GreeneStone Healthcare Corp. Porter's Five Forces Analysis

Don't Miss the Bigger Picture

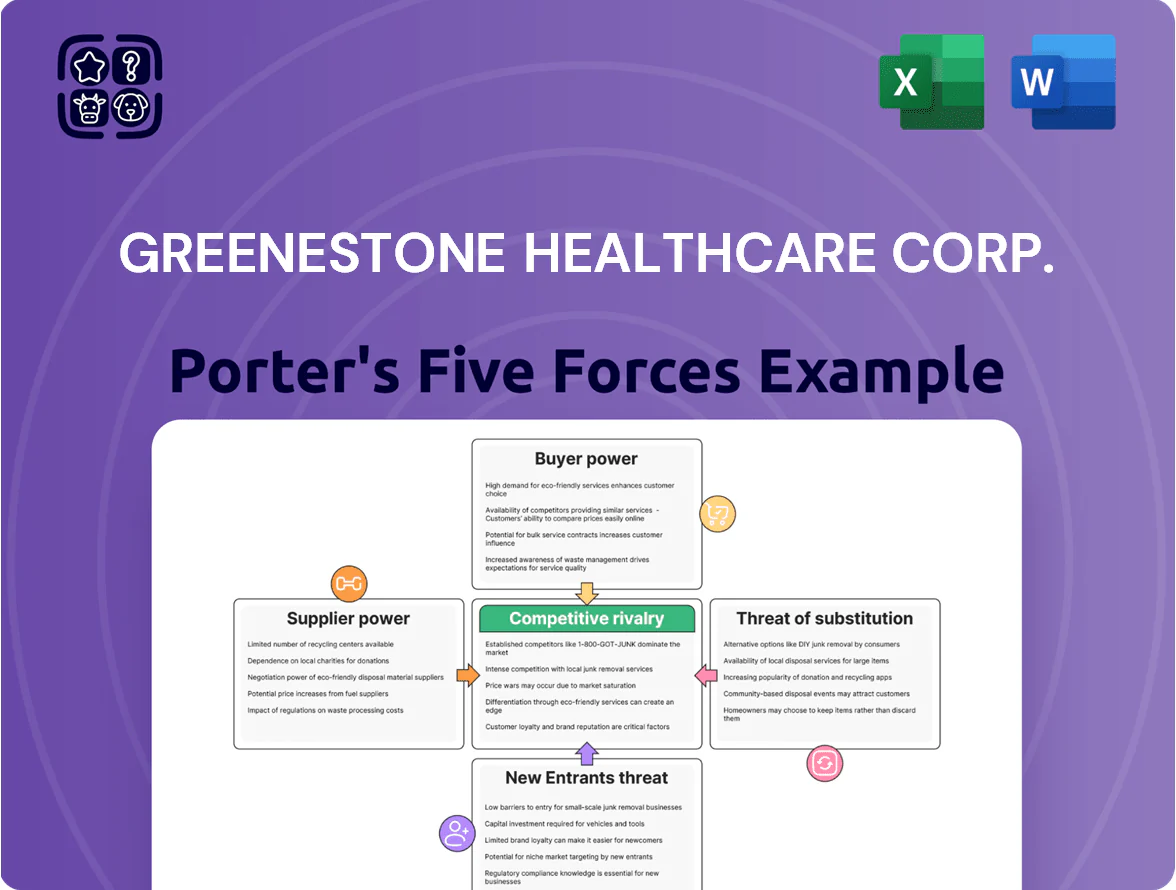

GreeneStone Healthcare faces moderate supplier power and regulatory pressures, while buyer demands and substitute innovations heighten competitive intensity—new entrants are tempered by scale and certification barriers. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore GreeneStone Healthcare Corp.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Medical Professionals

The addiction treatment sector depends on licensed psychiatrists, RNs, and certified addiction counselors, who commanded a 2024 US median wage premium of 18% over comparable roles and vacancy rates of 12–15% in behavioral health; this specialty and certification requirement gives suppliers strong bargaining power over GreeneStone Healthcare Corp., raising labor costs (staffing costs rose ~9% YoY in 2023) and risking operational disruption when turnover spikes or hiring lags.

Pharmaceutical and Medical Supply Vendors

Suppliers of specialized detox and pain meds are dominated by large pharma firms holding patents; in 2024 branded drugs accounted for 72% of US drug spending, boosting supplier leverage. Patents and formulary exclusivity limit GreeneStone Healthcare Corp.’s bargaining options, making these meds essential and price-inelastic in clinical use. A 10% drug-price rise in 2023 would cut operating margins by ~1.5–2 percentage points for comparable outpatient providers.

Real Estate and Facility Landlords

Residential treatment centers need specific zoning and facility upgrades to meet health and safety rules, so suitable sites are scarce; in the US in 2024, hospital-grade facility vacancies averaged under 6%, tightening options for GreeneStone Healthcare Corp. Landlords therefore hold strong leverage in lease terms and rent growth—commercial rent-for-healthcare rose 4.8% YoY in 2024—while relocating a clinical operation can cost $500k–$2M and disrupt revenue, creating significant supplier lock-in.

Accreditation and Regulatory Agencies

Provincial health authorities and accreditation bodies supply the legal license and professional status GreeneStone Healthcare needs; in Canada 2024, 98% of clinics required provincial certification to bill public plans, making these bodies gatekeepers of revenue.

They set mandatory standards for care, safety, and reporting—noncompliance leads to license revocation and immediate revenue loss; Ontario hospitals face fines up to CAD 100,000 and suspension risks tied to audit failures.

Their bargaining power is absolute: GreeneStone cannot substitute these suppliers, so regulatory shifts (e.g., 2025 updated infection-control rules) directly affect costs, capital spending, and operational continuity.

- 98% clinics need provincial certification to bill

- License loss = immediate revenue stop

- Fines up to CAD 100,000 for noncompliance

- 2025 infection-control rule changes raise capex

Specialized Healthcare Technology Providers

- Global EHR market $35.5B (2024)

- Switch costs $150–400k per clinic

- Switch time 6–12 months

- 72% outages tied to third-party software

Suppliers dominate behavioral health: wages, drugs, facilities, regs and EHRs squeeze margins

Suppliers hold strong bargaining power: skilled staff premiums (+18% wage gap; 12–15% vacancy), patented drugs (branded = 72% of US drug spend, price-inelastic), scarce compliant facilities (healthcare vacancy <6%, rent +4.8% YoY; relocation cost $500k–$2M), regulators (98% clinics need certification; fines up to CAD 100,000), and EHR vendors (global market $35.5B; switch $150–400k, 6–12 months).

| Metric | 2024/2025 |

|---|---|

| Staff wage premium | +18% |

| Behavioral health vacancy | 12–15% |

| Branded drug share | 72% US spend |

| Facility vacancy | <6% |

| Commercial rent growth | +4.8% YoY |

| Relocation cost | $500k–$2M |

| Certification required | 98% clinics |

| Max fine | CAD 100,000 |

| EHR market | $35.5B |

| Switch cost/time | $150–400k; 6–12m |

What is included in the product

Tailored Porter's Five Forces analysis for GreeneStone Healthcare Corp. uncovering competitive intensity, buyer and supplier leverage, threat of substitutes and new entrants, and strategic levers that protect or expose its market position.

A concise Porter's Five Forces snapshot for GreeneStone Healthcare Corp.—quickly highlights supplier & buyer leverage, competitive rivalry, threat of substitutes, and entry barriers to guide strategic moves.

Customers Bargaining Power

Individual Patient and Family Choice

Patients and families choosing private addiction treatment often compare 3–7 facilities before deciding, so individual buyers wield strong leverage over GreeneStone Healthcare Corp.; a 2023 Behavior Health report found 62% of admissions were influenced by online reviews and placement fees.

Because median private program costs range $15,000–$45,000 per episode (2024 SAMHSA-linked pricing), price sensitivity raises bargaining power and pushes providers to offer sliding scales or bundled services.

Reputation and amenities matter: 48% of prospective clients cite facility ratings and aftercare outcomes as top factors, so GreeneStone must maintain transparent outcomes and competitive amenities to limit churn.

Private Insurance Intermediaries

Private insurers control patient access and payment: in 2024 the top five US insurers covered about 60% of the commercially insured population, letting them demand lower rates and impose standardized care protocols that cut provider margins by 5–15% on average.

Government Health Funding and Agencies

Government health agencies in Canada fund about 70% of total health spending (CIHI 2023), so their coverage decisions set de facto price ceilings for services private providers can charge.

If provincial formularies or fee schedules shift—Ontario’s OHIP average physician fee rose 1.8% in 2024—private clinics must adjust pricing or offer non-covered add-ons to stay competitive.

For GreeneStone Healthcare Corp., dependence on public benchmarks limits margin expansion; captive segments often require alignment with publicly funded rates to retain patient volume.

Corporate Referral and Employee Assistance Programs

- 157M employees in employer plans (2024)

- 62% of employers negotiate bundled rates (2023)

- Ability to shift whole workforce = high bargaining leverage

- Pressure toward outcome-based, lower per-case fees

Information Transparency and Online Reviews

The rise of online reviews and public outcome data gives GreeneStone Healthcare Corp. patients more choice: 78% of US healthcare consumers used online ratings in 2024, and clinics with <3.5 ratings see 12-18% lower new-patient volume, so GreeneStone must sustain high outcomes and transparency to compete.

Transparency shifts bargaining power to patients, who can demand better service levels and price transparency; negative reviews quickly reduce referrals and revenue, pressuring quality investments.

- 78% of patients use online ratings (2024)

- <3.5-star clinics lose 12–18% new patients

- Public outcome reporting raises compliance costs

High buyer power: patients, insurers & employers squeeze GreeneStone on price and outcomes

Patients, insurers, employers and public payers exert high bargaining power on GreeneStone: patients compare 3–7 facilities and 78% use online ratings (2024); private program costs $15k–$45k (2024), driving price sensitivity; top‑5 insurers cover ~60% commercially (2024) and employers (157M covered, 2024) push bundled/outcome pricing.

| Metric | 2024/2023 |

|---|---|

| Patient comparison | 3–7 facilities |

| Online ratings use | 78% |

| Private cost per episode | $15k–$45k |

| Top‑5 insurer share | ~60% |

| Employees in plans | 157M |

Preview the Actual Deliverable

GreeneStone Healthcare Corp. Porter's Five Forces Analysis

This preview shows the exact GreeneStone Healthcare Corp. Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups; it's fully formatted and ready for download.

You're viewing the actual deliverable: a concise, professionally written assessment of competitive rivalry, supplier and buyer power, threat of entrants, and substitutes, available instantly once you complete payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

GreeneStone Healthcare faces moderate supplier power and regulatory pressures, while buyer demands and substitute innovations heighten competitive intensity—new entrants are tempered by scale and certification barriers. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore GreeneStone Healthcare Corp.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Medical Professionals

The addiction treatment sector depends on licensed psychiatrists, RNs, and certified addiction counselors, who commanded a 2024 US median wage premium of 18% over comparable roles and vacancy rates of 12–15% in behavioral health; this specialty and certification requirement gives suppliers strong bargaining power over GreeneStone Healthcare Corp., raising labor costs (staffing costs rose ~9% YoY in 2023) and risking operational disruption when turnover spikes or hiring lags.

Pharmaceutical and Medical Supply Vendors

Suppliers of specialized detox and pain meds are dominated by large pharma firms holding patents; in 2024 branded drugs accounted for 72% of US drug spending, boosting supplier leverage. Patents and formulary exclusivity limit GreeneStone Healthcare Corp.’s bargaining options, making these meds essential and price-inelastic in clinical use. A 10% drug-price rise in 2023 would cut operating margins by ~1.5–2 percentage points for comparable outpatient providers.

Real Estate and Facility Landlords

Residential treatment centers need specific zoning and facility upgrades to meet health and safety rules, so suitable sites are scarce; in the US in 2024, hospital-grade facility vacancies averaged under 6%, tightening options for GreeneStone Healthcare Corp. Landlords therefore hold strong leverage in lease terms and rent growth—commercial rent-for-healthcare rose 4.8% YoY in 2024—while relocating a clinical operation can cost $500k–$2M and disrupt revenue, creating significant supplier lock-in.

Accreditation and Regulatory Agencies

Provincial health authorities and accreditation bodies supply the legal license and professional status GreeneStone Healthcare needs; in Canada 2024, 98% of clinics required provincial certification to bill public plans, making these bodies gatekeepers of revenue.

They set mandatory standards for care, safety, and reporting—noncompliance leads to license revocation and immediate revenue loss; Ontario hospitals face fines up to CAD 100,000 and suspension risks tied to audit failures.

Their bargaining power is absolute: GreeneStone cannot substitute these suppliers, so regulatory shifts (e.g., 2025 updated infection-control rules) directly affect costs, capital spending, and operational continuity.

- 98% clinics need provincial certification to bill

- License loss = immediate revenue stop

- Fines up to CAD 100,000 for noncompliance

- 2025 infection-control rule changes raise capex

Specialized Healthcare Technology Providers

- Global EHR market $35.5B (2024)

- Switch costs $150–400k per clinic

- Switch time 6–12 months

- 72% outages tied to third-party software

Suppliers dominate behavioral health: wages, drugs, facilities, regs and EHRs squeeze margins

Suppliers hold strong bargaining power: skilled staff premiums (+18% wage gap; 12–15% vacancy), patented drugs (branded = 72% of US drug spend, price-inelastic), scarce compliant facilities (healthcare vacancy <6%, rent +4.8% YoY; relocation cost $500k–$2M), regulators (98% clinics need certification; fines up to CAD 100,000), and EHR vendors (global market $35.5B; switch $150–400k, 6–12 months).

| Metric | 2024/2025 |

|---|---|

| Staff wage premium | +18% |

| Behavioral health vacancy | 12–15% |

| Branded drug share | 72% US spend |

| Facility vacancy | <6% |

| Commercial rent growth | +4.8% YoY |

| Relocation cost | $500k–$2M |

| Certification required | 98% clinics |

| Max fine | CAD 100,000 |

| EHR market | $35.5B |

| Switch cost/time | $150–400k; 6–12m |

What is included in the product

Tailored Porter's Five Forces analysis for GreeneStone Healthcare Corp. uncovering competitive intensity, buyer and supplier leverage, threat of substitutes and new entrants, and strategic levers that protect or expose its market position.

A concise Porter's Five Forces snapshot for GreeneStone Healthcare Corp.—quickly highlights supplier & buyer leverage, competitive rivalry, threat of substitutes, and entry barriers to guide strategic moves.

Customers Bargaining Power

Individual Patient and Family Choice

Patients and families choosing private addiction treatment often compare 3–7 facilities before deciding, so individual buyers wield strong leverage over GreeneStone Healthcare Corp.; a 2023 Behavior Health report found 62% of admissions were influenced by online reviews and placement fees.

Because median private program costs range $15,000–$45,000 per episode (2024 SAMHSA-linked pricing), price sensitivity raises bargaining power and pushes providers to offer sliding scales or bundled services.

Reputation and amenities matter: 48% of prospective clients cite facility ratings and aftercare outcomes as top factors, so GreeneStone must maintain transparent outcomes and competitive amenities to limit churn.

Private Insurance Intermediaries

Private insurers control patient access and payment: in 2024 the top five US insurers covered about 60% of the commercially insured population, letting them demand lower rates and impose standardized care protocols that cut provider margins by 5–15% on average.

Government Health Funding and Agencies

Government health agencies in Canada fund about 70% of total health spending (CIHI 2023), so their coverage decisions set de facto price ceilings for services private providers can charge.

If provincial formularies or fee schedules shift—Ontario’s OHIP average physician fee rose 1.8% in 2024—private clinics must adjust pricing or offer non-covered add-ons to stay competitive.

For GreeneStone Healthcare Corp., dependence on public benchmarks limits margin expansion; captive segments often require alignment with publicly funded rates to retain patient volume.

Corporate Referral and Employee Assistance Programs

- 157M employees in employer plans (2024)

- 62% of employers negotiate bundled rates (2023)

- Ability to shift whole workforce = high bargaining leverage

- Pressure toward outcome-based, lower per-case fees

Information Transparency and Online Reviews

The rise of online reviews and public outcome data gives GreeneStone Healthcare Corp. patients more choice: 78% of US healthcare consumers used online ratings in 2024, and clinics with <3.5 ratings see 12-18% lower new-patient volume, so GreeneStone must sustain high outcomes and transparency to compete.

Transparency shifts bargaining power to patients, who can demand better service levels and price transparency; negative reviews quickly reduce referrals and revenue, pressuring quality investments.

- 78% of patients use online ratings (2024)

- <3.5-star clinics lose 12–18% new patients

- Public outcome reporting raises compliance costs

High buyer power: patients, insurers & employers squeeze GreeneStone on price and outcomes

Patients, insurers, employers and public payers exert high bargaining power on GreeneStone: patients compare 3–7 facilities and 78% use online ratings (2024); private program costs $15k–$45k (2024), driving price sensitivity; top‑5 insurers cover ~60% commercially (2024) and employers (157M covered, 2024) push bundled/outcome pricing.

| Metric | 2024/2023 |

|---|---|

| Patient comparison | 3–7 facilities |

| Online ratings use | 78% |

| Private cost per episode | $15k–$45k |

| Top‑5 insurer share | ~60% |

| Employees in plans | 157M |

Preview the Actual Deliverable

GreeneStone Healthcare Corp. Porter's Five Forces Analysis

This preview shows the exact GreeneStone Healthcare Corp. Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups; it's fully formatted and ready for download.

You're viewing the actual deliverable: a concise, professionally written assessment of competitive rivalry, supplier and buyer power, threat of entrants, and substitutes, available instantly once you complete payment.