Guardian Capital Boston Consulting Group Matrix

See the Bigger Picture

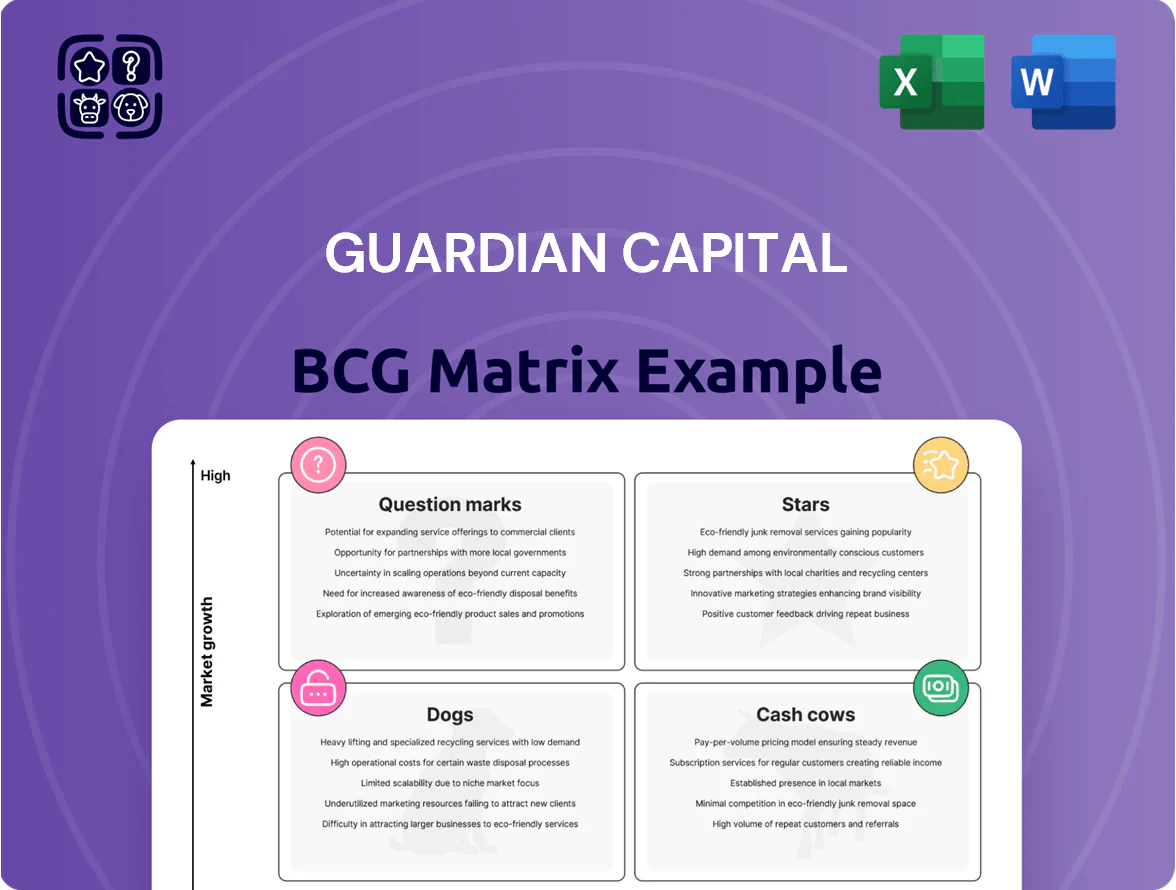

The Guardian Capital BCG Matrix preview highlights how its business units map across market share and growth—spotting potential Stars, Cash Cows, Dogs, and Question Marks that define strategic priorities. This snapshot teases actionable insights on resource allocation, divestment candidates, and growth bets—but the full BCG Matrix delivers quadrant-by-quadrant data, tailored recommendations, and editable Word/Excel files to execute decisions with confidence. Purchase the complete report to get the definitive strategic roadmap and stop guessing where to invest or cut.

Stars

US Asset Management Segment

US Asset Management is a Star: after buying Sterling and Galibier, client assets surged to over $100 billion by mid-2025, making it Guardian’s main growth engine.

It competes in the high-growth US market, chasing share via aggressive integration of the two subsidiaries and expanded equity strategies.

Revenue is strong, but heavy reinvestment is needed for integration costs, systems harmonization, and marketing to sustain scale.

Sterling Capital Management Subsidiary

Sterling Capital Management, newly integrated into Guardian Capital, is a US institutional leader driving ~60% of group revenue growth in 2024, while absorbing near-term integration costs equal to ~8% of Guardian’s operating cash flow.

Classified as a Star in the BCG matrix, Sterling combines high market share in US institutional mandates and double-digit AUM growth (2024: +12%), yet consumes cash for systems and client onboarding.

If Sterling sustains its >10% CAGR and US market share as the market matures, it can convert to a cash cow by 2027–2028, funding group-wide returns.

Guardian Capital Partners Fund IV

Guardian Capital Partners Fund IV hit its hard cap of 441,000,000 USD in Jan 2026, signaling strong investor demand and targeting lower‑middle market founder‑led companies with high growth potential.

As an oversubscribed, first‑to‑market leader in its niche, the fund commands premium deal flow and pricing power, positioning it as a Star in Guardian Capital’s BCG Matrix.

The fund is actively deploying into new platforms, requiring intensive operational support; management projects EBITDA expansion across portfolio companies that could drive double‑digit IRRs over a 5–7 year hold.

Global Dividend Growth Strategies

Global Dividend Growth Strategies saw assets under management rise to $4.2 billion by Dec 31, 2025, as investors chased quality growth amid 2025 volatility; net inflows totaled $620 million year-to-date, marking a 17% market-share gain versus peers.

Guardian prioritized these funds for global distribution, increasing placement staff by 25% and boosting marketing spend to $8.5 million in H1 2025 to capture competitor flows.

They qualify as Stars in Guardian’s BCG matrix because they sit in high-growth markets (global equity income up ~9% CAGR 2021–25) and retain top-quartile three-year returns, plus ongoing placement support.

- AuM $4.2B; YTD inflows $620M

- Marketing spend $8.5M H1 2025

- Placement team +25% staff

- 3-yr top-quartile returns; market share +17%

Digital Infrastructure Private Equity

Guardian Capital’s GPS program has pushed $1.2bn into digital infrastructure since 2023, fueling stakes in Raptor Power Systems and LINX and targeting AI/cloud-driven growth where demand for power and interconnects rose ~28% YoY in 2024.

These assets are cash-intensive during scale-up—capex and working capital absorb ~60–70% of early-year free cash flow—but offer top-quartile alternative returns and potential market leadership in a >$300bn global digital infra market.

- Deployed capital: $1.2bn since 2023

- Target sectors: power systems, interconnects (Raptor, LINX)

- Market growth: ~28% YoY demand (2024) for AI/cloud infra

- Cash burn: ~60–70% of early FCF

- Market size: >$300bn global digital infra

High-growth asset mix: US AUM $100B+, Fund IV $441M cap, $1.2B infra deployed

Stars: US Asset Mgmt (AUM >$100B mid‑2025; Sterling driving ~60% group growth; integration costs ≈8% operating cash flow), Partners Fund IV (hard cap $441M Jan‑2026; deploying for double‑digit IRRs), Global Dividend Growth (AUM $4.2B; YTD inflows $620M), GPS digital infra (deployed $1.2B; market >$300B).

| Asset | Key metric | Cash burn/notes |

|---|---|---|

| US Asset Mgmt | AUM >$100B; Sterling +12% AUM (2024) | Integration ≈8% op CF |

| Partners Fund IV | Hard cap $441M (Jan 2026) | Deploying; target 10%+ IRR |

| Global Dividend Growth | AUM $4.2B; inflows $620M YTD | Marketing $8.5M H1 2025 |

| GPS digital infra | Deployed $1.2B; market >$300B | FCF absorbed 60–70% early |

What is included in the product

Comprehensive BCG Matrix analysis of Guardian Capital’s units with strategic recommendations for Stars, Cash Cows, Question Marks, and Dogs.

One-page overview placing each Guardian Capital business unit in a BCG quadrant for quick strategic clarity.

Cash Cows

Canadian Institutional Asset Management

Canadian institutional asset management is Guardian Capital’s bedrock, with the firm holding a top domestic share for over 60 years and managing roughly CAD 25 billion in Canadian institutional AUM as of FY2025.

It delivers stable, high-margin management fees (operating margins ~35% in 2024) and needs minimal new marketing or infrastructure spend, producing consistent free cash flow.

That cash funds dividends (yield ~3.5% in 2025) and finances Guardian’s US and alternatives expansion, which saw buy-side deal outlays of ~CAD 120 million in 2024.

Private Wealth Operations

Private Wealth Operations, comprising Guardian Capital Advisors and Guardian Partners, manages over $11 billion AUM as of late 2025, delivering steady, predictable inflows that classify it as a Cash Cow in the BCG matrix.

Canada’s mature private wealth market lets Guardian milk returns from its reputation and long-term client relationships, producing stable fee revenue and low acquisition costs.

That cash funds corporate debt servicing and backs multi-year tech upgrades—recent budgets show ~ $30–50M annual IT spending commitments through 2026.

Bank of Montreal Equity Portfolio

Guardian Capital holds a large proprietary equity stake concentrated in Bank of Montreal (BMO) that had a fair value > $1.3 billion by late 2025, serving as a cash cow through dividends and low volatility capital gains.

Traditional Fixed Income Funds

Traditional Fixed Income Funds became beneficiaries of a late 2025 shift to lower-risk assets, boosting inflows and stabilizing NAVs; Guardian held roughly a 22% share of Canada’s fixed-income mutual fund market as of Dec 2025, keeping customer-acquisition spend low.

Growth in fixed income trails equities (estimated 3–5% CAGR vs equities’ 8–10% in 2026–28), yet Guardian’s mature lineup yields steady management fees covering core admin costs—fees generated roughly C$120–150m annually in 2025.

- High market share ~22% (Dec 2025)

- Estimated fee revenue C$120–150m (2025)

- Market CAGR fixed income 3–5% (2026–28)

- Low promo spend, steady cashflow

Alexandria Bancorp Limited

Alexandria Bancorp Limited, Guardian Capital’s offshore private bank, operates in a mature niche market providing private banking and trust services with low competitive volatility and high margins; FY2024 pre-tax margin reported ~34% and ROE ~18% supporting stable profitability.

The unit serves a loyal client base (assets under management ~US$4.2bn as of Dec 31, 2024), delivers steady cash flow covering ~12% of group operating cash flow, and helps fund quarterly dividends.

- Mature niche: private banking/trusts

- High margins: FY2024 pre-tax ~34%

- AUM: ~US$4.2bn (Dec 31, 2024)

- Contributes ~12% group operating cash flow

- Supports quarterly dividends

Guardian’s Wealth & Institutional Arms: CAD36B+ AUM, C$120–150M Fees, ~35% Margins

Guardian’s Canadian institutional and Private Wealth units are Cash Cows: ~CAD 25bn institutional AUM (FY2025) and >CAD 11bn private wealth (late 2025), generating ~C$120–150m fees (2025) with ~35% margins and ~3.5% dividend yield; Alexandria Bancorp adds US$4.2bn AUM (Dec 2024) and ~34% pre-tax margin.

| Metric | Value |

|---|---|

| Institutional AUM | CAD 25bn (FY2025) |

| Private Wealth AUM | CAD 11bn (late 2025) |

| Fee revenue | C$120–150m (2025) |

| Operating margin | ~35% (2024) |

| Dividend yield | ~3.5% (2025) |

| Alexandria AUM | US$4.2bn (Dec 31, 2024) |

| Alexandria pre-tax | ~34% (FY2024) |

Full Transparency, Always

Guardian Capital BCG Matrix

The preview you're viewing is the exact Guardian Capital BCG Matrix file you'll receive after purchase—no watermarks, no sample content, just the finalized, professionally formatted report ready for strategic use. This document reflects the same market-backed analysis and clarity found in the downloadable version and will be delivered directly to your inbox upon purchase. Once unlocked, it's immediately editable, printable, and presentation-ready for your team or clients.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

The Guardian Capital BCG Matrix preview highlights how its business units map across market share and growth—spotting potential Stars, Cash Cows, Dogs, and Question Marks that define strategic priorities. This snapshot teases actionable insights on resource allocation, divestment candidates, and growth bets—but the full BCG Matrix delivers quadrant-by-quadrant data, tailored recommendations, and editable Word/Excel files to execute decisions with confidence. Purchase the complete report to get the definitive strategic roadmap and stop guessing where to invest or cut.

Stars

US Asset Management Segment

US Asset Management is a Star: after buying Sterling and Galibier, client assets surged to over $100 billion by mid-2025, making it Guardian’s main growth engine.

It competes in the high-growth US market, chasing share via aggressive integration of the two subsidiaries and expanded equity strategies.

Revenue is strong, but heavy reinvestment is needed for integration costs, systems harmonization, and marketing to sustain scale.

Sterling Capital Management Subsidiary

Sterling Capital Management, newly integrated into Guardian Capital, is a US institutional leader driving ~60% of group revenue growth in 2024, while absorbing near-term integration costs equal to ~8% of Guardian’s operating cash flow.

Classified as a Star in the BCG matrix, Sterling combines high market share in US institutional mandates and double-digit AUM growth (2024: +12%), yet consumes cash for systems and client onboarding.

If Sterling sustains its >10% CAGR and US market share as the market matures, it can convert to a cash cow by 2027–2028, funding group-wide returns.

Guardian Capital Partners Fund IV

Guardian Capital Partners Fund IV hit its hard cap of 441,000,000 USD in Jan 2026, signaling strong investor demand and targeting lower‑middle market founder‑led companies with high growth potential.

As an oversubscribed, first‑to‑market leader in its niche, the fund commands premium deal flow and pricing power, positioning it as a Star in Guardian Capital’s BCG Matrix.

The fund is actively deploying into new platforms, requiring intensive operational support; management projects EBITDA expansion across portfolio companies that could drive double‑digit IRRs over a 5–7 year hold.

Global Dividend Growth Strategies

Global Dividend Growth Strategies saw assets under management rise to $4.2 billion by Dec 31, 2025, as investors chased quality growth amid 2025 volatility; net inflows totaled $620 million year-to-date, marking a 17% market-share gain versus peers.

Guardian prioritized these funds for global distribution, increasing placement staff by 25% and boosting marketing spend to $8.5 million in H1 2025 to capture competitor flows.

They qualify as Stars in Guardian’s BCG matrix because they sit in high-growth markets (global equity income up ~9% CAGR 2021–25) and retain top-quartile three-year returns, plus ongoing placement support.

- AuM $4.2B; YTD inflows $620M

- Marketing spend $8.5M H1 2025

- Placement team +25% staff

- 3-yr top-quartile returns; market share +17%

Digital Infrastructure Private Equity

Guardian Capital’s GPS program has pushed $1.2bn into digital infrastructure since 2023, fueling stakes in Raptor Power Systems and LINX and targeting AI/cloud-driven growth where demand for power and interconnects rose ~28% YoY in 2024.

These assets are cash-intensive during scale-up—capex and working capital absorb ~60–70% of early-year free cash flow—but offer top-quartile alternative returns and potential market leadership in a >$300bn global digital infra market.

- Deployed capital: $1.2bn since 2023

- Target sectors: power systems, interconnects (Raptor, LINX)

- Market growth: ~28% YoY demand (2024) for AI/cloud infra

- Cash burn: ~60–70% of early FCF

- Market size: >$300bn global digital infra

High-growth asset mix: US AUM $100B+, Fund IV $441M cap, $1.2B infra deployed

Stars: US Asset Mgmt (AUM >$100B mid‑2025; Sterling driving ~60% group growth; integration costs ≈8% operating cash flow), Partners Fund IV (hard cap $441M Jan‑2026; deploying for double‑digit IRRs), Global Dividend Growth (AUM $4.2B; YTD inflows $620M), GPS digital infra (deployed $1.2B; market >$300B).

| Asset | Key metric | Cash burn/notes |

|---|---|---|

| US Asset Mgmt | AUM >$100B; Sterling +12% AUM (2024) | Integration ≈8% op CF |

| Partners Fund IV | Hard cap $441M (Jan 2026) | Deploying; target 10%+ IRR |

| Global Dividend Growth | AUM $4.2B; inflows $620M YTD | Marketing $8.5M H1 2025 |

| GPS digital infra | Deployed $1.2B; market >$300B | FCF absorbed 60–70% early |

What is included in the product

Comprehensive BCG Matrix analysis of Guardian Capital’s units with strategic recommendations for Stars, Cash Cows, Question Marks, and Dogs.

One-page overview placing each Guardian Capital business unit in a BCG quadrant for quick strategic clarity.

Cash Cows

Canadian Institutional Asset Management

Canadian institutional asset management is Guardian Capital’s bedrock, with the firm holding a top domestic share for over 60 years and managing roughly CAD 25 billion in Canadian institutional AUM as of FY2025.

It delivers stable, high-margin management fees (operating margins ~35% in 2024) and needs minimal new marketing or infrastructure spend, producing consistent free cash flow.

That cash funds dividends (yield ~3.5% in 2025) and finances Guardian’s US and alternatives expansion, which saw buy-side deal outlays of ~CAD 120 million in 2024.

Private Wealth Operations

Private Wealth Operations, comprising Guardian Capital Advisors and Guardian Partners, manages over $11 billion AUM as of late 2025, delivering steady, predictable inflows that classify it as a Cash Cow in the BCG matrix.

Canada’s mature private wealth market lets Guardian milk returns from its reputation and long-term client relationships, producing stable fee revenue and low acquisition costs.

That cash funds corporate debt servicing and backs multi-year tech upgrades—recent budgets show ~ $30–50M annual IT spending commitments through 2026.

Bank of Montreal Equity Portfolio

Guardian Capital holds a large proprietary equity stake concentrated in Bank of Montreal (BMO) that had a fair value > $1.3 billion by late 2025, serving as a cash cow through dividends and low volatility capital gains.

Traditional Fixed Income Funds

Traditional Fixed Income Funds became beneficiaries of a late 2025 shift to lower-risk assets, boosting inflows and stabilizing NAVs; Guardian held roughly a 22% share of Canada’s fixed-income mutual fund market as of Dec 2025, keeping customer-acquisition spend low.

Growth in fixed income trails equities (estimated 3–5% CAGR vs equities’ 8–10% in 2026–28), yet Guardian’s mature lineup yields steady management fees covering core admin costs—fees generated roughly C$120–150m annually in 2025.

- High market share ~22% (Dec 2025)

- Estimated fee revenue C$120–150m (2025)

- Market CAGR fixed income 3–5% (2026–28)

- Low promo spend, steady cashflow

Alexandria Bancorp Limited

Alexandria Bancorp Limited, Guardian Capital’s offshore private bank, operates in a mature niche market providing private banking and trust services with low competitive volatility and high margins; FY2024 pre-tax margin reported ~34% and ROE ~18% supporting stable profitability.

The unit serves a loyal client base (assets under management ~US$4.2bn as of Dec 31, 2024), delivers steady cash flow covering ~12% of group operating cash flow, and helps fund quarterly dividends.

- Mature niche: private banking/trusts

- High margins: FY2024 pre-tax ~34%

- AUM: ~US$4.2bn (Dec 31, 2024)

- Contributes ~12% group operating cash flow

- Supports quarterly dividends

Guardian’s Wealth & Institutional Arms: CAD36B+ AUM, C$120–150M Fees, ~35% Margins

Guardian’s Canadian institutional and Private Wealth units are Cash Cows: ~CAD 25bn institutional AUM (FY2025) and >CAD 11bn private wealth (late 2025), generating ~C$120–150m fees (2025) with ~35% margins and ~3.5% dividend yield; Alexandria Bancorp adds US$4.2bn AUM (Dec 2024) and ~34% pre-tax margin.

| Metric | Value |

|---|---|

| Institutional AUM | CAD 25bn (FY2025) |

| Private Wealth AUM | CAD 11bn (late 2025) |

| Fee revenue | C$120–150m (2025) |

| Operating margin | ~35% (2024) |

| Dividend yield | ~3.5% (2025) |

| Alexandria AUM | US$4.2bn (Dec 31, 2024) |

| Alexandria pre-tax | ~34% (FY2024) |

Full Transparency, Always

Guardian Capital BCG Matrix

The preview you're viewing is the exact Guardian Capital BCG Matrix file you'll receive after purchase—no watermarks, no sample content, just the finalized, professionally formatted report ready for strategic use. This document reflects the same market-backed analysis and clarity found in the downloadable version and will be delivered directly to your inbox upon purchase. Once unlocked, it's immediately editable, printable, and presentation-ready for your team or clients.