Grupo Clarín Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

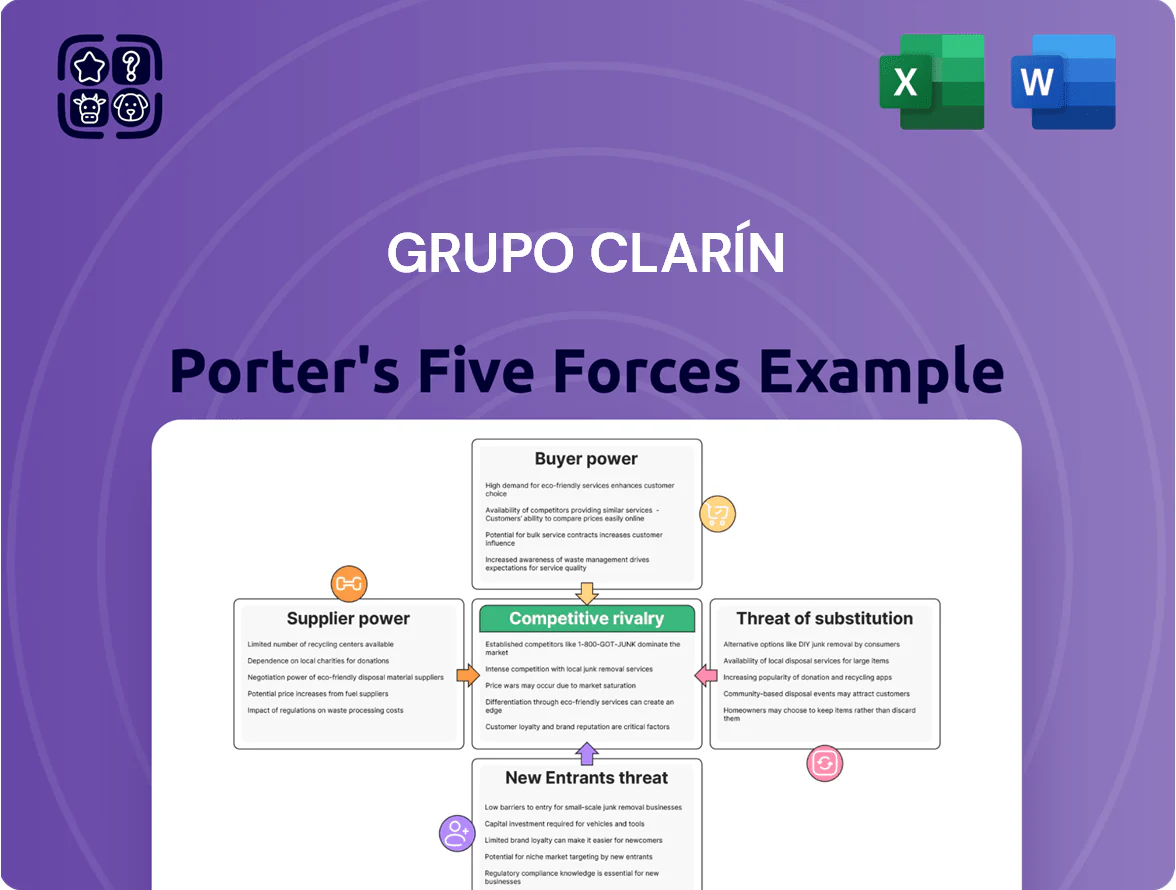

Grupo Clarín faces moderate buyer power and high rivalry amid digital disruption, while supplier and entrant threats remain contained by scale and regulatory ties; substitutes from streaming and social media pose growing risks to traditional advertising and print revenues. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Grupo Clarín’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Vertical Integration in Newsprint Production

Grupo Clarín gains material supplier power via Papel Prensa, Argentina’s main newsprint mill, which it part-owns and which supplied about 70% of national newsprint in 2023; owning this asset cuts external paper purchasing and weakens supplier leverage. By internalizing newsprint production, Clarín shields itself from the 2021–2024 global pulp price swings (peak +45% in 2021) and local shortages that raised import costs by roughly 18% in 2023. This vertical integration secures margins for print operations and lowers volatility in operating costs.

Control Over High-Value Content Rights

Suppliers of premium content—international sports leagues and film studios—hold moderate power because rights are exclusive, but Grupo Clarín’s control of El Trece and TyC Sports (combined TV ad share ~34% in 2024) makes it essential in Argentina, letting Clarín secure more favorable licensing fees than smaller rivals.

Technological Infrastructure and Telecom Equipment

For telecom and digital operations, Grupo Clarín depends on global vendors like Huawei and Nokia for 5G and high‑speed hardware; these suppliers command strong bargaining power because specialized kit and limited Argentine alternatives raise switching costs. In 2025, with 5G adoption in Argentina projected to reach ~35% of mobile connections, Clarín must secure vendor SLAs and parts inventory to avoid service hits and capex overruns—vendor terms can sway margins by several percentage points.

Dependence on Specialized Creative Talent

Dependence on specialized journalists, producers, and on-air talent gives suppliers strong leverage over Grupo Clarín because audience loyalty often follows personalities; top anchors can lift ratings by 10–30 percentage points in key slots (Nielsen IBOPE 2024 data).

Clarín remains a prestige employer, yet independent digital platforms and podcasts grew creator revenue shares by ~25% in 2023–24, raising churn risk as talent can command higher pay or move platforms.

The group must balance competitive salaries with managing inflation-driven wage pressure—Argentina CPI hit 124% in 2023 and wage indexation pushed media payroll costs up ~40% year-over-year for some outlets.

- High supplier leverage: personality-driven ratings +10–30%

- Creator alternatives: digital revenue +25% (2023–24)

- Cost pressure: Argentina CPI 124% (2023); payrolls +~40% YoY

Energy and Utility Provider Constraints

As a major industrial operator with printing plants and data centers, Grupo Clarín faces high supplier power from state-regulated energy and utility providers, which act as regional monopolies in Argentina.

Policy and tariff shifts in 2025 raised industrial electricity tariffs by about 28% year-on-year, squeezing Clarín’s operating margins and lifting utility cost share of COGS toward ~12%.

These services are essential and non-discretionary, leaving Clarín little room to negotiate fixed rates or switch suppliers, increasing margin volatility.

- 2025 industrial electricity tariffs +28% y/y

- Utility costs ≈12% of COGS

- Regional monopolies limit supplier switching

- High margin sensitivity to tariff policy

Suppliers wield mixed-to-high power: paper, talent, 5G and utilities drive costs

Suppliers exert mixed-to-high power: Papel Prensa supplies ~70% newsprint (2023), cutting Clarín’s paper costs and volatility; premium content and top talent hold moderate-to-strong leverage (anchors can shift ratings +10–30%, Nielsen IBOPE 2024); 5G vendors and regional utilities are strong suppliers—industrial power +28% y/y (2025) and utility costs ≈12% of COGS.

| Supplier | Key stat | Impact |

|---|---|---|

| Papel Prensa | ~70% national supply (2023) | Reduces external costs |

| Top talent | +10–30% ratings | High wage risk |

| 5G vendors | 5G adoption ~35% (2025) | High switching cost |

| Utilities | Electricity +28% y/y (2025) | ↑COGS to ~12% |

What is included in the product

Tailored for Grupo Clarín, this Porter's Five Forces overview uncovers competitive drivers, buyer/supplier leverage, entry barriers, substitutes, and disruptive threats shaping its media market position.

A concise, one-sheet Porter’s Five Forces for Grupo Clarín—quickly assess competitive intensity and regulatory risk to speed strategic decisions.

Customers Bargaining Power

Fragmented Individual Consumer Base

The millions of Clarín readers, TV viewers and 7.5 million+ Grupo Clarín digital subscribers (2025 internal reporting) are highly fragmented, so individual customers hold low bargaining power. While switching is easy, no single consumer can sway Clarín’s pricing or strategic direction. That fragmentation lets Clarín keep control over subscription fees and bundle structures across print, TV and digital units. Average ARPU estimates remain stable near ARS 1,200 monthly in 2024–25.

Corporate Advertiser Leverage and Reach

Low Switching Costs in Digital Media

Low switching costs in digital media give Grupo Clarín's customers strong bargaining power; with global free news and social platforms capturing attention, subscribers can quit monthly plans easily, pressuring prices and content quality.

In 2025 Argentina, streaming/news churn rose to ~20% annually and 62% of digital users surveyed said price matters most, so Clarín must offer exclusive, high-value journalism to justify paywalls and reduce cancellations.

High Switching Costs in Telecom Services

Customers of Clarín’s telecom arm, Telecom Argentina, face high switching costs from bundled internet, TV and mobile packages plus installation and number-porting hassles, lowering consumer bargaining power.

That stickiness means more predictable revenue: Telecom Argentina reported ARS 112.3 billion in service revenue for 2024, with broadband churn under 1.8% quarterly, so small price gaps rarely trigger moves.

- Bundling: internet+TV+mobile increases lock-in

- Installation/porting hassles raise exit cost

- 2024 service revenue ARS 112.3 bn; broadband churn ~1.8%

Government as a Strategic Institutional Client

The Argentine government is a major institutional client for Grupo Clarín, supplying official public advertising and institutional contracts that materially affect revenue streams; in 2024 public ad spending reached roughly ARS 120 billion, with Clarín-group outlets historically receiving a sizable share.

- Government = major ad client; public ad ~ARS 120B in 2024

- Political shifts alter allocations; revenue swing possible 10–20%

- 2025 performance tied to regulatory and fiscal priorities

High ad dependence and rising digital churn squeeze ARPU amid strong telecom stickiness

Customers vary: millions of fragmented consumers give low individual bargaining power, though digital churn (~20% annually in 2025) pressures pricing; ARPU ~ARS 1,200. Large advertisers hold moderate power—ads = ~42% of Grupo Clarín’s ARS 118B 2024 revenue—yet Clarín’s >60% TV reach limits leverage. Telecom customers face high switching costs; Telecom service revenue ARS 112.3B (2024), broadband churn ~1.8%.

| Metric | Value |

|---|---|

| Digital subscribers (2025) | 7.5M+ |

| ARPU (2024–25) | ARS 1,200/mo |

| Ad revenue share (2024) | 42% of ARS 118B |

| Digital churn (2025) | ~20% annual |

| Telecom service rev (2024) | ARS 112.3B |

| Broadband churn (2024) | ~1.8% quarterly |

Full Version Awaits

Grupo Clarín Porter's Five Forces Analysis

This preview shows the actual Grupo Clarín Porter's Five Forces analysis you'll receive after purchase—no placeholders or samples, fully formatted and ready for use.

The document displayed here is the exact file available for immediate download once you buy, containing the complete competitive forces evaluation and practical insights.

No surprises: the previewed content is the final deliverable—professional, comprehensive, and ready for your decision-making needs.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Grupo Clarín faces moderate buyer power and high rivalry amid digital disruption, while supplier and entrant threats remain contained by scale and regulatory ties; substitutes from streaming and social media pose growing risks to traditional advertising and print revenues. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Grupo Clarín’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Vertical Integration in Newsprint Production

Grupo Clarín gains material supplier power via Papel Prensa, Argentina’s main newsprint mill, which it part-owns and which supplied about 70% of national newsprint in 2023; owning this asset cuts external paper purchasing and weakens supplier leverage. By internalizing newsprint production, Clarín shields itself from the 2021–2024 global pulp price swings (peak +45% in 2021) and local shortages that raised import costs by roughly 18% in 2023. This vertical integration secures margins for print operations and lowers volatility in operating costs.

Control Over High-Value Content Rights

Suppliers of premium content—international sports leagues and film studios—hold moderate power because rights are exclusive, but Grupo Clarín’s control of El Trece and TyC Sports (combined TV ad share ~34% in 2024) makes it essential in Argentina, letting Clarín secure more favorable licensing fees than smaller rivals.

Technological Infrastructure and Telecom Equipment

For telecom and digital operations, Grupo Clarín depends on global vendors like Huawei and Nokia for 5G and high‑speed hardware; these suppliers command strong bargaining power because specialized kit and limited Argentine alternatives raise switching costs. In 2025, with 5G adoption in Argentina projected to reach ~35% of mobile connections, Clarín must secure vendor SLAs and parts inventory to avoid service hits and capex overruns—vendor terms can sway margins by several percentage points.

Dependence on Specialized Creative Talent

Dependence on specialized journalists, producers, and on-air talent gives suppliers strong leverage over Grupo Clarín because audience loyalty often follows personalities; top anchors can lift ratings by 10–30 percentage points in key slots (Nielsen IBOPE 2024 data).

Clarín remains a prestige employer, yet independent digital platforms and podcasts grew creator revenue shares by ~25% in 2023–24, raising churn risk as talent can command higher pay or move platforms.

The group must balance competitive salaries with managing inflation-driven wage pressure—Argentina CPI hit 124% in 2023 and wage indexation pushed media payroll costs up ~40% year-over-year for some outlets.

- High supplier leverage: personality-driven ratings +10–30%

- Creator alternatives: digital revenue +25% (2023–24)

- Cost pressure: Argentina CPI 124% (2023); payrolls +~40% YoY

Energy and Utility Provider Constraints

As a major industrial operator with printing plants and data centers, Grupo Clarín faces high supplier power from state-regulated energy and utility providers, which act as regional monopolies in Argentina.

Policy and tariff shifts in 2025 raised industrial electricity tariffs by about 28% year-on-year, squeezing Clarín’s operating margins and lifting utility cost share of COGS toward ~12%.

These services are essential and non-discretionary, leaving Clarín little room to negotiate fixed rates or switch suppliers, increasing margin volatility.

- 2025 industrial electricity tariffs +28% y/y

- Utility costs ≈12% of COGS

- Regional monopolies limit supplier switching

- High margin sensitivity to tariff policy

Suppliers wield mixed-to-high power: paper, talent, 5G and utilities drive costs

Suppliers exert mixed-to-high power: Papel Prensa supplies ~70% newsprint (2023), cutting Clarín’s paper costs and volatility; premium content and top talent hold moderate-to-strong leverage (anchors can shift ratings +10–30%, Nielsen IBOPE 2024); 5G vendors and regional utilities are strong suppliers—industrial power +28% y/y (2025) and utility costs ≈12% of COGS.

| Supplier | Key stat | Impact |

|---|---|---|

| Papel Prensa | ~70% national supply (2023) | Reduces external costs |

| Top talent | +10–30% ratings | High wage risk |

| 5G vendors | 5G adoption ~35% (2025) | High switching cost |

| Utilities | Electricity +28% y/y (2025) | ↑COGS to ~12% |

What is included in the product

Tailored for Grupo Clarín, this Porter's Five Forces overview uncovers competitive drivers, buyer/supplier leverage, entry barriers, substitutes, and disruptive threats shaping its media market position.

A concise, one-sheet Porter’s Five Forces for Grupo Clarín—quickly assess competitive intensity and regulatory risk to speed strategic decisions.

Customers Bargaining Power

Fragmented Individual Consumer Base

The millions of Clarín readers, TV viewers and 7.5 million+ Grupo Clarín digital subscribers (2025 internal reporting) are highly fragmented, so individual customers hold low bargaining power. While switching is easy, no single consumer can sway Clarín’s pricing or strategic direction. That fragmentation lets Clarín keep control over subscription fees and bundle structures across print, TV and digital units. Average ARPU estimates remain stable near ARS 1,200 monthly in 2024–25.

Corporate Advertiser Leverage and Reach

Low Switching Costs in Digital Media

Low switching costs in digital media give Grupo Clarín's customers strong bargaining power; with global free news and social platforms capturing attention, subscribers can quit monthly plans easily, pressuring prices and content quality.

In 2025 Argentina, streaming/news churn rose to ~20% annually and 62% of digital users surveyed said price matters most, so Clarín must offer exclusive, high-value journalism to justify paywalls and reduce cancellations.

High Switching Costs in Telecom Services

Customers of Clarín’s telecom arm, Telecom Argentina, face high switching costs from bundled internet, TV and mobile packages plus installation and number-porting hassles, lowering consumer bargaining power.

That stickiness means more predictable revenue: Telecom Argentina reported ARS 112.3 billion in service revenue for 2024, with broadband churn under 1.8% quarterly, so small price gaps rarely trigger moves.

- Bundling: internet+TV+mobile increases lock-in

- Installation/porting hassles raise exit cost

- 2024 service revenue ARS 112.3 bn; broadband churn ~1.8%

Government as a Strategic Institutional Client

The Argentine government is a major institutional client for Grupo Clarín, supplying official public advertising and institutional contracts that materially affect revenue streams; in 2024 public ad spending reached roughly ARS 120 billion, with Clarín-group outlets historically receiving a sizable share.

- Government = major ad client; public ad ~ARS 120B in 2024

- Political shifts alter allocations; revenue swing possible 10–20%

- 2025 performance tied to regulatory and fiscal priorities

High ad dependence and rising digital churn squeeze ARPU amid strong telecom stickiness

Customers vary: millions of fragmented consumers give low individual bargaining power, though digital churn (~20% annually in 2025) pressures pricing; ARPU ~ARS 1,200. Large advertisers hold moderate power—ads = ~42% of Grupo Clarín’s ARS 118B 2024 revenue—yet Clarín’s >60% TV reach limits leverage. Telecom customers face high switching costs; Telecom service revenue ARS 112.3B (2024), broadband churn ~1.8%.

| Metric | Value |

|---|---|

| Digital subscribers (2025) | 7.5M+ |

| ARPU (2024–25) | ARS 1,200/mo |

| Ad revenue share (2024) | 42% of ARS 118B |

| Digital churn (2025) | ~20% annual |

| Telecom service rev (2024) | ARS 112.3B |

| Broadband churn (2024) | ~1.8% quarterly |

Full Version Awaits

Grupo Clarín Porter's Five Forces Analysis

This preview shows the actual Grupo Clarín Porter's Five Forces analysis you'll receive after purchase—no placeholders or samples, fully formatted and ready for use.

The document displayed here is the exact file available for immediate download once you buy, containing the complete competitive forces evaluation and practical insights.

No surprises: the previewed content is the final deliverable—professional, comprehensive, and ready for your decision-making needs.