GR Infraprojects PESTLE Analysis

Skip the Research. Get the Strategy.

Gain a strategic advantage with our focused PESTLE Analysis of GR Infraprojects—uncover how political shifts, economic cycles, regulatory pressures, and technological trends could affect project pipelines and margins; buy the full report to access actionable insights, risk scenarios, and ready-to-use slides for investors and strategists.

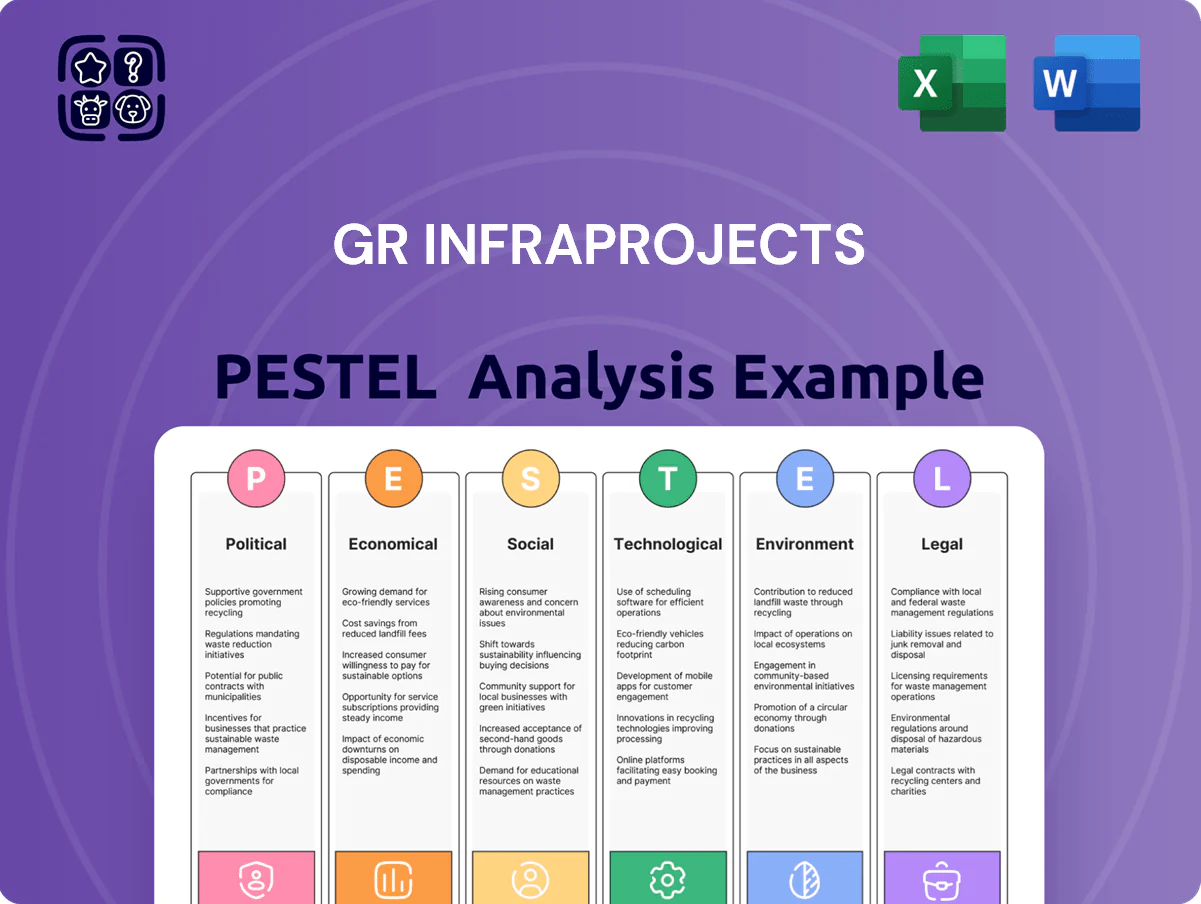

Political factors

Government Infrastructure Spending Focus

The Indian government’s PM Gati Shakti plan and Bharatmala Pariyojana drive capex of over ₹100 trillion by 2026–27, creating a steady pipeline of high-value road projects; for GR Infraprojects this translates into multi-year order book visibility, with road sector allocations rising ~12% YoY in 2024–25 and central outlays supporting expected revenue stability through 2026.

Policy Stability and Regulatory Reforms

The continuity of the current administration supports policy stability, benefiting large EPC players like GR Infraprojects as public capex rose 12% to Rs 9.4 trillion in FY2024, boosting tender pipelines.

Streamlined approvals and digital governance (e-procurement adoption up ~28% in 2023–24) have cut bidding-to-award times, reducing start-up delays and working capital drag.

This political stability lets GR Infraprojects plan capital allocation with lower policy-reversal risk, aiding its FY2025 order-book targeting and debt management strategies.

Geopolitical Influence on Supply Chains

Global political tensions and shifting trade alliances have pushed steel prices up ~15% YoY in 2024 and bitumen prices surged ~22% between 2023–24, directly raising input costs for GR Infraprojects’ EPC projects.

Import duties and tighter trade policies on construction equipment—tariffs rising in key markets to 5–12% in 2024—compress project margins and extend procurement lead times.

GR Infraprojects must hedge procurement, diversify suppliers across India, Middle East and SE Asia, and use long-term contracts to protect its integrated EPC margins against volatile geopolitics.

State-Level Political Dynamics

- Execution depends on state politics despite favorable central policy

- Land acquisition support varies by state, affecting timelines

- As of FY2024 GR Infra operates in 12 states to mitigate localization risk

Public-Private Partnership Initiatives

Government push for Public-Private Partnerships, especially via the Hybrid Annuity Model, has increased bids awarded to private players; HAM accounted for ~35% of central road awards in FY2024-25, boosting opportunities for GR Infraprojects.

Political backing for private participation in public assets enables GR Infraprojects to pursue larger, capital-intensive projects, supporting its order book of ~INR 112.5 billion as of Sep 2025.

The state-private collaboration remains central to GR Infraprojects’ growth strategy, driving higher-margin EPC-HAM mix and faster execution cycles through shared risk models.

- HAM share ~35% of central road awards FY24-25

- GR Infraprojects order book ~INR 112.5 bn (Sep 2025)

- Enables larger, capital-intensive EPC projects

GR Infraprojects: Strong FY24 capex & INR112.5bn orderbook; HAM bids boost margins

Stable central policies (PM Gati Shakti, Bharatmala) and 12% public capex growth in FY2024 support GR Infraprojects’ multi-year order book (~INR 112.5 bn Sep 2025) and HAM-led higher-margin bids (~35% of central road awards FY24‑25); state-level political variance and land-acquisition delays persist, with operations across 12 states mitigating concentration (38% SBW order-book in south/west).

| Metric | Value |

|---|---|

| Order book (Sep 2025) | INR 112.5 bn |

| HAM share (FY24‑25) | ~35% |

| Public capex growth (FY2024) | +12% |

| States of operation (FY2024) | 12 |

| Regional concentration | 38% south/west |

What is included in the product

Explores how external macro-environmental factors uniquely affect GR Infraprojects across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify threats, opportunities, and scenario-driven strategic insights tailored for executives, investors, and advisors.

A concise, visually segmented PESTLE snapshot of GR Infraprojects that’s ready to drop into presentations, easily shared across teams, and editable for region- or project-specific notes to streamline risk discussions and strategic planning.

Economic factors

Interest Rate Volatility

The cost of borrowing remains critical for capital-intensive GR Infraprojects; India’s repo rate climbed to 6.50% by Dec 2024 from 4.00% in 2021, lifting average corporate borrowing costs and project yields. Fluctuations in RBI policy directly affect financing of new projects and servicing of ~₹10,200 crore net debt reported in FY2023–24, increasing interest burden. GR Infra actively monitors rate movements to optimize tenor mix, fixed vs floating exposure and maintain liquidity covenants.

Input Cost Inflation

Rising input costs—cement up ~12% and rebar/steel up ~18% YoY in India (2024–25), plus diesel averaging ~80–90 INR/liter—compress margins on fixed-price EPC contracts for GR Infraprojects, which reported EBITDA margin pressure in FY2024. Economic cycles pushing global iron ore and energy prices mandate stronger procurement, hedging, and price-escalation clauses to protect margins. Managing inflation through 2026 is critical to preserve cashflow and debt-service capacity.

National Infrastructure Pipeline Momentum

The National Infrastructure Pipeline, mobilizing ~INR 111 trillion (2020–25) and extended targets pushing investments toward INR 130–150 trillion by 2025–26, is a primary demand driver for construction; as India targets 6–7%+ GDP growth, demand for efficient logistics and transport networks remains robust. This momentum supports GR Infraprojects’ expansion across roads, railways and power transmission, underpinning order-book growth and revenue visibility.

Hybrid Annuity Model Viability

The Hybrid Annuity Model (HAM) boosted bankability by sharing 40–60% risk with the government, lowering developers equity needs; GR Infraprojects can pursue ₹2,000–4,000 crore projects leveraging execution strength while cutting upfront equity by ~30–40% versus EPC-only bids.

Ongoing refinements—faster bid timelines and enhanced milestone payments—help sustain sector investment, with HAM projects accounting for ~25% of central road awards in 2024–25.

- HAM shares 40–60% risk with government

- Equity requirement reduced ~30–40% vs EPC

- GR can target ₹2,000–4,000 crore projects

- HAM ≈25% of central road awards in 2024–25

Credit Availability and Debt Markets

Access to competitive financing from banks and domestic institutional investors is critical for GR Infraprojects to bid on large EPC and HAM projects; India's bank credit growth was 12.8% YoY in Dec 2025 and corporate bond outstanding reached Rs 47.6 trillion in FY2024, affecting liquidity available for infrastructure developers.

GR Infraprojects maintains investment-grade ratings (CRISIL AA-/Stable as of 2025) to ensure access to term loans and bond markets for its diversified Rs ~30,000 crore orderbook and ongoing capex needs.

- Bank credit growth 12.8% YoY (Dec 2025)

- Corporate bond market Rs 47.6 trillion (FY2024)

- GR Infra rating CRISIL AA-/Stable (2025)

- Orderbook ~Rs 30,000 crore (2025)

Higher rates, input inflation squeeze EPC margins despite robust NIP funding and credit growth

Higher rates (repo 6.50% Dec 2024) raise interest costs against ~₹10,200cr net debt (FY24); input inflation (cement +12%, steel +18% YoY 2024–25) compresses EPC margins; NIP funding (~₹130–150tn by 2025–26) and HAM share (~25% awards 2024–25) support order inflows; bank credit growth 12.8% (Dec 2025) and corporate bond market ₹47.6tn (FY24) sustain financing access.

| Metric | Value |

|---|---|

| Repo rate (Dec 2024) | 6.50% |

| Net debt (FY24) | ₹10,200cr |

| Cement/Steel YoY (24–25) | +12% / +18% |

| NIP (2025–26) | ₹130–150tn |

| Bank credit growth (Dec 2025) | 12.8% |

Preview Before You Purchase

GR Infraprojects PESTLE Analysis

The preview shown here is the exact GR Infraprojects PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Gain a strategic advantage with our focused PESTLE Analysis of GR Infraprojects—uncover how political shifts, economic cycles, regulatory pressures, and technological trends could affect project pipelines and margins; buy the full report to access actionable insights, risk scenarios, and ready-to-use slides for investors and strategists.

Political factors

Government Infrastructure Spending Focus

The Indian government’s PM Gati Shakti plan and Bharatmala Pariyojana drive capex of over ₹100 trillion by 2026–27, creating a steady pipeline of high-value road projects; for GR Infraprojects this translates into multi-year order book visibility, with road sector allocations rising ~12% YoY in 2024–25 and central outlays supporting expected revenue stability through 2026.

Policy Stability and Regulatory Reforms

The continuity of the current administration supports policy stability, benefiting large EPC players like GR Infraprojects as public capex rose 12% to Rs 9.4 trillion in FY2024, boosting tender pipelines.

Streamlined approvals and digital governance (e-procurement adoption up ~28% in 2023–24) have cut bidding-to-award times, reducing start-up delays and working capital drag.

This political stability lets GR Infraprojects plan capital allocation with lower policy-reversal risk, aiding its FY2025 order-book targeting and debt management strategies.

Geopolitical Influence on Supply Chains

Global political tensions and shifting trade alliances have pushed steel prices up ~15% YoY in 2024 and bitumen prices surged ~22% between 2023–24, directly raising input costs for GR Infraprojects’ EPC projects.

Import duties and tighter trade policies on construction equipment—tariffs rising in key markets to 5–12% in 2024—compress project margins and extend procurement lead times.

GR Infraprojects must hedge procurement, diversify suppliers across India, Middle East and SE Asia, and use long-term contracts to protect its integrated EPC margins against volatile geopolitics.

State-Level Political Dynamics

- Execution depends on state politics despite favorable central policy

- Land acquisition support varies by state, affecting timelines

- As of FY2024 GR Infra operates in 12 states to mitigate localization risk

Public-Private Partnership Initiatives

Government push for Public-Private Partnerships, especially via the Hybrid Annuity Model, has increased bids awarded to private players; HAM accounted for ~35% of central road awards in FY2024-25, boosting opportunities for GR Infraprojects.

Political backing for private participation in public assets enables GR Infraprojects to pursue larger, capital-intensive projects, supporting its order book of ~INR 112.5 billion as of Sep 2025.

The state-private collaboration remains central to GR Infraprojects’ growth strategy, driving higher-margin EPC-HAM mix and faster execution cycles through shared risk models.

- HAM share ~35% of central road awards FY24-25

- GR Infraprojects order book ~INR 112.5 bn (Sep 2025)

- Enables larger, capital-intensive EPC projects

GR Infraprojects: Strong FY24 capex & INR112.5bn orderbook; HAM bids boost margins

Stable central policies (PM Gati Shakti, Bharatmala) and 12% public capex growth in FY2024 support GR Infraprojects’ multi-year order book (~INR 112.5 bn Sep 2025) and HAM-led higher-margin bids (~35% of central road awards FY24‑25); state-level political variance and land-acquisition delays persist, with operations across 12 states mitigating concentration (38% SBW order-book in south/west).

| Metric | Value |

|---|---|

| Order book (Sep 2025) | INR 112.5 bn |

| HAM share (FY24‑25) | ~35% |

| Public capex growth (FY2024) | +12% |

| States of operation (FY2024) | 12 |

| Regional concentration | 38% south/west |

What is included in the product

Explores how external macro-environmental factors uniquely affect GR Infraprojects across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and trends to identify threats, opportunities, and scenario-driven strategic insights tailored for executives, investors, and advisors.

A concise, visually segmented PESTLE snapshot of GR Infraprojects that’s ready to drop into presentations, easily shared across teams, and editable for region- or project-specific notes to streamline risk discussions and strategic planning.

Economic factors

Interest Rate Volatility

The cost of borrowing remains critical for capital-intensive GR Infraprojects; India’s repo rate climbed to 6.50% by Dec 2024 from 4.00% in 2021, lifting average corporate borrowing costs and project yields. Fluctuations in RBI policy directly affect financing of new projects and servicing of ~₹10,200 crore net debt reported in FY2023–24, increasing interest burden. GR Infra actively monitors rate movements to optimize tenor mix, fixed vs floating exposure and maintain liquidity covenants.

Input Cost Inflation

Rising input costs—cement up ~12% and rebar/steel up ~18% YoY in India (2024–25), plus diesel averaging ~80–90 INR/liter—compress margins on fixed-price EPC contracts for GR Infraprojects, which reported EBITDA margin pressure in FY2024. Economic cycles pushing global iron ore and energy prices mandate stronger procurement, hedging, and price-escalation clauses to protect margins. Managing inflation through 2026 is critical to preserve cashflow and debt-service capacity.

National Infrastructure Pipeline Momentum

The National Infrastructure Pipeline, mobilizing ~INR 111 trillion (2020–25) and extended targets pushing investments toward INR 130–150 trillion by 2025–26, is a primary demand driver for construction; as India targets 6–7%+ GDP growth, demand for efficient logistics and transport networks remains robust. This momentum supports GR Infraprojects’ expansion across roads, railways and power transmission, underpinning order-book growth and revenue visibility.

Hybrid Annuity Model Viability

The Hybrid Annuity Model (HAM) boosted bankability by sharing 40–60% risk with the government, lowering developers equity needs; GR Infraprojects can pursue ₹2,000–4,000 crore projects leveraging execution strength while cutting upfront equity by ~30–40% versus EPC-only bids.

Ongoing refinements—faster bid timelines and enhanced milestone payments—help sustain sector investment, with HAM projects accounting for ~25% of central road awards in 2024–25.

- HAM shares 40–60% risk with government

- Equity requirement reduced ~30–40% vs EPC

- GR can target ₹2,000–4,000 crore projects

- HAM ≈25% of central road awards in 2024–25

Credit Availability and Debt Markets

Access to competitive financing from banks and domestic institutional investors is critical for GR Infraprojects to bid on large EPC and HAM projects; India's bank credit growth was 12.8% YoY in Dec 2025 and corporate bond outstanding reached Rs 47.6 trillion in FY2024, affecting liquidity available for infrastructure developers.

GR Infraprojects maintains investment-grade ratings (CRISIL AA-/Stable as of 2025) to ensure access to term loans and bond markets for its diversified Rs ~30,000 crore orderbook and ongoing capex needs.

- Bank credit growth 12.8% YoY (Dec 2025)

- Corporate bond market Rs 47.6 trillion (FY2024)

- GR Infra rating CRISIL AA-/Stable (2025)

- Orderbook ~Rs 30,000 crore (2025)

Higher rates, input inflation squeeze EPC margins despite robust NIP funding and credit growth

Higher rates (repo 6.50% Dec 2024) raise interest costs against ~₹10,200cr net debt (FY24); input inflation (cement +12%, steel +18% YoY 2024–25) compresses EPC margins; NIP funding (~₹130–150tn by 2025–26) and HAM share (~25% awards 2024–25) support order inflows; bank credit growth 12.8% (Dec 2025) and corporate bond market ₹47.6tn (FY24) sustain financing access.

| Metric | Value |

|---|---|

| Repo rate (Dec 2024) | 6.50% |

| Net debt (FY24) | ₹10,200cr |

| Cement/Steel YoY (24–25) | +12% / +18% |

| NIP (2025–26) | ₹130–150tn |

| Bank credit growth (Dec 2025) | 12.8% |

Preview Before You Purchase

GR Infraprojects PESTLE Analysis

The preview shown here is the exact GR Infraprojects PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decision-making.