Grid Dynamics Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

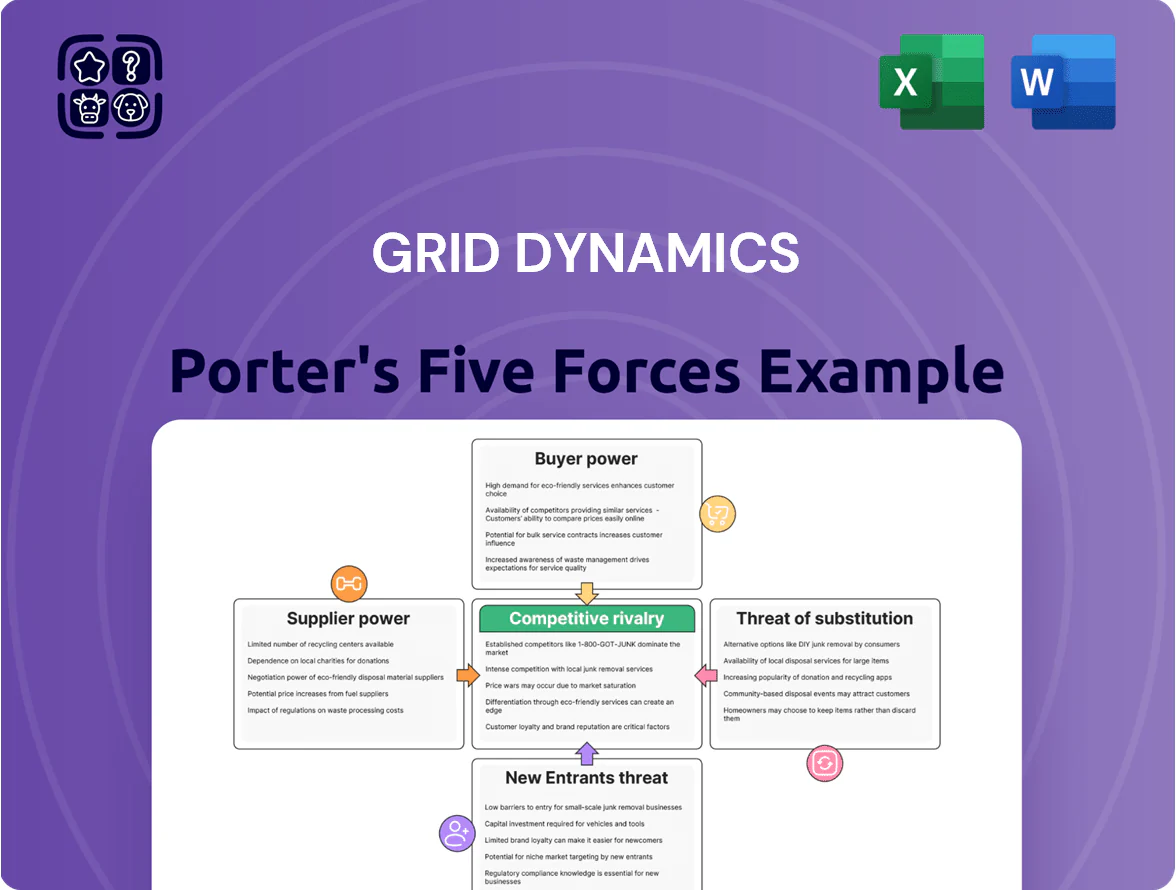

Grid Dynamics faces moderate supplier power, high buyer expectations for customization, and intense rivalry from digital transformation specialists, with moderate threats from new entrants and substitutes due to rapid tech innovation.

Suppliers Bargaining Power

Scarcity of specialized technical talent

The primary suppliers for Grid Dynamics are highly skilled software engineers and data scientists, and by late 2025 scarcity of Generative AI and advanced cloud-architecture experts raised workforce bargaining power—industry reports show a 28% supply shortfall in ML specialists and a 22% rise in median total compensation for cloud engineers in 2024–25. Grid Dynamics must invest in retention and pay increases—estimated at 10–18% incremental labor cost—to sustain delivery capacity.

Dominance of cloud infrastructure providers

Grid Dynamics depends on AWS, Microsoft Azure, and Google Cloud for core delivery; together the three control over 65% of global cloud IaaS/PaaS market (2024) so supplier leverage is high.

Their platforms are essential for cloud-native engineering, meaning API or service changes can force rework and delay roadmaps; in 2024 hyperscaler price hikes averaged ~8–12% across key services.

Price or access shifts directly squeeze project margins—Grid Dynamics reported cloud-related costs as a material input in 2024 revenue mix, affecting gross margins on large engagements.

Geopolitical stability of talent hubs

Grid Dynamics sources engineers heavily from Eastern Europe and emerging hubs in Central Asia and Latin America; in 2024 about 48% of its delivery staff were based in these regions, so regional political shifts or labor-law changes can sharply disrupt hiring and ramp times. Such concentration raises indirect bargaining power for local labor markets and governments, risking wage inflation—recently wage growth hit 12–18% in parts of Eastern Europe—and can increase operating costs and margin pressure.

Influence of specialized software vendors

The delivery of complex data analytics and AI solutions often relies on proprietary third-party software (licenses for tools like Databricks, Snowflake, NVIDIA SDKs), which gives specialized vendors leverage via tiered pricing and mandatory partner certifications; in 2024 enterprise software licensing grew 8.7% globally to $620B, raising Grid Dynamics’ input costs.

Grid Dynamics must keep close supplier ties and certified engineers to stay competitive while negotiating volume discounts and balancing partner-program fees that can exceed 5–10% of project margins.

- Proprietary licenses drive supplier power

- Partner certifications required, add fixed costs

- Volume discounts and long-term contracts lower risk

- Software fees can eat 5–10% of margins

Academic and certification institutions

The supply of entry-level talent and upskilling at Grid Dynamics depends heavily on universities and certification bodies that set technical standards and funnel new hires; US STEM graduates rose 3.8% to 224,000 in 2023, keeping pressure on demand for cloud, AI, and data skills.

Shorter tech cycles mean these suppliers shape hiring speed and quality—certifications like AWS, Google Cloud, and Coursera specializations drove 18% year-on-year growth in hires with cloud credentials in 2024, affecting training budgets and time-to-productivity.

Dependency creates bargaining power: institutions can influence hiring costs and curricula, so Grid Dynamics must co-invest in partnerships, apprenticeships, and sponsored curricula to secure industry-ready talent.

- 224,000 US STEM grads (2023)

- +18% hires with cloud certs (2024)

- Higher training budgets and faster reskilling needs

Hyperscalers, rising software costs & talent gaps squeeze margins—partner discounts needed

Suppliers hold high power: hyperscalers (AWS, Azure, GCP) control 65%+ IaaS/PaaS (2024), proprietary tool licensing grew 8.7% to $620B (2024), and skilled talent shortages (28% ML shortfall, 22% cloud pay rise 2024–25) force 10–18% higher labor costs—together these compress margins and require partner discounts and retention spend.

| Metric | Value |

|---|---|

| Hyperscaler market share (2024) | 65%+ |

| Enterprise software spend (2024) | $620B (+8.7%) |

| ML talent shortfall (2025) | 28% |

| Cloud engineer pay rise (2024–25) | 22% |

| Estimated extra labor cost | 10–18% |

What is included in the product

Tailored analysis of Grid Dynamics using Porter’s Five Forces to reveal competitive intensity, buyer and supplier influence, barriers to entry, threat of substitutes, and insights on strategic levers to protect and grow market share.

Condenses Grid Dynamics’ Porter’s Five Forces into a single, editable sheet—letting teams quickly gauge competitive pressure, tweak force intensities with live data, and drop a clean spider chart straight into pitch decks or reports.

Customers Bargaining Power

Concentration of high-value enterprise clients

Grid Dynamics targets Fortune 1000 enterprises; in 2024 roughly 60% of revenue came from large accounts, so a few clients drive cash flow and utilization.

These buyers wield strong bargaining power: big IT budgets and demand for custom SLAs, pricing, and IP rights force concesssions and margin pressure.

Losing one major client — historically causing up to a 10–15% revenue hit in comparable firms — would sharply reduce utilization and quarterly results.

Low switching costs between service providers

While digital transformation projects are complex, core engineering skills transfer easily across vendors, keeping switching costs low; IDC reported in 2024 that 62% of enterprises use multi-vendor cloud or services stacks to avoid lock-in.

Large firms use multi-vendor strategies to force price competition and retain leverage—Grid Dynamics faces buyer power as clients can reallocate work to competitors if they find better rates or specialized expertise.

Internalization of digital capabilities

Many Fortune 500 firms now build internal AI/Data Centers of Excellence (CoEs); McKinsey found 42% of adopters did so by 2024, reducing external spend by ~15–30% per program. This insourcing trend boosts customer bargaining power—clients can push rates down or shift work internally—so Grid Dynamics must prove superior R&D and deliver measurable ROI (e.g., 20%+ efficiency gains) to remain a strategic external partner.

Demand for outcome-based pricing models

By 2025, 42% of enterprise IT deals shift from time-and-materials to outcome-based pricing, moving financial risk to Grid Dynamics and raising buyer leverage over milestones and success criteria.

Clients demand contracts tying fees to measurable KPIs—revenue lift, cost savings, or deployment speed—so buyers extract stronger governance and ROI guarantees.

Availability of alternative delivery models

The rise of high-quality offshore and nearshore engineering providers—regions like Poland, Romania, India, and Latin America—means Grid Dynamics faces buyers who can easily shop price vs. quality; Deloitte reported 2024 offshore software delivery grew 8.5% with average hourly rates 30–60% below US/Western Europe. Buyers use this price transparency to push harder on fees and SLAs, narrowing Grid Dynamics’ margin flexibility.

- Global offshore growth 8.5% (2024, Deloitte)

- Offshore rates 30–60% lower than US/EU

- Buyers compare Grid to giants and boutiques

- Transparency increases negotiation power

Big clients, rising insourcing, and offshore pressure squeeze vendor margins

Large Fortune 1000 clients give Grid Dynamics high buyer power: ~60% revenue from big accounts (2024), easy vendor switching, and rising insourcing—McKinsey: 42% built AI CoEs (2024). Outcome-based deals rose to 42% (2025), shifting financial risk to providers. Offshore competition grew 8.5% (2024) with rates 30–60% lower, squeezing margins and forcing KPI-tied contracts.

| Metric | Value |

|---|---|

| Revenue from large accounts (2024) | ~60% |

| AI CoEs built (2024, McKinsey) | 42% |

| Outcome-based deals (2025) | 42% |

| Offshore growth (2024, Deloitte) | 8.5% |

| Offshore rate discount | 30–60% |

Full Version Awaits

Grid Dynamics Porter's Five Forces Analysis

This preview shows the exact Grid Dynamics Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for use.

The document displayed here is the same professionally written deliverable available for instant download upon payment, containing complete force assessments, evidence-based insights, and actionable implications.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Grid Dynamics faces moderate supplier power, high buyer expectations for customization, and intense rivalry from digital transformation specialists, with moderate threats from new entrants and substitutes due to rapid tech innovation.

Suppliers Bargaining Power

Scarcity of specialized technical talent

The primary suppliers for Grid Dynamics are highly skilled software engineers and data scientists, and by late 2025 scarcity of Generative AI and advanced cloud-architecture experts raised workforce bargaining power—industry reports show a 28% supply shortfall in ML specialists and a 22% rise in median total compensation for cloud engineers in 2024–25. Grid Dynamics must invest in retention and pay increases—estimated at 10–18% incremental labor cost—to sustain delivery capacity.

Dominance of cloud infrastructure providers

Grid Dynamics depends on AWS, Microsoft Azure, and Google Cloud for core delivery; together the three control over 65% of global cloud IaaS/PaaS market (2024) so supplier leverage is high.

Their platforms are essential for cloud-native engineering, meaning API or service changes can force rework and delay roadmaps; in 2024 hyperscaler price hikes averaged ~8–12% across key services.

Price or access shifts directly squeeze project margins—Grid Dynamics reported cloud-related costs as a material input in 2024 revenue mix, affecting gross margins on large engagements.

Geopolitical stability of talent hubs

Grid Dynamics sources engineers heavily from Eastern Europe and emerging hubs in Central Asia and Latin America; in 2024 about 48% of its delivery staff were based in these regions, so regional political shifts or labor-law changes can sharply disrupt hiring and ramp times. Such concentration raises indirect bargaining power for local labor markets and governments, risking wage inflation—recently wage growth hit 12–18% in parts of Eastern Europe—and can increase operating costs and margin pressure.

Influence of specialized software vendors

The delivery of complex data analytics and AI solutions often relies on proprietary third-party software (licenses for tools like Databricks, Snowflake, NVIDIA SDKs), which gives specialized vendors leverage via tiered pricing and mandatory partner certifications; in 2024 enterprise software licensing grew 8.7% globally to $620B, raising Grid Dynamics’ input costs.

Grid Dynamics must keep close supplier ties and certified engineers to stay competitive while negotiating volume discounts and balancing partner-program fees that can exceed 5–10% of project margins.

- Proprietary licenses drive supplier power

- Partner certifications required, add fixed costs

- Volume discounts and long-term contracts lower risk

- Software fees can eat 5–10% of margins

Academic and certification institutions

The supply of entry-level talent and upskilling at Grid Dynamics depends heavily on universities and certification bodies that set technical standards and funnel new hires; US STEM graduates rose 3.8% to 224,000 in 2023, keeping pressure on demand for cloud, AI, and data skills.

Shorter tech cycles mean these suppliers shape hiring speed and quality—certifications like AWS, Google Cloud, and Coursera specializations drove 18% year-on-year growth in hires with cloud credentials in 2024, affecting training budgets and time-to-productivity.

Dependency creates bargaining power: institutions can influence hiring costs and curricula, so Grid Dynamics must co-invest in partnerships, apprenticeships, and sponsored curricula to secure industry-ready talent.

- 224,000 US STEM grads (2023)

- +18% hires with cloud certs (2024)

- Higher training budgets and faster reskilling needs

Hyperscalers, rising software costs & talent gaps squeeze margins—partner discounts needed

Suppliers hold high power: hyperscalers (AWS, Azure, GCP) control 65%+ IaaS/PaaS (2024), proprietary tool licensing grew 8.7% to $620B (2024), and skilled talent shortages (28% ML shortfall, 22% cloud pay rise 2024–25) force 10–18% higher labor costs—together these compress margins and require partner discounts and retention spend.

| Metric | Value |

|---|---|

| Hyperscaler market share (2024) | 65%+ |

| Enterprise software spend (2024) | $620B (+8.7%) |

| ML talent shortfall (2025) | 28% |

| Cloud engineer pay rise (2024–25) | 22% |

| Estimated extra labor cost | 10–18% |

What is included in the product

Tailored analysis of Grid Dynamics using Porter’s Five Forces to reveal competitive intensity, buyer and supplier influence, barriers to entry, threat of substitutes, and insights on strategic levers to protect and grow market share.

Condenses Grid Dynamics’ Porter’s Five Forces into a single, editable sheet—letting teams quickly gauge competitive pressure, tweak force intensities with live data, and drop a clean spider chart straight into pitch decks or reports.

Customers Bargaining Power

Concentration of high-value enterprise clients

Grid Dynamics targets Fortune 1000 enterprises; in 2024 roughly 60% of revenue came from large accounts, so a few clients drive cash flow and utilization.

These buyers wield strong bargaining power: big IT budgets and demand for custom SLAs, pricing, and IP rights force concesssions and margin pressure.

Losing one major client — historically causing up to a 10–15% revenue hit in comparable firms — would sharply reduce utilization and quarterly results.

Low switching costs between service providers

While digital transformation projects are complex, core engineering skills transfer easily across vendors, keeping switching costs low; IDC reported in 2024 that 62% of enterprises use multi-vendor cloud or services stacks to avoid lock-in.

Large firms use multi-vendor strategies to force price competition and retain leverage—Grid Dynamics faces buyer power as clients can reallocate work to competitors if they find better rates or specialized expertise.

Internalization of digital capabilities

Many Fortune 500 firms now build internal AI/Data Centers of Excellence (CoEs); McKinsey found 42% of adopters did so by 2024, reducing external spend by ~15–30% per program. This insourcing trend boosts customer bargaining power—clients can push rates down or shift work internally—so Grid Dynamics must prove superior R&D and deliver measurable ROI (e.g., 20%+ efficiency gains) to remain a strategic external partner.

Demand for outcome-based pricing models

By 2025, 42% of enterprise IT deals shift from time-and-materials to outcome-based pricing, moving financial risk to Grid Dynamics and raising buyer leverage over milestones and success criteria.

Clients demand contracts tying fees to measurable KPIs—revenue lift, cost savings, or deployment speed—so buyers extract stronger governance and ROI guarantees.

Availability of alternative delivery models

The rise of high-quality offshore and nearshore engineering providers—regions like Poland, Romania, India, and Latin America—means Grid Dynamics faces buyers who can easily shop price vs. quality; Deloitte reported 2024 offshore software delivery grew 8.5% with average hourly rates 30–60% below US/Western Europe. Buyers use this price transparency to push harder on fees and SLAs, narrowing Grid Dynamics’ margin flexibility.

- Global offshore growth 8.5% (2024, Deloitte)

- Offshore rates 30–60% lower than US/EU

- Buyers compare Grid to giants and boutiques

- Transparency increases negotiation power

Big clients, rising insourcing, and offshore pressure squeeze vendor margins

Large Fortune 1000 clients give Grid Dynamics high buyer power: ~60% revenue from big accounts (2024), easy vendor switching, and rising insourcing—McKinsey: 42% built AI CoEs (2024). Outcome-based deals rose to 42% (2025), shifting financial risk to providers. Offshore competition grew 8.5% (2024) with rates 30–60% lower, squeezing margins and forcing KPI-tied contracts.

| Metric | Value |

|---|---|

| Revenue from large accounts (2024) | ~60% |

| AI CoEs built (2024, McKinsey) | 42% |

| Outcome-based deals (2025) | 42% |

| Offshore growth (2024, Deloitte) | 8.5% |

| Offshore rate discount | 30–60% |

Full Version Awaits

Grid Dynamics Porter's Five Forces Analysis

This preview shows the exact Grid Dynamics Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for use.

The document displayed here is the same professionally written deliverable available for instant download upon payment, containing complete force assessments, evidence-based insights, and actionable implications.