GWA Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

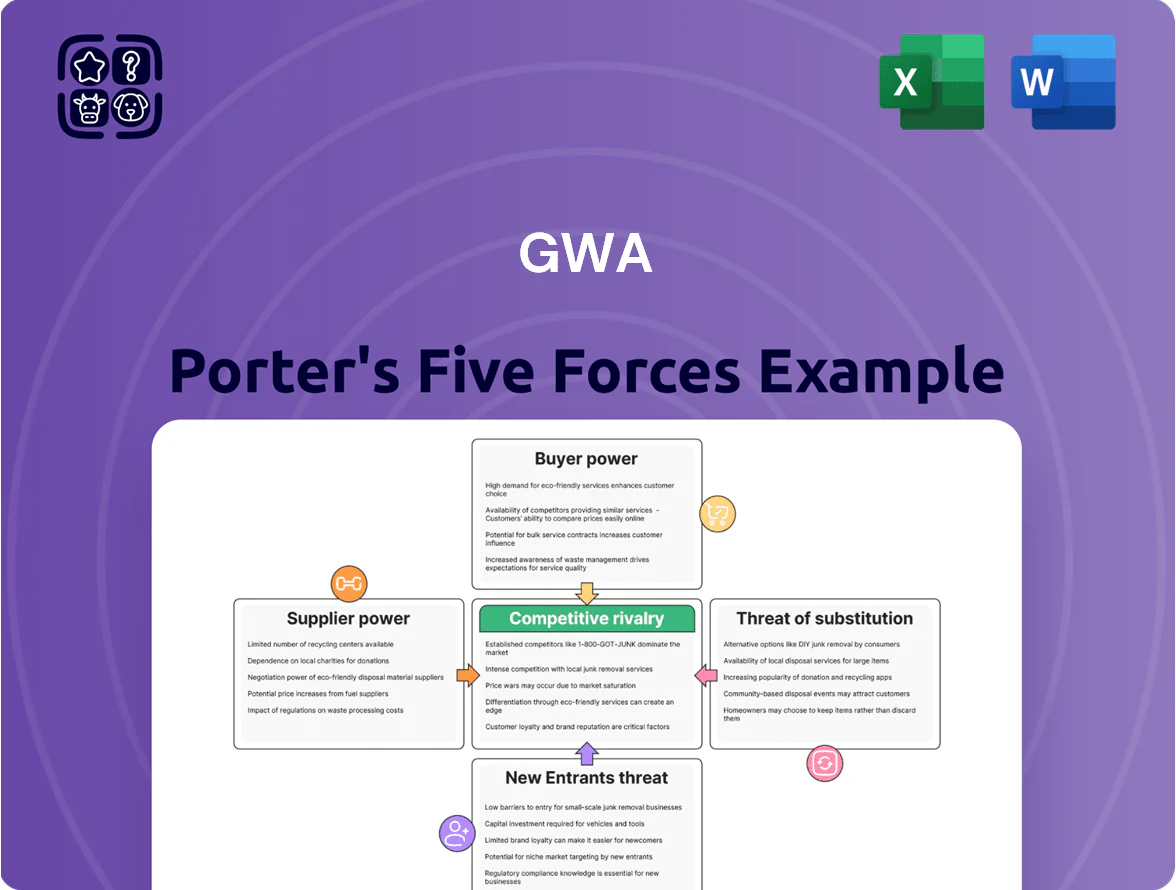

GWA faces moderate supplier power and concentrated buyer segments, while entry barriers and substitution threats shape its pricing leverage and innovation pace; competitive rivalry is steady but ripe for disruption. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore GWA’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Reliance on Asian Manufacturing Hubs

GWA Group sources much of its sanitaryware from Asian manufacturers, notably China and Vietnam, creating dependency for cost-effective ceramic production; in FY2024 about 62% of imported plumbing products originated from these markets per company disclosures.

Volatility in Raw Material and Energy Costs

Suppliers face volatile raw-material and energy costs—brass, chrome, and clay prices rose 12–18% YoY in 2024 and natural gas for kilns averaged $8.50/MMBtu in 2024 vs $4.20 in 2020—so they push costs onto GWA, squeezing gross margins if GWA can’t hike retail prices quickly; by Q3 2025 persistent energy inflation kept suppliers able to renegotiate prices upward.

Supply Chain and Logistics Dependencies

The bargaining power of suppliers rises because they control production timelines and tie into global shipping lanes; in 2024 logistics delays added an average 22% lead-time to APAC imports, so GWA must sync orders with carriers to keep inventory days on hand around 45–60 to avoid stockouts in Australia and New Zealand. Any supplier disruption can quickly delay major commercial-project deliveries and cut quarterly revenue—GWA reported supply-chain impacts reduced FY2024 revenue growth by ~3.1%.

Strict Compliance and Sustainability Standards

As GWA tightens ESG reporting and sets 2030 net-zero-aligned targets, it forces suppliers to meet strict environmental and labor standards, narrowing the supplier base to certified vendors with green-building tech and traceable supply chains.

That reliance raises supplier power: compliant vendors commanding premium pricing and longer lead times are harder to replace—industry data shows certified suppliers can charge 5–12% higher margins and reduce switching options by ~30%.

- Smaller pool of certified suppliers

- Compliant suppliers earn 5–12% price premium

- Supply-switching options drop ~30%

Technical Specialization and Tooling

GWA’s reliance on proprietary designs and supplier-held tooling creates high switching costs—relocating molds and recalibrating machines can exceed A$0.5–2.0m per product line and take 3–9 months, so suppliers gain moderate leverage at renewal.

That lock-in helps suppliers extract price or delivery concessions; GWA reported supplier-related capex of ~A$12m in FY2024, underscoring dependence.

- High switching cost: A$0.5–2.0m per line

- Time to switch: 3–9 months

- FY2024 supplier capex: ~A$12m

Suppliers wield strong leverage: 62% imports, rising costs, higher premiums & limited options

Suppliers hold moderate-to-high bargaining power: 62% of imports from China/Vietnam (FY2024), raw-material costs rose 12–18% YoY in 2024, logistics added 22% lead-time, switching costs A$0.5–2.0m per product line and supplier-related capex ~A$12m (FY2024), and certified suppliers charge 5–12% premiums while cutting options ~30%.

| Metric | Value |

|---|---|

| Imports from China/VN | 62% (FY2024) |

| Raw-materials change | +12–18% YoY (2024) |

| Logistics delay | +22% lead-time (2024) |

| Switching cost | A$0.5–2.0m/line |

| Supplier capex | ~A$12m (FY2024) |

| Certified supplier premium | +5–12% |

| Reduction in options | ~30% |

What is included in the product

Tailored Porter's Five Forces analysis for GWA that uncovers key competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats to its market share.

Compact Porter's Five Forces summary tailored for GWA—quickly highlights strategic pressures and relief points to streamline decision-making and prioritize actions.

Customers Bargaining Power

Concentration of Major Retail Channels

Influence of Trade Professionals

Plumbers and developers influence purchase decisions for roughly 40–60% of GWA’s end-users in Australia, prioritising ease of installation, reliability, and after-sales support to avoid callbacks that can cost A$500–A$1,200 per incident.

These trade professionals stick with trusted brands; GWA’s 2024 trade loyalty programs and training reduced product returns by 18% and lifted repeat-specification rates by 12% year-over-year.

GWA must keep investing ~A$3–5M annually in trade engagement, training, and warranty support to prevent switching to lower-cost rivals and protect gross margins near 28%.

Price Sensitivity in Residential Construction

Demand for GWA products tracks residential renovations and new builds, which fell ~7% nationally in 2024 and remained weak into 2025 as mortgage rates rose above 7%, making customers more price-sensitive.

In 2025 many buyers trade down to entry ranges; GWA must keep competitive pricing across tiers to avoid share loss to budget rivals like Reece and online discounters, or face margin compression.

Digital Transparency and Information Access

- 81% of buyers research online (2024)

- Competitors undercut by 10–20%

- Improve SEO, UX, product content

- Use customer reviews and case studies

Low Switching Costs for End Users

Low switching costs mean individual consumers and small renovators can switch from GWA brands like Caroma to competitors at purchase with minimal effort, since most fixtures use standard sizes; industry data shows 70–80% of household fixture replacements in Australia follow standard fittings (ABS, 2023), so technical barriers are low.

This keeps pressure on GWA (ASX: GWA) to sustain brand equity and perceived quality—GWA reported 2024 consumer segment gross margins near 42%, so margin retention depends on brand strength.

- Standard fittings = low technical barrier

- 70–80% replacements follow standards (ABS 2023)

- GWA consumer margins ~42% (2024)

- High brand equity needed to prevent churn

GWA under squeeze: 55% chain sales, thin 28% gross margin, A$3–5M trade spend

| Metric | Value |

|---|---|

| Revenue via chains | ~55% FY2025 |

| Gross margin | ~28.4% FY2024 |

| Consumer margin | ~42% 2024 |

| Online research | 81% 2024 |

| Std fittings | 70–80% ABS 2023 |

| Trade spend | A$3–5M/yr |

Preview Before You Purchase

GWA Porter's Five Forces Analysis

This preview shows the exact GWA Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. The document displayed is fully formatted and ready for download the moment you buy, containing the same professional insights, data-driven evaluation, and strategic implications as the delivered file. You're viewing the final deliverable, available instantly after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

GWA faces moderate supplier power and concentrated buyer segments, while entry barriers and substitution threats shape its pricing leverage and innovation pace; competitive rivalry is steady but ripe for disruption. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore GWA’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Reliance on Asian Manufacturing Hubs

GWA Group sources much of its sanitaryware from Asian manufacturers, notably China and Vietnam, creating dependency for cost-effective ceramic production; in FY2024 about 62% of imported plumbing products originated from these markets per company disclosures.

Volatility in Raw Material and Energy Costs

Suppliers face volatile raw-material and energy costs—brass, chrome, and clay prices rose 12–18% YoY in 2024 and natural gas for kilns averaged $8.50/MMBtu in 2024 vs $4.20 in 2020—so they push costs onto GWA, squeezing gross margins if GWA can’t hike retail prices quickly; by Q3 2025 persistent energy inflation kept suppliers able to renegotiate prices upward.

Supply Chain and Logistics Dependencies

The bargaining power of suppliers rises because they control production timelines and tie into global shipping lanes; in 2024 logistics delays added an average 22% lead-time to APAC imports, so GWA must sync orders with carriers to keep inventory days on hand around 45–60 to avoid stockouts in Australia and New Zealand. Any supplier disruption can quickly delay major commercial-project deliveries and cut quarterly revenue—GWA reported supply-chain impacts reduced FY2024 revenue growth by ~3.1%.

Strict Compliance and Sustainability Standards

As GWA tightens ESG reporting and sets 2030 net-zero-aligned targets, it forces suppliers to meet strict environmental and labor standards, narrowing the supplier base to certified vendors with green-building tech and traceable supply chains.

That reliance raises supplier power: compliant vendors commanding premium pricing and longer lead times are harder to replace—industry data shows certified suppliers can charge 5–12% higher margins and reduce switching options by ~30%.

- Smaller pool of certified suppliers

- Compliant suppliers earn 5–12% price premium

- Supply-switching options drop ~30%

Technical Specialization and Tooling

GWA’s reliance on proprietary designs and supplier-held tooling creates high switching costs—relocating molds and recalibrating machines can exceed A$0.5–2.0m per product line and take 3–9 months, so suppliers gain moderate leverage at renewal.

That lock-in helps suppliers extract price or delivery concessions; GWA reported supplier-related capex of ~A$12m in FY2024, underscoring dependence.

- High switching cost: A$0.5–2.0m per line

- Time to switch: 3–9 months

- FY2024 supplier capex: ~A$12m

Suppliers wield strong leverage: 62% imports, rising costs, higher premiums & limited options

Suppliers hold moderate-to-high bargaining power: 62% of imports from China/Vietnam (FY2024), raw-material costs rose 12–18% YoY in 2024, logistics added 22% lead-time, switching costs A$0.5–2.0m per product line and supplier-related capex ~A$12m (FY2024), and certified suppliers charge 5–12% premiums while cutting options ~30%.

| Metric | Value |

|---|---|

| Imports from China/VN | 62% (FY2024) |

| Raw-materials change | +12–18% YoY (2024) |

| Logistics delay | +22% lead-time (2024) |

| Switching cost | A$0.5–2.0m/line |

| Supplier capex | ~A$12m (FY2024) |

| Certified supplier premium | +5–12% |

| Reduction in options | ~30% |

What is included in the product

Tailored Porter's Five Forces analysis for GWA that uncovers key competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats to its market share.

Compact Porter's Five Forces summary tailored for GWA—quickly highlights strategic pressures and relief points to streamline decision-making and prioritize actions.

Customers Bargaining Power

Concentration of Major Retail Channels

Influence of Trade Professionals

Plumbers and developers influence purchase decisions for roughly 40–60% of GWA’s end-users in Australia, prioritising ease of installation, reliability, and after-sales support to avoid callbacks that can cost A$500–A$1,200 per incident.

These trade professionals stick with trusted brands; GWA’s 2024 trade loyalty programs and training reduced product returns by 18% and lifted repeat-specification rates by 12% year-over-year.

GWA must keep investing ~A$3–5M annually in trade engagement, training, and warranty support to prevent switching to lower-cost rivals and protect gross margins near 28%.

Price Sensitivity in Residential Construction

Demand for GWA products tracks residential renovations and new builds, which fell ~7% nationally in 2024 and remained weak into 2025 as mortgage rates rose above 7%, making customers more price-sensitive.

In 2025 many buyers trade down to entry ranges; GWA must keep competitive pricing across tiers to avoid share loss to budget rivals like Reece and online discounters, or face margin compression.

Digital Transparency and Information Access

- 81% of buyers research online (2024)

- Competitors undercut by 10–20%

- Improve SEO, UX, product content

- Use customer reviews and case studies

Low Switching Costs for End Users

Low switching costs mean individual consumers and small renovators can switch from GWA brands like Caroma to competitors at purchase with minimal effort, since most fixtures use standard sizes; industry data shows 70–80% of household fixture replacements in Australia follow standard fittings (ABS, 2023), so technical barriers are low.

This keeps pressure on GWA (ASX: GWA) to sustain brand equity and perceived quality—GWA reported 2024 consumer segment gross margins near 42%, so margin retention depends on brand strength.

- Standard fittings = low technical barrier

- 70–80% replacements follow standards (ABS 2023)

- GWA consumer margins ~42% (2024)

- High brand equity needed to prevent churn

GWA under squeeze: 55% chain sales, thin 28% gross margin, A$3–5M trade spend

| Metric | Value |

|---|---|

| Revenue via chains | ~55% FY2025 |

| Gross margin | ~28.4% FY2024 |

| Consumer margin | ~42% 2024 |

| Online research | 81% 2024 |

| Std fittings | 70–80% ABS 2023 |

| Trade spend | A$3–5M/yr |

Preview Before You Purchase

GWA Porter's Five Forces Analysis

This preview shows the exact GWA Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. The document displayed is fully formatted and ready for download the moment you buy, containing the same professional insights, data-driven evaluation, and strategic implications as the delivered file. You're viewing the final deliverable, available instantly after payment.