Green Dot Boston Consulting Group Matrix

Actionable Strategy Starts Here

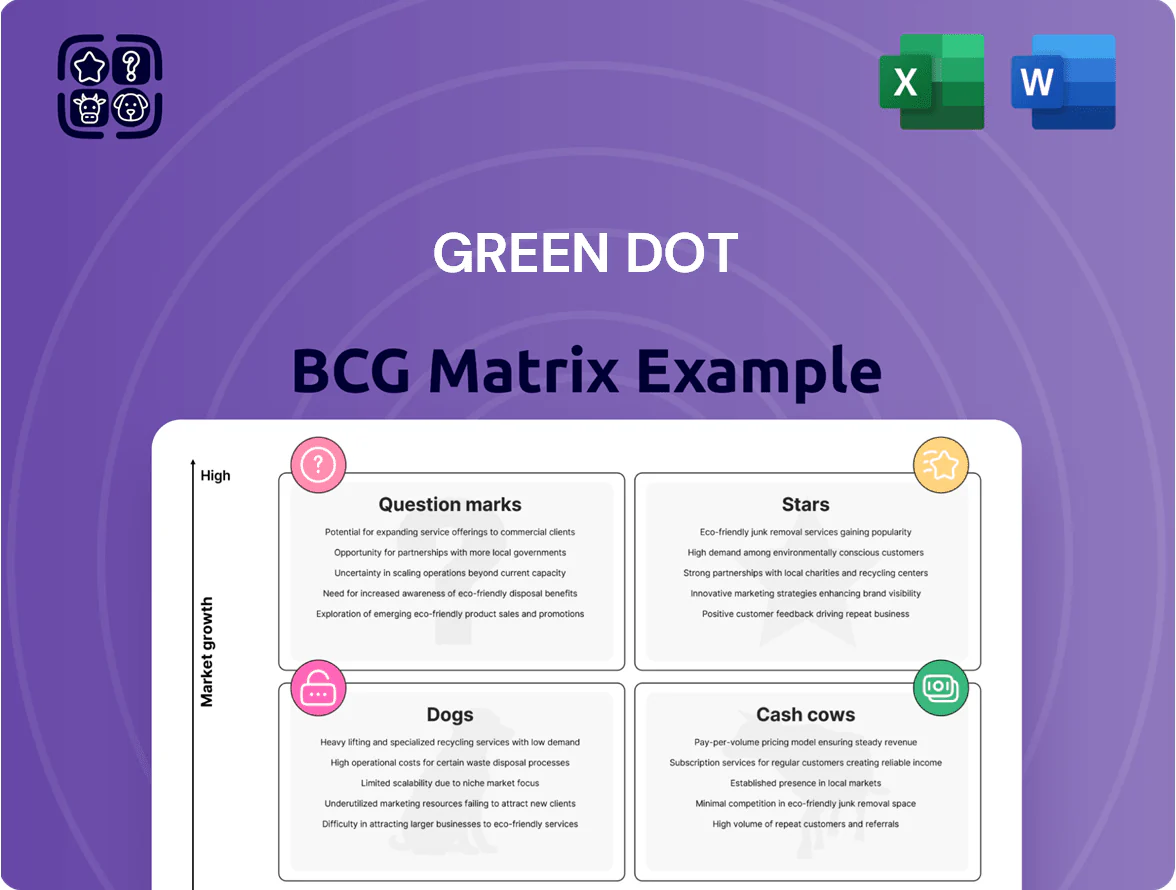

The Green Dot BCG Matrix preview highlights how its product portfolio balances market share and growth potential, revealing likely Stars, Cash Cows, Dogs, and Question Marks to inform resource allocation and strategic focus. This snapshot clarifies competitive strengths and risk areas but only scratches the surface of actionable strategy. Purchase the full BCG Matrix for quadrant-by-quadrant placement, data-backed recommendations, and downloadable Word and Excel files that let you present, prioritize, and deploy capital with confidence.

Stars

BaaS Enterprise Platform

The Banking-as-a-Service (BaaS) Enterprise Platform is Green Dot’s primary growth engine as of late 2025, supporting major tech ecosystems including Apple and Uber and driving roughly 62% of Green Dot’s 2024–2025 revenue growth trajectory.

The unit holds high market share among regulated bank partners for non-financial corporates, managing over $40 billion in annual transaction volume and servicing more than 25 large platform clients.

Continued investment is required to handle complex compliance—covering CFPB, OCC, and state-level rules—and to scale tech for peak loads that exceed 100,000 TPS (transactions per second) during promotional events.

GO2bank Digital Brand

GO2bank, Green Dot’s flagship digital account, holds an estimated 18–22% share of the US mobile-first underbanked segment as of Q4 2025, up from ~12% in 2022.

The brand sits in a high-growth market—digital banking users grew 9% CAGR 2022–2025—driven by demand for low-fee accounts and mobile cash services.

Green Dot reported GO2bank-related marketing and promo spend of ~$220 million in 2024 to defend share against neo-banks and maintain market leadership.

Embedded Finance Integrations

Green Dot leads embedded finance for corporates, leveraging bank holding company status to win deals over fintechs; embedded-account volumes grew ~28% YoY to $18.4B TPV in FY2024, per company filings.

Direct Deposit Capture

Direct Deposit Capture is a Star: Green Dot targets primary account status by integrating with employer payrolls, driving 18% year-over-year growth in funded accounts and adding $2.3B in low-cost deposits in 2025 that lower funding costs and support lending.

Securing steady payroll inflows converts one-off card users to long-term digital banking customers, boosting cross-sell rates by 27% and reducing funding volatility.

- 18% YoY funded-account growth

- $2.3B payroll-driven deposits in 2025

- 27% higher cross-sell after direct deposit

- Lowered funding cost via stable deposits

Modernized Tax Processing

Through its TPG unit, Green Dot processes tax refund disbursements for roughly 15 million Americans annually and moved about $12 billion in refunds in 2024, keeping Modernized Tax Processing a Star due to scale and network effects.

The tax industry is mature, but digital-only disbursements grew ~18% YoY through 2025, and Green Dot’s market share (~35% of refund reloads) sustains strong margins and high cash flow velocity.

- 15M customers served annually

- $12B refunds processed in 2024

- ~35% market share in refund reloads

- Digital disbursements +18% YoY to 2025

BaaS, GO2bank & TPG Fuel Rapid Growth: $40B TPV, $2.3B Payroll, $12B Refunds

Stars: BaaS platform, GO2bank payroll capture, and TPG tax disbursements drive growth—BaaS ~62% of 2024–25 revenue growth, $40B TPV, 100k TPS; GO2bank 18–22% underbanked share, 18% YoY funded-account growth, $2.3B payroll deposits (2025); TPG processes 15M customers, $12B refunds (2024), ~35% refund-reload share.

| Unit | Key metrics |

|---|---|

| BaaS | 62% growth, $40B TPV, 100k TPS |

| GO2bank | 18–22% share, 18% YoY, $2.3B deposits |

| TPG | 15M customers, $12B (2024), ~35% share |

What is included in the product

Comprehensive BCG Matrix review of Green Dot’s portfolio with quadrant-specific strategies, risks, and investment recommendations.

One-page Green Dot BCG Matrix placing units in quadrants for instant portfolio clarity and decision-making

Cash Cows

Retail Prepaid Card Distribution

Green Dot controls the physical retail prepaid card channel across thousands of outlets, including Walmart and Walgreens, holding an estimated 40–50% market share in U.S. retail prepaid sales as of 2025; unit volumes are stable, with ~30 million cards activated annually. This mature, low-growth market yields high gross margins—reported prepaid card margin contribution approximated $350–450 million in 2024—so Green Dot converts sales into cash efficiently. With infrastructure fully built (retail POS, distribution, clearing), incremental capital expenditure is minimal, enabling strong free cash flow generation and steady dividends to fund growth areas. What this hides: customer acquisition and interchange pressures could compress margins over time.

Walmart MoneyCard Partnership

The Walmart MoneyCard partnership delivers steady revenue—Green Dot reported that prepaid and payments revenue tied to retailer relationships represented about $799 million of total 2024 revenue, giving predictable cash flows that outpace internal consumption.

As a mature product, MoneyCard needs minimal promo spend versus Green Dot’s digital initiatives; card-related marketing and fulfillment costs fell year-over-year, keeping margins higher.

Cash from this partnership funds growth into higher-risk fintech plays—Green Dot had $1.1 billion in cash and equivalents at end-2024, a buffer used to invest in volatile segments.

The Green Dot Reload Network

The Green Dot Reload Network processes cash loads at over 80,000 retail points nationwide, making it the industry standard for in-store cash-in as of 2025; that ubiquity supports a >40% market share in physical retail cash loading.

With system-wide load volumes around $18 billion in 2024 and fee-based margin near 65%, the network provides steady, low-cost cash flow and requires minimal ongoing capex and maintenance.

Corporate Payroll Card Services

Green Dot’s Corporate Payroll Card Services act as a cash cow: over 3.5 million payroll cards in force (2025 filing) serve large, stable corporate clients providing pay to largely unbanked employees, producing high retention and steady fee revenue with low market growth.

This segment generated about $420 million in 2024 net revenue, underpinning operating cash flow and bolstering liquidity—helping Green Dot report $1.1 billion cash and equivalents at year-end 2024.

- High retention: low churn among corporate clients

- Scale: 3.5M payroll cards in force (2025)

- Revenue: ~$420M net (2024)

- Liquidity support: $1.1B cash & equivalents (YE 2024)

Government Benefit Disbursement

Government Benefit Disbursement is a legacy service with high market share and low volatility; Green Dot processed about $22 billion in state and federal disbursements in 2024, retaining roughly 35% market share in prepaid benefit programs.

Market growth is modest, ~2–3% CAGR expected through 2027, but Green Dot’s certified compliance framework and SOC 1/SOC 2 reports make it a preferred partner for 30+ state programs.

Steady per-account fees generated ~$120 million in 2024 revenue, helping cover corporate debt servicing and funding R&D for new digital payments products.

- Stable cash flow: ~$120M revenue (2024)

- Scale: processed ~$22B (2024)

- Market share: ~35% in prepaid benefits

- Growth: 2–3% CAGR to 2027

- Compliance: SOC 1/2, 30+ state contracts

Green Dot's cash-cow lineup fuels strong FCF with low capex and $1.1B cash

Green Dot's cash cows—retail prepaid (40–50% share; ~30M cards/yr), Walmart MoneyCard (part of $799M retailer-tied 2024 revenue), Reload Network (~$18B loads, 65% fee margin in 2024), payroll cards (3.5M cards; ~$420M net 2024), and government disbursements (~$22B processed; ~$120M revenue 2024)—produce strong free cash flow and low incremental capex.

| Metric | 2024/2025 |

|---|---|

| Retail share | 40–50% |

| Cards activated | ~30M/yr |

| Reload volume | $18B |

| Payroll cards | 3.5M |

| Cash | $1.1B |

Delivered as Shown

Green Dot BCG Matrix

The file you're previewing on this page is the final Green Dot BCG Matrix you'll receive after purchase—no watermarks, no demo content—just a fully formatted, ready-to-use strategic report built for clarity and professional presentation.

This preview is the exact same Green Dot BCG Matrix report you'll download post-purchase, crafted with precise market insight and formatted for immediate use in planning, pitching, or board reviews.

What you see is the actual file delivered after one-time purchase; once bought, the full Green Dot BCG Matrix is immediately editable, printable, and presentation-ready for your team or clients.

The document on display is the real Green Dot BCG Matrix you'll get—professionally designed by strategy experts and formatted for seamless integration into your business analysis without surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

The Green Dot BCG Matrix preview highlights how its product portfolio balances market share and growth potential, revealing likely Stars, Cash Cows, Dogs, and Question Marks to inform resource allocation and strategic focus. This snapshot clarifies competitive strengths and risk areas but only scratches the surface of actionable strategy. Purchase the full BCG Matrix for quadrant-by-quadrant placement, data-backed recommendations, and downloadable Word and Excel files that let you present, prioritize, and deploy capital with confidence.

Stars

BaaS Enterprise Platform

The Banking-as-a-Service (BaaS) Enterprise Platform is Green Dot’s primary growth engine as of late 2025, supporting major tech ecosystems including Apple and Uber and driving roughly 62% of Green Dot’s 2024–2025 revenue growth trajectory.

The unit holds high market share among regulated bank partners for non-financial corporates, managing over $40 billion in annual transaction volume and servicing more than 25 large platform clients.

Continued investment is required to handle complex compliance—covering CFPB, OCC, and state-level rules—and to scale tech for peak loads that exceed 100,000 TPS (transactions per second) during promotional events.

GO2bank Digital Brand

GO2bank, Green Dot’s flagship digital account, holds an estimated 18–22% share of the US mobile-first underbanked segment as of Q4 2025, up from ~12% in 2022.

The brand sits in a high-growth market—digital banking users grew 9% CAGR 2022–2025—driven by demand for low-fee accounts and mobile cash services.

Green Dot reported GO2bank-related marketing and promo spend of ~$220 million in 2024 to defend share against neo-banks and maintain market leadership.

Embedded Finance Integrations

Green Dot leads embedded finance for corporates, leveraging bank holding company status to win deals over fintechs; embedded-account volumes grew ~28% YoY to $18.4B TPV in FY2024, per company filings.

Direct Deposit Capture

Direct Deposit Capture is a Star: Green Dot targets primary account status by integrating with employer payrolls, driving 18% year-over-year growth in funded accounts and adding $2.3B in low-cost deposits in 2025 that lower funding costs and support lending.

Securing steady payroll inflows converts one-off card users to long-term digital banking customers, boosting cross-sell rates by 27% and reducing funding volatility.

- 18% YoY funded-account growth

- $2.3B payroll-driven deposits in 2025

- 27% higher cross-sell after direct deposit

- Lowered funding cost via stable deposits

Modernized Tax Processing

Through its TPG unit, Green Dot processes tax refund disbursements for roughly 15 million Americans annually and moved about $12 billion in refunds in 2024, keeping Modernized Tax Processing a Star due to scale and network effects.

The tax industry is mature, but digital-only disbursements grew ~18% YoY through 2025, and Green Dot’s market share (~35% of refund reloads) sustains strong margins and high cash flow velocity.

- 15M customers served annually

- $12B refunds processed in 2024

- ~35% market share in refund reloads

- Digital disbursements +18% YoY to 2025

BaaS, GO2bank & TPG Fuel Rapid Growth: $40B TPV, $2.3B Payroll, $12B Refunds

Stars: BaaS platform, GO2bank payroll capture, and TPG tax disbursements drive growth—BaaS ~62% of 2024–25 revenue growth, $40B TPV, 100k TPS; GO2bank 18–22% underbanked share, 18% YoY funded-account growth, $2.3B payroll deposits (2025); TPG processes 15M customers, $12B refunds (2024), ~35% refund-reload share.

| Unit | Key metrics |

|---|---|

| BaaS | 62% growth, $40B TPV, 100k TPS |

| GO2bank | 18–22% share, 18% YoY, $2.3B deposits |

| TPG | 15M customers, $12B (2024), ~35% share |

What is included in the product

Comprehensive BCG Matrix review of Green Dot’s portfolio with quadrant-specific strategies, risks, and investment recommendations.

One-page Green Dot BCG Matrix placing units in quadrants for instant portfolio clarity and decision-making

Cash Cows

Retail Prepaid Card Distribution

Green Dot controls the physical retail prepaid card channel across thousands of outlets, including Walmart and Walgreens, holding an estimated 40–50% market share in U.S. retail prepaid sales as of 2025; unit volumes are stable, with ~30 million cards activated annually. This mature, low-growth market yields high gross margins—reported prepaid card margin contribution approximated $350–450 million in 2024—so Green Dot converts sales into cash efficiently. With infrastructure fully built (retail POS, distribution, clearing), incremental capital expenditure is minimal, enabling strong free cash flow generation and steady dividends to fund growth areas. What this hides: customer acquisition and interchange pressures could compress margins over time.

Walmart MoneyCard Partnership

The Walmart MoneyCard partnership delivers steady revenue—Green Dot reported that prepaid and payments revenue tied to retailer relationships represented about $799 million of total 2024 revenue, giving predictable cash flows that outpace internal consumption.

As a mature product, MoneyCard needs minimal promo spend versus Green Dot’s digital initiatives; card-related marketing and fulfillment costs fell year-over-year, keeping margins higher.

Cash from this partnership funds growth into higher-risk fintech plays—Green Dot had $1.1 billion in cash and equivalents at end-2024, a buffer used to invest in volatile segments.

The Green Dot Reload Network

The Green Dot Reload Network processes cash loads at over 80,000 retail points nationwide, making it the industry standard for in-store cash-in as of 2025; that ubiquity supports a >40% market share in physical retail cash loading.

With system-wide load volumes around $18 billion in 2024 and fee-based margin near 65%, the network provides steady, low-cost cash flow and requires minimal ongoing capex and maintenance.

Corporate Payroll Card Services

Green Dot’s Corporate Payroll Card Services act as a cash cow: over 3.5 million payroll cards in force (2025 filing) serve large, stable corporate clients providing pay to largely unbanked employees, producing high retention and steady fee revenue with low market growth.

This segment generated about $420 million in 2024 net revenue, underpinning operating cash flow and bolstering liquidity—helping Green Dot report $1.1 billion cash and equivalents at year-end 2024.

- High retention: low churn among corporate clients

- Scale: 3.5M payroll cards in force (2025)

- Revenue: ~$420M net (2024)

- Liquidity support: $1.1B cash & equivalents (YE 2024)

Government Benefit Disbursement

Government Benefit Disbursement is a legacy service with high market share and low volatility; Green Dot processed about $22 billion in state and federal disbursements in 2024, retaining roughly 35% market share in prepaid benefit programs.

Market growth is modest, ~2–3% CAGR expected through 2027, but Green Dot’s certified compliance framework and SOC 1/SOC 2 reports make it a preferred partner for 30+ state programs.

Steady per-account fees generated ~$120 million in 2024 revenue, helping cover corporate debt servicing and funding R&D for new digital payments products.

- Stable cash flow: ~$120M revenue (2024)

- Scale: processed ~$22B (2024)

- Market share: ~35% in prepaid benefits

- Growth: 2–3% CAGR to 2027

- Compliance: SOC 1/2, 30+ state contracts

Green Dot's cash-cow lineup fuels strong FCF with low capex and $1.1B cash

Green Dot's cash cows—retail prepaid (40–50% share; ~30M cards/yr), Walmart MoneyCard (part of $799M retailer-tied 2024 revenue), Reload Network (~$18B loads, 65% fee margin in 2024), payroll cards (3.5M cards; ~$420M net 2024), and government disbursements (~$22B processed; ~$120M revenue 2024)—produce strong free cash flow and low incremental capex.

| Metric | 2024/2025 |

|---|---|

| Retail share | 40–50% |

| Cards activated | ~30M/yr |

| Reload volume | $18B |

| Payroll cards | 3.5M |

| Cash | $1.1B |

Delivered as Shown

Green Dot BCG Matrix

The file you're previewing on this page is the final Green Dot BCG Matrix you'll receive after purchase—no watermarks, no demo content—just a fully formatted, ready-to-use strategic report built for clarity and professional presentation.

This preview is the exact same Green Dot BCG Matrix report you'll download post-purchase, crafted with precise market insight and formatted for immediate use in planning, pitching, or board reviews.

What you see is the actual file delivered after one-time purchase; once bought, the full Green Dot BCG Matrix is immediately editable, printable, and presentation-ready for your team or clients.

The document on display is the real Green Dot BCG Matrix you'll get—professionally designed by strategy experts and formatted for seamless integration into your business analysis without surprises.