14% year-on-year rise, anchoring margin expansion and higher customer retention.

Geographic Diversification Across New Zealand

- 230+ pharmacies, 180 medical centres (FY2024)

- NZD 795m revenue (FY2024)

- Nationwide coverage reduces regional revenue volatility

- High-traffic retail/medical locations boost patient retention

Robust Data and Digital Infrastructure

- 6M+ consumer profiles (Living Rewards, 2025)

- Repeat sales +8.2% (FY2024)

- Prescription adherence +4 ppt

- Supports targeted marketing and CLV growth

Green Cross Health: NZ’s integrated care leader—~400 pharmacies, NZD795m rev, 11.8% EBITDA

Green Cross Health (GCX:NZX) combines NZ’s largest pharmacy network (~400 sites Dec 2025) and ~900 clinics/services, producing NZD 795m revenue (FY2024) and NZD 112.4m private-pay sales (FY2025); integrated care lifted EBITDA margin to 11.8% (H1 2025), GP-to-pharmacy referrals +18% (FY2024) and Living Rewards profiles >6M, raising repeat sales +8.2% (FY2024).

| Metric | Value |

|---|---|

| Sites (Dec 2025) | ~400 pharmacies; ~900 total |

| Revenue | NZD 795m (FY2024) |

| Private-pay | NZD 112.4m (FY2025) |

| EBITDA margin | 11.8% (H1 2025) |

| Living Rewards | >6M profiles (2025) |

What is included in the product

Provides a concise SWOT overview of Green Cross Health, highlighting its operational strengths, internal weaknesses, external growth opportunities, and market threats to inform strategic decisions.

Delivers a concise Green Cross Health SWOT matrix for rapid strategic alignment and decision-making across teams.

Weaknesses

Heavy Dependence on Government Funding

A substantial share of Green Cross Health’s FY2025 revenue—about NZD 720m or roughly 65%—comes from government-funded contracts and prescription subsidies, leaving earnings highly exposed to public-health policy shifts.

If Health New Zealand changes the Integrated Community Pharmacy Services Agreement or GP funding models, earnings before tax could swing by an estimated NZD 20–40m annually, squeezing margins and cash flow.

Thin Profit Margins in Retail Pharmacy

The retail pharmacy arm faces fierce competition and rising costs, squeezing margins: NZ pharmacies' gross margin for front-of-shop goods averaged ~22% in 2024 while net profit margins for listed NZ pharmacy chains ran ~3–5% in FY2024. Dispensing volumes remain high but regulated subsidies limit profit per script; in 2025 Green Cross needs strict cost control and >8 inventory turns/year to sustain retail profitability.

Shortage of Qualified Healthcare Professionals

Like much of global healthcare, Green Cross Health faces ongoing shortages of pharmacists and GPs; New Zealand reported a 2024 shortfall of about 1,200 primary care clinicians, tightening local hiring pools and raising turnover.

Higher labor costs—wage growth for nurses and pharmacists rose ~6% in 2023–24—push operating expenses and trimmed FY2024 operating margin by roughly 0.8 percentage points.

Staff limits cap clinic capacity: workforce bottlenecks restrict extended hours and slow new clinic openings, risking lost revenue from unmet demand.

Geographic Concentration Risk

Despite national dominance, Green Cross Health operates solely in New Zealand, exposing it to local downturns and policy shifts; NZ GDP fell 0.1% q/q in Q3 2025, highlighting cyclical risk.

Concentration risks magnify: 2024 revenue NZD 895m came almost entirely from domestic pharmacy, medical and related services, so a regulatory hit or recession would disproportionately affect cash flows.

- Single-market exposure: 100% NZ operations

- Revenue FY2024: NZD 895 million

- NZ GDP contraction Q3 2025: -0.1% q/q

- High policy sensitivity: local health reforms can cut margins

Integration Complexity of Acquisitions

NZ healthcare operator exposed: 65% public funding, thin margins, staffing squeeze

Heavy reliance on NZ public funding (~NZD 720m, ~65% of FY2025 revenue) makes earnings sensitive to policy changes; a contract shift could swing EBT by NZD 20–40m. Retail margins are thin (front-shop gross ~22% in 2024; listed chains net 3–5% FY2024) and require >8 inventory turns/year. Workforce shortages (≈1,200 primary care shortfall in 2024) and 12% higher admin costs plus NZD 9.8m integration spend strain margins.

| Metric | Value |

|---|---|

| Total revenue FY2024 | NZD 895m |

| Public-funding share FY2025 | NZD 720m (≈65%) |

| Potential EBT swing | NZD 20–40m |

| Integration cost FY24 | NZD 9.8m |

| Admin cost rise 2024 | 12% |

| Primary care shortfall 2024 | ≈1,200 clinicians |

Preview the Actual Deliverable

Green Cross Health SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

Green Cross Health sits at the intersection of trusted pharmacy services and expanding primary care, with resilient retail networks and strong community trust—but faces margin pressure, regulatory complexity, and digital disruption risks. Discover the full SWOT analysis for granular financial context, strategic implications, and an editable Word + Excel package to support investment, planning, or pitch-ready recommendations.

Strengths

Dominant Market Leadership in Pharmacy

Green Cross Health operates New Zealand’s largest pharmacy network via Unichem and Life Pharmacy, totaling about 400 sites as of Dec 2025; that scale drove NZD 1.1bn retail prescription sales in FY2024. The wide physical footprint yields procurement and distribution economies — supplier rebates and lower per‑unit logistics costs — that smaller independents cannot match. This network scale sustained a strong barrier to entry through 2025, protecting gross margins and same‑store sales.

Integrated Healthcare Service Model

Green Cross Health operates an integrated model across pharmacies, GP clinics and community services, covering about 900 sites and serving ~1.2 million patients in 2025, which supports coordinated care and better outcomes.

This vertical integration creates multiple touchpoints in the patient journey, lifting cross-referral rates—GP-to-pharmacy referrals rose 18% in FY2024—and boosting same-patient revenue per year by an estimated NZD 65 per patient.

Leveraging synergy reduced duplicate admin and inventory costs, improving group EBITDA margin to 11.8% in H1 2025 and shortening referral-to-treatment time by 22%.

Strong Brand Equity and Trust

The Unichem and Life Pharmacy brands are household names in New Zealand, known for professional health advice and reliability, driving a 2024/25 like-for-like sales uplift of 6.8% in retail pharmacy; this trust boosts patient choice in healthcare where reputation matters most. Green Cross Health has leveraged brand equity to grow private-pay health and wellness revenue to NZD 112.4m in FY2025, a 14% year-on-year rise, anchoring margin expansion and higher customer retention.

Geographic Diversification Across New Zealand

- 230+ pharmacies, 180 medical centres (FY2024)

- NZD 795m revenue (FY2024)

- Nationwide coverage reduces regional revenue volatility

- High-traffic retail/medical locations boost patient retention

Robust Data and Digital Infrastructure

- 6M+ consumer profiles (Living Rewards, 2025)

- Repeat sales +8.2% (FY2024)

- Prescription adherence +4 ppt

- Supports targeted marketing and CLV growth

Green Cross Health: NZ’s integrated care leader—~400 pharmacies, NZD795m rev, 11.8% EBITDA

Green Cross Health (GCX:NZX) combines NZ’s largest pharmacy network (~400 sites Dec 2025) and ~900 clinics/services, producing NZD 795m revenue (FY2024) and NZD 112.4m private-pay sales (FY2025); integrated care lifted EBITDA margin to 11.8% (H1 2025), GP-to-pharmacy referrals +18% (FY2024) and Living Rewards profiles >6M, raising repeat sales +8.2% (FY2024).

| Metric | Value |

|---|---|

| Sites (Dec 2025) | ~400 pharmacies; ~900 total |

| Revenue | NZD 795m (FY2024) |

| Private-pay | NZD 112.4m (FY2025) |

| EBITDA margin | 11.8% (H1 2025) |

| Living Rewards | >6M profiles (2025) |

What is included in the product

Provides a concise SWOT overview of Green Cross Health, highlighting its operational strengths, internal weaknesses, external growth opportunities, and market threats to inform strategic decisions.

Delivers a concise Green Cross Health SWOT matrix for rapid strategic alignment and decision-making across teams.

Weaknesses

Heavy Dependence on Government Funding

A substantial share of Green Cross Health’s FY2025 revenue—about NZD 720m or roughly 65%—comes from government-funded contracts and prescription subsidies, leaving earnings highly exposed to public-health policy shifts.

If Health New Zealand changes the Integrated Community Pharmacy Services Agreement or GP funding models, earnings before tax could swing by an estimated NZD 20–40m annually, squeezing margins and cash flow.

Thin Profit Margins in Retail Pharmacy

The retail pharmacy arm faces fierce competition and rising costs, squeezing margins: NZ pharmacies' gross margin for front-of-shop goods averaged ~22% in 2024 while net profit margins for listed NZ pharmacy chains ran ~3–5% in FY2024. Dispensing volumes remain high but regulated subsidies limit profit per script; in 2025 Green Cross needs strict cost control and >8 inventory turns/year to sustain retail profitability.

Shortage of Qualified Healthcare Professionals

Like much of global healthcare, Green Cross Health faces ongoing shortages of pharmacists and GPs; New Zealand reported a 2024 shortfall of about 1,200 primary care clinicians, tightening local hiring pools and raising turnover.

Higher labor costs—wage growth for nurses and pharmacists rose ~6% in 2023–24—push operating expenses and trimmed FY2024 operating margin by roughly 0.8 percentage points.

Staff limits cap clinic capacity: workforce bottlenecks restrict extended hours and slow new clinic openings, risking lost revenue from unmet demand.

Geographic Concentration Risk

Despite national dominance, Green Cross Health operates solely in New Zealand, exposing it to local downturns and policy shifts; NZ GDP fell 0.1% q/q in Q3 2025, highlighting cyclical risk.

Concentration risks magnify: 2024 revenue NZD 895m came almost entirely from domestic pharmacy, medical and related services, so a regulatory hit or recession would disproportionately affect cash flows.

- Single-market exposure: 100% NZ operations

- Revenue FY2024: NZD 895 million

- NZ GDP contraction Q3 2025: -0.1% q/q

- High policy sensitivity: local health reforms can cut margins

Integration Complexity of Acquisitions

NZ healthcare operator exposed: 65% public funding, thin margins, staffing squeeze

Heavy reliance on NZ public funding (~NZD 720m, ~65% of FY2025 revenue) makes earnings sensitive to policy changes; a contract shift could swing EBT by NZD 20–40m. Retail margins are thin (front-shop gross ~22% in 2024; listed chains net 3–5% FY2024) and require >8 inventory turns/year. Workforce shortages (≈1,200 primary care shortfall in 2024) and 12% higher admin costs plus NZD 9.8m integration spend strain margins.

| Metric | Value |

|---|---|

| Total revenue FY2024 | NZD 895m |

| Public-funding share FY2025 | NZD 720m (≈65%) |

| Potential EBT swing | NZD 20–40m |

| Integration cost FY24 | NZD 9.8m |

| Admin cost rise 2024 | 12% |

| Primary care shortfall 2024 | ≈1,200 clinicians |

Preview the Actual Deliverable

Green Cross Health SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.