Green Thumb SWOT Analysis

Your Strategic Toolkit Starts Here

Green Thumb’s SWOT preview highlights its strong brand, scalable retail model, and regulatory resilience, but also flags supply-chain risks and competitive pressure; uncover how these factors translate to valuation, strategy, and growth in the full report. Purchase the complete SWOT analysis to get a professionally formatted Word report and editable Excel matrix—designed for investors, advisors, and strategists who need actionable, research-backed insights.

Strengths

Leading Market Position in Key States

Green Thumb Brands holds top market share in Illinois and New Jersey—states with limited-license regimes—posting combined FY2024 retail revenues of about $420 million, helping gross margins stay ~28% versus ~18% in open markets.

Its Rise dispensary network (over 60 stores in those states by Dec 31, 2024) strengthens brand loyalty and contributed roughly 35% of company-wide retail same-store sales in 2024.

Strong Financial Performance and Cash Flow

Unlike many peers, Green Thumb Growth (CSE: GTII; OTCQX: GTBIF) has generated positive operating cash flow every quarter since 2021, producing $172.4 million cash from operations in FY2024, giving it a clear edge in a capital-constrained cannabis sector.

This cash strength funds organic expansion and acquisitions without heavy equity raises; Green Thumb ended FY2024 with $195 million in cash and $320 million net debt, keeping leverage lower than several major multi-state operators.

Diverse and Recognized Brand Portfolio

Green Thumb Brands owns high-recognition labels like RYTHM, Dogwalkers, and Incredibles, covering premium flower, value flower, and edibles segments to reach varied consumers.

In 2024 GTB reported net revenue of $665.2 million and retail same-store sales growth of 6.3%, showing brand pull in a crowded market.

Strong brand equity preserved wholesale shelf space: top-3 SKUs accounted for ~18% of wholesale volume in 2024, sustaining distributor relationships and promotional leverage.

Effective Vertical Integration Strategy

Green Thumb’s vertical integration captures margins across cultivation, processing, and retail, contributing to adjusted gross margin of about 45% in FY2024 (Green Thumb Industries, 2024).

Controlling the chain improves quality and cut supply-disruption risk—inventory turnover rose to 6.2x in 2024, lowering dependence on wholesale price swings.

Direct retail data informs product launches and marketing; stores generated 38% of revenue in 2024, enabling faster SKU optimization.

- 45% adjusted gross margin (FY2024)

- 6.2x inventory turnover (2024)

- Stores = 38% revenue (2024)

Disciplined Management and Capital Allocation

Market-leading IL/NJ retailer: $420M revenue, 45% gross margin, $172M CFO, 60+ stores

Market leader in IL/NJ with FY2024 revenue concentration ~420M and adjusted gross margin ~45%; Rise retail (60+ stores) drove ~35% of same-store sales and 38% of revenue; positive operating cash flow every quarter since 2021 with $172.4M CFO in FY2024, $195M cash and $320M net debt; disciplined capex ≤8% revenue, inventory turnover 6.2x.

| Metric | Value |

|---|---|

| FY2024 retail revenue (IL+NJ) | $420M |

| Adjusted gross margin (FY2024) | 45% |

| CFO (FY2024) | $172.4M |

| Cash / Net debt (FY2024) | $195M / $320M |

| Rise stores (Dec 31, 2024) | 60+ |

| Inventory turnover (2024) | 6.2x |

What is included in the product

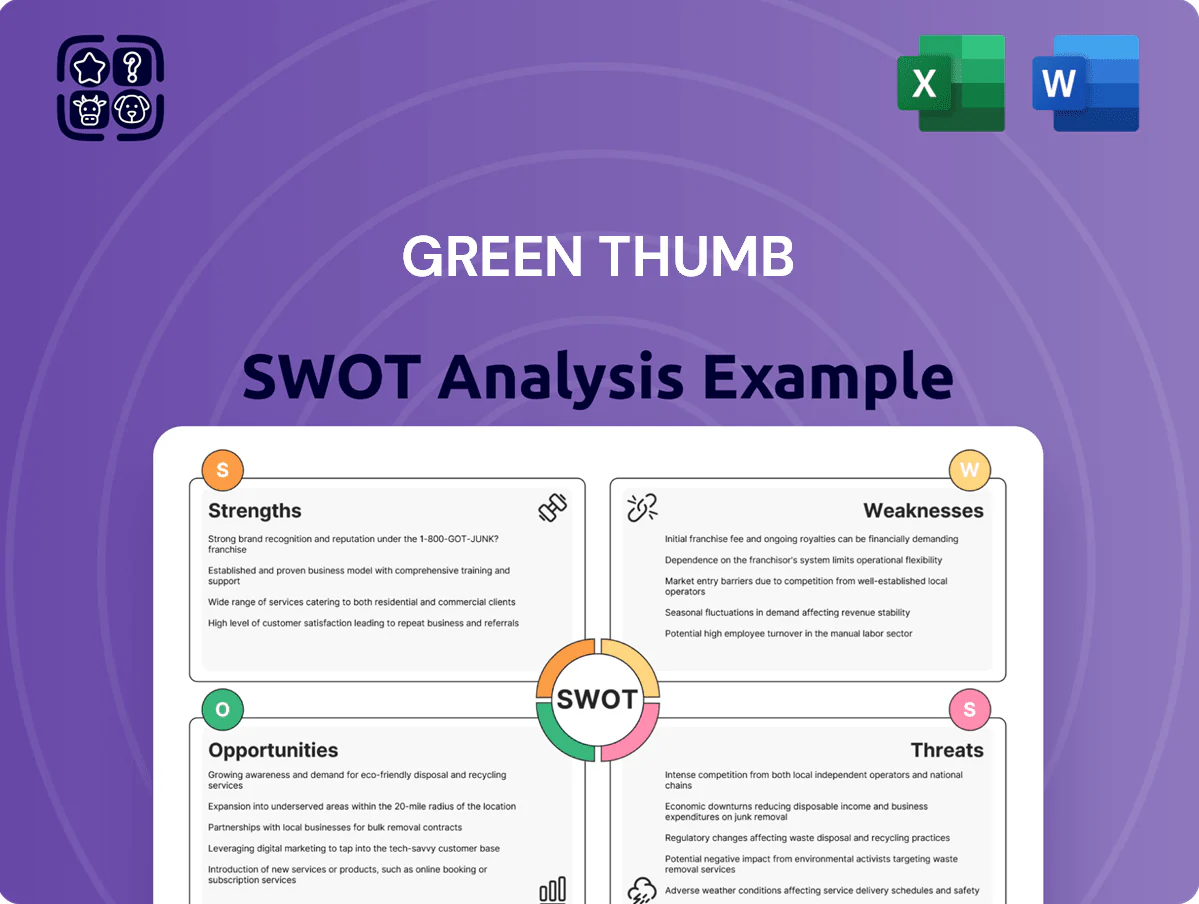

Provides a concise SWOT overview of Green Thumb, outlining its core strengths and weaknesses alongside market opportunities and external threats shaping its strategic direction.

Delivers a focused SWOT snapshot tailored for Green Thumb to quickly identify strategic levers and pain-point remedies for management action.

Weaknesses

Continued Impact of 280E Tax Restrictions

Despite progress toward rescheduling, Section 280E historically raised Green Thumb Growth (GTI) effective tax rates to ~60% on cannabis income, cutting 2019–2023 cumulative free cash flow by an estimated $350–450M and limiting reinvestment in store rollouts.

High Complexity in Multi-State Operations

Operating across 30+ state jurisdictions adds major legal and admin overhead—Green Thumb reported $42.3M in compliance and SG&A costs in FY2024, up 18% year-over-year, driven by state-specific packaging, testing, and distribution rules that block national scale economies. Fragmentation raises compliance error risk: the industry average fine per violation was $1.2M in 2024, and license revocations have hit 4% of operators, exposing Green Thumb to material regulatory and financial downside.

Reliance on High-Cost Capital Markets

Green Thumb faces higher borrowing costs due to federal cannabis illegality; its 2024 effective interest on debt averaged ~9–11% vs 4–6% for CPG peers, per company filings and industry reports.

Limited access to FDIC banks and institutional loans forces use of private debt and equity, raising weighted average cost of capital and diluting shareholders.

This higher cost constrains capex: planned 2025 facility expansions of ~$120m may slow or need phased builds.

Vulnerability to Wholesale Price Compression

Green Thumb faces downward wholesale price pressure: U.S. adult-use flower wholesale fell ~25% in 2024 in mature states, squeezing gross margins when supply outpaces demand.

If Green Thumb’s cost per gram doesn’t drop with scale, a 10–15% price cut can cut EBITDA margin by several percentage points; premium pricing needs ~5–10% higher R&D and marketing spend to sustain.

- Wholesale decline ~25% (2024, mature states)

- Price cuts of 10–15% → EBITDA fall several pts

- Premium sustainment needs ~5–10% extra R&D/marketing

Infrastructure and Maintenance Costs

- 2023–24 capex $210M

- Upgrade cost increase 10–25%

- High fixed costs raise margin risk

Section 280E, high debt costs and wholesale drops squeeze cash, margins and growth

High effective tax rates (Section 280E) cut 2019–2023 FCF by ~$350–450M and keep cash reinvestment tight; FY2024 compliance/SG&A rose to $42.3M (+18% YoY).

Federal illegality drives debt costs ~9–11% (2024) and forces private financing, raising WACC and diluting equity; 2023–24 capex was $210M, with upgrades adding 10–25%.

Wholesale prices fell ~25% (2024 mature states), a 10–15% price cut can shave several EBITDA pts.

| Metric | Value (2024) |

|---|---|

| Compliance/SG&A | $42.3M |

| Capex 2023–24 | $210M |

| Debt cost | ~9–11% |

| Wholesale decline | ~25% |

| 2019–23 FCF hit | $350–450M |

Same Document Delivered

Green Thumb SWOT Analysis

This is the actual Green Thumb SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get; buy to unlock the complete, editable version.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Strategic Toolkit Starts Here

Green Thumb’s SWOT preview highlights its strong brand, scalable retail model, and regulatory resilience, but also flags supply-chain risks and competitive pressure; uncover how these factors translate to valuation, strategy, and growth in the full report. Purchase the complete SWOT analysis to get a professionally formatted Word report and editable Excel matrix—designed for investors, advisors, and strategists who need actionable, research-backed insights.

Strengths

Leading Market Position in Key States

Green Thumb Brands holds top market share in Illinois and New Jersey—states with limited-license regimes—posting combined FY2024 retail revenues of about $420 million, helping gross margins stay ~28% versus ~18% in open markets.

Its Rise dispensary network (over 60 stores in those states by Dec 31, 2024) strengthens brand loyalty and contributed roughly 35% of company-wide retail same-store sales in 2024.

Strong Financial Performance and Cash Flow

Unlike many peers, Green Thumb Growth (CSE: GTII; OTCQX: GTBIF) has generated positive operating cash flow every quarter since 2021, producing $172.4 million cash from operations in FY2024, giving it a clear edge in a capital-constrained cannabis sector.

This cash strength funds organic expansion and acquisitions without heavy equity raises; Green Thumb ended FY2024 with $195 million in cash and $320 million net debt, keeping leverage lower than several major multi-state operators.

Diverse and Recognized Brand Portfolio

Green Thumb Brands owns high-recognition labels like RYTHM, Dogwalkers, and Incredibles, covering premium flower, value flower, and edibles segments to reach varied consumers.

In 2024 GTB reported net revenue of $665.2 million and retail same-store sales growth of 6.3%, showing brand pull in a crowded market.

Strong brand equity preserved wholesale shelf space: top-3 SKUs accounted for ~18% of wholesale volume in 2024, sustaining distributor relationships and promotional leverage.

Effective Vertical Integration Strategy

Green Thumb’s vertical integration captures margins across cultivation, processing, and retail, contributing to adjusted gross margin of about 45% in FY2024 (Green Thumb Industries, 2024).

Controlling the chain improves quality and cut supply-disruption risk—inventory turnover rose to 6.2x in 2024, lowering dependence on wholesale price swings.

Direct retail data informs product launches and marketing; stores generated 38% of revenue in 2024, enabling faster SKU optimization.

- 45% adjusted gross margin (FY2024)

- 6.2x inventory turnover (2024)

- Stores = 38% revenue (2024)

Disciplined Management and Capital Allocation

Market-leading IL/NJ retailer: $420M revenue, 45% gross margin, $172M CFO, 60+ stores

Market leader in IL/NJ with FY2024 revenue concentration ~420M and adjusted gross margin ~45%; Rise retail (60+ stores) drove ~35% of same-store sales and 38% of revenue; positive operating cash flow every quarter since 2021 with $172.4M CFO in FY2024, $195M cash and $320M net debt; disciplined capex ≤8% revenue, inventory turnover 6.2x.

| Metric | Value |

|---|---|

| FY2024 retail revenue (IL+NJ) | $420M |

| Adjusted gross margin (FY2024) | 45% |

| CFO (FY2024) | $172.4M |

| Cash / Net debt (FY2024) | $195M / $320M |

| Rise stores (Dec 31, 2024) | 60+ |

| Inventory turnover (2024) | 6.2x |

What is included in the product

Provides a concise SWOT overview of Green Thumb, outlining its core strengths and weaknesses alongside market opportunities and external threats shaping its strategic direction.

Delivers a focused SWOT snapshot tailored for Green Thumb to quickly identify strategic levers and pain-point remedies for management action.

Weaknesses

Continued Impact of 280E Tax Restrictions

Despite progress toward rescheduling, Section 280E historically raised Green Thumb Growth (GTI) effective tax rates to ~60% on cannabis income, cutting 2019–2023 cumulative free cash flow by an estimated $350–450M and limiting reinvestment in store rollouts.

High Complexity in Multi-State Operations

Operating across 30+ state jurisdictions adds major legal and admin overhead—Green Thumb reported $42.3M in compliance and SG&A costs in FY2024, up 18% year-over-year, driven by state-specific packaging, testing, and distribution rules that block national scale economies. Fragmentation raises compliance error risk: the industry average fine per violation was $1.2M in 2024, and license revocations have hit 4% of operators, exposing Green Thumb to material regulatory and financial downside.

Reliance on High-Cost Capital Markets

Green Thumb faces higher borrowing costs due to federal cannabis illegality; its 2024 effective interest on debt averaged ~9–11% vs 4–6% for CPG peers, per company filings and industry reports.

Limited access to FDIC banks and institutional loans forces use of private debt and equity, raising weighted average cost of capital and diluting shareholders.

This higher cost constrains capex: planned 2025 facility expansions of ~$120m may slow or need phased builds.

Vulnerability to Wholesale Price Compression

Green Thumb faces downward wholesale price pressure: U.S. adult-use flower wholesale fell ~25% in 2024 in mature states, squeezing gross margins when supply outpaces demand.

If Green Thumb’s cost per gram doesn’t drop with scale, a 10–15% price cut can cut EBITDA margin by several percentage points; premium pricing needs ~5–10% higher R&D and marketing spend to sustain.

- Wholesale decline ~25% (2024, mature states)

- Price cuts of 10–15% → EBITDA fall several pts

- Premium sustainment needs ~5–10% extra R&D/marketing

Infrastructure and Maintenance Costs

- 2023–24 capex $210M

- Upgrade cost increase 10–25%

- High fixed costs raise margin risk

Section 280E, high debt costs and wholesale drops squeeze cash, margins and growth

High effective tax rates (Section 280E) cut 2019–2023 FCF by ~$350–450M and keep cash reinvestment tight; FY2024 compliance/SG&A rose to $42.3M (+18% YoY).

Federal illegality drives debt costs ~9–11% (2024) and forces private financing, raising WACC and diluting equity; 2023–24 capex was $210M, with upgrades adding 10–25%.

Wholesale prices fell ~25% (2024 mature states), a 10–15% price cut can shave several EBITDA pts.

| Metric | Value (2024) |

|---|---|

| Compliance/SG&A | $42.3M |

| Capex 2023–24 | $210M |

| Debt cost | ~9–11% |

| Wholesale decline | ~25% |

| 2019–23 FCF hit | $350–450M |

Same Document Delivered

Green Thumb SWOT Analysis

This is the actual Green Thumb SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get; buy to unlock the complete, editable version.