Guillin SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

Uncover Guillin’s strategic edge and hidden risks with our full SWOT analysis—packed with market context, competitive benchmarks, and tactical recommendations to inform investment or strategic moves.

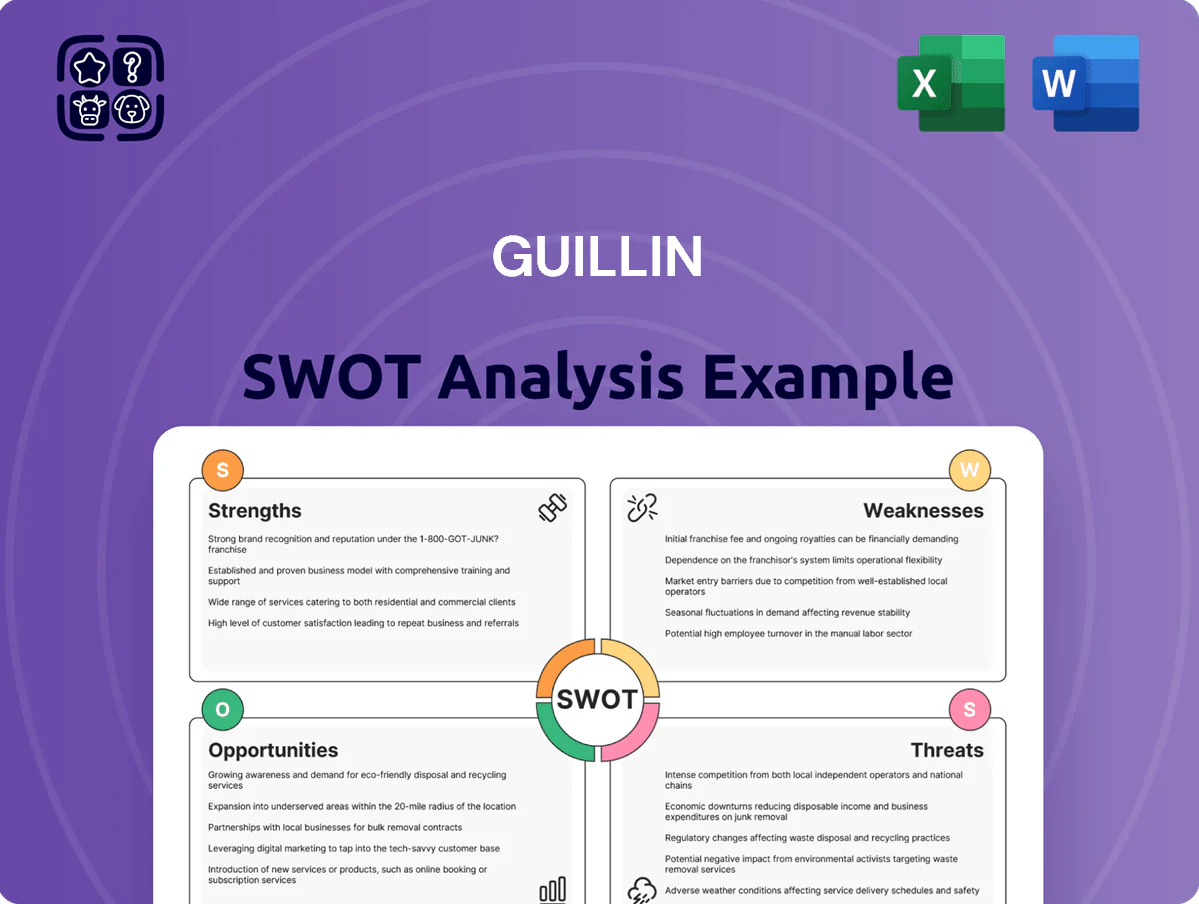

Strengths

Dominant European Market Position

Groupe Guillin holds a leading European food-packaging position via 20+ plants and a 300-strong distribution footprint across 15 countries, enabling supply to top retailers and processors with >€450m 2024 group revenue and c.12% EBITDA margin; this scale supports high-volume contracts and 98% on-time delivery, while a long track record in food safety and quality certification creates a durable moat vs smaller regional players.

Vertical Integration and Supply Control

Guillin’s vertical integration—internal sourcing and recycling—secures ~40% of its raw material needs in-house (2024), cutting exposure to PVC and resin price swings and lowering COGS by an estimated 150–200 bps versus peers.

Advanced R&D and Eco-Design

Guillin’s R&D spend reached €18.4M in FY2024, driving lightweighting that cut average container weight 12% since 2020 and raised rPET content to 35% in food-grade lines by Q4 2025; this keeps compliance with EU Packaging Waste Regulation while preserving barrier performance and cut costs per unit by ~4.6% year-over-year.

Diversified Food Industry Exposure

- Revenue mix: produce 28%, meat 22%, bakery 18%, catering 12%

- Repeat orders +9% YoY (2024)

- Diversification reduces segment volatility

Robust Financial Health

Groupe Guillin reports steady revenue and cash generation: €420m revenue and €36m EBITDA in FY2024, with net debt/EBITDA around 1.1x at year-end 2024, supporting acquisitions and capex without heavy leverage.

That balance-sheet strength funds €45m planned capex for 2025—mainly automation and PET recycling lines—while preserving liquidity to ride downturns and back long-term growth.

- FY2024 revenue €420m

- FY2024 EBITDA €36m

- Net debt/EBITDA ~1.1x (Dec 2024)

- Planned 2025 capex €45m

Guillin: €420M leader in EU food-packaging—€36M EBITDA, sustainability & growth focus

Guillin leads EU food-packaging with €420m revenue and €36m EBITDA in 2024 (net debt/EBITDA ~1.1x), 20+ plants, 300 distributors, 98% on-time delivery, ~40% vertically sourced inputs, R&D €18.4m (2024) cutting container weight 12% since 2020 and raising rPET to 35% by Q4 2025; repeat orders +9% YoY (2024).

| Metric | 2024/2025 |

|---|---|

| Revenue | €420m |

| EBITDA | €36m |

| Net debt/EBITDA | 1.1x |

| R&D | €18.4m |

| rPET (food) | 35% (Q4 2025) |

What is included in the product

Provides a concise SWOT overview of Guillin, highlighting its core strengths and weaknesses while mapping opportunities and external threats shaping the company’s strategic outlook.

Delivers a clear SWOT snapshot of Guillin for rapid strategic alignment and concise stakeholder briefings.

Weaknesses

Reliance on Plastic-Based Polymers

Guillin still makes most products from hydrocarbon-based plastic resins, leaving margins exposed to oil-price swings; Brent rose ~45% from $69 to $100/bbl in 2021–23, showing sensitivity in resin costs.

Growing anti-plastic sentiment cuts demand—global single-use plastic bans reached 60+ countries by 2024—raising reputational and regulatory risk for core lines.

Shifting the full portfolio to biopolymers or recycled feedstock needs large capex and time; an estimated industry transition capex is $200–400M for mid-size converters, affecting near-term cash flow.

Geographic Concentration in Europe

Sensitivity to Raw Material Volatility

The profitability of Guillin Group Holdings Co., Ltd. (Guillin), a major Chinese rigid plastic packaging maker, is tightly linked to virgin and recycled resin prices; HDPE and PET spot prices swung 18–30% in 2023–2024, amplifying cost risk. Vertical integration (in-house compounding and recycling) cushions exposure, but sudden resin spikes can't always be passed to buyers because ~40% of 2024 sales were under multi-year contracts. That lag caused margin compression in H1 2024, when gross margin fell ~220 basis points year-on-year.

Complexity in Multi-Material Recycling

- High-performance films harder to recycle

- EU/France regs tighten 2025—EPR fees +≈15%

- Retrofit/reformulation needs raise CAPEX

- Operational logistics remain a key barrier

Perception as a Traditional Manufacturer

- 2024 sales €1.1bn vs €45m recycling capex

- 62% EU consumers avoid plastic (2023)

- Only 8% sustainable funds hold packaging stocks (2024)

Guillin faces margin pressure from oil swings, EU exposure & costly green transition

Guillin’s margins are exposed to oil/resin swings (Brent +45% 2021–23; HDPE/PET spot moves 18–30% in 2023–24), heavy EU reliance (≈68% revenue FY2024) raises regulatory/GDP sensitivity, transition to biopolymers/recycling demands €200–400m capex for mid-size converters, and complex multi-layer products face higher EPR/waste costs (~+15%) and recycling stigma (62% EU avoid plastic, only 8% sustainable funds hold packaging).

| Metric | Value |

|---|---|

| FY2024 revenue share EU | 68% |

| Brent 2021–23 change | +45% |

| HDPE/PET spot vol | 18–30% |

| Estimated transition capex | €200–400m |

| 2024 operating margin | ~6% |

| EPR/waste cost rise (complex) | ≈+15% |

| EU consumers avoiding plastic | 62% |

| Sustainable funds holding packaging | 8% |

Full Version Awaits

Guillin SWOT Analysis

This is the actual Guillin SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report, and the content shown is the real, editable file included in your download. Buy now to unlock the complete, detailed version immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Uncover Guillin’s strategic edge and hidden risks with our full SWOT analysis—packed with market context, competitive benchmarks, and tactical recommendations to inform investment or strategic moves.

Strengths

Dominant European Market Position

Groupe Guillin holds a leading European food-packaging position via 20+ plants and a 300-strong distribution footprint across 15 countries, enabling supply to top retailers and processors with >€450m 2024 group revenue and c.12% EBITDA margin; this scale supports high-volume contracts and 98% on-time delivery, while a long track record in food safety and quality certification creates a durable moat vs smaller regional players.

Vertical Integration and Supply Control

Guillin’s vertical integration—internal sourcing and recycling—secures ~40% of its raw material needs in-house (2024), cutting exposure to PVC and resin price swings and lowering COGS by an estimated 150–200 bps versus peers.

Advanced R&D and Eco-Design

Guillin’s R&D spend reached €18.4M in FY2024, driving lightweighting that cut average container weight 12% since 2020 and raised rPET content to 35% in food-grade lines by Q4 2025; this keeps compliance with EU Packaging Waste Regulation while preserving barrier performance and cut costs per unit by ~4.6% year-over-year.

Diversified Food Industry Exposure

- Revenue mix: produce 28%, meat 22%, bakery 18%, catering 12%

- Repeat orders +9% YoY (2024)

- Diversification reduces segment volatility

Robust Financial Health

Groupe Guillin reports steady revenue and cash generation: €420m revenue and €36m EBITDA in FY2024, with net debt/EBITDA around 1.1x at year-end 2024, supporting acquisitions and capex without heavy leverage.

That balance-sheet strength funds €45m planned capex for 2025—mainly automation and PET recycling lines—while preserving liquidity to ride downturns and back long-term growth.

- FY2024 revenue €420m

- FY2024 EBITDA €36m

- Net debt/EBITDA ~1.1x (Dec 2024)

- Planned 2025 capex €45m

Guillin: €420M leader in EU food-packaging—€36M EBITDA, sustainability & growth focus

Guillin leads EU food-packaging with €420m revenue and €36m EBITDA in 2024 (net debt/EBITDA ~1.1x), 20+ plants, 300 distributors, 98% on-time delivery, ~40% vertically sourced inputs, R&D €18.4m (2024) cutting container weight 12% since 2020 and raising rPET to 35% by Q4 2025; repeat orders +9% YoY (2024).

| Metric | 2024/2025 |

|---|---|

| Revenue | €420m |

| EBITDA | €36m |

| Net debt/EBITDA | 1.1x |

| R&D | €18.4m |

| rPET (food) | 35% (Q4 2025) |

What is included in the product

Provides a concise SWOT overview of Guillin, highlighting its core strengths and weaknesses while mapping opportunities and external threats shaping the company’s strategic outlook.

Delivers a clear SWOT snapshot of Guillin for rapid strategic alignment and concise stakeholder briefings.

Weaknesses

Reliance on Plastic-Based Polymers

Guillin still makes most products from hydrocarbon-based plastic resins, leaving margins exposed to oil-price swings; Brent rose ~45% from $69 to $100/bbl in 2021–23, showing sensitivity in resin costs.

Growing anti-plastic sentiment cuts demand—global single-use plastic bans reached 60+ countries by 2024—raising reputational and regulatory risk for core lines.

Shifting the full portfolio to biopolymers or recycled feedstock needs large capex and time; an estimated industry transition capex is $200–400M for mid-size converters, affecting near-term cash flow.

Geographic Concentration in Europe

Sensitivity to Raw Material Volatility

The profitability of Guillin Group Holdings Co., Ltd. (Guillin), a major Chinese rigid plastic packaging maker, is tightly linked to virgin and recycled resin prices; HDPE and PET spot prices swung 18–30% in 2023–2024, amplifying cost risk. Vertical integration (in-house compounding and recycling) cushions exposure, but sudden resin spikes can't always be passed to buyers because ~40% of 2024 sales were under multi-year contracts. That lag caused margin compression in H1 2024, when gross margin fell ~220 basis points year-on-year.

Complexity in Multi-Material Recycling

- High-performance films harder to recycle

- EU/France regs tighten 2025—EPR fees +≈15%

- Retrofit/reformulation needs raise CAPEX

- Operational logistics remain a key barrier

Perception as a Traditional Manufacturer

- 2024 sales €1.1bn vs €45m recycling capex

- 62% EU consumers avoid plastic (2023)

- Only 8% sustainable funds hold packaging stocks (2024)

Guillin faces margin pressure from oil swings, EU exposure & costly green transition

Guillin’s margins are exposed to oil/resin swings (Brent +45% 2021–23; HDPE/PET spot moves 18–30% in 2023–24), heavy EU reliance (≈68% revenue FY2024) raises regulatory/GDP sensitivity, transition to biopolymers/recycling demands €200–400m capex for mid-size converters, and complex multi-layer products face higher EPR/waste costs (~+15%) and recycling stigma (62% EU avoid plastic, only 8% sustainable funds hold packaging).

| Metric | Value |

|---|---|

| FY2024 revenue share EU | 68% |

| Brent 2021–23 change | +45% |

| HDPE/PET spot vol | 18–30% |

| Estimated transition capex | €200–400m |

| 2024 operating margin | ~6% |

| EPR/waste cost rise (complex) | ≈+15% |

| EU consumers avoiding plastic | 62% |

| Sustainable funds holding packaging | 8% |

Full Version Awaits

Guillin SWOT Analysis

This is the actual Guillin SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report, and the content shown is the real, editable file included in your download. Buy now to unlock the complete, detailed version immediately after checkout.