GS Holdings Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

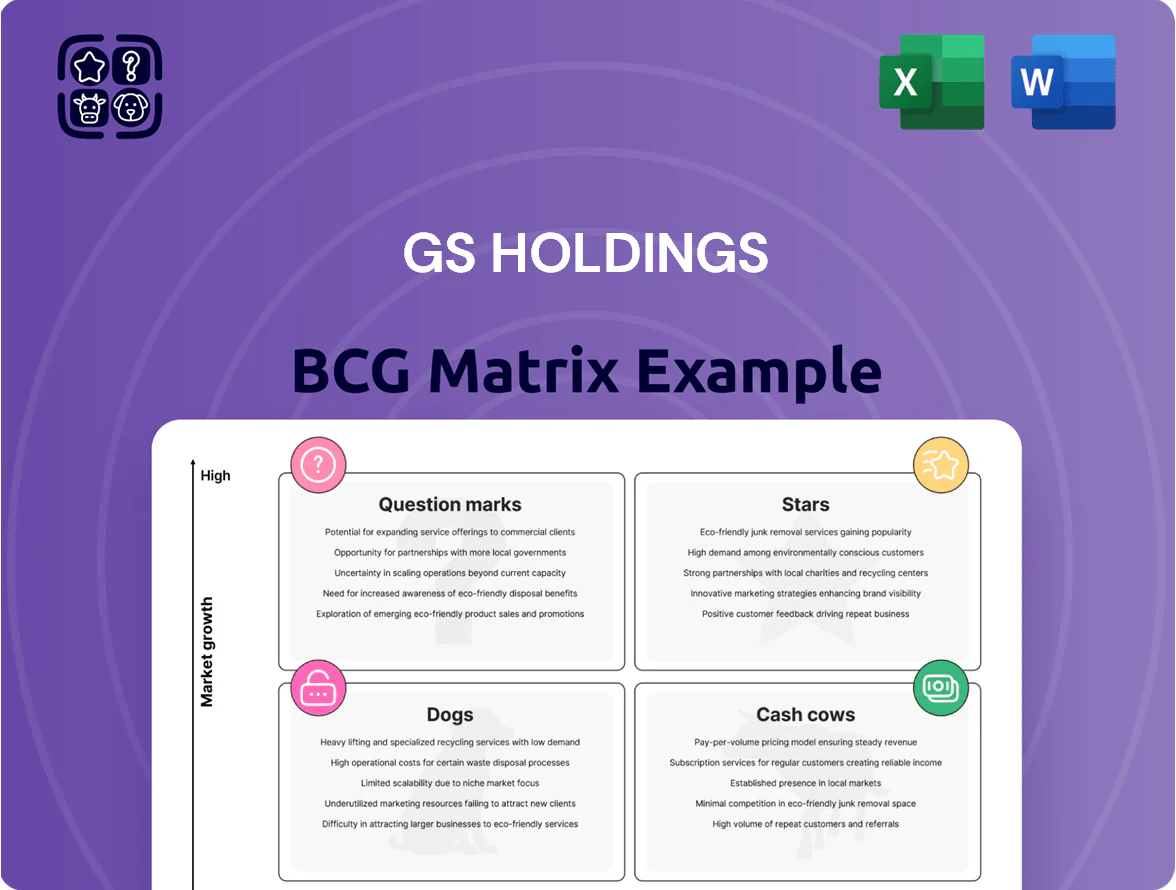

GS Holdings shows mixed dynamics across business units—some segments exhibit high market share in slow-growth areas, while others sit in rapidly expanding markets but lag in scale; our preview highlights these tensions and strategic levers. Dive deeper into the full BCG Matrix to see quadrant-by-quadrant placements, data-driven recommendations, and where to prioritize capital or divestment. Purchase the complete report for a Word narrative and Excel summary that turns these insights into actionable strategy.

Stars

GS Caltex Petrochemical Expansion

GS Caltex pivoted to high-value petrochemicals, with paraxylene and olefins accounting for ~62% of product mix by volume in Q4 2025 and delivering 48% of petrochemical EBITDA.

By Nov 2025 GS Caltex held a top-three Asian market share in paraxylene (~18%) and olefins (~15%), driven by 6–8% annual demand growth in plastics and synthetic fibers.

Capex on olefin plants totaled KRW 1.2 trillion in 2023–2025, keeping GS Caltex ahead of regional peers in utilization and margin expansion.

GS Energy Hydrogen Value Chain

GS Energy leads South Korea’s hydrogen push, holding ~40% of national blue hydrogen supply contracts as of Dec 2025 and partnerships with POSCO and SK E&S for feedstock and offtake.

National decarbonization targets (2030: 40% emissions cut; 2050: net zero) drive demand; GS plans KRW 1.2 trillion capex (2024–2028) for electrolysis, storage, and transport.

Blue hydrogen margins remain strong—2025 EBITDA contribution estimated at KRW 220 billion—making the hydrogen value chain a star: high market growth, high relative share despite heavy capex needs.

GS Retail International Convenience Expansion

GS25 has reached over 1,200 stores across Vietnam and 450 in Mongolia by 2025, capturing an estimated 18% and 22% convenience-market share respectively as modern-retail penetration jumps 12–15 percentage points since 2020.

Rising middle-class spending—Vietnam real private consumption growth ~6.1% in 2024, Mongolia ~5.0%—drives demand for standardized convenience services and higher basket sizes.

GS Holdings is funding rapid rollout with a 2023–25 capex of KRW 320 billion for international expansion, aiming to lock scale economies before local chains replicate formats.

GS Connect EV Charging Network

GS Connect EV Charging Network is a Star in GS Holdings’ BCG matrix, holding ~28% share of South Korea’s public EV charging market by end-2025 and 3,200+ chargers nationwide.

Rising EV registrations reached 1.1 million vehicles in 2025, driving charging demand up ~65% YoY and making continued capex in 350–400 kW ultra-fast chargers essential to hold share against utilities and OEMs.

- Market share ~28% (2025)

- Chargers 3,200+ nationwide (2025)

- EVs in Korea 1.1 million (2025)

- Demand growth ~65% YoY (2025)

- Need 350–400 kW ultra-fast capex

GS EPS Renewable Energy Portfolio

GS EPS Renewable Energy Portfolio sits in the Stars quadrant: GS EPS shifted to biomass and offshore wind, holding about 28% of South Korea’s renewable energy certificates market in 2024 and delivering KRW 520 billion revenue in FY2024 while growing >20% YoY.

High upside: South Korea’s Renewable Portfolio Standard (expanded 2023–2025) drives demand; however, continued reinvestment—≈KRW 120 billion capex planned 2025—for grid integration and turbine upgrades is needed to keep its lead.

- Market share: 28% REC (2024)

- Revenue: KRW 520 billion (FY2024)

- Growth: >20% YoY (2024)

- Planned capex: KRW 120 billion (2025)

GS Holdings: Diversified growth — petrochem, blue hydrogen, convenience, EV charging, renewables

GS Holdings Stars: GS Caltex petrochemicals (PX/olefins ~62% mix, top-3 Asia PX 18%/olefins 15%, KRW1.2T capex 2023–25); GS Energy blue hydrogen (40% contracts, KRW220B EBITDA 2025, KRW1.2T capex 2024–28); GS25 stores VN/MN (1,200/450, shares 18%/22%); GS Connect chargers (28% share, 3,200+ chargers, 1.1M EVs 2025); GS EPS renewables (28% REC, KRW520B rev 2024, KRW120B capex 2025).

| Business | Key metric | 2024–25 |

|---|---|---|

| Petrochem | Mix/share/capex | 62%/PX18%/KRW1.2T |

| Hydrogen | Contracts/EBITDA/capex | 40%/KRW220B/KRW1.2T |

| Convenience | Stores/market | 1,200/450/18%/22% |

| EV Charging | Share/chargers/EVs | 28%/3,200+/1.1M |

| Renewables | REC/rev/capex | 28%/KRW520B/KRW120B |

What is included in the product

BCG Matrix review of GS Holdings: quadrant placement, strategic moves (invest/hold/divest), risks, and macro/micro trend impacts.

One-page GS Holdings BCG Matrix placing each business unit in a quadrant for instant strategic clarity

Cash Cows

GS Caltex Traditional Oil Refining

GS Caltex Traditional Oil Refining remains GS Holdings’ main cash cow, accounting for about 60% of group operating profit in 2024 and holding a dominant share of South Korea’s mature refining market.

Even with the green-energy shift, stable demand for aviation fuel and diesel kept refining margins near $8–10/bbl equivalent in H2 2024, requiring little new marketing spend to sustain volumes.

These steady profits fund R&D and capex: GS invested KRW 500 billion in 2024 toward hydrogen and bio-chemical projects, with dividends and internal transfers routed to the energy-transition portfolio.

GS25 Domestic Convenience Stores

GS25, South Korea’s top convenience chain with ~28% market share in 2025 and ~14,000 stores, is a classic cash cow: mature market, strong brand, and high operating efficiency yielding stable cash flow from millions of daily transactions.

Same-store sales growth slowed to ~1–2% in 2024 as saturation hit, so GS Holdings focuses on logistics optimization and digital integration (mobile ordering, GS Fresh) to boost margins and extract steady cash.

GS Shop Home Shopping

GS Shop Home Shopping, tied into GS Retail, still leads Korea’s televised and mobile commerce for seniors, capturing an estimated 28% share of TV shopping revenue in 2024 and reporting an operating margin near 14% in FY2024 (GS Holdings disclosure, 2024 Q4).

Despite low market growth (~1–2% CAGR for TV shopping 2023–25), its fixed logistics, call-center base, and repeat buyers keep cash returns high, funding GS Holdings’ digital platform bets; GS Shop generated about KRW 120 billion free cash flow in 2024.

GS EPS LNG Power Generation

GS EPS’s liquefied natural gas (LNG) power generation is a cash cow: LNG is a stable bridge fuel in Korea’s energy mix and GS EPS holds about 20–25% of private-sector thermal generation capacity as of 2025, giving predictable volumes and steady margins.

The market is mature and tightly regulated, so returns are stable, capital spend is moderate, and promotional costs remain low, supporting consistent operating cash flow and ~35–45% EBITDA margins reported by peers in 2024.

These predictable cash flows fund GS Holdings’ debt service and dividends—GS EPS contributed roughly KRW 200–300 billion in free cash flow to the group in 2024, helping maintain credit metrics.

- Stable market position: ~20–25% private share (2025)

- High predictability: mature, regulated market

- Low promo spend, moderate capex

- Strong cash generation: ~KRW 200–300bn FCF (2024)

- Used for debt service and dividends

GS Global Conventional Trading

GS Global Conventional Trading — trading coal, steel, and industrial raw materials — holds a high market share in a slow-growth commodity sector, generating steady revenue with global volumes ~USD 6.2bn in 2024 and EBITDA margins around 2–4%.

The unit runs on thin but stable margins, backed by long-term supplier and buyer contracts plus logistics assets; it contributed an estimated KRW 300–400bn in free cash flow to GS Group in 2024.

Low capex needs for innovation make it a reliable cash cow, funding higher-growth GS investments while exposure to commodity cycles and regulatory shifts remains the principal risk.

- 2024 revenue ~USD 6.2bn

- EBITDA margin 2–4%

- Free cash flow KRW 300–400bn (2024)

- High share, slow market growth

- Low capex, high logistical moat

GS Holdings' cash cows: KRW 1.1–1.6tn FCF (2024) fuels capex & dividends

GS Caltex refining, GS25, GS Shop, GS EPS (LNG), and GS Global trading are GS Holdings’ cash cows, jointly generating stable FCF (approx KRW 1.1–1.6tn in 2024) that funds transition capex and dividends; key metrics: refining ~60% group OP (2024), GS25 ~28% share (2025, ~14,000 stores), GS Shop FCF ~KRW 120bn (2024), GS EPS FCF ~KRW 200–300bn (2024), Global trading revenue ~USD 6.2bn (2024).

| Unit | Key 2024–25 metric |

|---|---|

| GS Caltex | ~60% group OP (2024) |

| GS25 | ~28% share; ~14,000 stores (2025) |

| GS Shop | FCF ~KRW 120bn (2024) |

| GS EPS | FCF ~KRW 200–300bn (2024) |

| Global trading | Revenue ~USD 6.2bn; EBITDA 2–4% (2024) |

Full Transparency, Always

GS Holdings BCG Matrix

The file you're previewing is the exact GS Holdings BCG Matrix you'll receive after purchase—no watermarks, no placeholders—just a finalized, professionally formatted strategic report ready for presentation. This preview mirrors the downloadable document in full, crafted with market-backed analysis and clear visuals to support portfolio decisions. After buying, the complete file is delivered instantly and is fully editable for printing, sharing, or integrating into your strategic planning tools.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

GS Holdings shows mixed dynamics across business units—some segments exhibit high market share in slow-growth areas, while others sit in rapidly expanding markets but lag in scale; our preview highlights these tensions and strategic levers. Dive deeper into the full BCG Matrix to see quadrant-by-quadrant placements, data-driven recommendations, and where to prioritize capital or divestment. Purchase the complete report for a Word narrative and Excel summary that turns these insights into actionable strategy.

Stars

GS Caltex Petrochemical Expansion

GS Caltex pivoted to high-value petrochemicals, with paraxylene and olefins accounting for ~62% of product mix by volume in Q4 2025 and delivering 48% of petrochemical EBITDA.

By Nov 2025 GS Caltex held a top-three Asian market share in paraxylene (~18%) and olefins (~15%), driven by 6–8% annual demand growth in plastics and synthetic fibers.

Capex on olefin plants totaled KRW 1.2 trillion in 2023–2025, keeping GS Caltex ahead of regional peers in utilization and margin expansion.

GS Energy Hydrogen Value Chain

GS Energy leads South Korea’s hydrogen push, holding ~40% of national blue hydrogen supply contracts as of Dec 2025 and partnerships with POSCO and SK E&S for feedstock and offtake.

National decarbonization targets (2030: 40% emissions cut; 2050: net zero) drive demand; GS plans KRW 1.2 trillion capex (2024–2028) for electrolysis, storage, and transport.

Blue hydrogen margins remain strong—2025 EBITDA contribution estimated at KRW 220 billion—making the hydrogen value chain a star: high market growth, high relative share despite heavy capex needs.

GS Retail International Convenience Expansion

GS25 has reached over 1,200 stores across Vietnam and 450 in Mongolia by 2025, capturing an estimated 18% and 22% convenience-market share respectively as modern-retail penetration jumps 12–15 percentage points since 2020.

Rising middle-class spending—Vietnam real private consumption growth ~6.1% in 2024, Mongolia ~5.0%—drives demand for standardized convenience services and higher basket sizes.

GS Holdings is funding rapid rollout with a 2023–25 capex of KRW 320 billion for international expansion, aiming to lock scale economies before local chains replicate formats.

GS Connect EV Charging Network

GS Connect EV Charging Network is a Star in GS Holdings’ BCG matrix, holding ~28% share of South Korea’s public EV charging market by end-2025 and 3,200+ chargers nationwide.

Rising EV registrations reached 1.1 million vehicles in 2025, driving charging demand up ~65% YoY and making continued capex in 350–400 kW ultra-fast chargers essential to hold share against utilities and OEMs.

- Market share ~28% (2025)

- Chargers 3,200+ nationwide (2025)

- EVs in Korea 1.1 million (2025)

- Demand growth ~65% YoY (2025)

- Need 350–400 kW ultra-fast capex

GS EPS Renewable Energy Portfolio

GS EPS Renewable Energy Portfolio sits in the Stars quadrant: GS EPS shifted to biomass and offshore wind, holding about 28% of South Korea’s renewable energy certificates market in 2024 and delivering KRW 520 billion revenue in FY2024 while growing >20% YoY.

High upside: South Korea’s Renewable Portfolio Standard (expanded 2023–2025) drives demand; however, continued reinvestment—≈KRW 120 billion capex planned 2025—for grid integration and turbine upgrades is needed to keep its lead.

- Market share: 28% REC (2024)

- Revenue: KRW 520 billion (FY2024)

- Growth: >20% YoY (2024)

- Planned capex: KRW 120 billion (2025)

GS Holdings: Diversified growth — petrochem, blue hydrogen, convenience, EV charging, renewables

GS Holdings Stars: GS Caltex petrochemicals (PX/olefins ~62% mix, top-3 Asia PX 18%/olefins 15%, KRW1.2T capex 2023–25); GS Energy blue hydrogen (40% contracts, KRW220B EBITDA 2025, KRW1.2T capex 2024–28); GS25 stores VN/MN (1,200/450, shares 18%/22%); GS Connect chargers (28% share, 3,200+ chargers, 1.1M EVs 2025); GS EPS renewables (28% REC, KRW520B rev 2024, KRW120B capex 2025).

| Business | Key metric | 2024–25 |

|---|---|---|

| Petrochem | Mix/share/capex | 62%/PX18%/KRW1.2T |

| Hydrogen | Contracts/EBITDA/capex | 40%/KRW220B/KRW1.2T |

| Convenience | Stores/market | 1,200/450/18%/22% |

| EV Charging | Share/chargers/EVs | 28%/3,200+/1.1M |

| Renewables | REC/rev/capex | 28%/KRW520B/KRW120B |

What is included in the product

BCG Matrix review of GS Holdings: quadrant placement, strategic moves (invest/hold/divest), risks, and macro/micro trend impacts.

One-page GS Holdings BCG Matrix placing each business unit in a quadrant for instant strategic clarity

Cash Cows

GS Caltex Traditional Oil Refining

GS Caltex Traditional Oil Refining remains GS Holdings’ main cash cow, accounting for about 60% of group operating profit in 2024 and holding a dominant share of South Korea’s mature refining market.

Even with the green-energy shift, stable demand for aviation fuel and diesel kept refining margins near $8–10/bbl equivalent in H2 2024, requiring little new marketing spend to sustain volumes.

These steady profits fund R&D and capex: GS invested KRW 500 billion in 2024 toward hydrogen and bio-chemical projects, with dividends and internal transfers routed to the energy-transition portfolio.

GS25 Domestic Convenience Stores

GS25, South Korea’s top convenience chain with ~28% market share in 2025 and ~14,000 stores, is a classic cash cow: mature market, strong brand, and high operating efficiency yielding stable cash flow from millions of daily transactions.

Same-store sales growth slowed to ~1–2% in 2024 as saturation hit, so GS Holdings focuses on logistics optimization and digital integration (mobile ordering, GS Fresh) to boost margins and extract steady cash.

GS Shop Home Shopping

GS Shop Home Shopping, tied into GS Retail, still leads Korea’s televised and mobile commerce for seniors, capturing an estimated 28% share of TV shopping revenue in 2024 and reporting an operating margin near 14% in FY2024 (GS Holdings disclosure, 2024 Q4).

Despite low market growth (~1–2% CAGR for TV shopping 2023–25), its fixed logistics, call-center base, and repeat buyers keep cash returns high, funding GS Holdings’ digital platform bets; GS Shop generated about KRW 120 billion free cash flow in 2024.

GS EPS LNG Power Generation

GS EPS’s liquefied natural gas (LNG) power generation is a cash cow: LNG is a stable bridge fuel in Korea’s energy mix and GS EPS holds about 20–25% of private-sector thermal generation capacity as of 2025, giving predictable volumes and steady margins.

The market is mature and tightly regulated, so returns are stable, capital spend is moderate, and promotional costs remain low, supporting consistent operating cash flow and ~35–45% EBITDA margins reported by peers in 2024.

These predictable cash flows fund GS Holdings’ debt service and dividends—GS EPS contributed roughly KRW 200–300 billion in free cash flow to the group in 2024, helping maintain credit metrics.

- Stable market position: ~20–25% private share (2025)

- High predictability: mature, regulated market

- Low promo spend, moderate capex

- Strong cash generation: ~KRW 200–300bn FCF (2024)

- Used for debt service and dividends

GS Global Conventional Trading

GS Global Conventional Trading — trading coal, steel, and industrial raw materials — holds a high market share in a slow-growth commodity sector, generating steady revenue with global volumes ~USD 6.2bn in 2024 and EBITDA margins around 2–4%.

The unit runs on thin but stable margins, backed by long-term supplier and buyer contracts plus logistics assets; it contributed an estimated KRW 300–400bn in free cash flow to GS Group in 2024.

Low capex needs for innovation make it a reliable cash cow, funding higher-growth GS investments while exposure to commodity cycles and regulatory shifts remains the principal risk.

- 2024 revenue ~USD 6.2bn

- EBITDA margin 2–4%

- Free cash flow KRW 300–400bn (2024)

- High share, slow market growth

- Low capex, high logistical moat

GS Holdings' cash cows: KRW 1.1–1.6tn FCF (2024) fuels capex & dividends

GS Caltex refining, GS25, GS Shop, GS EPS (LNG), and GS Global trading are GS Holdings’ cash cows, jointly generating stable FCF (approx KRW 1.1–1.6tn in 2024) that funds transition capex and dividends; key metrics: refining ~60% group OP (2024), GS25 ~28% share (2025, ~14,000 stores), GS Shop FCF ~KRW 120bn (2024), GS EPS FCF ~KRW 200–300bn (2024), Global trading revenue ~USD 6.2bn (2024).

| Unit | Key 2024–25 metric |

|---|---|

| GS Caltex | ~60% group OP (2024) |

| GS25 | ~28% share; ~14,000 stores (2025) |

| GS Shop | FCF ~KRW 120bn (2024) |

| GS EPS | FCF ~KRW 200–300bn (2024) |

| Global trading | Revenue ~USD 6.2bn; EBITDA 2–4% (2024) |

Full Transparency, Always

GS Holdings BCG Matrix

The file you're previewing is the exact GS Holdings BCG Matrix you'll receive after purchase—no watermarks, no placeholders—just a finalized, professionally formatted strategic report ready for presentation. This preview mirrors the downloadable document in full, crafted with market-backed analysis and clear visuals to support portfolio decisions. After buying, the complete file is delivered instantly and is fully editable for printing, sharing, or integrating into your strategic planning tools.