Grupo Herdez Porter's Five Forces Analysis

From Overview to Strategy Blueprint

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Grupo Herdez’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Commodity Price Volatility

As of late 2025, Grupo Herdez remains highly sensitive to agricultural price swings: vegetables, wheat and fruits accounted for ~28% of COGS in 2024 and saw year-on-year price swings up to 18% during 2022–25. Suppliers gain leverage when global yields fall or climate events hit Mexican regions—Hurricane Otis (2023) and 2024 droughts pushed local prices 12–20% higher. Herdez counters with multi-year hedges covering ~45% of wheat exposure and diversified sourcing across Mexico, Chile and the US, cutting peak-cost risk by an estimated 6–8% of EBITDA volatility.

Packaging Material Costs

Suppliers of aluminum, glass, and PET plastic exert moderate bargaining power because food-grade specs limit substitutes; aluminum cans account for ~35% of Herdez’s packaging spend and glass for ~20% (2024 internal procurement mix).

Consolidation—top 3 global metal-pack suppliers control ~60% capacity—raises input-cost risk; a 2023 aluminum price spike (+45% YoY) pushed COGS up for Mexican food firms.

Herdez uses multi-year contracts covering ~70% of volume to lock prices and secure supply, trimming volatility but leaving spot exposure for ~30% of purchases.

Strategic Joint Ventures

Strategic joint ventures with global suppliers like McCormick & Company neutralize supplier power for Grupo Herdez by securing preferential pricing and supply; Herdez reported a 12% reduction in seasoning costs in 2024 versus 2021 after closer supply-chain integration.

Energy and Logistics Providers

Energy and fuel costs give suppliers moderate to high bargaining power for Grupo Herdez because processing plants and distribution rely heavily on electricity and diesel; in 2024 energy and logistics accounted for an estimated 9–12% of COGS for frozen foods and ice cream.

Electricity price swings in Mexico in 2025 (±6–10% year) bite margins directly, so Herdez is cutting exposure by investing in renewables—company reports show ~35 GWh of captive solar capacity planned by end-2025, aiming to cover ~18% of site consumption.

- Energy/logistics ≈9–12% COGS

- Electricity volatility ±6–10% (2025)

- Planned captive solar ≈35 GWh by 2025

- Target cover ≈18% of consumption

Labor Market Dynamics

The supply of skilled and unskilled labor in Mexico’s food manufacturing sector has tightened, raising suppliers’ bargaining power as a critical input for Grupo Herdez; national minimum wage rose to MXN 260/day by 2025, up ~37% since 2020, and formal employment reforms increased social costs.

Herdez faces higher human-capital costs—labor now ~18–22% of COGS in comparable packagers—so it must balance wage competitiveness with automation (robotics/ERP) to protect margins and output.

Herdez manages high supplier cost risk with hedges, contracts and 35 GWh solar

Suppliers exert moderate-to-high power: agri inputs (28% of COGS, ±18% price swings 2022–25) and packaging (aluminum 35%, glass 20%) raise cost risk; energy/logistics ~9–12% COGS with electricity volatility ±6–10% (2025). Herdez offsets via hedges (wheat ~45% covered), multi-year contracts (~70% volume), JV pricing cuts (seasoning costs -12% vs 2021), and planned 35 GWh solar to cover ~18% consumption.

| Metric | Value |

|---|---|

| Agri share COGS | ~28% |

| Packaging mix | Al 35% / Glass 20% |

| Hedges | Wheat ~45% |

| Contracts | ~70% vol |

| Energy % COGS | 9–12% |

| Solar planned | 35 GWh (~18%) |

What is included in the product

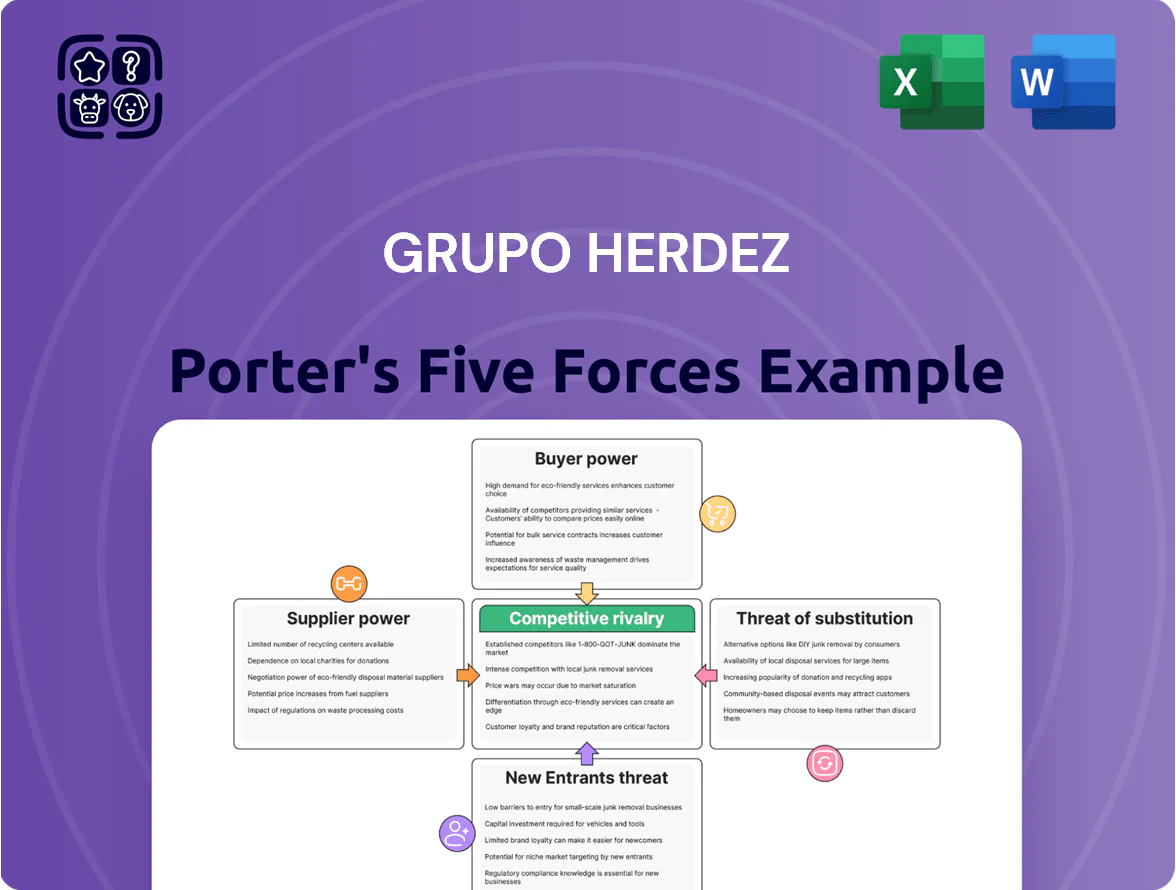

Provides a concise Porter’s Five Forces overview for Grupo Herdez, assessing competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry while highlighting disruptive risks and strategic implications for pricing and market share.

Concise Five Forces snapshot for Grupo Herdez—quickly assess competitive intensity and supplier/buyer leverage to guide strategic responses.

Customers Bargaining Power

Retail Giant Dominance

Fragmented Traditional Trade

The mom-and-pop stores and small wholesalers across Mexico have low individual bargaining power but are crucial: they account for roughly 35% of Grupo Herdez’s domestic volume (2024), so collectively they force Herdez to run a complex direct-to-store delivery network to keep shelf presence. They cannot push prices like Walmart, but this channel yields higher gross margins—about 18% vs 12% in modern retail—protecting revenues amid supermarket price pressure.

Brand Loyalty and Consumer Preference

End-consumers drive bargaining power via switching and price sensitivity; in packaged foods, Herdez’s 2025 brand equity—reflected in a 38% premium in Nielsen brand preference surveys and 22% YoY loyalty retention in core salsa and spreads—lowers switching to cheaper private labels.

That loyalty let Grupo Herdez pass roughly 60–70% of 2024–25 input-cost inflation into prices while holding national market share near 24.5%, so consumer power is moderated but still risks rising if inflation persists.

Growth of Private Label Brands

Retailers are expanding private-label share—Mexican supermarket private brands rose to ~18% of FMCG sales in 2024—pressuring Grupo Herdez on price and shelf space.

This shift boosts retailer leverage: chains can de-list or downgrade Herdez SKUs in favor of higher-margin house brands, squeezing Herdez’s trade terms and promotion spend.

Herdez fights back by premiumizing and innovating—launching upscale salsas and gourmet lines in 2023–24 that deliver higher margins and are harder for private labels to match.

- Private labels ~18% of Mexican FMCG sales (2024)

- Retailers can cut Herdez visibility, raising trade costs

- Herdez focuses on premium/innovation to protect margin

Digital and E-commerce Shifts

By late 2025 quick-commerce and online grocery platforms drive 22–28% of urban FMCG grocery trips in Mexico, giving Grupo Herdez first-party data but forcing higher fulfillment costs and 8–12% incremental marketing spend to win placement in digital search and app shelves.

These platforms squeeze margins via 15–25% delivery/service fees; active management of channel economics and co-marketing deals is essential to prevent margin erosion and protect brand control.

- 22–28% urban online grocery share (late 2025)

- 8–12% extra marketing spend for visibility

- 15–25% delivery/service fees risk

- First-party data gains vs. fulfillment cost trade-off

Big chains dictate pricing despite mom‑and‑pop margins; online grocers lift costs

| Metric | Value |

|---|---|

| Retailer share | 30–40% |

| Mom‑and‑pop volume | ~35% |

| Gross margin (mom‑and‑pop) | ~18% |

| Gross margin (modern retail) | ~12% |

| Private label FMCG (2024) | ~18% |

| Online urban grocery (late 2025) | 22–28% |

| Delivery/service fees | 15–25% |

| Extra digital marketing | +8–12% |

Same Document Delivered

Grupo Herdez Porter's Five Forces Analysis

This preview shows the exact Grupo Herdez Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is a professionally written, fully formatted file—ready for download and immediate use the moment you buy.

You're viewing the final deliverable: the same complete analysis, organized and actionable, available to you instantly after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Grupo Herdez’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Commodity Price Volatility

As of late 2025, Grupo Herdez remains highly sensitive to agricultural price swings: vegetables, wheat and fruits accounted for ~28% of COGS in 2024 and saw year-on-year price swings up to 18% during 2022–25. Suppliers gain leverage when global yields fall or climate events hit Mexican regions—Hurricane Otis (2023) and 2024 droughts pushed local prices 12–20% higher. Herdez counters with multi-year hedges covering ~45% of wheat exposure and diversified sourcing across Mexico, Chile and the US, cutting peak-cost risk by an estimated 6–8% of EBITDA volatility.

Packaging Material Costs

Suppliers of aluminum, glass, and PET plastic exert moderate bargaining power because food-grade specs limit substitutes; aluminum cans account for ~35% of Herdez’s packaging spend and glass for ~20% (2024 internal procurement mix).

Consolidation—top 3 global metal-pack suppliers control ~60% capacity—raises input-cost risk; a 2023 aluminum price spike (+45% YoY) pushed COGS up for Mexican food firms.

Herdez uses multi-year contracts covering ~70% of volume to lock prices and secure supply, trimming volatility but leaving spot exposure for ~30% of purchases.

Strategic Joint Ventures

Strategic joint ventures with global suppliers like McCormick & Company neutralize supplier power for Grupo Herdez by securing preferential pricing and supply; Herdez reported a 12% reduction in seasoning costs in 2024 versus 2021 after closer supply-chain integration.

Energy and Logistics Providers

Energy and fuel costs give suppliers moderate to high bargaining power for Grupo Herdez because processing plants and distribution rely heavily on electricity and diesel; in 2024 energy and logistics accounted for an estimated 9–12% of COGS for frozen foods and ice cream.

Electricity price swings in Mexico in 2025 (±6–10% year) bite margins directly, so Herdez is cutting exposure by investing in renewables—company reports show ~35 GWh of captive solar capacity planned by end-2025, aiming to cover ~18% of site consumption.

- Energy/logistics ≈9–12% COGS

- Electricity volatility ±6–10% (2025)

- Planned captive solar ≈35 GWh by 2025

- Target cover ≈18% of consumption

Labor Market Dynamics

The supply of skilled and unskilled labor in Mexico’s food manufacturing sector has tightened, raising suppliers’ bargaining power as a critical input for Grupo Herdez; national minimum wage rose to MXN 260/day by 2025, up ~37% since 2020, and formal employment reforms increased social costs.

Herdez faces higher human-capital costs—labor now ~18–22% of COGS in comparable packagers—so it must balance wage competitiveness with automation (robotics/ERP) to protect margins and output.

Herdez manages high supplier cost risk with hedges, contracts and 35 GWh solar

Suppliers exert moderate-to-high power: agri inputs (28% of COGS, ±18% price swings 2022–25) and packaging (aluminum 35%, glass 20%) raise cost risk; energy/logistics ~9–12% COGS with electricity volatility ±6–10% (2025). Herdez offsets via hedges (wheat ~45% covered), multi-year contracts (~70% volume), JV pricing cuts (seasoning costs -12% vs 2021), and planned 35 GWh solar to cover ~18% consumption.

| Metric | Value |

|---|---|

| Agri share COGS | ~28% |

| Packaging mix | Al 35% / Glass 20% |

| Hedges | Wheat ~45% |

| Contracts | ~70% vol |

| Energy % COGS | 9–12% |

| Solar planned | 35 GWh (~18%) |

What is included in the product

Provides a concise Porter’s Five Forces overview for Grupo Herdez, assessing competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry while highlighting disruptive risks and strategic implications for pricing and market share.

Concise Five Forces snapshot for Grupo Herdez—quickly assess competitive intensity and supplier/buyer leverage to guide strategic responses.

Customers Bargaining Power

Retail Giant Dominance

Fragmented Traditional Trade

The mom-and-pop stores and small wholesalers across Mexico have low individual bargaining power but are crucial: they account for roughly 35% of Grupo Herdez’s domestic volume (2024), so collectively they force Herdez to run a complex direct-to-store delivery network to keep shelf presence. They cannot push prices like Walmart, but this channel yields higher gross margins—about 18% vs 12% in modern retail—protecting revenues amid supermarket price pressure.

Brand Loyalty and Consumer Preference

End-consumers drive bargaining power via switching and price sensitivity; in packaged foods, Herdez’s 2025 brand equity—reflected in a 38% premium in Nielsen brand preference surveys and 22% YoY loyalty retention in core salsa and spreads—lowers switching to cheaper private labels.

That loyalty let Grupo Herdez pass roughly 60–70% of 2024–25 input-cost inflation into prices while holding national market share near 24.5%, so consumer power is moderated but still risks rising if inflation persists.

Growth of Private Label Brands

Retailers are expanding private-label share—Mexican supermarket private brands rose to ~18% of FMCG sales in 2024—pressuring Grupo Herdez on price and shelf space.

This shift boosts retailer leverage: chains can de-list or downgrade Herdez SKUs in favor of higher-margin house brands, squeezing Herdez’s trade terms and promotion spend.

Herdez fights back by premiumizing and innovating—launching upscale salsas and gourmet lines in 2023–24 that deliver higher margins and are harder for private labels to match.

- Private labels ~18% of Mexican FMCG sales (2024)

- Retailers can cut Herdez visibility, raising trade costs

- Herdez focuses on premium/innovation to protect margin

Digital and E-commerce Shifts

By late 2025 quick-commerce and online grocery platforms drive 22–28% of urban FMCG grocery trips in Mexico, giving Grupo Herdez first-party data but forcing higher fulfillment costs and 8–12% incremental marketing spend to win placement in digital search and app shelves.

These platforms squeeze margins via 15–25% delivery/service fees; active management of channel economics and co-marketing deals is essential to prevent margin erosion and protect brand control.

- 22–28% urban online grocery share (late 2025)

- 8–12% extra marketing spend for visibility

- 15–25% delivery/service fees risk

- First-party data gains vs. fulfillment cost trade-off

Big chains dictate pricing despite mom‑and‑pop margins; online grocers lift costs

| Metric | Value |

|---|---|

| Retailer share | 30–40% |

| Mom‑and‑pop volume | ~35% |

| Gross margin (mom‑and‑pop) | ~18% |

| Gross margin (modern retail) | ~12% |

| Private label FMCG (2024) | ~18% |

| Online urban grocery (late 2025) | 22–28% |

| Delivery/service fees | 15–25% |

| Extra digital marketing | +8–12% |

Same Document Delivered

Grupo Herdez Porter's Five Forces Analysis

This preview shows the exact Grupo Herdez Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is a professionally written, fully formatted file—ready for download and immediate use the moment you buy.

You're viewing the final deliverable: the same complete analysis, organized and actionable, available to you instantly after payment.