Great Wall Motor Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Great Wall Motor faces intense competitive rivalry, rising buyer expectations, and evolving EV-related supplier dynamics that together reshape profit potential and strategic priorities; this snapshot highlights key pressure points but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable implications tailored to Great Wall Motor for smarter investment and strategy decisions.

Suppliers Bargaining Power

High Degree of Vertical Integration

Great Wall Motor (GWM) cuts supplier power via vertical integration: subsidiaries Hycet and Svolt produce engines, transmissions, and battery cells, covering an estimated 40–55% of core parts by value as of 2024, lowering external supplier spend and exposure. In 2024 GWM’s in-house battery output rose to ~30 GWh capacity, reducing procurement volatility and shielding margins from component price spikes and supply shocks.

Reliance on Critical Raw Materials

Despite vertical integration, Great Wall Motor (GWM) remains exposed to suppliers of lithium, cobalt and high-strength steel; lithium prices rose ~120% from 2020 to 2023 and battery-grade lithium carbonate averaged $55,000/ton in 2024, raising input costs for GWM’s Ora EV line. As Ora expands, GWM’s reliance on global miners (e.g., SQM, Tianqi) increases, giving suppliers leverage due to finite reserves and surging EV battery demand—global lithium demand forecast +52% by 2027.

Strategic Semiconductor Partnerships

While Great Wall Motor is building in-house automotive chip design, it still depends on global semiconductor leaders like Qualcomm and Nvidia for high-end SoCs and smart cockpit chips; these suppliers held ~40–60% ASP premiums in 2024 for premium automotive processors. Their tech is critical for advanced driver assistance, giving them strong bargaining power. GWM reduces risk via multi-year supply deals and equity ties, securing priority access to scarce wafers and cutting lead times by an estimated 20–30% in 2024. What this hides: pricing remains sensitive to node shortages and export controls.

Standardized Commodity Parts

For standardized commodity parts like glass, tires, and interior plastics, supplier power is low for Great Wall Motor (GWM); in 2024 over 60% of these parts were sourced from a competitive pool of domestic and global vendors, pressuring prices down.

This vendor depth helps GWM keep COGS low on mass-market Haval SUVs, supporting a gross margin ~18% in 2024 versus 12–14% for some rivals.

- Low supplier power: many vendors

- 2024: >60% standardized sourcing

- GWM gross margin ~18% (2024)

- Supports cost advantage for Haval series

Transition to New Energy Systems

GWM's move to hydrogen fuel cells in its Forest Ecosystem raises supplier power: few qualified makers of high‑pressure storage and membrane electrode assemblies (MEAs) control pricing and delivery, pushing premiums ~15–30% vs standard parts in 2024 procurement data.

GWM plans to internalize key stack and storage tech with accelerated R&D and pilot lines, targeting in‑house production by end‑2025 to cut supplier dependence and reduce component cost by an estimated 20%.

- Few qualified hydrogen suppliers → higher leverage

- 2024 premiums ~15–30% on niche components

- GWM aims in‑house production end‑2025

- Projected component cost cut ~20%

GWM boosts margins via vertical integration—40–55% in‑house, 30GWh batteries, ~18% GM

GWM cuts supplier power via vertical integration (Hycet, Svolt): 40–55% core parts in‑house (2024), battery output ~30 GWh (2024), gross margin ~18% (2024).

| Metric | 2024 value |

|---|---|

| In‑house parts (% value) | 40–55% |

| Battery capacity | ~30 GWh |

| Gross margin | ~18% |

| Lithium price (LC/kg equiv.) | $55,000/ton |

| Hydrogen premium | +15–30% |

What is included in the product

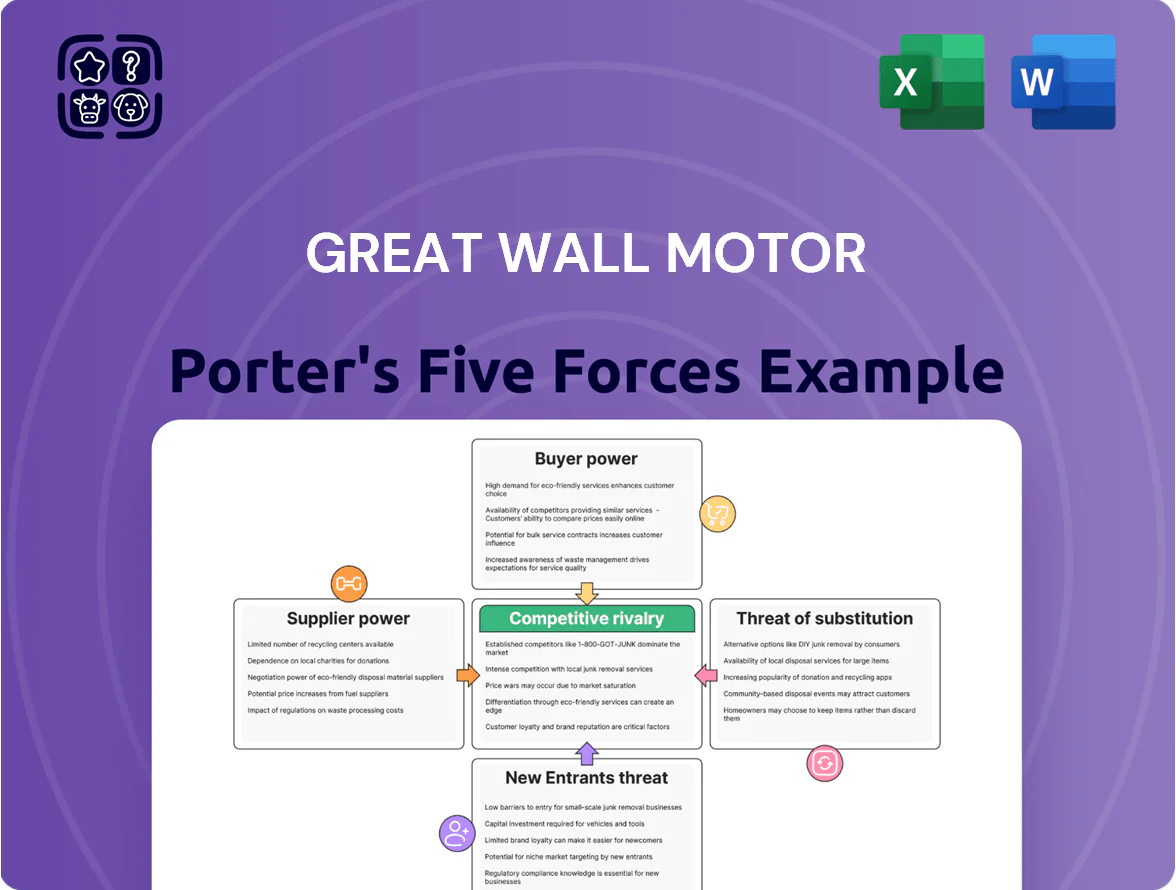

Tailored Porter's Five Forces analysis for Great Wall Motor uncovering competitive intensity, buyer and supplier leverage, threat of substitutes and new entrants, and strategic implications for pricing, profitability, and market defense.

Condensed Porter's Five Forces for Great Wall Motor—one-sheet clarity to pinpoint competitive threats and opportunities fast.

Customers Bargaining Power

High Volume of Market Alternatives

Chinese buyers face 300+ passenger vehicle brands and over 28 million new-car sales in 2024, so GWM’s Haval and Wey compete directly with BYD, Geely, Chery on price and specs.

This saturation means customers easily compare features, driving GWM to match rivals’ EV ranges (BYD ~600 km NEDC) and keep margins tight—2024 gross margin pressure noted across Chinese OEMs.

Information Transparency and Digital Comparison

Modern buyers use digital platforms and social media to compare prices, specs, and reviews; global auto shoppers rely on sites like Autohome and CarGurus where 72% consult online reviews before purchase (2024 JD Power data), raising price sensitivity for GWM.

This transparency lets customers demand better prices and hold Great Wall Motor (GWM) accountable for defects—recalls and warranty claims cut margins, as seen in China's 2023 auto warranty expense rise of ~0.4 percentage points industry-wide.

To influence informed buyers, GWM must boost digital marketing and CRM spend; automakers' median digital ad spend rose 22% in 2024, and reallocating ~1–2% of revenue to CRM could lift retention in export markets.

Low Switching Costs for Individual Buyers

For the average passenger-vehicle buyer, switching from Great Wall Motor to rivals is cheap—no lease penalties and median trade-in loss under $2,000 in China 2024, so retention rests on GWM.

GWM counters with improved after-sales: 1,800+ service centers in China by Dec 2024 and a reported 12% rise in paid service visits year-on-year, plus trade-in incentives up to ¥10,000 to reduce churn.

Price Sensitivity in Mass Market Segments

A large share of Great Wall Motor (GWM) sales—about 62% of 2024 unit volumes—comes from price-sensitive SUV and pickup buyers, making demand highly elastic; a 1% price rise risks a >1% drop in volume in mass segments.

Chinese price wars and frequent incentives (average dealer discount ~6% in 2024) have trained customers to expect promotions, constraining GWM’s pricing power and margin expansion.

- 62% of 2024 volumes from budget SUVs/pickups

- Average dealer discount ≈6% in 2024

- Price rises >1% likely cut volumes >1%

Niche Power in Specialized Segments

In niche off-road segments served by the Tank brand, customer bargaining power is slightly lower because fewer direct alternatives exist; Tank sold about 43,000 units in 2024, giving Great Wall Motor (GWM) room to charge premiums near 8–12% above mainstream SUV pricing.

That edge is eroding as rivals like Ford and Toyota expand rugged SUV launches and new Chinese entrants increased hardcore SUV offerings by ~25% in 2024, compressing margins and strengthening buyer leverage.

- Tank 2024 sales ~43,000 units

- Price premium ~8–12% vs mainstream SUVs

- Hardcore SUV entrants up ~25% in 2024

- Buyer leverage rising, margin compression evident

Buyers Rule: Price-Sensitive Market Shrinks Tank’s Premium as Competition Surges

Buyers are highly powerful: 300+ brands, 28M new-car sales (2024), 62% of GWM volumes price-sensitive; avg dealer discount ~6% (2024); 1% price rise risks >1% volume drop. Tank niche weaker: 43,000 units (2024), 8–12% premium but competitors up 25% (2024) eroding advantage.

| Metric | 2024 |

|---|---|

| New-car sales China | 28M |

| GWM volume share price-sensitive | 62% |

| Avg dealer discount | ~6% |

| Tank sales | 43,000 |

Same Document Delivered

Great Wall Motor Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Great Wall Motor you'll receive immediately after purchase—no placeholders, no samples.

The document displayed here is the final, professionally formatted file covering competitive rivalry, buyer and supplier power, threats of new entrants and substitutes, and strategic implications.

Once you complete your purchase, you’ll have instant access to this same ready-to-use analysis for download and application.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Great Wall Motor faces intense competitive rivalry, rising buyer expectations, and evolving EV-related supplier dynamics that together reshape profit potential and strategic priorities; this snapshot highlights key pressure points but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable implications tailored to Great Wall Motor for smarter investment and strategy decisions.

Suppliers Bargaining Power

High Degree of Vertical Integration

Great Wall Motor (GWM) cuts supplier power via vertical integration: subsidiaries Hycet and Svolt produce engines, transmissions, and battery cells, covering an estimated 40–55% of core parts by value as of 2024, lowering external supplier spend and exposure. In 2024 GWM’s in-house battery output rose to ~30 GWh capacity, reducing procurement volatility and shielding margins from component price spikes and supply shocks.

Reliance on Critical Raw Materials

Despite vertical integration, Great Wall Motor (GWM) remains exposed to suppliers of lithium, cobalt and high-strength steel; lithium prices rose ~120% from 2020 to 2023 and battery-grade lithium carbonate averaged $55,000/ton in 2024, raising input costs for GWM’s Ora EV line. As Ora expands, GWM’s reliance on global miners (e.g., SQM, Tianqi) increases, giving suppliers leverage due to finite reserves and surging EV battery demand—global lithium demand forecast +52% by 2027.

Strategic Semiconductor Partnerships

While Great Wall Motor is building in-house automotive chip design, it still depends on global semiconductor leaders like Qualcomm and Nvidia for high-end SoCs and smart cockpit chips; these suppliers held ~40–60% ASP premiums in 2024 for premium automotive processors. Their tech is critical for advanced driver assistance, giving them strong bargaining power. GWM reduces risk via multi-year supply deals and equity ties, securing priority access to scarce wafers and cutting lead times by an estimated 20–30% in 2024. What this hides: pricing remains sensitive to node shortages and export controls.

Standardized Commodity Parts

For standardized commodity parts like glass, tires, and interior plastics, supplier power is low for Great Wall Motor (GWM); in 2024 over 60% of these parts were sourced from a competitive pool of domestic and global vendors, pressuring prices down.

This vendor depth helps GWM keep COGS low on mass-market Haval SUVs, supporting a gross margin ~18% in 2024 versus 12–14% for some rivals.

- Low supplier power: many vendors

- 2024: >60% standardized sourcing

- GWM gross margin ~18% (2024)

- Supports cost advantage for Haval series

Transition to New Energy Systems

GWM's move to hydrogen fuel cells in its Forest Ecosystem raises supplier power: few qualified makers of high‑pressure storage and membrane electrode assemblies (MEAs) control pricing and delivery, pushing premiums ~15–30% vs standard parts in 2024 procurement data.

GWM plans to internalize key stack and storage tech with accelerated R&D and pilot lines, targeting in‑house production by end‑2025 to cut supplier dependence and reduce component cost by an estimated 20%.

- Few qualified hydrogen suppliers → higher leverage

- 2024 premiums ~15–30% on niche components

- GWM aims in‑house production end‑2025

- Projected component cost cut ~20%

GWM boosts margins via vertical integration—40–55% in‑house, 30GWh batteries, ~18% GM

GWM cuts supplier power via vertical integration (Hycet, Svolt): 40–55% core parts in‑house (2024), battery output ~30 GWh (2024), gross margin ~18% (2024).

| Metric | 2024 value |

|---|---|

| In‑house parts (% value) | 40–55% |

| Battery capacity | ~30 GWh |

| Gross margin | ~18% |

| Lithium price (LC/kg equiv.) | $55,000/ton |

| Hydrogen premium | +15–30% |

What is included in the product

Tailored Porter's Five Forces analysis for Great Wall Motor uncovering competitive intensity, buyer and supplier leverage, threat of substitutes and new entrants, and strategic implications for pricing, profitability, and market defense.

Condensed Porter's Five Forces for Great Wall Motor—one-sheet clarity to pinpoint competitive threats and opportunities fast.

Customers Bargaining Power

High Volume of Market Alternatives

Chinese buyers face 300+ passenger vehicle brands and over 28 million new-car sales in 2024, so GWM’s Haval and Wey compete directly with BYD, Geely, Chery on price and specs.

This saturation means customers easily compare features, driving GWM to match rivals’ EV ranges (BYD ~600 km NEDC) and keep margins tight—2024 gross margin pressure noted across Chinese OEMs.

Information Transparency and Digital Comparison

Modern buyers use digital platforms and social media to compare prices, specs, and reviews; global auto shoppers rely on sites like Autohome and CarGurus where 72% consult online reviews before purchase (2024 JD Power data), raising price sensitivity for GWM.

This transparency lets customers demand better prices and hold Great Wall Motor (GWM) accountable for defects—recalls and warranty claims cut margins, as seen in China's 2023 auto warranty expense rise of ~0.4 percentage points industry-wide.

To influence informed buyers, GWM must boost digital marketing and CRM spend; automakers' median digital ad spend rose 22% in 2024, and reallocating ~1–2% of revenue to CRM could lift retention in export markets.

Low Switching Costs for Individual Buyers

For the average passenger-vehicle buyer, switching from Great Wall Motor to rivals is cheap—no lease penalties and median trade-in loss under $2,000 in China 2024, so retention rests on GWM.

GWM counters with improved after-sales: 1,800+ service centers in China by Dec 2024 and a reported 12% rise in paid service visits year-on-year, plus trade-in incentives up to ¥10,000 to reduce churn.

Price Sensitivity in Mass Market Segments

A large share of Great Wall Motor (GWM) sales—about 62% of 2024 unit volumes—comes from price-sensitive SUV and pickup buyers, making demand highly elastic; a 1% price rise risks a >1% drop in volume in mass segments.

Chinese price wars and frequent incentives (average dealer discount ~6% in 2024) have trained customers to expect promotions, constraining GWM’s pricing power and margin expansion.

- 62% of 2024 volumes from budget SUVs/pickups

- Average dealer discount ≈6% in 2024

- Price rises >1% likely cut volumes >1%

Niche Power in Specialized Segments

In niche off-road segments served by the Tank brand, customer bargaining power is slightly lower because fewer direct alternatives exist; Tank sold about 43,000 units in 2024, giving Great Wall Motor (GWM) room to charge premiums near 8–12% above mainstream SUV pricing.

That edge is eroding as rivals like Ford and Toyota expand rugged SUV launches and new Chinese entrants increased hardcore SUV offerings by ~25% in 2024, compressing margins and strengthening buyer leverage.

- Tank 2024 sales ~43,000 units

- Price premium ~8–12% vs mainstream SUVs

- Hardcore SUV entrants up ~25% in 2024

- Buyer leverage rising, margin compression evident

Buyers Rule: Price-Sensitive Market Shrinks Tank’s Premium as Competition Surges

Buyers are highly powerful: 300+ brands, 28M new-car sales (2024), 62% of GWM volumes price-sensitive; avg dealer discount ~6% (2024); 1% price rise risks >1% volume drop. Tank niche weaker: 43,000 units (2024), 8–12% premium but competitors up 25% (2024) eroding advantage.

| Metric | 2024 |

|---|---|

| New-car sales China | 28M |

| GWM volume share price-sensitive | 62% |

| Avg dealer discount | ~6% |

| Tank sales | 43,000 |

Same Document Delivered

Great Wall Motor Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Great Wall Motor you'll receive immediately after purchase—no placeholders, no samples.

The document displayed here is the final, professionally formatted file covering competitive rivalry, buyer and supplier power, threats of new entrants and substitutes, and strategic implications.

Once you complete your purchase, you’ll have instant access to this same ready-to-use analysis for download and application.