Guitar Center Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

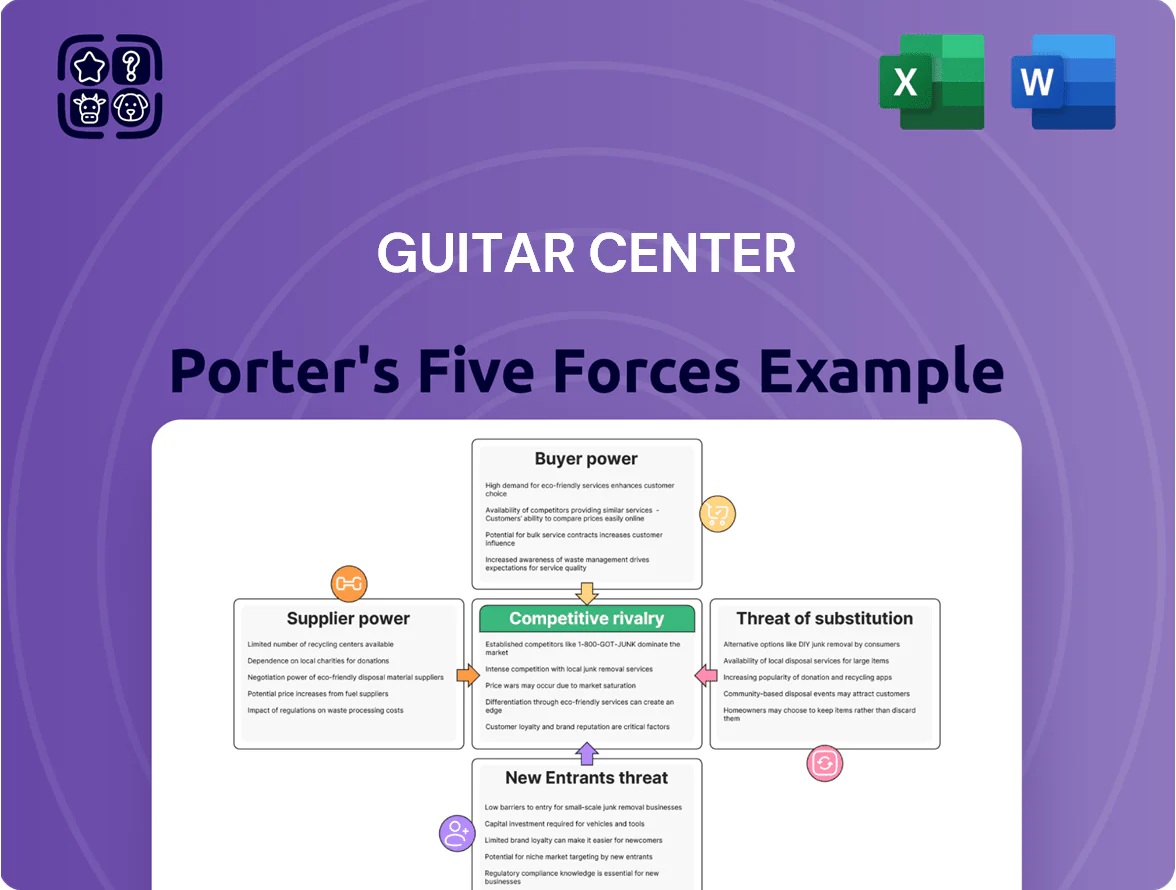

Guitar Center faces intense competitive rivalry from online retailers and niche specialty shops, moderate supplier power due to brand partnerships, and evolving buyer behavior driven by price sensitivity and experience-seeking; threats from substitutes and new entrants are tempered by scale and store network. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Guitar Center’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dominance of major iconic brands

The musical instrument market is concentrated: Fender, Gibson, and Yamaha together account for an estimated 40–50% of electric and acoustic guitar sales in the US (2024 NPD/Industry reports), giving them strong brand equity and bargaining power over Guitar Center.

These suppliers drive foot traffic and credibility with pro players, so product shortages or tighter dealer credit—Gibson cut dealer terms in 2023—would sharply reduce Guitar Center’s same-store sales and store conversion rates.

Limited alternative sourcing for premium gear

High-end pro gear uses proprietary tech and specialist manufacturing, so generic substitutes are rare; top brands like Fender, Gibson, and Neumann control supply of high-margin items, limiting Guitar Center’s sourcing options. In 2024 pro-segment gear drove ~22% of US musical-instrument retail revenue, so Guitar Center must stock these items to retain pros, reducing its price leverage. That dependency creates supplier-driven pricing for the most desirable segments.

Supplier forward integration into direct sales

Concentration of specialized component providers

Concentration of specialized component providers raises supplier power for Guitar Center: for synths and audio interfaces, a handful of chipmakers dominate, and 2023–2024 supply shocks pushed lead times from months to 9–18 months for certain ADC/DAC chips, causing industry-wide stockouts.

Guitar Center cannot quickly switch vendors, so manufacturers set delivery schedules and raised wholesale prices by an estimated 5–12% in 2024, squeezing margins and inventory turnover.

- Few suppliers: key chips concentrated among top 3 vendors

- Lead times: 9–18 months during 2023–24 shocks

- Price impact: wholesale up ~5–12% in 2024

- Risk: limited vendor substitution, higher stockout risk

Impact of exclusive distribution agreements

Suppliers use selective and exclusive distribution to protect brand prestige, often allocating limited-edition instrument lines to a few national chains; in 2024 Gibson and Fender allocated roughly 15–20% of key limited runs through exclusive retail partners.

Guitar Center depends on these exclusives to differentiate against local shops and online-only sellers, driving higher foot traffic and average ticket sizes—exclusive SKUs can raise basket value by ~12% per visit.

As a result Guitar Center must follow strict merchandising, pricing, and display rules tied to supplier agreements, limiting promotional flexibility and squeezing margin if price-matching is required.

- Exclusive SKUs: 15–20% of limited runs (2024)

- Basket lift from exclusives: ~12%

- Tradeoff: differentiation vs pricing/merchandising constraints

Supplier dominance squeezes Guitar Center: higher costs, longer lead times, tighter stock

Suppliers (Fender, Gibson, Yamaha) hold strong leverage—40–50% market share (2024 NPD), exclusive allocations of 15–20% of limited runs, and DTC margins 10–30% higher—forcing Guitar Center to accept strict merchandising, higher wholesale (+5–12% in 2024) and longer lead times (9–18 months), reducing price leverage and raising stockout and margin risk.

| Metric | 2023–24 |

|---|---|

| Top brands market share | 40–50% |

| Wholesale price increase | +5–12% |

| Lead times (chips) | 9–18 months |

| Exclusive allocation | 15–20% |

| DTC margin lift | +10–30% |

What is included in the product

Concise Porter’s Five Forces analysis tailored for Guitar Center, revealing competitive intensity, buyer and supplier power, substitution risks, and barriers to entry to inform strategic and investment decisions.

Quickly pinpoint Guitar Center’s competitive pressures with a one-sheet Porter's Five Forces summary—ideal for fast, board-ready insights and easy integration into pitch decks.

Customers Bargaining Power

High price sensitivity in the entry-level market

Novice musicians and hobbyists prioritize price over brand, with 62% of entry-level buyers checking three+ sites before purchase (2024 survey), so Guitar Center faces high price sensitivity.

Entry-level guitars are commoditized, enabling easy switching to lower-priced retailers or 0% APR financing options, pressuring loyalty.

Guitar Center uses aggressive promotions—Black Friday and clearance discounts cut ASPs by ~18% on mass models in 2024—compressing margins on high-volume items.

Low switching costs for online shoppers

The shift to digital means online shoppers can switch from Guitar Center to Sweetwater or Amazon in one click; US e‑commerce conversion rates hover around 2.5% (2024), so carts are volatile.

There are virtually no financial penalties for abandoning a cart—average US cart abandonment stood at 73.8% in 2024—so customers jump for faster shipping or better loyalty perks.

This low switching cost gives buyers leverage to demand lower prices, free/fast delivery, and superior service, pressuring Guitar Center’s margins and retention.

Access to comprehensive product information

Customers use phones to check reviews, watch demos, and compare prices in-store, and 73% of shoppers used mobile for price checks in 2024 (Pew/NRF). This data parity removes sales staff's info edge, boosting buyer leverage for discounts and specs. Guitar Center faces frequent demands for price matches; online competitors grew revenue share to ~28% of musical retail sales in 2024, strengthening customers’ bargaining power.

Influence of professional and institutional buyers

Large-scale purchasers—recording studios, schools, and touring productions—buy in bulk and demand steep volume discounts; in 2024 institutional B2B orders accounted for an estimated 18% of U.S. pro-audio and instrument spend, giving them price leverage over Guitar Center.

These high-value clients can negotiate bespoke contracts and SLAs unavailable to retail customers, and their ability to redirect multimillion-dollar budgets to competitors increases pressure on Guitar Center’s B2B margins and service terms.

- Institutional orders ≈18% market share (2024 est.)

- Bulk discounts and custom SLAs common

- High switching power versus GC B2B

Growth of the secondary used gear market

The rise of Reverb and eBay grew the used-gear market: Reverb reported $1.2B gross merchandise value in 2023, giving buyers cheaper, high-quality alternatives and setting a non-retail price ceiling that weakens Guitar Center’s margin power.

With 30–40% price discounts common on used instruments, many customers bypass new retail when perceived incremental value is low, raising buyer bargaining power and forcing GC to compete on service, warranty, or financing.

- Reverb GMV $1.2B (2023)

- Typical used discounts 30–40%

- eBay active listings ~millions of instruments

Price‑sensitive buyers, high abandonment, used market caps new prices — margin pressure

Buyers have high price sensitivity and low switching costs: 62% of entry buyers compare 3+ sites (2024); US e‑commerce conversion ~2.5% (2024); cart abandonment 73.8% (2024). Institutional B2B ≈18% of spend (2024) exerts volume leverage. Reverb GMV $1.2B (2023); used discounts 30–40%, capping new prices and pressuring GC margins.

| Metric | Value |

|---|---|

| Entry buyer comparison | 62% (2024) |

| e‑commerce conversion | 2.5% (2024) |

| Cart abandonment | 73.8% (2024) |

| B2B share | 18% (2024 est.) |

| Reverb GMV | $1.2B (2023) |

| Used discount | 30–40% |

Full Version Awaits

Guitar Center Porter's Five Forces Analysis

This preview shows the exact Guitar Center Porter’s Five Forces analysis you'll receive upon purchase—no placeholders or mockups, fully formatted and ready for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Guitar Center faces intense competitive rivalry from online retailers and niche specialty shops, moderate supplier power due to brand partnerships, and evolving buyer behavior driven by price sensitivity and experience-seeking; threats from substitutes and new entrants are tempered by scale and store network. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Guitar Center’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dominance of major iconic brands

The musical instrument market is concentrated: Fender, Gibson, and Yamaha together account for an estimated 40–50% of electric and acoustic guitar sales in the US (2024 NPD/Industry reports), giving them strong brand equity and bargaining power over Guitar Center.

These suppliers drive foot traffic and credibility with pro players, so product shortages or tighter dealer credit—Gibson cut dealer terms in 2023—would sharply reduce Guitar Center’s same-store sales and store conversion rates.

Limited alternative sourcing for premium gear

High-end pro gear uses proprietary tech and specialist manufacturing, so generic substitutes are rare; top brands like Fender, Gibson, and Neumann control supply of high-margin items, limiting Guitar Center’s sourcing options. In 2024 pro-segment gear drove ~22% of US musical-instrument retail revenue, so Guitar Center must stock these items to retain pros, reducing its price leverage. That dependency creates supplier-driven pricing for the most desirable segments.

Supplier forward integration into direct sales

Concentration of specialized component providers

Concentration of specialized component providers raises supplier power for Guitar Center: for synths and audio interfaces, a handful of chipmakers dominate, and 2023–2024 supply shocks pushed lead times from months to 9–18 months for certain ADC/DAC chips, causing industry-wide stockouts.

Guitar Center cannot quickly switch vendors, so manufacturers set delivery schedules and raised wholesale prices by an estimated 5–12% in 2024, squeezing margins and inventory turnover.

- Few suppliers: key chips concentrated among top 3 vendors

- Lead times: 9–18 months during 2023–24 shocks

- Price impact: wholesale up ~5–12% in 2024

- Risk: limited vendor substitution, higher stockout risk

Impact of exclusive distribution agreements

Suppliers use selective and exclusive distribution to protect brand prestige, often allocating limited-edition instrument lines to a few national chains; in 2024 Gibson and Fender allocated roughly 15–20% of key limited runs through exclusive retail partners.

Guitar Center depends on these exclusives to differentiate against local shops and online-only sellers, driving higher foot traffic and average ticket sizes—exclusive SKUs can raise basket value by ~12% per visit.

As a result Guitar Center must follow strict merchandising, pricing, and display rules tied to supplier agreements, limiting promotional flexibility and squeezing margin if price-matching is required.

- Exclusive SKUs: 15–20% of limited runs (2024)

- Basket lift from exclusives: ~12%

- Tradeoff: differentiation vs pricing/merchandising constraints

Supplier dominance squeezes Guitar Center: higher costs, longer lead times, tighter stock

Suppliers (Fender, Gibson, Yamaha) hold strong leverage—40–50% market share (2024 NPD), exclusive allocations of 15–20% of limited runs, and DTC margins 10–30% higher—forcing Guitar Center to accept strict merchandising, higher wholesale (+5–12% in 2024) and longer lead times (9–18 months), reducing price leverage and raising stockout and margin risk.

| Metric | 2023–24 |

|---|---|

| Top brands market share | 40–50% |

| Wholesale price increase | +5–12% |

| Lead times (chips) | 9–18 months |

| Exclusive allocation | 15–20% |

| DTC margin lift | +10–30% |

What is included in the product

Concise Porter’s Five Forces analysis tailored for Guitar Center, revealing competitive intensity, buyer and supplier power, substitution risks, and barriers to entry to inform strategic and investment decisions.

Quickly pinpoint Guitar Center’s competitive pressures with a one-sheet Porter's Five Forces summary—ideal for fast, board-ready insights and easy integration into pitch decks.

Customers Bargaining Power

High price sensitivity in the entry-level market

Novice musicians and hobbyists prioritize price over brand, with 62% of entry-level buyers checking three+ sites before purchase (2024 survey), so Guitar Center faces high price sensitivity.

Entry-level guitars are commoditized, enabling easy switching to lower-priced retailers or 0% APR financing options, pressuring loyalty.

Guitar Center uses aggressive promotions—Black Friday and clearance discounts cut ASPs by ~18% on mass models in 2024—compressing margins on high-volume items.

Low switching costs for online shoppers

The shift to digital means online shoppers can switch from Guitar Center to Sweetwater or Amazon in one click; US e‑commerce conversion rates hover around 2.5% (2024), so carts are volatile.

There are virtually no financial penalties for abandoning a cart—average US cart abandonment stood at 73.8% in 2024—so customers jump for faster shipping or better loyalty perks.

This low switching cost gives buyers leverage to demand lower prices, free/fast delivery, and superior service, pressuring Guitar Center’s margins and retention.

Access to comprehensive product information

Customers use phones to check reviews, watch demos, and compare prices in-store, and 73% of shoppers used mobile for price checks in 2024 (Pew/NRF). This data parity removes sales staff's info edge, boosting buyer leverage for discounts and specs. Guitar Center faces frequent demands for price matches; online competitors grew revenue share to ~28% of musical retail sales in 2024, strengthening customers’ bargaining power.

Influence of professional and institutional buyers

Large-scale purchasers—recording studios, schools, and touring productions—buy in bulk and demand steep volume discounts; in 2024 institutional B2B orders accounted for an estimated 18% of U.S. pro-audio and instrument spend, giving them price leverage over Guitar Center.

These high-value clients can negotiate bespoke contracts and SLAs unavailable to retail customers, and their ability to redirect multimillion-dollar budgets to competitors increases pressure on Guitar Center’s B2B margins and service terms.

- Institutional orders ≈18% market share (2024 est.)

- Bulk discounts and custom SLAs common

- High switching power versus GC B2B

Growth of the secondary used gear market

The rise of Reverb and eBay grew the used-gear market: Reverb reported $1.2B gross merchandise value in 2023, giving buyers cheaper, high-quality alternatives and setting a non-retail price ceiling that weakens Guitar Center’s margin power.

With 30–40% price discounts common on used instruments, many customers bypass new retail when perceived incremental value is low, raising buyer bargaining power and forcing GC to compete on service, warranty, or financing.

- Reverb GMV $1.2B (2023)

- Typical used discounts 30–40%

- eBay active listings ~millions of instruments

Price‑sensitive buyers, high abandonment, used market caps new prices — margin pressure

Buyers have high price sensitivity and low switching costs: 62% of entry buyers compare 3+ sites (2024); US e‑commerce conversion ~2.5% (2024); cart abandonment 73.8% (2024). Institutional B2B ≈18% of spend (2024) exerts volume leverage. Reverb GMV $1.2B (2023); used discounts 30–40%, capping new prices and pressuring GC margins.

| Metric | Value |

|---|---|

| Entry buyer comparison | 62% (2024) |

| e‑commerce conversion | 2.5% (2024) |

| Cart abandonment | 73.8% (2024) |

| B2B share | 18% (2024 est.) |

| Reverb GMV | $1.2B (2023) |

| Used discount | 30–40% |

Full Version Awaits

Guitar Center Porter's Five Forces Analysis

This preview shows the exact Guitar Center Porter’s Five Forces analysis you'll receive upon purchase—no placeholders or mockups, fully formatted and ready for immediate download and use.