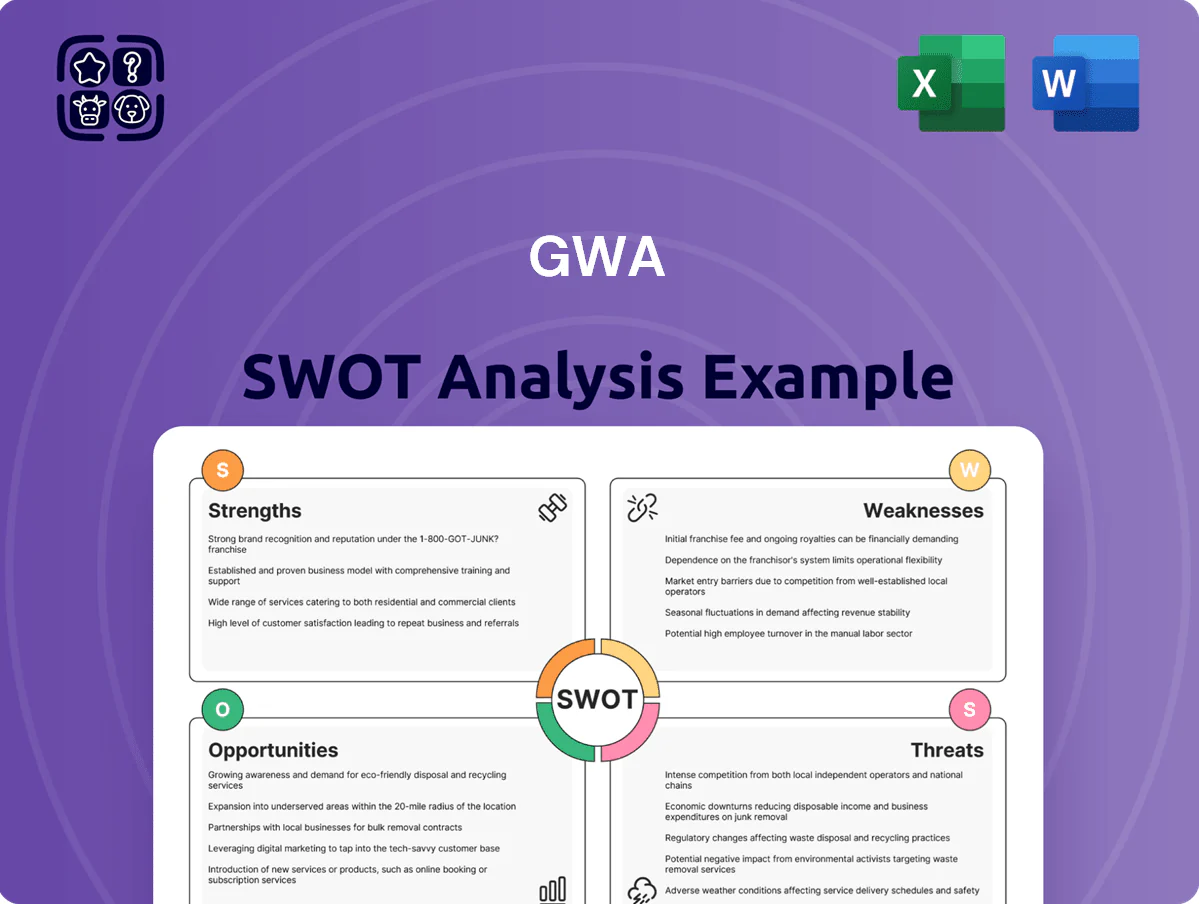

GWA SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

GWA’s SWOT preview highlights solid service diversification and regulatory resilience, counterbalanced by margin pressure and competitive threats; however, the full analysis uncovers strategic levers and financial sensitivities that matter for investors and planners.

Purchase the complete SWOT to receive a professionally written, editable Word report and Excel model with actionable recommendations, valuation context, and scenario analysis to inform confident decisions.

Strengths

Market Dominance of Iconic Brands

GWA Group’s portfolio—Caroma, Methven, Dorf—delivers market dominance in Australia and New Zealand, supporting a 2024‑25 premium pricing advantage that helped report gross margin of ~34.2% in FY2025. The brands’ high equity drives repeat demand from professional plumbers and retail buyers, keeping branded revenue at roughly 78% of total sales in FY2025. This positioning sustains pricing power and resilient volume despite market fluctuations.

Extensive Multi-Channel Distribution Network

GWA Group leverages long-term supply ties with Bunnings and Reece, giving national shelf presence across 1,400+ Bunnings stores and ~600 Reece branches as of FY2024, reaching DIY and trade buyers.

This dual-channel approach supported FY2024 domestic sales resilience: trade and retail split roughly 55/45, and gross margin held near 32.5% despite supply-cost pressures.

Advanced warehousing and a regional logistics hub network reduced inventory days to 72 in 2024, improving fill rates and lowering stockouts for large commercial projects.

Leadership in Water-Saving Innovation

GWA Group (ASX: GWA) has led water-saving fixtures for decades, with dual-flush and WELS 4–6 star tapware lowering household water use by ~30% versus legacy fittings; product-led sales helped FY2024 revenue recover to AUD 410m.

Targeted R&D spending (~2.8% of sales in 2024) aligns with ESG rules and saves customers water and costs, keeping GWA ahead of tightening Australian and NZ efficiency standards.

That engineering depth and patents create a high barrier to entry, limiting small competitors and supporting GWA’s stable domestic market share (~35% in sanitaryware as of 2024).

Resilient Financial Performance and Cash Flow

GWA maintained FY2024 underlying EBIT margin of 12.8% and generated operating cash flow of A$112m, showing resilience through 2023–24 market volatility.

That cash flow funded A$18m R&D and supported a 2024 dividend yield of 4.1%, while net debt/EBITDA stayed at a conservative 0.6x, reflecting disciplined capital management.

- FY2024 EBIT margin 12.8%

- Operating cash flow A$112m

- R&D spend A$18m

- Dividend yield 4.1%

- Net debt/EBITDA 0.6x

Comprehensive Product Portfolio for Diverse Segments

The wide range of fixtures and fittings lets GWA Group serve as a one-stop shop for residential, commercial and aged-care projects, simplifying procurement for developers and builders.

This breadth lets GWA capture value across price points and building types; FY2024 revenue mix showed 38% residential, 34% commercial and 28% aged-care/other, supporting cross-segment margins.

- One supplier for multiple segments

- Reduces developer sourcing complexity

- Captures value across price tiers

- FY2024 mix: 38% res, 34% comm, 28% aged-care/other

GWA: Strong brands drive 34% margins, A$410m revenue, 4.1% dividend yield

GWA’s strong brands (Caroma, Methven, Dorf) drove FY2025 gross margin ~34.2% and branded revenue ~78% of sales; national reach via 1,400+ Bunnings and ~600 Reece outlets supported FY2024 revenue A$410m and OCF A$112m; R&D A$18m (2.8% sales) and net debt/EBITDA 0.6x underpinned a 2024 dividend yield 4.1%.

| Metric | Value |

|---|---|

| FY2025 Gross Margin | ~34.2% |

| Branded Sales | ~78% |

| FY2024 Revenue | A$410m |

| OCF FY2024 | A$112m |

| R&D FY2024 | A$18m (2.8%) |

| Net debt/EBITDA | 0.6x |

| Dividend Yield 2024 | 4.1% |

What is included in the product

Provides a concise SWOT assessment of GWA, outlining its core strengths and weaknesses while identifying external opportunities and threats shaping its strategic outlook.

Delivers a compact GWA SWOT matrix for rapid strategy alignment and clear stakeholder briefings, enabling quick edits to reflect evolving priorities and seamless integration into reports and presentations.

Weaknesses

High Geographic Concentration in Australasia

The vast majority of GWA Group Ltd revenue—about 85% of FY2024 sales (A$576m of A$678m total)—comes from Australia and New Zealand, leaving the company highly exposed to ANZ housing cycles and consumer spending shifts.

This limited geographic diversity means a 5–10% ANZ housing-market correction or tighter plumbing/fixture regulations could cut group EBITDA materially, given domestic margins near 18% in FY2024.

International expansion into Asia and North America is underway, but current ANZ reliance remains a structural vulnerability until offshore sales exceed ~30% of revenue.

Dependency on Third-Party International Manufacturing

GWA outsources over 70% of manufacturing to Asian suppliers, leaving it exposed to supply-chain shocks: 2023 port congestion raised lead times 25% and supplier disruptions drove a 12% jump in COGS vs 2021; quality failures and recalls from vendors can hit margins and brand trust; geopolitical tensions in the South China Sea and rising freight rates (sea freight up ~40% since 2020) risk inventory shortages and higher operating costs.

Sensitivity to Residential Construction Cycles

Exposure to Raw Material and Input Cost Volatility

- Brass +18% (2024)

- Resins +12% (2024)

- Raw materials ≈28% of COGS (FY2024)

Complexity in Managing Multiple Brand Identities

Maintaining GWA Group’s multiple brands—Caroma, Methven, Dorf—raises high coordination costs; group FY2024 marketing and distribution spend was A$84.2m, pressuring margins and requiring tight brand governance to prevent internal cannibalization.

Overlapping kitchen and bathroom ranges risk confusing retailers and consumers, potentially diluting Caroma’s premium plumbing image versus Dorf’s mid-market positioning; product overlap accounted for ~12% of SKUs in 2024.

Leadership must constantly reallocate marketing budgets—inefficient spend across identities can lower ROI; GWA reported a 6.8% decline in brand-level gross margin for overlapping categories in 2024.

- High marketing/distribution cost: A$84.2m (FY2024)

- SKU overlap: ~12% of portfolio (2024)

- Gross margin impact: -6.8% in overlapping categories (2024)

ANZ-heavy A$678m business faces housing slump, rising input costs and margin squeeze

Heavy ANZ concentration (≈85% of A$678m FY2024 sales) ties revenue to local housing cycles; 2024 new approvals -18% to 137,000. High outsourcing (>70%) and input inflation (brass +18%, resins +12% in 2024; raw materials ≈28% of COGS) raise supply and margin risk. Brand/sku overlap (≈12% SKUs) and A$84.2m marketing spend pressured overlapping-category gross margins -6.8% in 2024.

| Metric | Value (2024) |

|---|---|

| ANZ sales share | ≈85% |

| Total sales | A$678m |

| New approvals | 137,000 (-18%) |

| Outsourced mfg | >70% |

| Brass | +18% |

| Resins | +12% |

| Raw mats % of COGS | ≈28% |

| Marketing & distribution | A$84.2m |

| SKU overlap | ≈12% |

| Overlap gross margin impact | -6.8% |

What You See Is What You Get

GWA SWOT Analysis

This is the actual GWA SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the complete, editable version.

You’re viewing a live excerpt of the real analysis file; the entire, detailed document becomes available immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

GWA’s SWOT preview highlights solid service diversification and regulatory resilience, counterbalanced by margin pressure and competitive threats; however, the full analysis uncovers strategic levers and financial sensitivities that matter for investors and planners.

Purchase the complete SWOT to receive a professionally written, editable Word report and Excel model with actionable recommendations, valuation context, and scenario analysis to inform confident decisions.

Strengths

Market Dominance of Iconic Brands

GWA Group’s portfolio—Caroma, Methven, Dorf—delivers market dominance in Australia and New Zealand, supporting a 2024‑25 premium pricing advantage that helped report gross margin of ~34.2% in FY2025. The brands’ high equity drives repeat demand from professional plumbers and retail buyers, keeping branded revenue at roughly 78% of total sales in FY2025. This positioning sustains pricing power and resilient volume despite market fluctuations.

Extensive Multi-Channel Distribution Network

GWA Group leverages long-term supply ties with Bunnings and Reece, giving national shelf presence across 1,400+ Bunnings stores and ~600 Reece branches as of FY2024, reaching DIY and trade buyers.

This dual-channel approach supported FY2024 domestic sales resilience: trade and retail split roughly 55/45, and gross margin held near 32.5% despite supply-cost pressures.

Advanced warehousing and a regional logistics hub network reduced inventory days to 72 in 2024, improving fill rates and lowering stockouts for large commercial projects.

Leadership in Water-Saving Innovation

GWA Group (ASX: GWA) has led water-saving fixtures for decades, with dual-flush and WELS 4–6 star tapware lowering household water use by ~30% versus legacy fittings; product-led sales helped FY2024 revenue recover to AUD 410m.

Targeted R&D spending (~2.8% of sales in 2024) aligns with ESG rules and saves customers water and costs, keeping GWA ahead of tightening Australian and NZ efficiency standards.

That engineering depth and patents create a high barrier to entry, limiting small competitors and supporting GWA’s stable domestic market share (~35% in sanitaryware as of 2024).

Resilient Financial Performance and Cash Flow

GWA maintained FY2024 underlying EBIT margin of 12.8% and generated operating cash flow of A$112m, showing resilience through 2023–24 market volatility.

That cash flow funded A$18m R&D and supported a 2024 dividend yield of 4.1%, while net debt/EBITDA stayed at a conservative 0.6x, reflecting disciplined capital management.

- FY2024 EBIT margin 12.8%

- Operating cash flow A$112m

- R&D spend A$18m

- Dividend yield 4.1%

- Net debt/EBITDA 0.6x

Comprehensive Product Portfolio for Diverse Segments

The wide range of fixtures and fittings lets GWA Group serve as a one-stop shop for residential, commercial and aged-care projects, simplifying procurement for developers and builders.

This breadth lets GWA capture value across price points and building types; FY2024 revenue mix showed 38% residential, 34% commercial and 28% aged-care/other, supporting cross-segment margins.

- One supplier for multiple segments

- Reduces developer sourcing complexity

- Captures value across price tiers

- FY2024 mix: 38% res, 34% comm, 28% aged-care/other

GWA: Strong brands drive 34% margins, A$410m revenue, 4.1% dividend yield

GWA’s strong brands (Caroma, Methven, Dorf) drove FY2025 gross margin ~34.2% and branded revenue ~78% of sales; national reach via 1,400+ Bunnings and ~600 Reece outlets supported FY2024 revenue A$410m and OCF A$112m; R&D A$18m (2.8% sales) and net debt/EBITDA 0.6x underpinned a 2024 dividend yield 4.1%.

| Metric | Value |

|---|---|

| FY2025 Gross Margin | ~34.2% |

| Branded Sales | ~78% |

| FY2024 Revenue | A$410m |

| OCF FY2024 | A$112m |

| R&D FY2024 | A$18m (2.8%) |

| Net debt/EBITDA | 0.6x |

| Dividend Yield 2024 | 4.1% |

What is included in the product

Provides a concise SWOT assessment of GWA, outlining its core strengths and weaknesses while identifying external opportunities and threats shaping its strategic outlook.

Delivers a compact GWA SWOT matrix for rapid strategy alignment and clear stakeholder briefings, enabling quick edits to reflect evolving priorities and seamless integration into reports and presentations.

Weaknesses

High Geographic Concentration in Australasia

The vast majority of GWA Group Ltd revenue—about 85% of FY2024 sales (A$576m of A$678m total)—comes from Australia and New Zealand, leaving the company highly exposed to ANZ housing cycles and consumer spending shifts.

This limited geographic diversity means a 5–10% ANZ housing-market correction or tighter plumbing/fixture regulations could cut group EBITDA materially, given domestic margins near 18% in FY2024.

International expansion into Asia and North America is underway, but current ANZ reliance remains a structural vulnerability until offshore sales exceed ~30% of revenue.

Dependency on Third-Party International Manufacturing

GWA outsources over 70% of manufacturing to Asian suppliers, leaving it exposed to supply-chain shocks: 2023 port congestion raised lead times 25% and supplier disruptions drove a 12% jump in COGS vs 2021; quality failures and recalls from vendors can hit margins and brand trust; geopolitical tensions in the South China Sea and rising freight rates (sea freight up ~40% since 2020) risk inventory shortages and higher operating costs.

Sensitivity to Residential Construction Cycles

Exposure to Raw Material and Input Cost Volatility

- Brass +18% (2024)

- Resins +12% (2024)

- Raw materials ≈28% of COGS (FY2024)

Complexity in Managing Multiple Brand Identities

Maintaining GWA Group’s multiple brands—Caroma, Methven, Dorf—raises high coordination costs; group FY2024 marketing and distribution spend was A$84.2m, pressuring margins and requiring tight brand governance to prevent internal cannibalization.

Overlapping kitchen and bathroom ranges risk confusing retailers and consumers, potentially diluting Caroma’s premium plumbing image versus Dorf’s mid-market positioning; product overlap accounted for ~12% of SKUs in 2024.

Leadership must constantly reallocate marketing budgets—inefficient spend across identities can lower ROI; GWA reported a 6.8% decline in brand-level gross margin for overlapping categories in 2024.

- High marketing/distribution cost: A$84.2m (FY2024)

- SKU overlap: ~12% of portfolio (2024)

- Gross margin impact: -6.8% in overlapping categories (2024)

ANZ-heavy A$678m business faces housing slump, rising input costs and margin squeeze

Heavy ANZ concentration (≈85% of A$678m FY2024 sales) ties revenue to local housing cycles; 2024 new approvals -18% to 137,000. High outsourcing (>70%) and input inflation (brass +18%, resins +12% in 2024; raw materials ≈28% of COGS) raise supply and margin risk. Brand/sku overlap (≈12% SKUs) and A$84.2m marketing spend pressured overlapping-category gross margins -6.8% in 2024.

| Metric | Value (2024) |

|---|---|

| ANZ sales share | ≈85% |

| Total sales | A$678m |

| New approvals | 137,000 (-18%) |

| Outsourced mfg | >70% |

| Brass | +18% |

| Resins | +12% |

| Raw mats % of COGS | ≈28% |

| Marketing & distribution | A$84.2m |

| SKU overlap | ≈12% |

| Overlap gross margin impact | -6.8% |

What You See Is What You Get

GWA SWOT Analysis

This is the actual GWA SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the complete, editable version.

You’re viewing a live excerpt of the real analysis file; the entire, detailed document becomes available immediately after checkout.