Banque Centrale Populaire Boston Consulting Group Matrix

See the Bigger Picture

Quickly assess Banque Centrale Populaire’s portfolio dynamics with our concise BCG Matrix preview—spot high-growth Stars, stable Cash Cows, underperforming Dogs, and tactical Question Marks to inform swift decisions. This snapshot highlights market share and growth signals but the full BCG Matrix delivers quadrant-by-quadrant placements, actionable recommendations, and ready-to-use Word and Excel files. Purchase the complete report for a data-driven roadmap to optimize capital allocation and sharpen your strategic advantage.

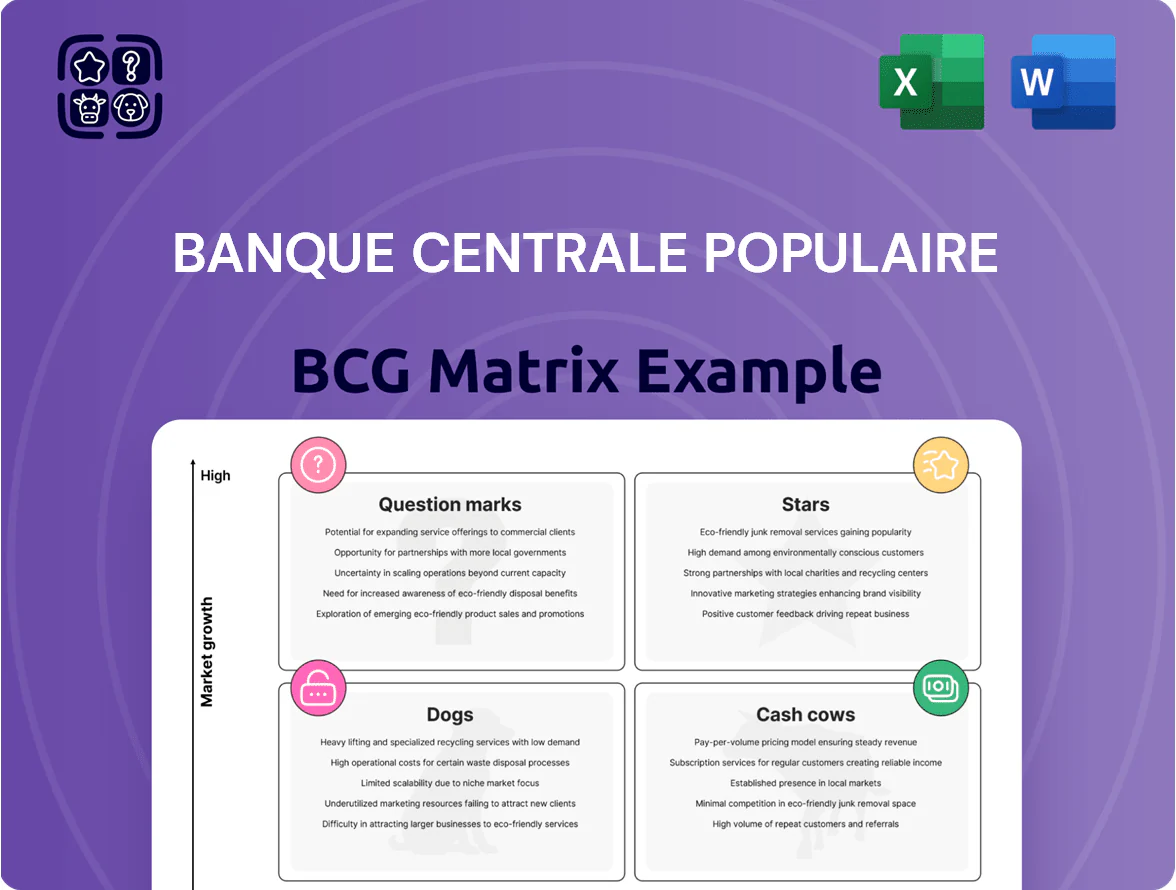

Stars

Digital Banking and Fintech Solutions

As of late 2025 Banque Centrale Populaire (BCP) accelerated digital transformation to capture Morocco’s fintech surge, reporting 27% year-on-year growth in mobile users and 31% growth in digital payments in 2025, lifting digital customers to 4.2 million.

Double-digit adoption owed to national financial-inclusion drives; digital channels now account for 42% of retail transactions, lowering branch costs and increasing fee income mix by 9 percentage points.

Continued expansion needs heavy capex: BCP budgeted MAD 1.1 billion (≈USD 110m) for cybersecurity and AI personalization in 2025, crucial to protect scale and enable targeted cross-sell.

These platforms position BCP as a Star in the BCG matrix—high market growth and strong share—supporting a shift of legacy clients into a lower-cost, higher-growth digital ecosystem.

Sub-Saharan African Expansion

BCP’s footprint across 16+ African countries via subsidiaries like Banque Atlantique makes it a Star in the BCG matrix, driving faster growth than Morocco; WAEMU markets show double-digit loan growth in recent years.

These operations now account for ~25% of group net banking income (2024), though regional expansion demands high capital for integration and compliance.

BCP continues heavy investment to secure top-tier continental status, allocating significant capex and equity to sustain growth.

Investment Banking and Market Activities

The Corporate and Investment Banking division is a star, with market activities income up >40% in 2024 and continuing strong through 2025, driving CIB to ~18% of group revenues by Q4 2025.

BCP holds leading market share in Moroccan infrastructure financing and sovereign debt management, financing ~MAD 28bn in national projects in 2024–25.

The segment benefits from higher rates and a growing pipeline of PPPs and energy projects; ROE for CIB rose to ~14% in 2025.

Ongoing capital allocation is required to sustain competitive trading desks and advisory teams amid rising regulatory and technological costs.

SME and Artisan Financing

BCP holds Morocco’s largest SME market share, aligning with the 2025 national plan; SME loans grew ~12% YoY to MAD 28.5bn in 2024, fueling high-growth potential within the SME and artisan segment.

BCP rolled out risk-sharing programs and specialized credit lines—co-lending and partial guarantee schemes—boosting SME approvals by 18% in 2024 but requiring intensive promotion and placement to control NPLs.

These offerings are core to the Excelling plan, targeting conversion of SMEs into corporate clients and aiming to raise SME lifetime value by 30% by 2027.

- SME loans MAD 28.5bn (2024)

- Loan growth ~12% YoY (2024)

- Approvals +18% via risk-share

- Target: +30% SME LTV by 2027

Sustainable and Green Finance

BCP leads Morocco’s green finance, issuing the country’s first sizable green bonds and financing 1.2 GW of renewables to date, securing a dominant market share in a fast-growing niche tied to Morocco’s 2030 climate targets.

The bank signed multi-million dollar deals—over $250m since 2020—with the World Bank Group and AfDB to fund sustainable agriculture and green energy projects nationwide.

Regulatory shifts toward ESG mean BCP must invest roughly $30–40m in staffing, compliance systems, and product R&D to scale; this unit is capital-intensive but high-growth.

BCP’s early-mover edge makes it the preferred lender for Morocco’s energy transition, positioning it to capture major upcoming project finance opportunities through 2030.

- Issued green bonds funding 1.2 GW renewables

- $250m+ in development-agency agreements since 2020

- Estimated $30–40m required for ESG buildout

- Early-mover, dominant share in a high-growth niche

BCP fuels growth: 4.2M digital users, 18% CIB share, MAD28.5bn SME, 1.2GW green

BCP’s digital, CIB, SME, and green-finance units are Stars: 2025 digital users 4.2M (+27% YoY), digital transactions 42% of retail, CIB ≈18% group revenue (ROE ~14%), SME loans MAD 28.5bn (+12% YoY), green financing 1.2GW; capex 2025 ≈MAD 1.1bn, ESG buildout $30–40m.

| Metric | Value |

|---|---|

| Digital users | 4.2M |

| CIB rev share | 18% |

| SME loans | MAD 28.5bn |

| Green GW | 1.2 |

What is included in the product

BCP BCG Matrix: strategic placement of business units with investment, hold, or divest recommendations per quadrant, plus trend-driven risks and advantages.

One-page BCG Matrix mapping Banque Centrale Populaire units into quadrants for quick strategic clarity and decision-making

Cash Cows

Traditional Retail Banking

BCP’s traditional retail banking is its cash cow, holding Morocco’s largest deposit base at MAD 420 billion as of Dec 31, 2025 and delivering steady net interest margins. The mature network posts high efficiency—cost-to-income near 41% in Q1 2025—so the bank focuses on milking revenue via service optimization, not costly expansion. Cash flows fund the group’s international push and digital investments, supporting ~MAD 6.5 billion in capex in 2025.

Regional Popular Banks (BPR)

The decentralized Regional Popular Banks (BPR) give Banque Centrale Populaire a dominant local share—about 45% of provincial deposits and 38% of consumer credit nationwide in 2024—operating in low-growth, high-loyalty markets that generate steady liquidity for the central group.

These mature units need only upkeep capex: physical branches plus modest digital upgrades (≈MAD 450m in 2024) to lift efficiency and service, not heavy expansion spend.

BPRs are the cooperative backbone, delivering predictable dividends and funding—roughly 30% of group distributable cash in 2024—supporting balance-sheet stability.

Bancassurance Services

BCP’s bancassurance, run with major insurers, captures roughly 35–40% of Morocco’s basic life and health premiums by using 1,900+ branches to cross-sell, producing steady commission margins near 25% and ROE-like cash yields above 15% in 2024.

Institutional Asset Management

BCP Asset Management controls roughly 30% of Morocco’s mutual fund market and manages about MAD 45 billion (≈USD 4.4 billion) in institutional mandates as of 2025, producing steady management fees from a mature, loyal client base.

Low operating leverage and minimal capital expenditure mean high cash conversion; profits can be redeployed to digital banking and lending or used for debt servicing, supporting group liquidity.

It anchors the group by offsetting volatility from growth units and contributing predictable revenue during market cycles.

- ~30% market share

- MAD 45bn AUM (2025)

- High margin, low capex

- Supports debt service and reinvestment

Remittance Services for Moroccans Living Abroad (MDM)

BCP (Banque Centrale Populaire) holds a near-monopoly on remittances from the Moroccan diaspora in Europe, delivering steady, low-marketing inflows that required minimal incremental spend in 2024—remittances to Morocco totaled about USD 9.2bn in 2024, with BCP estimated to handle ~35–40% of Europe-origin flows.

The Chaabi Bank European network provides a low-cost acquisition funnel, supplying predictable foreign-currency liquidity that supports BCP group liquidity ratios and funds trade finance lines without heavy capital allocation.

- 2024 Morocco remittances ~USD 9.2bn

- BCP share (Europe) est. 35–40%

- Low marketing spend; mature segment

- Supports liquidity ratios and trade finance

BCP’s high‑margin cash cows fund capex and debt—MAD420bn deposits, USD9.2bn remittances

BCP’s cash cows—retail banking, BPRs, bancassurance, asset management, and remittances—produce steady high-margin cash flows (MAD 420bn deposits; MAD 45bn AUM; bancassurance ROE-like yields >15%; remittances USD 9.2bn with BCP ~35–40%), funding capex (~MAD 6.5bn in 2025) and debt service while requiring low upkeep capex.

| Metric | Value (2024–25) |

|---|---|

| Deposits | MAD 420bn (2025) |

| AUM | MAD 45bn (2025) |

| Remittances (Morocco) | USD 9.2bn (2024) |

| Capex | MAD 6.5bn (2025) |

Preview = Final Product

Banque Centrale Populaire BCG Matrix

The file you're previewing is the exact Banque Centrale Populaire BCG Matrix report you'll receive after purchase—no watermarks, no demo pages—just the fully formatted, analysis-ready document designed for strategic clarity and professional presentation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

Quickly assess Banque Centrale Populaire’s portfolio dynamics with our concise BCG Matrix preview—spot high-growth Stars, stable Cash Cows, underperforming Dogs, and tactical Question Marks to inform swift decisions. This snapshot highlights market share and growth signals but the full BCG Matrix delivers quadrant-by-quadrant placements, actionable recommendations, and ready-to-use Word and Excel files. Purchase the complete report for a data-driven roadmap to optimize capital allocation and sharpen your strategic advantage.

Stars

Digital Banking and Fintech Solutions

As of late 2025 Banque Centrale Populaire (BCP) accelerated digital transformation to capture Morocco’s fintech surge, reporting 27% year-on-year growth in mobile users and 31% growth in digital payments in 2025, lifting digital customers to 4.2 million.

Double-digit adoption owed to national financial-inclusion drives; digital channels now account for 42% of retail transactions, lowering branch costs and increasing fee income mix by 9 percentage points.

Continued expansion needs heavy capex: BCP budgeted MAD 1.1 billion (≈USD 110m) for cybersecurity and AI personalization in 2025, crucial to protect scale and enable targeted cross-sell.

These platforms position BCP as a Star in the BCG matrix—high market growth and strong share—supporting a shift of legacy clients into a lower-cost, higher-growth digital ecosystem.

Sub-Saharan African Expansion

BCP’s footprint across 16+ African countries via subsidiaries like Banque Atlantique makes it a Star in the BCG matrix, driving faster growth than Morocco; WAEMU markets show double-digit loan growth in recent years.

These operations now account for ~25% of group net banking income (2024), though regional expansion demands high capital for integration and compliance.

BCP continues heavy investment to secure top-tier continental status, allocating significant capex and equity to sustain growth.

Investment Banking and Market Activities

The Corporate and Investment Banking division is a star, with market activities income up >40% in 2024 and continuing strong through 2025, driving CIB to ~18% of group revenues by Q4 2025.

BCP holds leading market share in Moroccan infrastructure financing and sovereign debt management, financing ~MAD 28bn in national projects in 2024–25.

The segment benefits from higher rates and a growing pipeline of PPPs and energy projects; ROE for CIB rose to ~14% in 2025.

Ongoing capital allocation is required to sustain competitive trading desks and advisory teams amid rising regulatory and technological costs.

SME and Artisan Financing

BCP holds Morocco’s largest SME market share, aligning with the 2025 national plan; SME loans grew ~12% YoY to MAD 28.5bn in 2024, fueling high-growth potential within the SME and artisan segment.

BCP rolled out risk-sharing programs and specialized credit lines—co-lending and partial guarantee schemes—boosting SME approvals by 18% in 2024 but requiring intensive promotion and placement to control NPLs.

These offerings are core to the Excelling plan, targeting conversion of SMEs into corporate clients and aiming to raise SME lifetime value by 30% by 2027.

- SME loans MAD 28.5bn (2024)

- Loan growth ~12% YoY (2024)

- Approvals +18% via risk-share

- Target: +30% SME LTV by 2027

Sustainable and Green Finance

BCP leads Morocco’s green finance, issuing the country’s first sizable green bonds and financing 1.2 GW of renewables to date, securing a dominant market share in a fast-growing niche tied to Morocco’s 2030 climate targets.

The bank signed multi-million dollar deals—over $250m since 2020—with the World Bank Group and AfDB to fund sustainable agriculture and green energy projects nationwide.

Regulatory shifts toward ESG mean BCP must invest roughly $30–40m in staffing, compliance systems, and product R&D to scale; this unit is capital-intensive but high-growth.

BCP’s early-mover edge makes it the preferred lender for Morocco’s energy transition, positioning it to capture major upcoming project finance opportunities through 2030.

- Issued green bonds funding 1.2 GW renewables

- $250m+ in development-agency agreements since 2020

- Estimated $30–40m required for ESG buildout

- Early-mover, dominant share in a high-growth niche

BCP fuels growth: 4.2M digital users, 18% CIB share, MAD28.5bn SME, 1.2GW green

BCP’s digital, CIB, SME, and green-finance units are Stars: 2025 digital users 4.2M (+27% YoY), digital transactions 42% of retail, CIB ≈18% group revenue (ROE ~14%), SME loans MAD 28.5bn (+12% YoY), green financing 1.2GW; capex 2025 ≈MAD 1.1bn, ESG buildout $30–40m.

| Metric | Value |

|---|---|

| Digital users | 4.2M |

| CIB rev share | 18% |

| SME loans | MAD 28.5bn |

| Green GW | 1.2 |

What is included in the product

BCP BCG Matrix: strategic placement of business units with investment, hold, or divest recommendations per quadrant, plus trend-driven risks and advantages.

One-page BCG Matrix mapping Banque Centrale Populaire units into quadrants for quick strategic clarity and decision-making

Cash Cows

Traditional Retail Banking

BCP’s traditional retail banking is its cash cow, holding Morocco’s largest deposit base at MAD 420 billion as of Dec 31, 2025 and delivering steady net interest margins. The mature network posts high efficiency—cost-to-income near 41% in Q1 2025—so the bank focuses on milking revenue via service optimization, not costly expansion. Cash flows fund the group’s international push and digital investments, supporting ~MAD 6.5 billion in capex in 2025.

Regional Popular Banks (BPR)

The decentralized Regional Popular Banks (BPR) give Banque Centrale Populaire a dominant local share—about 45% of provincial deposits and 38% of consumer credit nationwide in 2024—operating in low-growth, high-loyalty markets that generate steady liquidity for the central group.

These mature units need only upkeep capex: physical branches plus modest digital upgrades (≈MAD 450m in 2024) to lift efficiency and service, not heavy expansion spend.

BPRs are the cooperative backbone, delivering predictable dividends and funding—roughly 30% of group distributable cash in 2024—supporting balance-sheet stability.

Bancassurance Services

BCP’s bancassurance, run with major insurers, captures roughly 35–40% of Morocco’s basic life and health premiums by using 1,900+ branches to cross-sell, producing steady commission margins near 25% and ROE-like cash yields above 15% in 2024.

Institutional Asset Management

BCP Asset Management controls roughly 30% of Morocco’s mutual fund market and manages about MAD 45 billion (≈USD 4.4 billion) in institutional mandates as of 2025, producing steady management fees from a mature, loyal client base.

Low operating leverage and minimal capital expenditure mean high cash conversion; profits can be redeployed to digital banking and lending or used for debt servicing, supporting group liquidity.

It anchors the group by offsetting volatility from growth units and contributing predictable revenue during market cycles.

- ~30% market share

- MAD 45bn AUM (2025)

- High margin, low capex

- Supports debt service and reinvestment

Remittance Services for Moroccans Living Abroad (MDM)

BCP (Banque Centrale Populaire) holds a near-monopoly on remittances from the Moroccan diaspora in Europe, delivering steady, low-marketing inflows that required minimal incremental spend in 2024—remittances to Morocco totaled about USD 9.2bn in 2024, with BCP estimated to handle ~35–40% of Europe-origin flows.

The Chaabi Bank European network provides a low-cost acquisition funnel, supplying predictable foreign-currency liquidity that supports BCP group liquidity ratios and funds trade finance lines without heavy capital allocation.

- 2024 Morocco remittances ~USD 9.2bn

- BCP share (Europe) est. 35–40%

- Low marketing spend; mature segment

- Supports liquidity ratios and trade finance

BCP’s high‑margin cash cows fund capex and debt—MAD420bn deposits, USD9.2bn remittances

BCP’s cash cows—retail banking, BPRs, bancassurance, asset management, and remittances—produce steady high-margin cash flows (MAD 420bn deposits; MAD 45bn AUM; bancassurance ROE-like yields >15%; remittances USD 9.2bn with BCP ~35–40%), funding capex (~MAD 6.5bn in 2025) and debt service while requiring low upkeep capex.

| Metric | Value (2024–25) |

|---|---|

| Deposits | MAD 420bn (2025) |

| AUM | MAD 45bn (2025) |

| Remittances (Morocco) | USD 9.2bn (2024) |

| Capex | MAD 6.5bn (2025) |

Preview = Final Product

Banque Centrale Populaire BCG Matrix

The file you're previewing is the exact Banque Centrale Populaire BCG Matrix report you'll receive after purchase—no watermarks, no demo pages—just the fully formatted, analysis-ready document designed for strategic clarity and professional presentation.