Hanwha Aerospace Business Model Canvas

Hanwha Aerospace: Concise Business Model Canvas for Investors & Executives

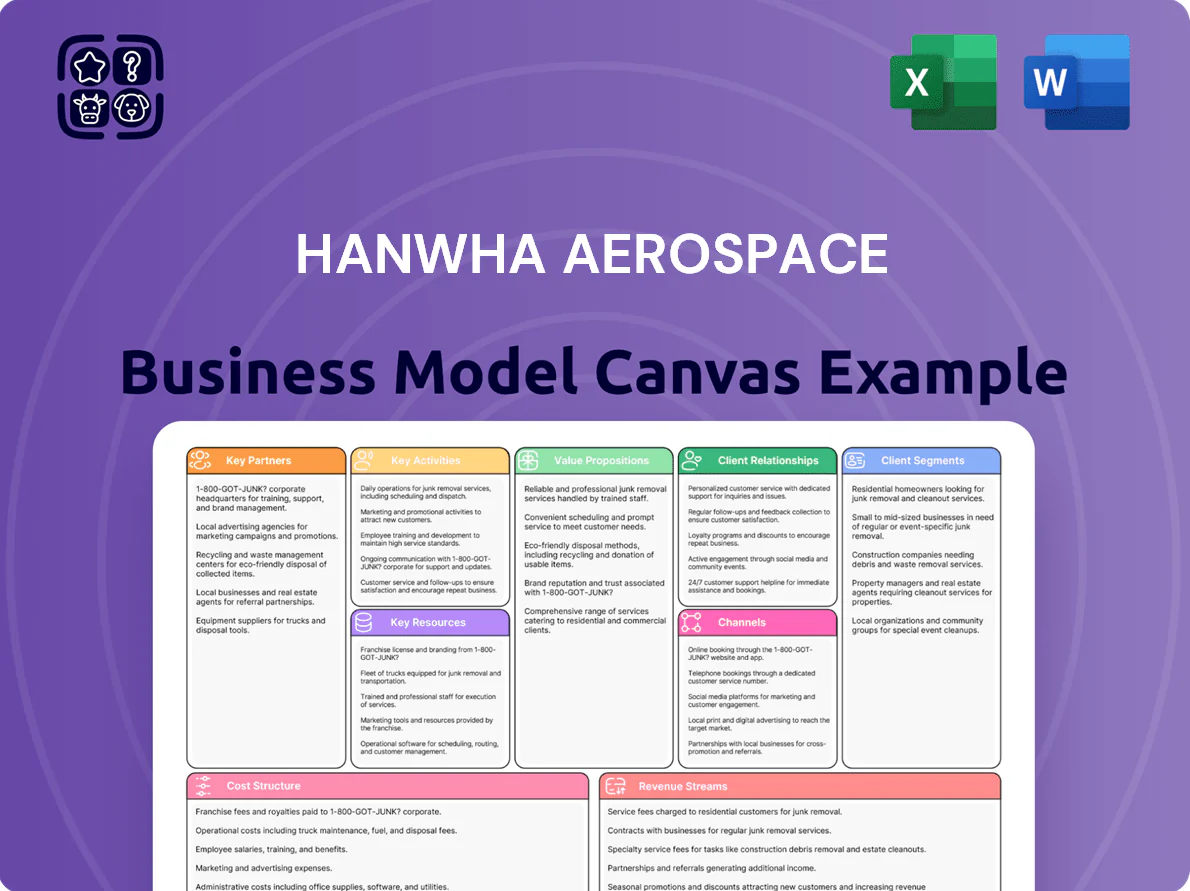

Unlock the full strategic blueprint behind Hanwha Aerospace’s business model—this concise Business Model Canvas maps value propositions, key partners, revenue streams, and growth levers to show how the company wins in defense and aerospace markets; ideal for investors, consultants, and executives seeking actionable insights.

Partnerships

Global Aero-Engine OEM Alliances

Hanwha Aerospace holds risk- and revenue-sharing partnerships with Pratt & Whitney, General Electric, and Rolls-Royce, jointly developing and producing high-tech engine components for commercial and military aircraft; these alliances underpin contracts representing about $1.2 billion in backlog through 2025. By sharing development costs and aftermarket revenue, Hanwha secures program positions on major platforms—reducing capital exposure while targeting mid-single-digit EBIT margin uplift from joint programs.

International Defense Procurement Agencies

Hanwha Aerospace deepens ties with foreign ministries of defense in Poland, Australia, and Egypt to secure multi-year export contracts—eg, Poland’s 2022 K9 order ~PLN 4.6bn (~USD 1.1bn) and Australia’s 2021 Redback program with potential fleet spend >USD 6bn—often via local production and tech-transfer offsets to meet procurement rules.

Domestic Research and Space Institutions

Close collaboration with the Korea Aerospace Research Institute (KARI) and other state-funded bodies secures Hanwha Aerospace’s leadership in South Korea’s space sector, supporting the Nuri launch vehicle program which recorded three successful launches by 2025 and a national budget allocation of KRW 1.5 trillion (2023–25) for space R&D. These partnerships accelerate lunar tech development and let Hanwha tap academic labs and government testbeds to stay at the cutting edge of aerospace innovation and national strategic projects.

Tier Two Component and Material Suppliers

A robust network of specialized suppliers provides high-grade titanium, specialty alloys, and electronic components necessary for Hanwha Aerospace’s precision manufacturing; in 2024 Hanwha reported supply-chain investments of ~KRW 120 billion to strengthen parts sourcing and quality control.

Hanwha runs supplier development programs to boost quality and resilience, reducing supplier-related delays by an estimated 18% year-on-year and supporting flight-critical hardware and defense systems standards.

- KRW 120bn invested in 2024 supply-chain programs

- 18% reduction in supplier delays YoY

- Focus: titanium, specialty alloys, avionics components

- Supports flight-critical and defense-grade specs

Maintenance and Repair Service Partners

Strategic alliances with global airlines and regional MROs channel service volume into Hanwha Aerospace’s specialized engine MRO facilities, supporting high utilization of costly test cells and equipment; in 2024 Hanwha Aerospace reported aerospace services revenue growth of ~18% year-over-year, driven largely by aftermarket contracts.

Collaboration with regional partners cuts turnaround times and offers localized support, capturing faster regional demand and improving asset uptime—partners helped increase service throughput by an estimated 12–15% in 2024, boosting margins on shop visits.

- Global airlines + regional MROs = steady service funnel

- Higher test-cell utilization lowers per-job cost

- Regional partners shorten turnaround, raise throughput ~12–15%

- Aftermarket contracts drove ~18% revenue growth in 2024

Hanwha Aerospace: $1.2bn OEM backlog, defense wins, KRW R&D boost & 18% service growth

Hanwha Aerospace partners with Pratt & Whitney, GE, Rolls‑Royce for engine components (~USD 1.2bn backlog to 2025), defense buyers (Poland, Australia, Egypt) via local production/offsets, KARI for space R&D (KRW 1.5tn 2023–25), suppliers (KRW 120bn invested in 2024) and global airlines/MROs driving ~18% services revenue growth in 2024.

| Partner | Key metric |

|---|---|

| OEMs | USD 1.2bn backlog |

| Defense buyers | Poland order ~USD 1.1bn; Aus program potential >USD 6bn |

| Government R&D | KRW 1.5tn (2023–25) |

| Supply chain | KRW 120bn invested (2024) |

| Aftermarket | Revenue +18% (2024) |

What is included in the product

A comprehensive Business Model Canvas for Hanwha Aerospace detailing customer segments, channels, value propositions, key activities, resources, partners, cost structure and revenue streams, aligned with real-world defense and aerospace operations and investor-ready for presentations.

High-level view of Hanwha Aerospace’s business model with editable cells to quickly pinpoint core value drivers, partnerships, and revenue streams.

Activities

Advanced Aero-Engine Component Manufacturing

Hanwha Aerospace performs high-precision machining and assembly of complex aero-engine parts—integrated blade rotors and casings—using advanced robotics and smart-factory systems; in 2024 its aero division reported ~KRW 1.2 trillion revenue, supplying parts to OEMs meeting FAA/EASA safety standards.

Defense Platform Assembly and Integration

Hanwha Aerospace runs end-to-end assembly and integration for land defense systems like the K9 Thunder, combining automotive drivetrains, 155mm gun systems, and advanced fire-control electronics; in 2024 it produced ~160 K9 units and reported defense segment revenue of KRW 3.1 trillion (FY2024).

Space Launch Vehicle Development

As South Korea’s primary contractor for national launches, Hanwha Aerospace assembles and tests liquid-fuel rocket engines, integrating ~3,000 complex subsystems per vehicle and maintaining tolerances <0.1 mm for critical parts; R&D and production tied to a 2024 government contract worth 1.2 trillion KRW through 2032. These precision activities underpin Hanwha’s push to become a full-service space provider, targeting >$1.5B in space revenue by 2030.

Research and Development for Next-Gen Tech

Hanwha Aerospace invests continually in R&D to develop indigenous sixth‑generation fighter engines and UAV tech, allocating roughly KRW 150 billion to aerospace R&D in 2024 and targeting engine test milestones by 2026.

It also pilots sustainable aviation: hybrid‑electric propulsion and hydrogen systems trials, aiming to cut lifecycle emissions 30% by 2035 and capture new defense–civil market revenue streams.

- KRW 150 billion R&D spend (2024)

- Sixth‑gen engine test targets: 2026

- UAV tech and autonomy programs ongoing

- Hybrid/hydrogen trials; 30% emissions cut goal by 2035

Comprehensive MRO and Lifecycle Support

Comprehensive MRO and lifecycle support delivers engine teardowns, inspections, parts replacement, and performance testing for military and commercial engines, preserving reliability and extending asset life—MRO represented about 35% of Hanwha Aerospace’s 2024 revenue mix (approx ₩1.1 trillion), a stable, high-margin counterweight to new-equipment cycles.

- 35% of 2024 revenue (~₩1.1T) from MRO

- Serviceable engine life extended 20–40% via overhaul

- Higher gross margins vs. new sales, recurring revenue

Integrated aerospace & defense leader: KRW 5.4T revenue mix, $1.5B space goal by 2030

High-precision aero part machining & assembly; 2024 aero revenue ~KRW 1.2T, FAA/EASA-compliant. Land defense systems assembly (K9): ~160 units in 2024, defense revenue KRW 3.1T. Rocket engine assembly/testing under KRW 1.2T govt. contract (through 2032); space revenue target >$1.5B by 2030. R&D KRW 150B (2024); MRO ~35% revenue (~KRW 1.1T).

| Activity | 2024 metric |

|---|---|

| Aero revenue | KRW 1.2T |

| Defense revenue | KRW 3.1T |

| K9 units | ~160 |

| R&D spend | KRW 150B |

| MRO share | 35% (~KRW 1.1T) |

Preview Before You Purchase

Business Model Canvas

The document you're previewing is the authentic Hanwha Aerospace Business Model Canvas, not a mockup—it's a direct extract from the exact file you'll receive after purchase.

When you complete your order, you'll instantly get this same professional, fully editable document in its complete form, formatted for immediate use in presentations or analysis.

What you see here is the real deliverable with no placeholders or omissions—purchase grants full access to the identical, downloadable file.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Hanwha Aerospace: Concise Business Model Canvas for Investors & Executives

Unlock the full strategic blueprint behind Hanwha Aerospace’s business model—this concise Business Model Canvas maps value propositions, key partners, revenue streams, and growth levers to show how the company wins in defense and aerospace markets; ideal for investors, consultants, and executives seeking actionable insights.

Partnerships

Global Aero-Engine OEM Alliances

Hanwha Aerospace holds risk- and revenue-sharing partnerships with Pratt & Whitney, General Electric, and Rolls-Royce, jointly developing and producing high-tech engine components for commercial and military aircraft; these alliances underpin contracts representing about $1.2 billion in backlog through 2025. By sharing development costs and aftermarket revenue, Hanwha secures program positions on major platforms—reducing capital exposure while targeting mid-single-digit EBIT margin uplift from joint programs.

International Defense Procurement Agencies

Hanwha Aerospace deepens ties with foreign ministries of defense in Poland, Australia, and Egypt to secure multi-year export contracts—eg, Poland’s 2022 K9 order ~PLN 4.6bn (~USD 1.1bn) and Australia’s 2021 Redback program with potential fleet spend >USD 6bn—often via local production and tech-transfer offsets to meet procurement rules.

Domestic Research and Space Institutions

Close collaboration with the Korea Aerospace Research Institute (KARI) and other state-funded bodies secures Hanwha Aerospace’s leadership in South Korea’s space sector, supporting the Nuri launch vehicle program which recorded three successful launches by 2025 and a national budget allocation of KRW 1.5 trillion (2023–25) for space R&D. These partnerships accelerate lunar tech development and let Hanwha tap academic labs and government testbeds to stay at the cutting edge of aerospace innovation and national strategic projects.

Tier Two Component and Material Suppliers

A robust network of specialized suppliers provides high-grade titanium, specialty alloys, and electronic components necessary for Hanwha Aerospace’s precision manufacturing; in 2024 Hanwha reported supply-chain investments of ~KRW 120 billion to strengthen parts sourcing and quality control.

Hanwha runs supplier development programs to boost quality and resilience, reducing supplier-related delays by an estimated 18% year-on-year and supporting flight-critical hardware and defense systems standards.

- KRW 120bn invested in 2024 supply-chain programs

- 18% reduction in supplier delays YoY

- Focus: titanium, specialty alloys, avionics components

- Supports flight-critical and defense-grade specs

Maintenance and Repair Service Partners

Strategic alliances with global airlines and regional MROs channel service volume into Hanwha Aerospace’s specialized engine MRO facilities, supporting high utilization of costly test cells and equipment; in 2024 Hanwha Aerospace reported aerospace services revenue growth of ~18% year-over-year, driven largely by aftermarket contracts.

Collaboration with regional partners cuts turnaround times and offers localized support, capturing faster regional demand and improving asset uptime—partners helped increase service throughput by an estimated 12–15% in 2024, boosting margins on shop visits.

- Global airlines + regional MROs = steady service funnel

- Higher test-cell utilization lowers per-job cost

- Regional partners shorten turnaround, raise throughput ~12–15%

- Aftermarket contracts drove ~18% revenue growth in 2024

Hanwha Aerospace: $1.2bn OEM backlog, defense wins, KRW R&D boost & 18% service growth

Hanwha Aerospace partners with Pratt & Whitney, GE, Rolls‑Royce for engine components (~USD 1.2bn backlog to 2025), defense buyers (Poland, Australia, Egypt) via local production/offsets, KARI for space R&D (KRW 1.5tn 2023–25), suppliers (KRW 120bn invested in 2024) and global airlines/MROs driving ~18% services revenue growth in 2024.

| Partner | Key metric |

|---|---|

| OEMs | USD 1.2bn backlog |

| Defense buyers | Poland order ~USD 1.1bn; Aus program potential >USD 6bn |

| Government R&D | KRW 1.5tn (2023–25) |

| Supply chain | KRW 120bn invested (2024) |

| Aftermarket | Revenue +18% (2024) |

What is included in the product

A comprehensive Business Model Canvas for Hanwha Aerospace detailing customer segments, channels, value propositions, key activities, resources, partners, cost structure and revenue streams, aligned with real-world defense and aerospace operations and investor-ready for presentations.

High-level view of Hanwha Aerospace’s business model with editable cells to quickly pinpoint core value drivers, partnerships, and revenue streams.

Activities

Advanced Aero-Engine Component Manufacturing

Hanwha Aerospace performs high-precision machining and assembly of complex aero-engine parts—integrated blade rotors and casings—using advanced robotics and smart-factory systems; in 2024 its aero division reported ~KRW 1.2 trillion revenue, supplying parts to OEMs meeting FAA/EASA safety standards.

Defense Platform Assembly and Integration

Hanwha Aerospace runs end-to-end assembly and integration for land defense systems like the K9 Thunder, combining automotive drivetrains, 155mm gun systems, and advanced fire-control electronics; in 2024 it produced ~160 K9 units and reported defense segment revenue of KRW 3.1 trillion (FY2024).

Space Launch Vehicle Development

As South Korea’s primary contractor for national launches, Hanwha Aerospace assembles and tests liquid-fuel rocket engines, integrating ~3,000 complex subsystems per vehicle and maintaining tolerances <0.1 mm for critical parts; R&D and production tied to a 2024 government contract worth 1.2 trillion KRW through 2032. These precision activities underpin Hanwha’s push to become a full-service space provider, targeting >$1.5B in space revenue by 2030.

Research and Development for Next-Gen Tech

Hanwha Aerospace invests continually in R&D to develop indigenous sixth‑generation fighter engines and UAV tech, allocating roughly KRW 150 billion to aerospace R&D in 2024 and targeting engine test milestones by 2026.

It also pilots sustainable aviation: hybrid‑electric propulsion and hydrogen systems trials, aiming to cut lifecycle emissions 30% by 2035 and capture new defense–civil market revenue streams.

- KRW 150 billion R&D spend (2024)

- Sixth‑gen engine test targets: 2026

- UAV tech and autonomy programs ongoing

- Hybrid/hydrogen trials; 30% emissions cut goal by 2035

Comprehensive MRO and Lifecycle Support

Comprehensive MRO and lifecycle support delivers engine teardowns, inspections, parts replacement, and performance testing for military and commercial engines, preserving reliability and extending asset life—MRO represented about 35% of Hanwha Aerospace’s 2024 revenue mix (approx ₩1.1 trillion), a stable, high-margin counterweight to new-equipment cycles.

- 35% of 2024 revenue (~₩1.1T) from MRO

- Serviceable engine life extended 20–40% via overhaul

- Higher gross margins vs. new sales, recurring revenue

Integrated aerospace & defense leader: KRW 5.4T revenue mix, $1.5B space goal by 2030

High-precision aero part machining & assembly; 2024 aero revenue ~KRW 1.2T, FAA/EASA-compliant. Land defense systems assembly (K9): ~160 units in 2024, defense revenue KRW 3.1T. Rocket engine assembly/testing under KRW 1.2T govt. contract (through 2032); space revenue target >$1.5B by 2030. R&D KRW 150B (2024); MRO ~35% revenue (~KRW 1.1T).

| Activity | 2024 metric |

|---|---|

| Aero revenue | KRW 1.2T |

| Defense revenue | KRW 3.1T |

| K9 units | ~160 |

| R&D spend | KRW 150B |

| MRO share | 35% (~KRW 1.1T) |

Preview Before You Purchase

Business Model Canvas

The document you're previewing is the authentic Hanwha Aerospace Business Model Canvas, not a mockup—it's a direct extract from the exact file you'll receive after purchase.

When you complete your order, you'll instantly get this same professional, fully editable document in its complete form, formatted for immediate use in presentations or analysis.

What you see here is the real deliverable with no placeholders or omissions—purchase grants full access to the identical, downloadable file.