GS Retail Porter's Five Forces Analysis

Don't Miss the Bigger Picture

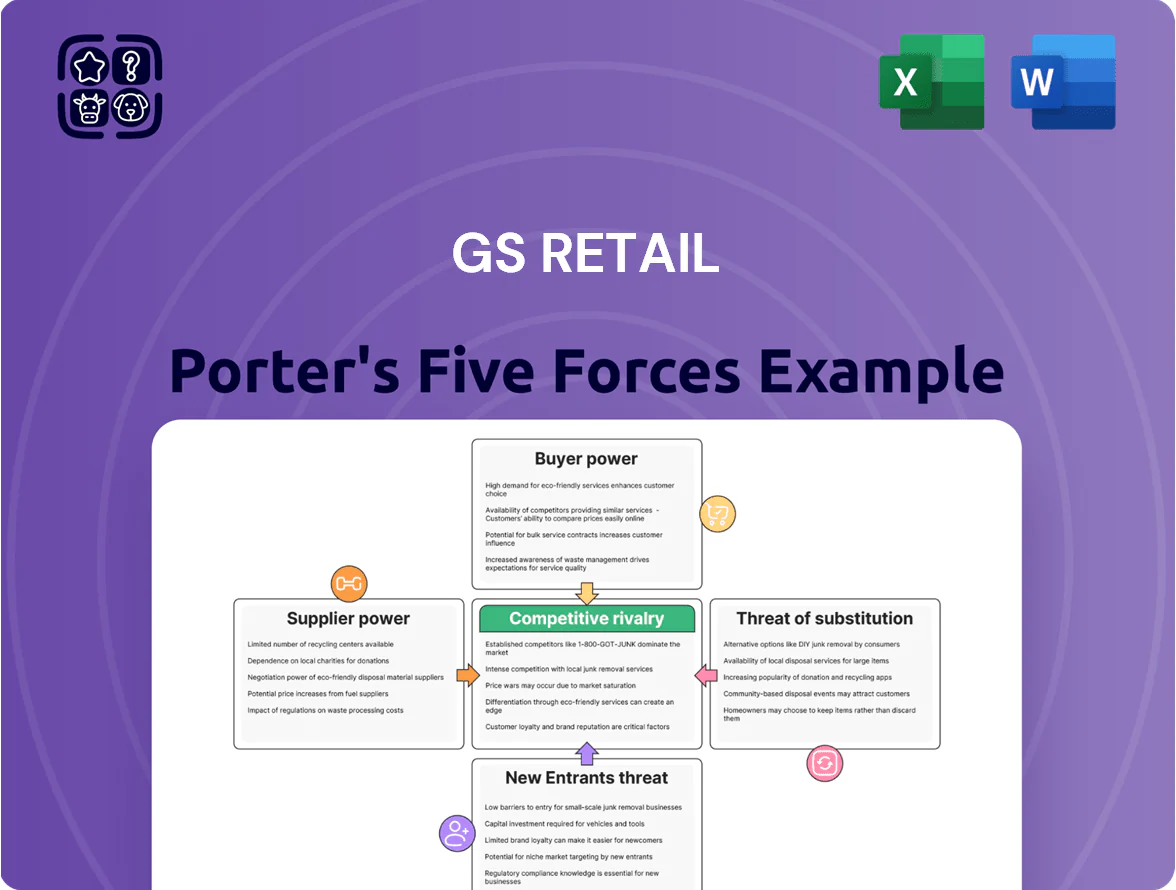

GS Retail operates in a highly competitive convenience-store market where supplier margins, intense rivalry, and evolving consumer preferences shape strategic choices; this snapshot highlights key pressures and potential vulnerabilities.

This brief only scratches the surface—unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable insights to inform investment and strategy decisions.

Suppliers Bargaining Power

Dominance of Large-Scale Procurement

GS Retail uses procurement across ~19,000 GS25 and GS THE FRESH stores (2025) to negotiate lower input costs, buying volumes that covered an estimated KRW 6–8 trillion in goods annually, so suppliers face pressure to accept GS terms.

By consolidating orders and logistics, GS Retail reduces supplier leverage; many manufacturers depend on its reach to access South Korea’s convenience and fresh channels, keeping GS as price maker in most negotiations.

Expansion of Private Brand Strategy

The aggressive expansion of GS Retail’s private brand YouUs cut reliance on national FMCG brands, with private label sales rising to 9.8% of GS Retail’s retail revenue in 2024 (vs 6.1% in 2021), reducing supplier leverage. By controlling product design, margins and shelf placement, GS can source or vertically integrate high-margin SKUs, creating a credible threat to bypass external suppliers. This shifts bargaining power: major FMCG firms now compete for limited shelf space against YouUs, pressuring their promo terms and slotting fees.

Fragmented Fresh Food Supply Chain

GS Retail sources fresh produce from thousands of local farms and small producers; in 2024 roughly 68% of its fresh supply came from suppliers with annual revenues under KRW 500m, giving GS Retail strong negotiating power over prices and 2024 procurement costs, which rose just 1.8% vs. market food inflation of 4.7%.

Sophisticated Logistics and Infrastructure

GS Retail’s ownership of advanced cold-chain logistics and 120+ distribution centers (2025: ~8.2 trillion KRW logistics assets) creates a market entry barrier suppliers must clear to reach its 13,000 stores.

Suppliers must integrate with GS Retail’s proprietary inventory-management systems (real-time SKU-level visibility), tying operations to GS processes and raising integration costs.

This technical lock-in raises supplier switching costs, boosting GS Retail’s leverage in pricing and long-term contracts.

- 120+ DCs; 8.2T KRW logistics assets (2025)

- 13,000 retail outlets nationwide (2025)

- Proprietary IMS requires API integration, real-time SKUs

- Higher switching costs → stronger supplier bargaining power for GS

Global Sourcing and Diversification

GS Retail sources roughly 28% of non-food inventory from overseas suppliers as of FY2024, reducing reliance on Korean vendors and limiting supplier pricing power.

The firm can switch vendors within 30–60 days for key SKUs, creating a practical hedge versus domestic supply shocks and inflation spikes (Korea CPI +2.5% in 2024).

No single local supplier controls >5% of category spend, so bargaining leverage stays with GS Retail during disruptions.

- 28% non-food imports (FY2024)

- 30–60 day vendor switch capability

- Single local supplier share <5%

- Domestic CPI +2.5% (2024)

GS Retail's Buying Power: KRW6–8T Spend, 13k Stores, 9.8% Private Brand

GS Retail wields strong supplier power: ~13,000 stores and 19,000 outlets (2025) drive KRW 6–8t annual buying, YouUs private brand = 9.8% revenue (2024), 120+ DCs and KRW 8.2t logistics assets (2025), 68% fresh from

| Metric | Value |

|---|---|

| Stores/outlets (2025) | 13,000 / 19,000 |

| Procurement spend | KRW 6–8 trillion |

| YouUs share (2024) | 9.8% |

| DCs / logistics assets (2025) | 120+ / KRW 8.2t |

| Fresh from small suppliers (2024) | 68% |

| Non-food imports (FY2024) | 28% |

| Vendor switch time | 30–60 days |

What is included in the product

Tailored Porter's Five Forces analysis of GS Retail uncovering competitive drivers, buyer and supplier influence, entry barriers, substitutes, and disruptive threats that shape its pricing power and profitability.

A concise Porter's Five Forces snapshot for GS Retail—instantly highlights competitive pressures and strategic levers to accelerate decision-making and reduce analysis time.

Customers Bargaining Power

Low Switching Costs for Consumers

South Korea has about 120,000 convenience stores nationwide; Seoul density exceeds 1 store per 300 residents, so consumers can switch to CU or 7-Eleven with near-zero cost and no penalty.

Most locations sit minutes apart, making proximity trump loyalty and pressuring GS Retail to win on service and store experience to stem churn; GS Retail reported 2024 convenience-store same-store sales growth of 3.8%, showing the margin for error.

Digital Price Transparency and Comparison

Mobile apps let consumers compare prices and promotions in real time across retailers; in South Korea 91% of shoppers used mobile price checks in 2024, raising price sensitivity for convenience chains like GS Retail.

GS25s Our Neighborhood GS app, with 8.2 million downloads by Dec 2025, is used to hunt discounts and check stock before visits, shifting bargaining leverage to informed buyers.

This transparency forces GS Retail to run tighter, often daily, price promotions and margin-sacrificing loyalty offers to retain traffic; same-store sales growth was 3.6% in 2024, reflecting competitive pressure.

High Sensitivity to Promotional Activity

South Korean shoppers respond strongly to 1+1/2+1 promotions, with Korea Consumer Agency surveys (2024) showing 62% buy mainly during promotions, so demand is event-driven and loyalty weak.

That shifts price power to buyers: GS Retail must match perceived value, not brand, or sales migrate to rivals during promo windows.

GS Retail reported 2024 convenience-store same-store sales growth 3.8% but relied on frequent promos; marketing spend rose 7% YoY to sustain traffic.

Demand for Premium Convenience

Demand for premium convenience is rising: South Korea's ready-to-eat meal market grew 8.7% in 2024 to KRW 6.2 trillion, and 62% of urban consumers reported preferring premium/healthy options in a 2025 survey, giving buyers leverage to reject low-quality substitutes.

GS Retail must refresh assortments frequently—launching premium meal lines and sourcing higher-grade produce—to retain shoppers and protect gross margins under rising customer quality expectations.

- RTE market +8.7% in 2024 to KRW 6.2T

- 62% of urban consumers prefer premium/healthy (2025)

- Frequent SKU upgrades raise procurement and COGS pressure

Influence of Delivery and Quick Commerce

The rise of quick commerce shifted expectations to sub-30-minute delivery and smooth online-to-offline (O2O) flows; in Korea quick commerce orders grew ~65% year-on-year in 2024, raising churn if GS Retail's app or delivery lags.

Buyers now insist GS Retail match convenience of physical stores via digital platforms; in 2024 GS Retail’s delivery share vs dedicated platforms fell where app NPS underperforms by >10 points.

When delivery or UX fails, customers migrate to dedicated apps—market surveys show 42% switch after two poor deliveries.

- Quick commerce +65% YoY growth (Korea, 2024)

- App NPS gap >10 points drives churn

- 42% switch after two poor deliveries

Dense stores + mobile checks squeeze GS Retail—promos up, margins pressured

High store density (≈120,000 nationwide; Seoul >1/300 residents) and mobile price checks (91% in 2024) give buyers strong switching power, forcing GS Retail into frequent promotions and SKU upgrades; 2024 same-store sales +3.8% came with higher marketing (+7% YoY) and margin pressure while RTE market grew 8.7% to KRW 6.2T.

| Metric | 2024/2025 |

|---|---|

| Store density | ≈120,000 |

| Mobile price checks | 91% (2024) |

| SSS growth | +3.8% (2024) |

| RTE market | KRW 6.2T (+8.7%) |

Preview Before You Purchase

GS Retail Porter's Five Forces Analysis

This preview shows the exact GS Retail Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no edits needed; the full, professionally formatted document is ready for download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

GS Retail operates in a highly competitive convenience-store market where supplier margins, intense rivalry, and evolving consumer preferences shape strategic choices; this snapshot highlights key pressures and potential vulnerabilities.

This brief only scratches the surface—unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable insights to inform investment and strategy decisions.

Suppliers Bargaining Power

Dominance of Large-Scale Procurement

GS Retail uses procurement across ~19,000 GS25 and GS THE FRESH stores (2025) to negotiate lower input costs, buying volumes that covered an estimated KRW 6–8 trillion in goods annually, so suppliers face pressure to accept GS terms.

By consolidating orders and logistics, GS Retail reduces supplier leverage; many manufacturers depend on its reach to access South Korea’s convenience and fresh channels, keeping GS as price maker in most negotiations.

Expansion of Private Brand Strategy

The aggressive expansion of GS Retail’s private brand YouUs cut reliance on national FMCG brands, with private label sales rising to 9.8% of GS Retail’s retail revenue in 2024 (vs 6.1% in 2021), reducing supplier leverage. By controlling product design, margins and shelf placement, GS can source or vertically integrate high-margin SKUs, creating a credible threat to bypass external suppliers. This shifts bargaining power: major FMCG firms now compete for limited shelf space against YouUs, pressuring their promo terms and slotting fees.

Fragmented Fresh Food Supply Chain

GS Retail sources fresh produce from thousands of local farms and small producers; in 2024 roughly 68% of its fresh supply came from suppliers with annual revenues under KRW 500m, giving GS Retail strong negotiating power over prices and 2024 procurement costs, which rose just 1.8% vs. market food inflation of 4.7%.

Sophisticated Logistics and Infrastructure

GS Retail’s ownership of advanced cold-chain logistics and 120+ distribution centers (2025: ~8.2 trillion KRW logistics assets) creates a market entry barrier suppliers must clear to reach its 13,000 stores.

Suppliers must integrate with GS Retail’s proprietary inventory-management systems (real-time SKU-level visibility), tying operations to GS processes and raising integration costs.

This technical lock-in raises supplier switching costs, boosting GS Retail’s leverage in pricing and long-term contracts.

- 120+ DCs; 8.2T KRW logistics assets (2025)

- 13,000 retail outlets nationwide (2025)

- Proprietary IMS requires API integration, real-time SKUs

- Higher switching costs → stronger supplier bargaining power for GS

Global Sourcing and Diversification

GS Retail sources roughly 28% of non-food inventory from overseas suppliers as of FY2024, reducing reliance on Korean vendors and limiting supplier pricing power.

The firm can switch vendors within 30–60 days for key SKUs, creating a practical hedge versus domestic supply shocks and inflation spikes (Korea CPI +2.5% in 2024).

No single local supplier controls >5% of category spend, so bargaining leverage stays with GS Retail during disruptions.

- 28% non-food imports (FY2024)

- 30–60 day vendor switch capability

- Single local supplier share <5%

- Domestic CPI +2.5% (2024)

GS Retail's Buying Power: KRW6–8T Spend, 13k Stores, 9.8% Private Brand

GS Retail wields strong supplier power: ~13,000 stores and 19,000 outlets (2025) drive KRW 6–8t annual buying, YouUs private brand = 9.8% revenue (2024), 120+ DCs and KRW 8.2t logistics assets (2025), 68% fresh from

| Metric | Value |

|---|---|

| Stores/outlets (2025) | 13,000 / 19,000 |

| Procurement spend | KRW 6–8 trillion |

| YouUs share (2024) | 9.8% |

| DCs / logistics assets (2025) | 120+ / KRW 8.2t |

| Fresh from small suppliers (2024) | 68% |

| Non-food imports (FY2024) | 28% |

| Vendor switch time | 30–60 days |

What is included in the product

Tailored Porter's Five Forces analysis of GS Retail uncovering competitive drivers, buyer and supplier influence, entry barriers, substitutes, and disruptive threats that shape its pricing power and profitability.

A concise Porter's Five Forces snapshot for GS Retail—instantly highlights competitive pressures and strategic levers to accelerate decision-making and reduce analysis time.

Customers Bargaining Power

Low Switching Costs for Consumers

South Korea has about 120,000 convenience stores nationwide; Seoul density exceeds 1 store per 300 residents, so consumers can switch to CU or 7-Eleven with near-zero cost and no penalty.

Most locations sit minutes apart, making proximity trump loyalty and pressuring GS Retail to win on service and store experience to stem churn; GS Retail reported 2024 convenience-store same-store sales growth of 3.8%, showing the margin for error.

Digital Price Transparency and Comparison

Mobile apps let consumers compare prices and promotions in real time across retailers; in South Korea 91% of shoppers used mobile price checks in 2024, raising price sensitivity for convenience chains like GS Retail.

GS25s Our Neighborhood GS app, with 8.2 million downloads by Dec 2025, is used to hunt discounts and check stock before visits, shifting bargaining leverage to informed buyers.

This transparency forces GS Retail to run tighter, often daily, price promotions and margin-sacrificing loyalty offers to retain traffic; same-store sales growth was 3.6% in 2024, reflecting competitive pressure.

High Sensitivity to Promotional Activity

South Korean shoppers respond strongly to 1+1/2+1 promotions, with Korea Consumer Agency surveys (2024) showing 62% buy mainly during promotions, so demand is event-driven and loyalty weak.

That shifts price power to buyers: GS Retail must match perceived value, not brand, or sales migrate to rivals during promo windows.

GS Retail reported 2024 convenience-store same-store sales growth 3.8% but relied on frequent promos; marketing spend rose 7% YoY to sustain traffic.

Demand for Premium Convenience

Demand for premium convenience is rising: South Korea's ready-to-eat meal market grew 8.7% in 2024 to KRW 6.2 trillion, and 62% of urban consumers reported preferring premium/healthy options in a 2025 survey, giving buyers leverage to reject low-quality substitutes.

GS Retail must refresh assortments frequently—launching premium meal lines and sourcing higher-grade produce—to retain shoppers and protect gross margins under rising customer quality expectations.

- RTE market +8.7% in 2024 to KRW 6.2T

- 62% of urban consumers prefer premium/healthy (2025)

- Frequent SKU upgrades raise procurement and COGS pressure

Influence of Delivery and Quick Commerce

The rise of quick commerce shifted expectations to sub-30-minute delivery and smooth online-to-offline (O2O) flows; in Korea quick commerce orders grew ~65% year-on-year in 2024, raising churn if GS Retail's app or delivery lags.

Buyers now insist GS Retail match convenience of physical stores via digital platforms; in 2024 GS Retail’s delivery share vs dedicated platforms fell where app NPS underperforms by >10 points.

When delivery or UX fails, customers migrate to dedicated apps—market surveys show 42% switch after two poor deliveries.

- Quick commerce +65% YoY growth (Korea, 2024)

- App NPS gap >10 points drives churn

- 42% switch after two poor deliveries

Dense stores + mobile checks squeeze GS Retail—promos up, margins pressured

High store density (≈120,000 nationwide; Seoul >1/300 residents) and mobile price checks (91% in 2024) give buyers strong switching power, forcing GS Retail into frequent promotions and SKU upgrades; 2024 same-store sales +3.8% came with higher marketing (+7% YoY) and margin pressure while RTE market grew 8.7% to KRW 6.2T.

| Metric | 2024/2025 |

|---|---|

| Store density | ≈120,000 |

| Mobile price checks | 91% (2024) |

| SSS growth | +3.8% (2024) |

| RTE market | KRW 6.2T (+8.7%) |

Preview Before You Purchase

GS Retail Porter's Five Forces Analysis

This preview shows the exact GS Retail Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders, no edits needed; the full, professionally formatted document is ready for download and use the moment you buy.