Guotai Junan Securities Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

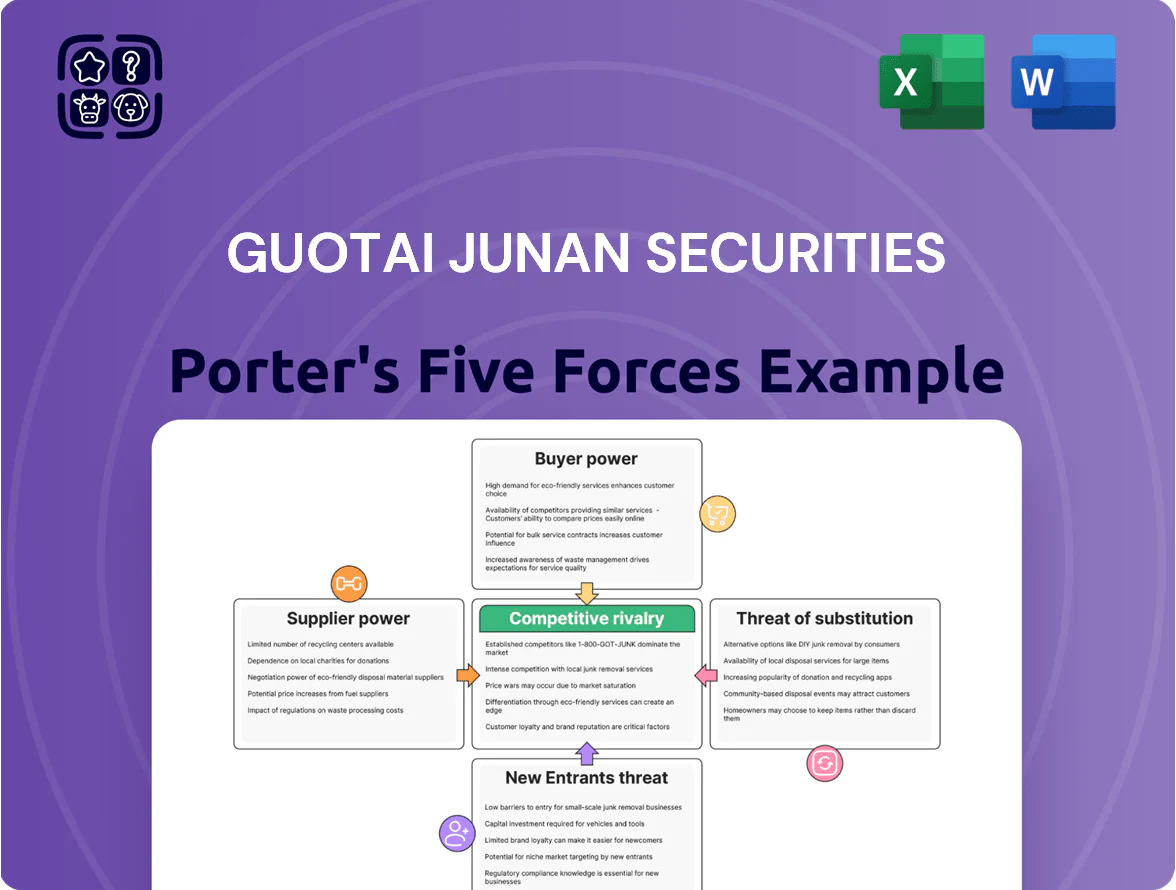

Guotai Junan faces intense rivalry and regulatory scrutiny, with strong buyer bargaining from institutional clients and moderate supplier influence tied to technology and capital access; threats from fintech entrants and substitutes are rising but incumbency and brand scale remain key defenses. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Guotai Junan Securities’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarcity of elite financial and tech talent

The demand for investment bankers, quants, and fintech developers in China stayed very high through 2025, with job postings for quant roles up 28% year-on-year in 2024 and fintech hiring budgets rising 22% per a ChinaTech HR survey (Dec 2024). Guotai Junan must match market-leading pay—senior quants fetched total comp of RMB 1.2–2.5m in 2024—to retain talent driving digital transformation. This reliance gives star hires and specialized agencies strong bargaining power over salary, equity, and remote-work terms, raising fixed-cost risk for the firm.

Dependence on global data and technology providers

Guotai Junan depends on global real-time data and trading systems from vendors like Bloomberg and Wind; 2024 vendor fees estimated at 0.4–0.7% of operating costs, and 60–80% of trading desks run on third-party platforms.

Cloud and fintech partners (Alibaba Cloud, Huawei Cloud, local middleware firms) host trading engines and data lakes; multiyear contracts and integration raise switching costs—migration could take 9–18 months and cost ~RMB 50–150m.

These factors give suppliers pricing power: limited substitutes, high exit costs, and concentrated vendor market share (top 3 suppliers ~70% of enterprise market), letting them sustain margins and firm pricing.

Influence of financial exchanges and clearing houses

Guotai Junan relies on the Shanghai and Shenzhen Stock Exchanges for market access and trade execution; these state-regulated monopolies set listing rules, fee schedules, and technical protocols that affect all brokers.

In 2024 the exchanges processed ~76 trillion RMB in trading value (Shanghai 52T, Shenzhen 24T), so fee changes or tech disruptions materially hit Guotai Junan’s revenues and operations.

The firm has negligible bargaining power over these systemic suppliers and must comply with any regulatory or operational shifts, absorbing costs or changing IT and compliance workflows quickly.

Cost of capital from institutional lenders

Guotai Junan depends on steady access to interbank loans and institutional bonds to fund proprietary trading and margin lending; in 2024 it held short-term debt and repo lines totaling about RMB 120 billion, making supplier rates material to profits.

Large state banks and bond funds can push spreads: when PBOC tightened in 2023–2024, 1-year SHIBOR rose from ~1.9% (Jan 2023) to ~2.8% (Dec 2024), raising funding costs and pressuring net interest margins.

Wholesale liquidity swings and central bank policy moves thus directly alter Guotai Junan’s interest expense and capital allocation decisions, increasing supplier bargaining power.

- RMB 120bn short-term funding (2024)

- SHIBOR 1y: ~1.9% → ~2.8% (2023–2024)

- State banks + bond funds = pricing power

- Policy rate shifts drive interest expense

Specialized legal and compliance consultancies

With China tightening financial rules by 2025, specialized legal and audit firms are critical for Guotai Junan Securities, providing certifications for cross-border deals and HK/SH listings; independent-verification mandates give these suppliers moderate fee leverage. In 2024–25, demand rose—lawyer-led compliance cases up ~18% and audit reviews for IPOs increased ~22%—so suppliers can demand premium rates but competition limits outsized price hikes.

- Regulatory tightening 2023–25: higher demand

- Compliance cases +18% (2024)

- IPO audit reviews +22% (2024–25)

- Moderate bargaining power: mandated role, but competitive market

Suppliers Dictate Costs & Risk: Talent, Data, Cloud, Funding, Exchanges, Advisers

Suppliers hold significant power: talent (senior quants RMB 1.2–2.5m), data vendors (Bloomberg/Wind fees 0.4–0.7% of costs; top-3 share ~70%), clouds (migration 9–18 months; RMB 50–150m), exchanges (2024 trading value RMB 76T), funding (RMB 120bn short-term; SHIBOR 1y 1.9%→2.8%), and regulated advisers (compliance cases +18%, IPO audits +22%).

| Supplier | Key metric (2024) |

|---|---|

| Talent | Senior quants RMB 1.2–2.5m |

| Data vendors | Fees 0.4–0.7%; top-3 70% |

| Clouds | Migration RMB 50–150m; 9–18m |

| Exchanges | Trading value RMB 76T |

| Funding | Short-term RMB 120bn; SHIBOR 1y 1.9→2.8% |

| Advisers | Compliance +18%; IPO audits +22% |

What is included in the product

Tailored exclusively for Guotai Junan Securities, this Porter's Five Forces overview uncovers key drivers of competition, customer influence, market entry risks, and disruptive substitutes, with strategic commentary on supplier and buyer power affecting pricing and profitability.

A concise Porter's Five Forces snapshot for Guotai Junan—quickly highlights competitive threats and strategic levers to ease decision-making in M&A, strategy, or investor decks.

Customers Bargaining Power

Institutional demand for commission transparency

Large institutional clients such as mutual funds and life insurers control outsized volumes—Guotai Junan handled an estimated Rmb1.2 trillion in client-driven equities trades in 2024—giving them strong leverage to demand lower commission fees and bundled research. These clients now seek transparent, often electronic, commission structures and bespoke research packages, pressuring Guotai Junan to cut rates or add services. To retain them, the firm must invest in low-cost execution, richer analytics, and dedicated account teams, or risk migration to rivals offering 10–30% cheaper commissions.

Retail investor price sensitivity and mobility

Retail investors are highly price-sensitive as low-cost apps cut average trading commissions to near zero—China’s retail brokerage account openings rose 28% in 2024 as discount platforms gained share, and 61% of retail traders cite fees as top switching reason in a 2025 survey.

Corporate client leverage in underwriting mandates

Major corporations seeking IPOs or bond issues invite multiple banks to bid, creating a buyer-led market where 60–75% of large China deals in 2024 were auctioned to shortlist banks, pushing down fees.

Clients demand low underwriting fees, high valuation support, and wide distribution—top mandates in 2024 saw fees fall to 1.0–1.5% for equity and 0.2–0.4% for primary bonds.

Guotai Junan must match price cuts and improve bookbuilding reach; losing one tier-1 deal can cost >CN¥50m in fees and pipeline momentum, so the firm competes aggressively on both price and service terms.

High net worth individuals seeking bespoke solutions

High-net-worth Chinese clients demand bespoke wealth solutions over off-the-shelf products, driving Guotai Junan to offer tailored portfolios and dedicated relationship managers; China had about 2.71 million HNWIs in 2024, up 7.4% YoY, so this segment’s sophistication is rising (Capgemini World Wealth Report 2024).

These clients’ capital lets them negotiate lower fees and premium service levels—an average Chinese HNWI held RMB 23.6 million in investable assets in 2024, giving them leverage to shift large mandates and pressure margins.

For Guotai Junan, retention hinges on bespoke reporting, tax-efficient solutions, and real-time access; losing a single RMB 200 million portfolio can cut fee income noticeably, so service customization is strategic.

- 2.71M HNWIs in China (2024)

- Avg RMB 23.6M investable assets per HNWI (2024)

- High bargaining power → fee pressure, demand for customization

Access to alternative digital investment platforms

The rise of integrated financial ecosystems lets customers bypass brokers for wealth needs; by 2024 over 320 million Chinese users accessed fintech wealth products, reducing stickiness for Guotai Junan Securities (GJS).

Nonbank platforms now offer money market funds and insurance with avg. yields comparable to bank wealth products, forcing GJS to match returns or launch exclusive structured products to retain assets under management (AUM).

Surging Chinese flows and HNWIs drive commissions and underwriting fees sharply lower

Clients hold strong price leverage: institutional flows (≈Rmb1.2trn equities trades in 2024) and 2.71M HNWIs (avg Rmb23.6M) push commissions down 10–30%; retail fee sensitivity rose as China added 28% more brokerage accounts in 2024 and 320M fintech wealth users; underwriting fees fell to 1.0–1.5% (equity) and 0.2–0.4% (bonds) in 2024.

| Metric | 2024 |

|---|---|

| Institutional equities trades | Rmb1.2tn |

| China HNWIs | 2.71M (avg Rmb23.6M) |

| Retail account growth | +28% YoY |

| Fintech users | 320M |

| Equity underwriting fees | 1.0–1.5% |

| Bond underwriting fees | 0.2–0.4% |

What You See Is What You Get

Guotai Junan Securities Porter's Five Forces Analysis

This preview shows the exact Guotai Junan Securities Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or samples, fully formatted and ready for use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Guotai Junan faces intense rivalry and regulatory scrutiny, with strong buyer bargaining from institutional clients and moderate supplier influence tied to technology and capital access; threats from fintech entrants and substitutes are rising but incumbency and brand scale remain key defenses. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Guotai Junan Securities’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarcity of elite financial and tech talent

The demand for investment bankers, quants, and fintech developers in China stayed very high through 2025, with job postings for quant roles up 28% year-on-year in 2024 and fintech hiring budgets rising 22% per a ChinaTech HR survey (Dec 2024). Guotai Junan must match market-leading pay—senior quants fetched total comp of RMB 1.2–2.5m in 2024—to retain talent driving digital transformation. This reliance gives star hires and specialized agencies strong bargaining power over salary, equity, and remote-work terms, raising fixed-cost risk for the firm.

Dependence on global data and technology providers

Guotai Junan depends on global real-time data and trading systems from vendors like Bloomberg and Wind; 2024 vendor fees estimated at 0.4–0.7% of operating costs, and 60–80% of trading desks run on third-party platforms.

Cloud and fintech partners (Alibaba Cloud, Huawei Cloud, local middleware firms) host trading engines and data lakes; multiyear contracts and integration raise switching costs—migration could take 9–18 months and cost ~RMB 50–150m.

These factors give suppliers pricing power: limited substitutes, high exit costs, and concentrated vendor market share (top 3 suppliers ~70% of enterprise market), letting them sustain margins and firm pricing.

Influence of financial exchanges and clearing houses

Guotai Junan relies on the Shanghai and Shenzhen Stock Exchanges for market access and trade execution; these state-regulated monopolies set listing rules, fee schedules, and technical protocols that affect all brokers.

In 2024 the exchanges processed ~76 trillion RMB in trading value (Shanghai 52T, Shenzhen 24T), so fee changes or tech disruptions materially hit Guotai Junan’s revenues and operations.

The firm has negligible bargaining power over these systemic suppliers and must comply with any regulatory or operational shifts, absorbing costs or changing IT and compliance workflows quickly.

Cost of capital from institutional lenders

Guotai Junan depends on steady access to interbank loans and institutional bonds to fund proprietary trading and margin lending; in 2024 it held short-term debt and repo lines totaling about RMB 120 billion, making supplier rates material to profits.

Large state banks and bond funds can push spreads: when PBOC tightened in 2023–2024, 1-year SHIBOR rose from ~1.9% (Jan 2023) to ~2.8% (Dec 2024), raising funding costs and pressuring net interest margins.

Wholesale liquidity swings and central bank policy moves thus directly alter Guotai Junan’s interest expense and capital allocation decisions, increasing supplier bargaining power.

- RMB 120bn short-term funding (2024)

- SHIBOR 1y: ~1.9% → ~2.8% (2023–2024)

- State banks + bond funds = pricing power

- Policy rate shifts drive interest expense

Specialized legal and compliance consultancies

With China tightening financial rules by 2025, specialized legal and audit firms are critical for Guotai Junan Securities, providing certifications for cross-border deals and HK/SH listings; independent-verification mandates give these suppliers moderate fee leverage. In 2024–25, demand rose—lawyer-led compliance cases up ~18% and audit reviews for IPOs increased ~22%—so suppliers can demand premium rates but competition limits outsized price hikes.

- Regulatory tightening 2023–25: higher demand

- Compliance cases +18% (2024)

- IPO audit reviews +22% (2024–25)

- Moderate bargaining power: mandated role, but competitive market

Suppliers Dictate Costs & Risk: Talent, Data, Cloud, Funding, Exchanges, Advisers

Suppliers hold significant power: talent (senior quants RMB 1.2–2.5m), data vendors (Bloomberg/Wind fees 0.4–0.7% of costs; top-3 share ~70%), clouds (migration 9–18 months; RMB 50–150m), exchanges (2024 trading value RMB 76T), funding (RMB 120bn short-term; SHIBOR 1y 1.9%→2.8%), and regulated advisers (compliance cases +18%, IPO audits +22%).

| Supplier | Key metric (2024) |

|---|---|

| Talent | Senior quants RMB 1.2–2.5m |

| Data vendors | Fees 0.4–0.7%; top-3 70% |

| Clouds | Migration RMB 50–150m; 9–18m |

| Exchanges | Trading value RMB 76T |

| Funding | Short-term RMB 120bn; SHIBOR 1y 1.9→2.8% |

| Advisers | Compliance +18%; IPO audits +22% |

What is included in the product

Tailored exclusively for Guotai Junan Securities, this Porter's Five Forces overview uncovers key drivers of competition, customer influence, market entry risks, and disruptive substitutes, with strategic commentary on supplier and buyer power affecting pricing and profitability.

A concise Porter's Five Forces snapshot for Guotai Junan—quickly highlights competitive threats and strategic levers to ease decision-making in M&A, strategy, or investor decks.

Customers Bargaining Power

Institutional demand for commission transparency

Large institutional clients such as mutual funds and life insurers control outsized volumes—Guotai Junan handled an estimated Rmb1.2 trillion in client-driven equities trades in 2024—giving them strong leverage to demand lower commission fees and bundled research. These clients now seek transparent, often electronic, commission structures and bespoke research packages, pressuring Guotai Junan to cut rates or add services. To retain them, the firm must invest in low-cost execution, richer analytics, and dedicated account teams, or risk migration to rivals offering 10–30% cheaper commissions.

Retail investor price sensitivity and mobility

Retail investors are highly price-sensitive as low-cost apps cut average trading commissions to near zero—China’s retail brokerage account openings rose 28% in 2024 as discount platforms gained share, and 61% of retail traders cite fees as top switching reason in a 2025 survey.

Corporate client leverage in underwriting mandates

Major corporations seeking IPOs or bond issues invite multiple banks to bid, creating a buyer-led market where 60–75% of large China deals in 2024 were auctioned to shortlist banks, pushing down fees.

Clients demand low underwriting fees, high valuation support, and wide distribution—top mandates in 2024 saw fees fall to 1.0–1.5% for equity and 0.2–0.4% for primary bonds.

Guotai Junan must match price cuts and improve bookbuilding reach; losing one tier-1 deal can cost >CN¥50m in fees and pipeline momentum, so the firm competes aggressively on both price and service terms.

High net worth individuals seeking bespoke solutions

High-net-worth Chinese clients demand bespoke wealth solutions over off-the-shelf products, driving Guotai Junan to offer tailored portfolios and dedicated relationship managers; China had about 2.71 million HNWIs in 2024, up 7.4% YoY, so this segment’s sophistication is rising (Capgemini World Wealth Report 2024).

These clients’ capital lets them negotiate lower fees and premium service levels—an average Chinese HNWI held RMB 23.6 million in investable assets in 2024, giving them leverage to shift large mandates and pressure margins.

For Guotai Junan, retention hinges on bespoke reporting, tax-efficient solutions, and real-time access; losing a single RMB 200 million portfolio can cut fee income noticeably, so service customization is strategic.

- 2.71M HNWIs in China (2024)

- Avg RMB 23.6M investable assets per HNWI (2024)

- High bargaining power → fee pressure, demand for customization

Access to alternative digital investment platforms

The rise of integrated financial ecosystems lets customers bypass brokers for wealth needs; by 2024 over 320 million Chinese users accessed fintech wealth products, reducing stickiness for Guotai Junan Securities (GJS).

Nonbank platforms now offer money market funds and insurance with avg. yields comparable to bank wealth products, forcing GJS to match returns or launch exclusive structured products to retain assets under management (AUM).

Surging Chinese flows and HNWIs drive commissions and underwriting fees sharply lower

Clients hold strong price leverage: institutional flows (≈Rmb1.2trn equities trades in 2024) and 2.71M HNWIs (avg Rmb23.6M) push commissions down 10–30%; retail fee sensitivity rose as China added 28% more brokerage accounts in 2024 and 320M fintech wealth users; underwriting fees fell to 1.0–1.5% (equity) and 0.2–0.4% (bonds) in 2024.

| Metric | 2024 |

|---|---|

| Institutional equities trades | Rmb1.2tn |

| China HNWIs | 2.71M (avg Rmb23.6M) |

| Retail account growth | +28% YoY |

| Fintech users | 320M |

| Equity underwriting fees | 1.0–1.5% |

| Bond underwriting fees | 0.2–0.4% |

What You See Is What You Get

Guotai Junan Securities Porter's Five Forces Analysis

This preview shows the exact Guotai Junan Securities Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or samples, fully formatted and ready for use.