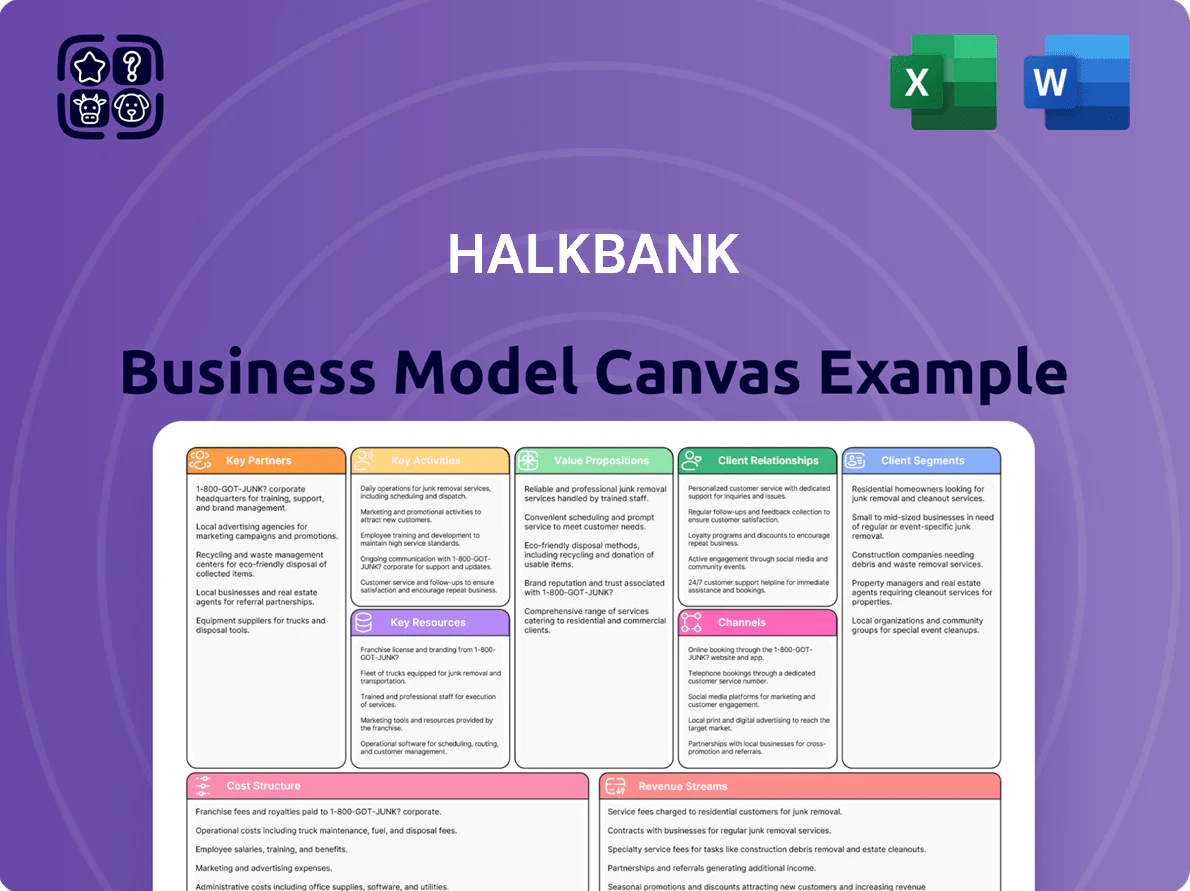

Halkbank Business Model Canvas

Halkbank Business Model Canvas: How the Bank Scales Value, Partners & Revenue

Discover Halkbank’s strategic engine with our concise Business Model Canvas—covering customer segments, value propositions, key partners, and revenue streams to show how the bank scales and sustains growth.

Partnerships

Turkish Wealth Fund and Government Entities

The Turkish Wealth Fund (Türkiye Varlık Fonu), as Halkbank’s majority shareholder since 2019, provides capital stability—the fund injected equity and guarantees supporting Halkbank’s CET1 ratio, which stood at ~12.5% in Q3 2025—and aligns the bank with national growth targets. This link lets Halkbank finance large public projects and state credit schemes (TL-denominated infrastructure loans exceeding TL 40bn in 2024) and, via ministries, channel targeted subsidies to SMEs and agriculture.

International Financial Institutions

Halkbank partners with institutions like the World Bank and European Investment Bank to secure long-term funding—€500m from EIB in 2023 and a $200m World Bank facility in 2024—for sustainable projects and green lending. These lines include dedicated credit for female entrepreneurs, boosting green financing share to 18% of new loans in 2024 and widening international credibility and funding diversification.

Fintech and Technology Providers

Collaboration with fintechs and tech firms lets Halkbank integrate blockchain, AI risk models, and mobile payments; in 2024 Halkbank ran pilots with 3 fintechs and reduced loan processing time 28% year-over-year.

These partners supply core infrastructure and cybersecurity; Halkbank spent TL 210 million on IT and third-party integrations in 2024 to keep API, AML, and mobile-wallet uptime above 99.8%.

Tradesmen and Artisan Cooperatives

- Partner: Turkish Confederation of Tradesmen and Craftsmen

- Reach: ~3.5 million small businesses

- 2024 SME lending: TL 18.4 billion

- Coverage: all 81 provinces, granular local access

Correspondent Banking Network

Halkbank’s correspondent banking network enables international trade finance, letters of credit, and cross-border transfers for corporates, supporting exporters/importers across Europe, MENA, and Central Asia; in 2024 correspondent-facilitated FX and trade flows helped underpin roughly 18% of Halkbank’s non-interest income (≈TRY 1.9bn).

- Global reach: partners in 60+ countries

- Supports letters of credit and trade finance

- Provides access to FX liquidity and cross-border payments

Halkbank partners deliver €500m+ funding, tech-driven 28% faster lending, TL18.4bn SME reach

Halkbank’s key partners—Türkiye Varlık Fonu, EIB/World Bank, fintechs, Turkish Confederation of Tradesmen and Craftsmen, and 60+ correspondent banks—provide capital stability, €500m+ long-term funding, tech integration (3 pilots; 28% faster loan processing in 2024), TL 18.4bn SME lending reach (~3.5m firms), and trade finance supporting ≈TRY 1.9bn non-interest income (2024).

| Partner | Key metric (2024/2025) |

|---|---|

| Türkiye Varlık Fonu | CET1 ≈12.5% Q3 2025 |

| EIB/World Bank | €500m (EIB 2023), $200m (WB 2024) |

| Fintechs/Tech | 3 pilots; −28% loan time (2024) |

| Tradesmen Confed. | Reach ≈3.5m; TL 18.4bn SME loans |

| Correspondents | 60+ countries; ≈TRY 1.9bn non-interest income |

What is included in the product

A concise Business Model Canvas for Halkbank detailing customer segments, value propositions, channels, revenue streams, key resources and partners, cost structure, and risk factors, reflecting real-world banking operations and competitive advantages for use in presentations and investor discussions.

High-level Halkbank Business Model Canvas that condenses its retail and corporate banking strategy into an editable one-page snapshot, saving hours of setup and enabling quick comparison, team collaboration, and boardroom-ready presentations.

Activities

Credit and Loan Disbursement

Halkbank rigorously evaluates and disburses credit to SMEs, corporates and individuals, emphasizing working capital and investment loans that support industrial production and trade; as of 2024 its corporate and commercial loan book was about TRY 280 billion, with SME loans ~TRY 95 billion. The process uses comprehensive credit scoring and collateral management to keep non-performing loans near the sector median (NPL ratio ~4.5% in 2024).

Deposit and Liquidity Management

Halkbank manages ~TRY 850bn in deposits (2024 annual report) to keep its loan-to-deposit ratio near 90%, using competitive retail/institutional rates and active treasury trades to control funding costs. Effective cash-flow forecasting and short-term liquidity buffers let the bank meet regulatory LCR (liquidity coverage ratio) targets—around 140% in 2024—while maximizing returns on overnight and government securities.

Digital Banking Transformation

Risk Management and Compliance

Halkbank continuously monitors market, credit and operational risks to protect its capital and meet BRSA rules, aligning capital adequacy with Basel III; as of 2024 CET1 ratio stood near 12.0% and total CAR ~16.5% (BRSA reporting).

Robust internal audit and anti-fraud controls support IFRS financial integrity and regulatory reporting, with credit cost-of-risk around 120 bp in 2024.

- Basel III alignment: CET1 ~12.0%

- Total CAR ~16.5%

- Credit cost-of-risk ~1.20%

- Continuous BRSA compliance monitoring

- Strong internal audit & anti-fraud controls

SME Development and Advisory

Halkbank runs SME capacity-building—financial literacy courses and strategic workshops—that raise borrower quality and lower default risk; in 2024 its SME advisory touched ~45,000 firms, coinciding with a 1.8 percentage-point fall in SME NPLs year-on-year.

These consulting services improve management, boost resilience and deepen loyalty, supporting Halkbank’s core SME loan book (~TRY 120 billion in 2024).

- ~45,000 SMEs trained in 2024

- SME NPLs down 1.8 pp YoY

- SME loan book ≈ TRY 120 billion (2024)

Halkbank: TRY 400bn loans, TRY 850bn deposits, strong liquidity & falling SME NPLs

Halkbank issues and services ~TRY 280bn corporate/commercial loans and ~TRY 120bn SME loans (2024), manages ~TRY 850bn deposits, keeps L/D ≈90%, LCR ≈140%, CET1 ≈12.0% and CAR ≈16.5%, and runs SME training (≈45,000 firms in 2024) while reducing NPLs (~4.5% overall; SME NPLs down 1.8 pp YOY).

| Metric | 2024 |

|---|---|

| Corporate/commercial loans | TRY 280bn |

| SME loan book | TRY 120bn |

| Deposits | TRY 850bn |

| Loan-to-deposit | ≈90% |

| LCR | ≈140% |

| CET1 | ≈12.0% |

| Total CAR | ≈16.5% |

| Overall NPL | ≈4.5% |

| SME training reach | ≈45,000 firms |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the actual Halkbank Business Model Canvas—not a mockup or sample—and it reflects the exact content and layout of the final deliverable you’ll receive after purchase.

When you complete your order, you’ll gain access to this same professional, ready-to-edit file in Word and Excel formats, with all sections included and formatted exactly as shown here.

We provide full transparency: no placeholders, no surprises—what you see in the preview is the precise document you will download and use immediately.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Halkbank Business Model Canvas: How the Bank Scales Value, Partners & Revenue

Discover Halkbank’s strategic engine with our concise Business Model Canvas—covering customer segments, value propositions, key partners, and revenue streams to show how the bank scales and sustains growth.

Partnerships

Turkish Wealth Fund and Government Entities

The Turkish Wealth Fund (Türkiye Varlık Fonu), as Halkbank’s majority shareholder since 2019, provides capital stability—the fund injected equity and guarantees supporting Halkbank’s CET1 ratio, which stood at ~12.5% in Q3 2025—and aligns the bank with national growth targets. This link lets Halkbank finance large public projects and state credit schemes (TL-denominated infrastructure loans exceeding TL 40bn in 2024) and, via ministries, channel targeted subsidies to SMEs and agriculture.

International Financial Institutions

Halkbank partners with institutions like the World Bank and European Investment Bank to secure long-term funding—€500m from EIB in 2023 and a $200m World Bank facility in 2024—for sustainable projects and green lending. These lines include dedicated credit for female entrepreneurs, boosting green financing share to 18% of new loans in 2024 and widening international credibility and funding diversification.

Fintech and Technology Providers

Collaboration with fintechs and tech firms lets Halkbank integrate blockchain, AI risk models, and mobile payments; in 2024 Halkbank ran pilots with 3 fintechs and reduced loan processing time 28% year-over-year.

These partners supply core infrastructure and cybersecurity; Halkbank spent TL 210 million on IT and third-party integrations in 2024 to keep API, AML, and mobile-wallet uptime above 99.8%.

Tradesmen and Artisan Cooperatives

- Partner: Turkish Confederation of Tradesmen and Craftsmen

- Reach: ~3.5 million small businesses

- 2024 SME lending: TL 18.4 billion

- Coverage: all 81 provinces, granular local access

Correspondent Banking Network

Halkbank’s correspondent banking network enables international trade finance, letters of credit, and cross-border transfers for corporates, supporting exporters/importers across Europe, MENA, and Central Asia; in 2024 correspondent-facilitated FX and trade flows helped underpin roughly 18% of Halkbank’s non-interest income (≈TRY 1.9bn).

- Global reach: partners in 60+ countries

- Supports letters of credit and trade finance

- Provides access to FX liquidity and cross-border payments

Halkbank partners deliver €500m+ funding, tech-driven 28% faster lending, TL18.4bn SME reach

Halkbank’s key partners—Türkiye Varlık Fonu, EIB/World Bank, fintechs, Turkish Confederation of Tradesmen and Craftsmen, and 60+ correspondent banks—provide capital stability, €500m+ long-term funding, tech integration (3 pilots; 28% faster loan processing in 2024), TL 18.4bn SME lending reach (~3.5m firms), and trade finance supporting ≈TRY 1.9bn non-interest income (2024).

| Partner | Key metric (2024/2025) |

|---|---|

| Türkiye Varlık Fonu | CET1 ≈12.5% Q3 2025 |

| EIB/World Bank | €500m (EIB 2023), $200m (WB 2024) |

| Fintechs/Tech | 3 pilots; −28% loan time (2024) |

| Tradesmen Confed. | Reach ≈3.5m; TL 18.4bn SME loans |

| Correspondents | 60+ countries; ≈TRY 1.9bn non-interest income |

What is included in the product

A concise Business Model Canvas for Halkbank detailing customer segments, value propositions, channels, revenue streams, key resources and partners, cost structure, and risk factors, reflecting real-world banking operations and competitive advantages for use in presentations and investor discussions.

High-level Halkbank Business Model Canvas that condenses its retail and corporate banking strategy into an editable one-page snapshot, saving hours of setup and enabling quick comparison, team collaboration, and boardroom-ready presentations.

Activities

Credit and Loan Disbursement

Halkbank rigorously evaluates and disburses credit to SMEs, corporates and individuals, emphasizing working capital and investment loans that support industrial production and trade; as of 2024 its corporate and commercial loan book was about TRY 280 billion, with SME loans ~TRY 95 billion. The process uses comprehensive credit scoring and collateral management to keep non-performing loans near the sector median (NPL ratio ~4.5% in 2024).

Deposit and Liquidity Management

Halkbank manages ~TRY 850bn in deposits (2024 annual report) to keep its loan-to-deposit ratio near 90%, using competitive retail/institutional rates and active treasury trades to control funding costs. Effective cash-flow forecasting and short-term liquidity buffers let the bank meet regulatory LCR (liquidity coverage ratio) targets—around 140% in 2024—while maximizing returns on overnight and government securities.

Digital Banking Transformation

Risk Management and Compliance

Halkbank continuously monitors market, credit and operational risks to protect its capital and meet BRSA rules, aligning capital adequacy with Basel III; as of 2024 CET1 ratio stood near 12.0% and total CAR ~16.5% (BRSA reporting).

Robust internal audit and anti-fraud controls support IFRS financial integrity and regulatory reporting, with credit cost-of-risk around 120 bp in 2024.

- Basel III alignment: CET1 ~12.0%

- Total CAR ~16.5%

- Credit cost-of-risk ~1.20%

- Continuous BRSA compliance monitoring

- Strong internal audit & anti-fraud controls

SME Development and Advisory

Halkbank runs SME capacity-building—financial literacy courses and strategic workshops—that raise borrower quality and lower default risk; in 2024 its SME advisory touched ~45,000 firms, coinciding with a 1.8 percentage-point fall in SME NPLs year-on-year.

These consulting services improve management, boost resilience and deepen loyalty, supporting Halkbank’s core SME loan book (~TRY 120 billion in 2024).

- ~45,000 SMEs trained in 2024

- SME NPLs down 1.8 pp YoY

- SME loan book ≈ TRY 120 billion (2024)

Halkbank: TRY 400bn loans, TRY 850bn deposits, strong liquidity & falling SME NPLs

Halkbank issues and services ~TRY 280bn corporate/commercial loans and ~TRY 120bn SME loans (2024), manages ~TRY 850bn deposits, keeps L/D ≈90%, LCR ≈140%, CET1 ≈12.0% and CAR ≈16.5%, and runs SME training (≈45,000 firms in 2024) while reducing NPLs (~4.5% overall; SME NPLs down 1.8 pp YOY).

| Metric | 2024 |

|---|---|

| Corporate/commercial loans | TRY 280bn |

| SME loan book | TRY 120bn |

| Deposits | TRY 850bn |

| Loan-to-deposit | ≈90% |

| LCR | ≈140% |

| CET1 | ≈12.0% |

| Total CAR | ≈16.5% |

| Overall NPL | ≈4.5% |

| SME training reach | ≈45,000 firms |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the actual Halkbank Business Model Canvas—not a mockup or sample—and it reflects the exact content and layout of the final deliverable you’ll receive after purchase.

When you complete your order, you’ll gain access to this same professional, ready-to-edit file in Word and Excel formats, with all sections included and formatted exactly as shown here.

We provide full transparency: no placeholders, no surprises—what you see in the preview is the precise document you will download and use immediately.