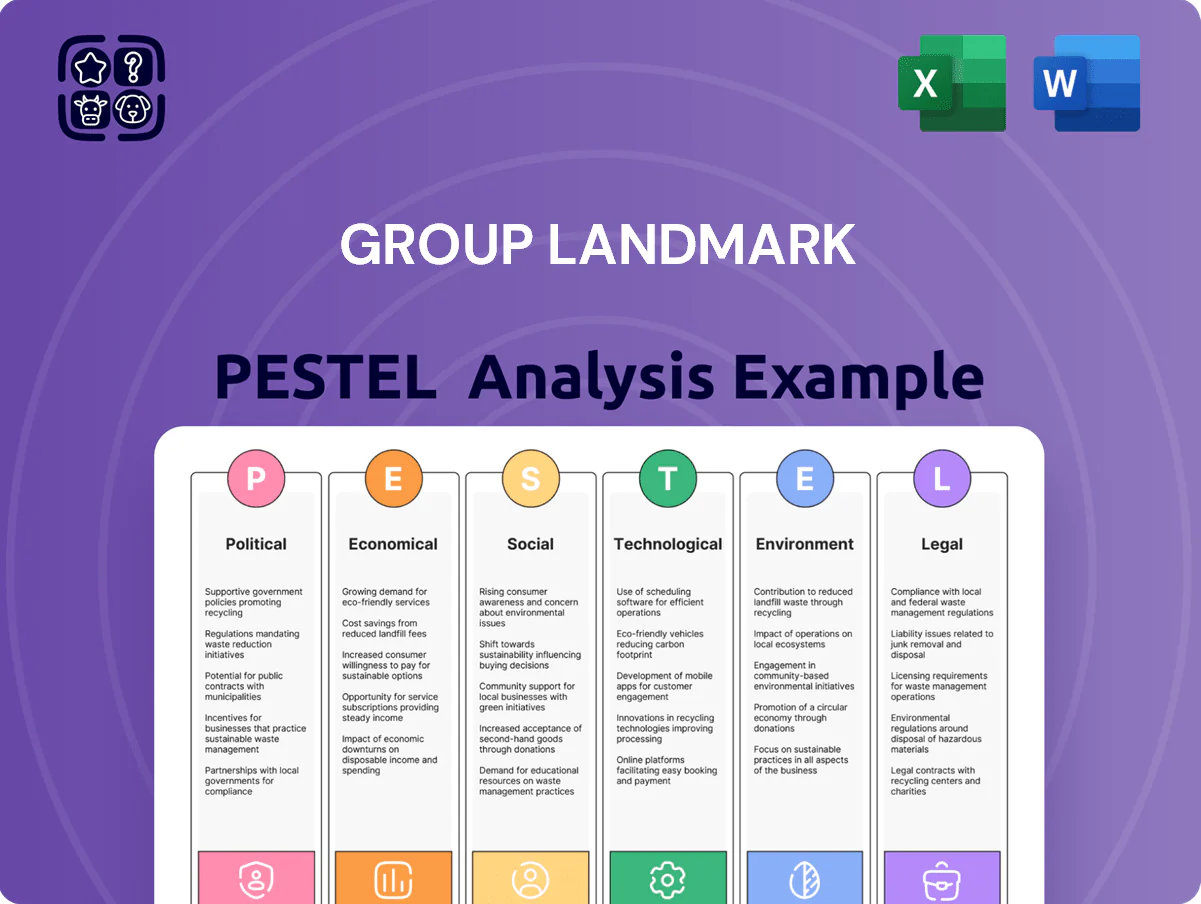

Group Landmark PESTLE Analysis

Your Competitive Advantage Starts with This Report

Gain a strategic edge with our PESTLE Analysis of Group Landmark—concise, current, and targeted to reveal the political, economic, social, technological, legal, and environmental forces shaping its future; download the full report to access granular insights, risk assessments, and actionable recommendations designed for investors, advisors, and strategists.

Political factors

Government Push for Electric Mobility

The Indian government's FAME-II and production-linked incentive (PLI) push — with FAME allocations of INR 10,000 crore through 2024–25 and PLI targets to spur 60–70% domestic EV component manufacturing by 2030 — compels Landmark to shift inventory toward BEVs and hybrids, renegotiate dealership terms with manufacturers targeting >30% EV market share by 2030, and plan capex for showroom charging networks (estimated INR 2–5 million per outlet) to meet regulatory and consumer demand.

Import Duties and Trade Policies

Fluctuations in customs duties on CKD and CBU units directly affect Landmark’s pricing for premium brands like Mercedes-Benz; a 5–10% duty change can swing retail prices by €3,000–€8,000 per vehicle based on 2024 MSRP ranges. Political moves on trade barriers or FTAs with the EU/UK could shift import cost structures, altering competitive parity with local assemblers. Analysts track tariff scenario modeling to forecast volume swings in the luxury segment, where 2024 sales concentrated 18% of group margins.

Infrastructure Development Initiatives

The rapid expansion of national highways and expressways under federal programs, with 12,000 km awarded in 2024 and a target of 25,000 km by 2025, increases demand for reliable passenger vehicles and SUVs, directly supporting Landmark’s sales pipeline.

Improved connectivity raises inter-city travel and vehicle utilization; India recorded a 9% rise in intercity trips in 2024, benefiting Landmark’s servicing and resale volumes.

Government urban infrastructure spending of $40 billion in 2024 guides feasibility for new Landmark touchpoints in Tier-2 cities, where vehicle registrations grew 7.5% year-over-year.

State-Level Taxation and Subsidies

Varying state road taxes and registration subsidies fragment India’s market: states like Maharashtra levy EV registration incentives up to INR 10,000 while Uttar Pradesh offers scrappage-linked benefits, impacting dealership margins and pricing across 28 states and 8 UTs.

Landmark must navigate regional political climates where incentives favor LPG, CNG or EVs; in 2024 EV sales share reached ~3.5% nationwide but exceeded 10% in Delhi and Kerala, altering product mix and inventory strategy.

Strategic planning needs granular tracking of state policy shifts—monthly monitoring of tax notifications and subsidy caps enabled a 7% uplift in regional sales for dealer groups in 2024.

- Fragmented taxes/subsidies across states affect pricing and margins

- Local incentives drive fuel-type demand (EVs >10% in some states)

- Monthly policy monitoring linked to a 7% regional sales improvement

- Prepare state-specific inventory and pricing strategies

Fuel Pricing and Regulatory Stability

Government control or deregulation of fuel prices directly alters TCO for ICE vehicles; a 2024 IEA report shows global gasoline retail prices varied 40-60% across major markets, affecting ownership costs and purchase cycles.

Political stability ensures consistent rollout of policies like India’s Scrappage Policy; 2024 implementation rates and incentives drive replacement cycles, reducing uncertainty for Landmark’s demand forecasts.

For Landmark’s after-sales and spare-parts divisions, policy reversals could swing demand by an estimated 8-12% annually based on 2023–2024 market elasticity studies.

- Fuel price regime alters TCO and purchase timing

- Policy stability ensures predictable scrappage-driven replacements

- Demand volatility for parts estimated 8–12% with policy shifts

- 2024 fuel price dispersion 40–60% across key markets (IEA)

Policy & duty shocks steer Landmark to EV inventory, charging capex and regional mix

Policy incentives (FAME‑II INR 10,000cr; PLI aiming 60–70% local EV components by 2030) push Landmark toward EV inventory, charging capex (~INR 2–5m/outlet) and dealer renegotiation; customs duty swings (±5–10%) alter premium pricing by €3k–€8k; state tax/incentive fragmentation (EV incentives up to INR 10k) shifts regional mix (national EV share ~3.5%, Delhi/Kerala >10%) and parts demand (policy-shock impact 8–12%).

| Metric | 2024 Value | Impact |

|---|---|---|

| FAME‑II allocation | INR 10,000cr | EV adoption/stocking |

| PLI EV target | 60–70% components by 2030 | Local sourcing, margin shifts |

| EV national share | 3.5% | Product mix |

| Delhi/Kerala EV share | >10% | Regional demand |

| Duty volatility | ±5–10% | Price swing €3–8k |

| Charging capex/outlet | INR 2–5m | Capex planning |

| Parts demand swing | 8–12% | After‑sales revenue |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Group Landmark, with each section supported by current data and regional market dynamics to identify risks and opportunities.

Condenses the full Group Landmark PESTLE into a concise, visually segmented summary for quick reference in meetings, presentations, or shared planning sessions.

Economic factors

Interest Rate Environment and Financing

The cost of auto loans is a key determinant of vehicle sales in mass-market and mid-premium segments; with RBI policy rate at 6.50% (Feb 2026) and typical retail auto loan EMI rates averaging 9–11% in 2025, financing costs materially shape demand. Landmark’s sales closely track lending-rate movements—each 100 bps rise historically trimmed monthly volumes by ~3–4%. High rates in 2022–23 depressed purchases, while the 2024–25 easing cycle (net 125 bps cuts) correlated with a 12% rebound in showroom footfall.

Rising Disposable Income and Premiumization

India’s middle class is projected at 350–400 million by 2025 and HNWIs rose 12% to ~820,000 in 2024, driving premiumization in autos; sales of SUVs and luxury cars grew ~18% in FY2024 vs passenger cars’ 6%. Landmark’s partnerships with Mercedes-Benz and Jeep position it to capture higher ASPs and margin expansion as buyers shift from functional hatchbacks to lifestyle SUVs and luxury sedans. Economic prosperity—GDP per capita rising to ~$2,600 in 2024—correlates with increased premium vehicle uptake, benefiting Landmark’s luxury-focused inventory and aftersales revenue streams.

Inflationary Pressures on Operational Costs

Rising input costs—global semiconductor shortages lifted but commodity-driven input inflation saw input price indices up ~7% YoY in 2024—force manufacturers to raise vehicle prices, which Landmark must convey to price-sensitive buyers, risking volume declines.

Landmark’s wage bills and prime showroom rents rose with UK CPI averaging 3.9% in 2024 and commercial rents up ~5% in prime locations, squeezing margins.

When macro inflation outpaces service revenue growth—aftermarket revenue growth for dealers averaged ~2–3% in 2024—maintaining profitability requires tighter cost control and selective pricing.

Used Car Market Valuation

Used-car valuations drive Landmark’s pre-owned unit: India’s organized used-car market grew to about USD 57 billion in 2024 with residual values averaging 45–60% for 3–5 year vehicles, directly influencing margins and inventory turnover.

During 2023–24 downturns, trade-ins rose ~18%, shifting buyers to secondary markets and cushioning Landmark against a ~7–10% dip in new-car volumes.

Formalization lets Landmark capture share from unorganized sellers; organized channels held ~25% of transactions in 2024, offering scale and higher gross margins.

- Residual values 45–60% (3–5 yrs)

- Organized market ~25% (2024)

- Trade-ins +18% in downturns

Currency Exchange Rate Volatility

Currency volatility impacts Landmark as the INR fell ~8% vs USD and ~6% vs EUR in 2022–2023, raising imported component costs and pressuring luxury vehicle margins.

Sharp INR depreciation in 2023–24 forced several OEMs to raise prices by 3–7%, curbing premium demand; a repeat could reduce Landmark sales in the luxury segment.

Landmark should hedge forex exposure, adjust inventory cadence, and communicate likely price shifts to customers during high volatility.

- INR moves (±5–8%) materially change landed costs

- OEM price hikes in 2023–24: ~3–7%

- Actions: hedging, tighter inventory, proactive customer communication

Higher rates squeeze volumes; premiumization and used-car strength lift margins

Higher financing costs (RBI 6.50% Feb 2026; retail auto EMI 9–11% in 2025) and input inflation (~7% YoY 2024) constrain volumes; premiumization (middle class 350–400M 2025; HNWIs ~820k in 2024) boosts SUV/luxury demand; used-car market USD57bn (2024) with residuals 45–60% supports margins; INR volatility (−8% vs USD 2022–23) raises import costs.

| Metric | Value |

|---|---|

| RBI rate | 6.50% (Feb 2026) |

| Retail EMI | 9–11% (2025) |

| Used market | USD57bn (2024) |

| Residuals | 45–60% (3–5yr) |

Preview Before You Purchase

Group Landmark PESTLE Analysis

The preview shown here is the exact Group Landmark PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use without placeholders or edits.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Gain a strategic edge with our PESTLE Analysis of Group Landmark—concise, current, and targeted to reveal the political, economic, social, technological, legal, and environmental forces shaping its future; download the full report to access granular insights, risk assessments, and actionable recommendations designed for investors, advisors, and strategists.

Political factors

Government Push for Electric Mobility

The Indian government's FAME-II and production-linked incentive (PLI) push — with FAME allocations of INR 10,000 crore through 2024–25 and PLI targets to spur 60–70% domestic EV component manufacturing by 2030 — compels Landmark to shift inventory toward BEVs and hybrids, renegotiate dealership terms with manufacturers targeting >30% EV market share by 2030, and plan capex for showroom charging networks (estimated INR 2–5 million per outlet) to meet regulatory and consumer demand.

Import Duties and Trade Policies

Fluctuations in customs duties on CKD and CBU units directly affect Landmark’s pricing for premium brands like Mercedes-Benz; a 5–10% duty change can swing retail prices by €3,000–€8,000 per vehicle based on 2024 MSRP ranges. Political moves on trade barriers or FTAs with the EU/UK could shift import cost structures, altering competitive parity with local assemblers. Analysts track tariff scenario modeling to forecast volume swings in the luxury segment, where 2024 sales concentrated 18% of group margins.

Infrastructure Development Initiatives

The rapid expansion of national highways and expressways under federal programs, with 12,000 km awarded in 2024 and a target of 25,000 km by 2025, increases demand for reliable passenger vehicles and SUVs, directly supporting Landmark’s sales pipeline.

Improved connectivity raises inter-city travel and vehicle utilization; India recorded a 9% rise in intercity trips in 2024, benefiting Landmark’s servicing and resale volumes.

Government urban infrastructure spending of $40 billion in 2024 guides feasibility for new Landmark touchpoints in Tier-2 cities, where vehicle registrations grew 7.5% year-over-year.

State-Level Taxation and Subsidies

Varying state road taxes and registration subsidies fragment India’s market: states like Maharashtra levy EV registration incentives up to INR 10,000 while Uttar Pradesh offers scrappage-linked benefits, impacting dealership margins and pricing across 28 states and 8 UTs.

Landmark must navigate regional political climates where incentives favor LPG, CNG or EVs; in 2024 EV sales share reached ~3.5% nationwide but exceeded 10% in Delhi and Kerala, altering product mix and inventory strategy.

Strategic planning needs granular tracking of state policy shifts—monthly monitoring of tax notifications and subsidy caps enabled a 7% uplift in regional sales for dealer groups in 2024.

- Fragmented taxes/subsidies across states affect pricing and margins

- Local incentives drive fuel-type demand (EVs >10% in some states)

- Monthly policy monitoring linked to a 7% regional sales improvement

- Prepare state-specific inventory and pricing strategies

Fuel Pricing and Regulatory Stability

Government control or deregulation of fuel prices directly alters TCO for ICE vehicles; a 2024 IEA report shows global gasoline retail prices varied 40-60% across major markets, affecting ownership costs and purchase cycles.

Political stability ensures consistent rollout of policies like India’s Scrappage Policy; 2024 implementation rates and incentives drive replacement cycles, reducing uncertainty for Landmark’s demand forecasts.

For Landmark’s after-sales and spare-parts divisions, policy reversals could swing demand by an estimated 8-12% annually based on 2023–2024 market elasticity studies.

- Fuel price regime alters TCO and purchase timing

- Policy stability ensures predictable scrappage-driven replacements

- Demand volatility for parts estimated 8–12% with policy shifts

- 2024 fuel price dispersion 40–60% across key markets (IEA)

Policy & duty shocks steer Landmark to EV inventory, charging capex and regional mix

Policy incentives (FAME‑II INR 10,000cr; PLI aiming 60–70% local EV components by 2030) push Landmark toward EV inventory, charging capex (~INR 2–5m/outlet) and dealer renegotiation; customs duty swings (±5–10%) alter premium pricing by €3k–€8k; state tax/incentive fragmentation (EV incentives up to INR 10k) shifts regional mix (national EV share ~3.5%, Delhi/Kerala >10%) and parts demand (policy-shock impact 8–12%).

| Metric | 2024 Value | Impact |

|---|---|---|

| FAME‑II allocation | INR 10,000cr | EV adoption/stocking |

| PLI EV target | 60–70% components by 2030 | Local sourcing, margin shifts |

| EV national share | 3.5% | Product mix |

| Delhi/Kerala EV share | >10% | Regional demand |

| Duty volatility | ±5–10% | Price swing €3–8k |

| Charging capex/outlet | INR 2–5m | Capex planning |

| Parts demand swing | 8–12% | After‑sales revenue |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Group Landmark, with each section supported by current data and regional market dynamics to identify risks and opportunities.

Condenses the full Group Landmark PESTLE into a concise, visually segmented summary for quick reference in meetings, presentations, or shared planning sessions.

Economic factors

Interest Rate Environment and Financing

The cost of auto loans is a key determinant of vehicle sales in mass-market and mid-premium segments; with RBI policy rate at 6.50% (Feb 2026) and typical retail auto loan EMI rates averaging 9–11% in 2025, financing costs materially shape demand. Landmark’s sales closely track lending-rate movements—each 100 bps rise historically trimmed monthly volumes by ~3–4%. High rates in 2022–23 depressed purchases, while the 2024–25 easing cycle (net 125 bps cuts) correlated with a 12% rebound in showroom footfall.

Rising Disposable Income and Premiumization

India’s middle class is projected at 350–400 million by 2025 and HNWIs rose 12% to ~820,000 in 2024, driving premiumization in autos; sales of SUVs and luxury cars grew ~18% in FY2024 vs passenger cars’ 6%. Landmark’s partnerships with Mercedes-Benz and Jeep position it to capture higher ASPs and margin expansion as buyers shift from functional hatchbacks to lifestyle SUVs and luxury sedans. Economic prosperity—GDP per capita rising to ~$2,600 in 2024—correlates with increased premium vehicle uptake, benefiting Landmark’s luxury-focused inventory and aftersales revenue streams.

Inflationary Pressures on Operational Costs

Rising input costs—global semiconductor shortages lifted but commodity-driven input inflation saw input price indices up ~7% YoY in 2024—force manufacturers to raise vehicle prices, which Landmark must convey to price-sensitive buyers, risking volume declines.

Landmark’s wage bills and prime showroom rents rose with UK CPI averaging 3.9% in 2024 and commercial rents up ~5% in prime locations, squeezing margins.

When macro inflation outpaces service revenue growth—aftermarket revenue growth for dealers averaged ~2–3% in 2024—maintaining profitability requires tighter cost control and selective pricing.

Used Car Market Valuation

Used-car valuations drive Landmark’s pre-owned unit: India’s organized used-car market grew to about USD 57 billion in 2024 with residual values averaging 45–60% for 3–5 year vehicles, directly influencing margins and inventory turnover.

During 2023–24 downturns, trade-ins rose ~18%, shifting buyers to secondary markets and cushioning Landmark against a ~7–10% dip in new-car volumes.

Formalization lets Landmark capture share from unorganized sellers; organized channels held ~25% of transactions in 2024, offering scale and higher gross margins.

- Residual values 45–60% (3–5 yrs)

- Organized market ~25% (2024)

- Trade-ins +18% in downturns

Currency Exchange Rate Volatility

Currency volatility impacts Landmark as the INR fell ~8% vs USD and ~6% vs EUR in 2022–2023, raising imported component costs and pressuring luxury vehicle margins.

Sharp INR depreciation in 2023–24 forced several OEMs to raise prices by 3–7%, curbing premium demand; a repeat could reduce Landmark sales in the luxury segment.

Landmark should hedge forex exposure, adjust inventory cadence, and communicate likely price shifts to customers during high volatility.

- INR moves (±5–8%) materially change landed costs

- OEM price hikes in 2023–24: ~3–7%

- Actions: hedging, tighter inventory, proactive customer communication

Higher rates squeeze volumes; premiumization and used-car strength lift margins

Higher financing costs (RBI 6.50% Feb 2026; retail auto EMI 9–11% in 2025) and input inflation (~7% YoY 2024) constrain volumes; premiumization (middle class 350–400M 2025; HNWIs ~820k in 2024) boosts SUV/luxury demand; used-car market USD57bn (2024) with residuals 45–60% supports margins; INR volatility (−8% vs USD 2022–23) raises import costs.

| Metric | Value |

|---|---|

| RBI rate | 6.50% (Feb 2026) |

| Retail EMI | 9–11% (2025) |

| Used market | USD57bn (2024) |

| Residuals | 45–60% (3–5yr) |

Preview Before You Purchase

Group Landmark PESTLE Analysis

The preview shown here is the exact Group Landmark PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use without placeholders or edits.