GS-Hydro Porter's Five Forces Analysis

Don't Miss the Bigger Picture

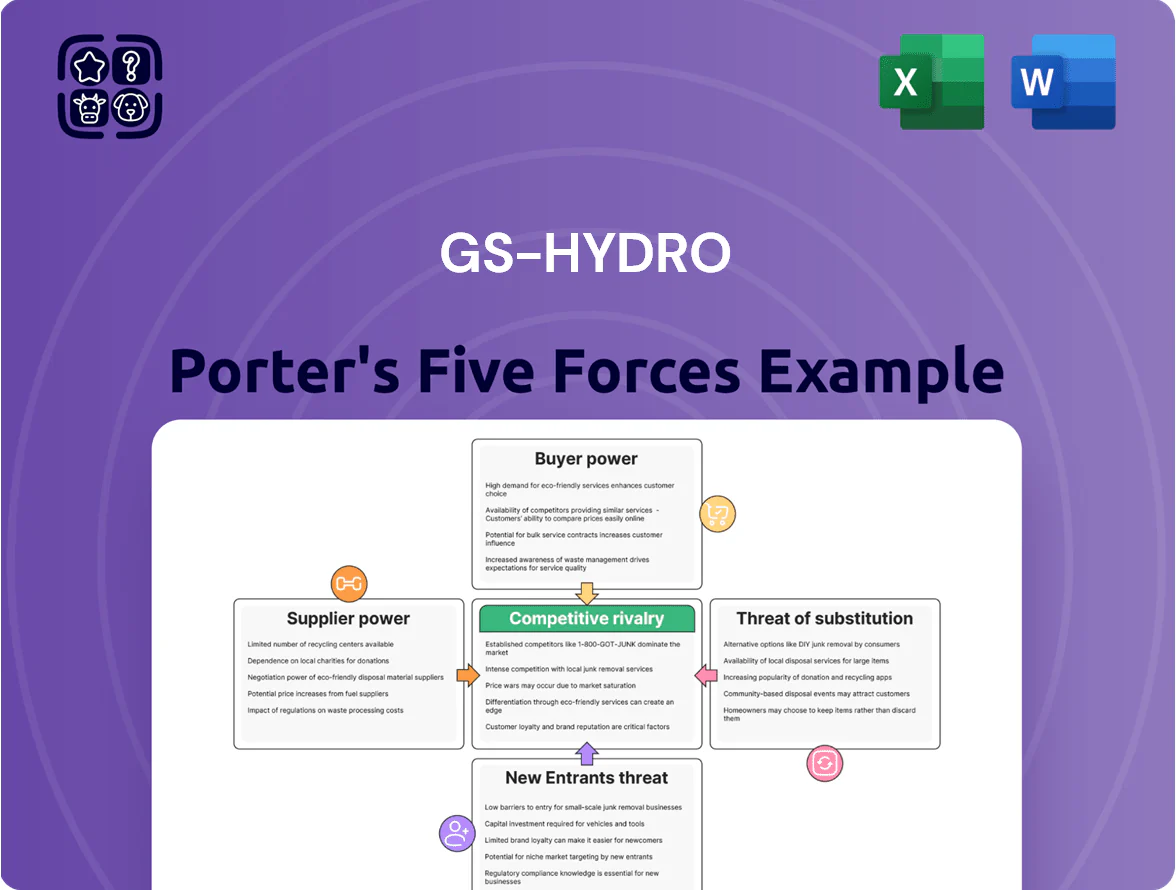

GS-Hydro faces moderate supplier power and differentiated tech advantages, while buyer concentration and capital-intensive barriers temper new entrants and substitutes; competitive rivalry centers on innovation, service breadth, and global reach.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore GS-Hydro’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material price volatility

High-grade carbon and stainless steel—GS-Hydro’s main inputs—track global commodity swings: stainless rose 24% in 2023–24 and alloy premiums spiked 15% by mid-2025. Suppliers hold leverage because a 10% metal-price rise adds roughly 6–8% to GS-Hydro flange and pipe COGS, squeezing margins unless passed to customers. Green-steel shifts cut premium-alloy availability by about 12% in 2025, concentrating supply among specialized mills and boosting their pricing power.

Specialized component dependency

GS-Hydro depends on a small set of certified suppliers for seals, O-rings and precision bolts that guarantee leak-free flanged systems; fewer than 10 global vendors meet the needed ISO 9001/AS9100 tolerances and NDT certifications.

That supplier concentration lets vendors set prices and 8–16 week lead times; in 2024 semiconductor and shipping delays pushed some seal lead times 35%, raising component spend by an estimated 4–6% for industrial fabricators.

Energy and logistics costs

Energy and logistics costs press supplier power: heavy piping needs high energy for welding and bending and special transport for 10–40 tonne modules, so energy and haulage suppliers can squeeze GS-Hydro’s margins.

In 2025 diesel averaged ~1.15 USD/liter in Europe and global container rates spiked 60% in 2021–22; fuel or container shortages can add 5–12% to landed costs for large orders.

Supplier consolidation in the steel industry

Ongoing consolidation in steel—led by 2023–2025 deals such as ArcelorMittal’s asset moves and Nippon Steel’s capacity deals—cut global primary steelmakers by ~15% among top 50 producers, strengthening suppliers vs mid-sized firms like GS-Hydro and raising input price leverage.

Larger, vertically integrated suppliers now negotiate longer contracts and higher minimum volumes, reducing GS-Hydro’s ability to pit vendors against each other for better terms.

- Top 50 steelmakers down ~15% (2023–2025)

- Longer supply contracts common—3–5 years

- Higher minimum order volumes limit small buyers

- Price pass-through risk increased

Stringent quality and certification standards

Suppliers to GS-Hydro must meet ISO 9001 and maritime certifications (e.g., DNV, Lloyds) and provide material certificates, creating a high barrier—only ~12% of applicants pass initial qualification based on industry averages for hydraulic OEMs in 2024.

Documented traceability and destructive/non-destructive testing (NDT) add procurement lead times of 8–16 weeks and switching costs that can exceed 1.5–3% of annual procurement spend, locking GS-Hydro to its certified vendor base.

- High entry barrier: strict ISO/DNV/Lloyds rules

- ~12% supplier qualification rate (2024 industry avg)

- 8–16 week lead times from testing/traceability

- Switching cost ~1.5–3% of annual spend

Supplier power squeezes margins: long lead times, price shocks add 6–12% COGS

Suppliers hold high bargaining power: concentrated certified steel and seal vendors, longer contracts (3–5y), and 8–16 week lead times raise switching costs (1.5–3% annual spend) and pass-through risk; metal-price swings (stainless +24% 2023–24) add ~6–8% to flange/pipe COGS per 10% price rise, while diesel ~1.15 USD/liter (2025) and container spikes can add 5–12% to landed costs.

| Metric | Value |

|---|---|

| Top-50 steelmakers change (2023–25) | -15% |

| Supplier qualification rate (2024) | ~12% |

| Lead times | 8–16 weeks |

| Switching cost | 1.5–3% annual spend |

What is included in the product

Tailored Porter’s Five Forces for GS-Hydro, revealing competitive intensity, buyer and supplier power, entry barriers, substitutes, and strategic vulnerabilities with actionable insights to guide pricing, growth, and defensive strategies.

A concise GS-Hydro Porter's Five Forces one-sheet that highlights competitive pressures and relief strategies for rapid boardroom decisions.

Customers Bargaining Power

Concentration of large-scale industrial buyers

The customer base in marine, offshore, and industrial sectors is concentrated among a few shipyards and energy conglomerates—top 10 buyers account for roughly 55% of orders—giving them strong leverage to demand volume discounts of 8–15% and extended payment terms (90–180 days).

These large buyers place bulk orders (often >€5m per contract) so GS-Hydro faces price pressure and margin compression; in 2024 GS-Hydro reported COGS rising 4% amid negotiated discounts.

Their early-stage influence on specifications forces GS-Hydro to provide bespoke hydraulic systems and integrated engineering, increasing R&D and project engineering hours by an estimated 20–30% per contract.

Availability of alternative piping technologies

Availability of alternative piping technologies—welded joints and mechanical couplings—gives buyers leverage; in 2024 roughly 40% of industrial piping contracts still specified welded systems, enabling competitive bids that compress GS-Hydro pricing.

Customers compare GS-Hydro’s higher upfront non-welded cost (often 10–30% premium) to lifecycle savings—clients cite 15–25% lower maintenance over 10 years—so GS-Hydro must prove NPV gains to win tenders.

Low switching costs for standard applications

In less specialized industrial uses, switching costs for piping systems are low, so buyers often choose on price; studies show price-sensitive procurement drives 60–80% of supplier switches in commodity hydraulic components (2023 supply-chain report). If a rival offers a similar flanged system at a 10–20% lower price, customers have little brand loyalty, forcing GS-Hydro to protect share via superior service and technical support.

Information transparency and digital procurement

By 2025, digital procurement platforms have pushed pricing and specs transparency: buyers can compare GS-Hydro piping costs and performance across vendors in minutes, cutting quoting time by ~40% and bid spreads by ~25% (McKinsey 2024 procurement report).

This reduces information asymmetry that let manufacturers keep margins via proprietary specs; GS-Hydro faces stronger price pressure as customers demand verifiable performance metrics and total cost of ownership data.

- Platform-driven quoting: -40% time

- Bid spread compression: -25%

- Global comparisons in minutes

- Higher demand for TCO and verified metrics

Sensitivity to capital expenditure cycles

GS-Hydro’s customers in oil, gas, and shipping face cyclical capex tied to commodity prices; for example, global oil capex fell about 24% in 2020 and remained 10% below 2019 levels through 2023, giving buyers leverage to delay projects.

During downturns customers demand deeper discounts and longer payment terms, pushing GS-Hydro to cut margins or offer price flexibility to keep a 2024 order backlog recovery intact.

- Clients: cyclical oil, gas, shipping

- Capex sensitivity: -24% (2020), ≈-10% vs 2019 through 2023

- Buyer tactics: delay projects, demand cost cuts

- GS-Hydro response: flexible pricing, margin pressure

Concentrated buyers squeeze margins—8–15% discounts, long terms; digital bids cut costs

Large, concentrated buyers (top 10 ≈55% orders) exert strong price and payment leverage—typical discounts 8–15%, terms 90–180 days—forcing bespoke specs (+20–30% engineering cost) and margin pressure; digital procurement cut quoting time ~40% and bid spreads ~25%, while welded alternatives keep price competition (40% of contracts).

| Metric | Value |

|---|---|

| Top-10 share | ≈55% |

| Discounts | 8–15% |

| Payment terms | 90–180 days |

| Engr. cost lift | 20–30% |

| Quote time | -40% |

| Bid spread | -25% |

Same Document Delivered

GS-Hydro Porter's Five Forces Analysis

This preview shows the exact GS-Hydro Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders, no mockups; fully formatted and ready for use.

You're viewing the actual, professionally written document; once you complete your purchase, you’ll get instant access to this same file for download and application.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

GS-Hydro faces moderate supplier power and differentiated tech advantages, while buyer concentration and capital-intensive barriers temper new entrants and substitutes; competitive rivalry centers on innovation, service breadth, and global reach.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore GS-Hydro’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw material price volatility

High-grade carbon and stainless steel—GS-Hydro’s main inputs—track global commodity swings: stainless rose 24% in 2023–24 and alloy premiums spiked 15% by mid-2025. Suppliers hold leverage because a 10% metal-price rise adds roughly 6–8% to GS-Hydro flange and pipe COGS, squeezing margins unless passed to customers. Green-steel shifts cut premium-alloy availability by about 12% in 2025, concentrating supply among specialized mills and boosting their pricing power.

Specialized component dependency

GS-Hydro depends on a small set of certified suppliers for seals, O-rings and precision bolts that guarantee leak-free flanged systems; fewer than 10 global vendors meet the needed ISO 9001/AS9100 tolerances and NDT certifications.

That supplier concentration lets vendors set prices and 8–16 week lead times; in 2024 semiconductor and shipping delays pushed some seal lead times 35%, raising component spend by an estimated 4–6% for industrial fabricators.

Energy and logistics costs

Energy and logistics costs press supplier power: heavy piping needs high energy for welding and bending and special transport for 10–40 tonne modules, so energy and haulage suppliers can squeeze GS-Hydro’s margins.

In 2025 diesel averaged ~1.15 USD/liter in Europe and global container rates spiked 60% in 2021–22; fuel or container shortages can add 5–12% to landed costs for large orders.

Supplier consolidation in the steel industry

Ongoing consolidation in steel—led by 2023–2025 deals such as ArcelorMittal’s asset moves and Nippon Steel’s capacity deals—cut global primary steelmakers by ~15% among top 50 producers, strengthening suppliers vs mid-sized firms like GS-Hydro and raising input price leverage.

Larger, vertically integrated suppliers now negotiate longer contracts and higher minimum volumes, reducing GS-Hydro’s ability to pit vendors against each other for better terms.

- Top 50 steelmakers down ~15% (2023–2025)

- Longer supply contracts common—3–5 years

- Higher minimum order volumes limit small buyers

- Price pass-through risk increased

Stringent quality and certification standards

Suppliers to GS-Hydro must meet ISO 9001 and maritime certifications (e.g., DNV, Lloyds) and provide material certificates, creating a high barrier—only ~12% of applicants pass initial qualification based on industry averages for hydraulic OEMs in 2024.

Documented traceability and destructive/non-destructive testing (NDT) add procurement lead times of 8–16 weeks and switching costs that can exceed 1.5–3% of annual procurement spend, locking GS-Hydro to its certified vendor base.

- High entry barrier: strict ISO/DNV/Lloyds rules

- ~12% supplier qualification rate (2024 industry avg)

- 8–16 week lead times from testing/traceability

- Switching cost ~1.5–3% of annual spend

Supplier power squeezes margins: long lead times, price shocks add 6–12% COGS

Suppliers hold high bargaining power: concentrated certified steel and seal vendors, longer contracts (3–5y), and 8–16 week lead times raise switching costs (1.5–3% annual spend) and pass-through risk; metal-price swings (stainless +24% 2023–24) add ~6–8% to flange/pipe COGS per 10% price rise, while diesel ~1.15 USD/liter (2025) and container spikes can add 5–12% to landed costs.

| Metric | Value |

|---|---|

| Top-50 steelmakers change (2023–25) | -15% |

| Supplier qualification rate (2024) | ~12% |

| Lead times | 8–16 weeks |

| Switching cost | 1.5–3% annual spend |

What is included in the product

Tailored Porter’s Five Forces for GS-Hydro, revealing competitive intensity, buyer and supplier power, entry barriers, substitutes, and strategic vulnerabilities with actionable insights to guide pricing, growth, and defensive strategies.

A concise GS-Hydro Porter's Five Forces one-sheet that highlights competitive pressures and relief strategies for rapid boardroom decisions.

Customers Bargaining Power

Concentration of large-scale industrial buyers

The customer base in marine, offshore, and industrial sectors is concentrated among a few shipyards and energy conglomerates—top 10 buyers account for roughly 55% of orders—giving them strong leverage to demand volume discounts of 8–15% and extended payment terms (90–180 days).

These large buyers place bulk orders (often >€5m per contract) so GS-Hydro faces price pressure and margin compression; in 2024 GS-Hydro reported COGS rising 4% amid negotiated discounts.

Their early-stage influence on specifications forces GS-Hydro to provide bespoke hydraulic systems and integrated engineering, increasing R&D and project engineering hours by an estimated 20–30% per contract.

Availability of alternative piping technologies

Availability of alternative piping technologies—welded joints and mechanical couplings—gives buyers leverage; in 2024 roughly 40% of industrial piping contracts still specified welded systems, enabling competitive bids that compress GS-Hydro pricing.

Customers compare GS-Hydro’s higher upfront non-welded cost (often 10–30% premium) to lifecycle savings—clients cite 15–25% lower maintenance over 10 years—so GS-Hydro must prove NPV gains to win tenders.

Low switching costs for standard applications

In less specialized industrial uses, switching costs for piping systems are low, so buyers often choose on price; studies show price-sensitive procurement drives 60–80% of supplier switches in commodity hydraulic components (2023 supply-chain report). If a rival offers a similar flanged system at a 10–20% lower price, customers have little brand loyalty, forcing GS-Hydro to protect share via superior service and technical support.

Information transparency and digital procurement

By 2025, digital procurement platforms have pushed pricing and specs transparency: buyers can compare GS-Hydro piping costs and performance across vendors in minutes, cutting quoting time by ~40% and bid spreads by ~25% (McKinsey 2024 procurement report).

This reduces information asymmetry that let manufacturers keep margins via proprietary specs; GS-Hydro faces stronger price pressure as customers demand verifiable performance metrics and total cost of ownership data.

- Platform-driven quoting: -40% time

- Bid spread compression: -25%

- Global comparisons in minutes

- Higher demand for TCO and verified metrics

Sensitivity to capital expenditure cycles

GS-Hydro’s customers in oil, gas, and shipping face cyclical capex tied to commodity prices; for example, global oil capex fell about 24% in 2020 and remained 10% below 2019 levels through 2023, giving buyers leverage to delay projects.

During downturns customers demand deeper discounts and longer payment terms, pushing GS-Hydro to cut margins or offer price flexibility to keep a 2024 order backlog recovery intact.

- Clients: cyclical oil, gas, shipping

- Capex sensitivity: -24% (2020), ≈-10% vs 2019 through 2023

- Buyer tactics: delay projects, demand cost cuts

- GS-Hydro response: flexible pricing, margin pressure

Concentrated buyers squeeze margins—8–15% discounts, long terms; digital bids cut costs

Large, concentrated buyers (top 10 ≈55% orders) exert strong price and payment leverage—typical discounts 8–15%, terms 90–180 days—forcing bespoke specs (+20–30% engineering cost) and margin pressure; digital procurement cut quoting time ~40% and bid spreads ~25%, while welded alternatives keep price competition (40% of contracts).

| Metric | Value |

|---|---|

| Top-10 share | ≈55% |

| Discounts | 8–15% |

| Payment terms | 90–180 days |

| Engr. cost lift | 20–30% |

| Quote time | -40% |

| Bid spread | -25% |

Same Document Delivered

GS-Hydro Porter's Five Forces Analysis

This preview shows the exact GS-Hydro Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders, no mockups; fully formatted and ready for use.

You're viewing the actual, professionally written document; once you complete your purchase, you’ll get instant access to this same file for download and application.