Hanwha Aerospace PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Our PESTLE Analysis of Hanwha Aerospace reveals how geopolitical tensions, defense spending trends, supply-chain pressures, technological advances in propulsion and avionics, and tightening environmental and export regulations will shape the firm's trajectory—insights critical for investors and strategists. Purchase the full report to access the complete, actionable breakdown and ready-to-use slides and models.

Political factors

Global Geopolitical Instability

The ongoing conflicts in Eastern Europe and the Middle East have driven a roughly 18% rise in global demand for rapid-response defense systems since 2022, benefiting Hanwha Aerospace’s artillery and armored-vehicle lines.

Hanwha has secured multi-year contracts worth over $3.2 billion with NATO members and Indo-Pacific allies to accelerate fleet modernization and delivery schedules.

This geopolitical climate supports a robust backlog extending through 2025, with company defense revenue up 24% year-on-year in 2024.

South Korean Government Export Initiatives

Seoul’s aggressive export push—defense exports targeted to reach $10.2bn by 2026—has translated into strong diplomatic backing for Hanwha Aerospace, including state-led trade missions and ministerial support.

Government-facilitated bilateral defense agreements have opened markets in Southeast Asia and the Middle East, where recent deals exceeded $1.5bn in 2024.

Hanwha is central to the strategy, benefitting from state-backed financing (Export-Import Bank credit lines) and promotional slots at international forums like DSEI and DIMDEX.

Strategic Defense Alliances

Long-term partnerships in Poland, Australia and Egypt have expanded into strategic industrial hubs for Hanwha Aerospace, with Poland deal values exceeding $1.5bn (2023–2025) and Australian offsets totaling about A$1.2bn; these involve local manufacturing and technology transfer that deepen political ties.

Local production lines and tech-sharing agreements secure Hanwha an operational footprint, supporting cumulative employment of several thousand in partner nations and reducing exposure to protectionist measures.

Inter-Korean Relations

The persistent security threat from North Korea drives steady domestic defense spending; South Korea's defense budget rose to 55.6 trillion KRW in 2025, sustaining procurement cycles and tech upgrades that favor Hanwha Aerospace.

As the primary supplier to the ROK military, Hanwha reported defense sales of about 2.3 trillion KRW in FY2024, providing predictable revenue from the Ministry of National Defense and funding R&D.

This domestic base finances advanced systems—aircraft, missile systems, avionics—that Hanwha increasingly exports, with defense exports reaching roughly 1.1 trillion KRW in 2024.

- Reliable domestic demand: rising defense budget 55.6T KRW (2025)

- Stable revenues: Hanwha defense sales ~2.3T KRW (FY2024)

- Export leverage: defense exports ~1.1T KRW (2024)

International Export Control Regimes

Navigating export control regimes like the Wassenaar Arrangement, US ITAR and EAR, and EU dual-use rules is critical as Hanwha Aerospace supplies military and space systems; noncompliance risks fines, export bans, and lost contracts—US ITAR violations have led to fines exceeding $1m in recent cases. In 2024 Hanwha reported defense segment revenue of KRW 1.2tn, so sanctions or tighter controls could materially affect procurement and sales.

- Compliance imperative: ITAR/EAR/Wassenaar adherence

- Financial exposure: fines and contract losses (>$1m precedent)

- Revenue risk: 2024 defense sales ~KRW 1.2tn

- Trade shifts: sanctions/trade deals directly affect sourcing and exportability

Hanwha surges on NATO/Indo‑Pacific wins—24% revenue jump amid 18% global defense demand rise

Geopolitical conflicts raised global rapid-response defense demand ~18% since 2022, supporting Hanwha’s multi-year NATO/Indo-Pacific contracts >$3.2bn and a 24% rise in defense revenue in 2024; Seoul’s export push targets $10.2bn by 2026, aiding state-backed financing and market access; domestic defense budget 55.6T KRW (2025) underpins KRW 2.3T FY2024 sales, while ITAR/EAR/Wassenaar compliance is critical to avoid >$1m fines and revenue disruption.

| Metric | Value |

|---|---|

| Global demand change (since 2022) | ~+18% |

| Multi-year contracts | >$3.2bn |

| Defense rev growth (2024) | +24% |

| SK defense budget (2025) | 55.6T KRW |

| Hanwha defense sales (FY2024) | ~2.3T KRW |

| Defense exports (2024) | ~1.1T KRW |

| Compliance risk precedent | Fines >$1m |

What is included in the product

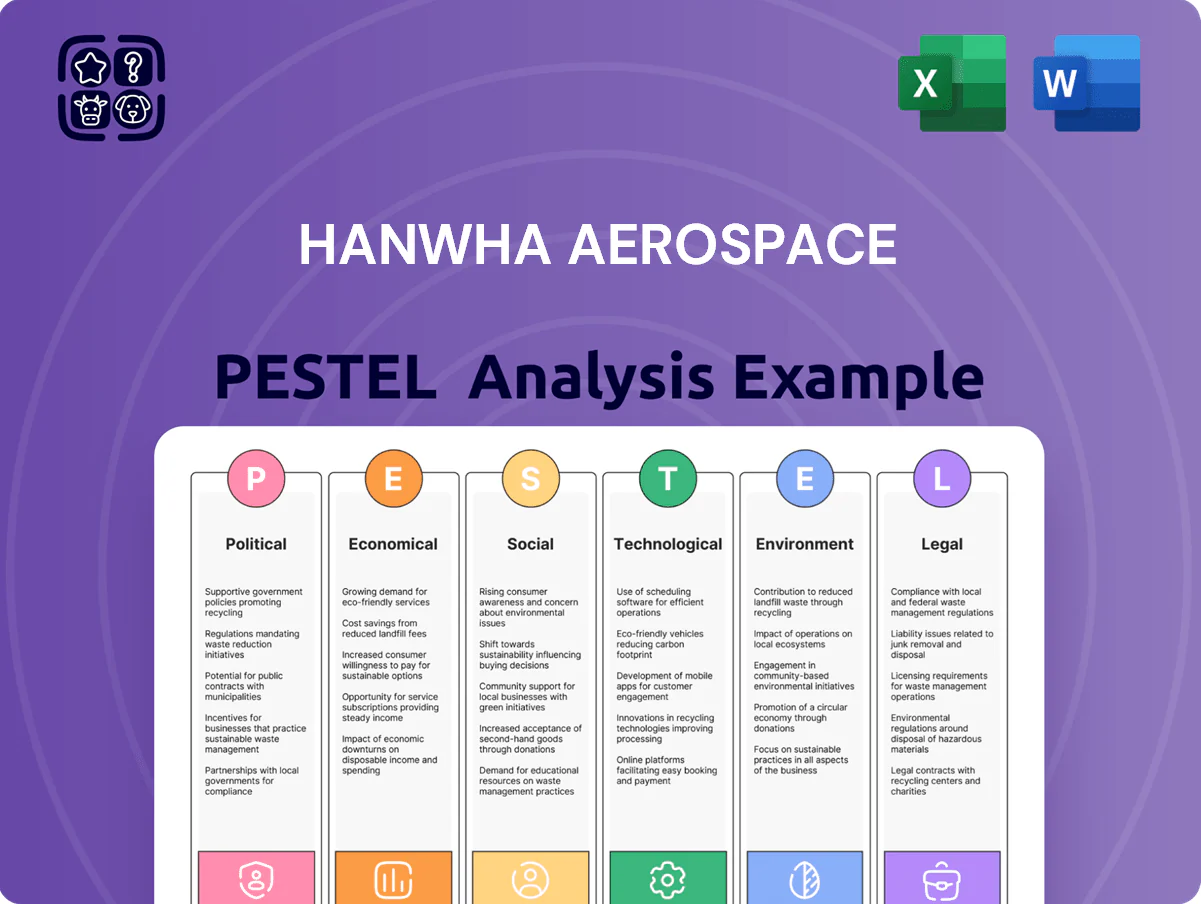

Explores how Political, Economic, Social, Technological, Environmental, and Legal factors uniquely affect Hanwha Aerospace, with data-backed trends and region-specific regulatory context to reveal industry threats and opportunities for executives and investors.

A concise, shareable Hanwha Aerospace PESTLE summary that’s visually segmented by category for quick interpretation, easily droppable into presentations and editable with notes for regional or business-line context to support planning, risk discussions, and client reports.

Economic factors

Rising Global Defense Budgets

Many nations pledged defense spending rises—NATO members aim for 2% of GDP and global military expenditure hit 2.4 trillion USD in 2023, up 6% year-on-year—directly boosting demand for Hanwha Aerospace’s offerings.

Increased allocations target modernization and replacement of Cold War–era platforms, reversing prior deprioritization of conventional warfare preparedness.

Hanwha’s diversified portfolio across land systems, aircraft engines, and munitions aligns with these budget shifts, supporting revenue growth as procurement cycles accelerate.

Currency Exchange Rate Volatility

As a major exporter, Hanwha Aerospace is highly sensitive to KRW volatility versus USD and EUR; a 10% KRW appreciation in 2023 would have reduced export competitiveness by a similar margin on dollar-priced contracts, and 2024 FX swings saw KRW move roughly 6–8% vs USD. Significant moves affect bid pricing in international tenders and repatriated earnings—Hanwha reported 2024 FX losses around KRW 45bn in disclosure. The firm uses forwards, options and natural hedges to stabilize results.

High Capital Intensity of R&D

Hanwha Aerospace faces high R&D capital intensity: the aerospace and defense sector typically allocates 8–12% of revenue to R&D, and Hanwha invested roughly KRW 350 billion in 2024 (~USD 265M) toward propulsion and space launch programs, pressuring short-term margins.

These outlays—targeting next-gen engines and small-satellite launchers—are critical to capture projected space market CAGR of ~12% through 2030 and defend long-term share in advanced aviation.

Supply Chain Inflation and Disruptions

- Titanium +8% YoY (2024)

- Electronic component premiums ~+12% vs pre-2020

- Increased capex for vertical integration and localized sourcing

- Long-term contract management critical to prevent margin erosion

Expansion of the MRO Market

The global MRO market reached about USD 88 billion in 2024 and is projected to grow to ~USD 115 billion by 2030, driven by a rising fleet of 40,000+ commercial aircraft and expanded defense platforms; this enlarges demand for engine and systems maintenance.

Hanwha is scaling MRO capacity—aiming for double-digit service revenue growth—to capture higher-margin, recurring income that cushions cyclical new-equipment dips.

Shifting industry mix toward services reduces revenue volatility and improves lifetime-value capture from installed bases, with services often yielding margins 5–10 percentage points above OEM new-builds.

- Global MRO ~USD 88bn (2024); ~USD 115bn by 2030

- Commercial fleet 40,000+ aircraft driving aftermarket

- Services margin premium ~5–10 pp vs new equipment

- Hanwha targeting double-digit MRO revenue growth

Defense spending hits $2.4T; Hanwha navigates FX, R&D and booming MRO opportunity

Defense spending rose to USD 2.4T in 2023 (+6% YoY); NATO 2% GDP pledges boost procurement. Hanwha faces KRW FX volatility (2024 ±6–8% vs USD; KRW 45bn FX loss 2024) and high R&D (KRW 350bn in 2024). Titanium +8% YoY; component premiums ~+12%. Global MRO USD 88bn (2024) → USD 115bn by 2030; Hanwha targets double-digit MRO growth.

| Metric | Value |

|---|---|

| Global defense spend 2023 | USD 2.4T |

| KRW FX move 2024 | ±6–8% vs USD |

| Hanwha R&D 2024 | KRW 350bn |

| Titanium price YoY 2024 | +8% |

| Global MRO 2024 | USD 88bn |

Full Version Awaits

Hanwha Aerospace PESTLE Analysis

The preview shown here is the exact Hanwha Aerospace PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions. The document includes political, economic, social, technological, legal, and environmental factors with concise insights and implications tailored to Hanwha Aerospace. No placeholders or teasers—this is the final file you’ll download immediately after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Our PESTLE Analysis of Hanwha Aerospace reveals how geopolitical tensions, defense spending trends, supply-chain pressures, technological advances in propulsion and avionics, and tightening environmental and export regulations will shape the firm's trajectory—insights critical for investors and strategists. Purchase the full report to access the complete, actionable breakdown and ready-to-use slides and models.

Political factors

Global Geopolitical Instability

The ongoing conflicts in Eastern Europe and the Middle East have driven a roughly 18% rise in global demand for rapid-response defense systems since 2022, benefiting Hanwha Aerospace’s artillery and armored-vehicle lines.

Hanwha has secured multi-year contracts worth over $3.2 billion with NATO members and Indo-Pacific allies to accelerate fleet modernization and delivery schedules.

This geopolitical climate supports a robust backlog extending through 2025, with company defense revenue up 24% year-on-year in 2024.

South Korean Government Export Initiatives

Seoul’s aggressive export push—defense exports targeted to reach $10.2bn by 2026—has translated into strong diplomatic backing for Hanwha Aerospace, including state-led trade missions and ministerial support.

Government-facilitated bilateral defense agreements have opened markets in Southeast Asia and the Middle East, where recent deals exceeded $1.5bn in 2024.

Hanwha is central to the strategy, benefitting from state-backed financing (Export-Import Bank credit lines) and promotional slots at international forums like DSEI and DIMDEX.

Strategic Defense Alliances

Long-term partnerships in Poland, Australia and Egypt have expanded into strategic industrial hubs for Hanwha Aerospace, with Poland deal values exceeding $1.5bn (2023–2025) and Australian offsets totaling about A$1.2bn; these involve local manufacturing and technology transfer that deepen political ties.

Local production lines and tech-sharing agreements secure Hanwha an operational footprint, supporting cumulative employment of several thousand in partner nations and reducing exposure to protectionist measures.

Inter-Korean Relations

The persistent security threat from North Korea drives steady domestic defense spending; South Korea's defense budget rose to 55.6 trillion KRW in 2025, sustaining procurement cycles and tech upgrades that favor Hanwha Aerospace.

As the primary supplier to the ROK military, Hanwha reported defense sales of about 2.3 trillion KRW in FY2024, providing predictable revenue from the Ministry of National Defense and funding R&D.

This domestic base finances advanced systems—aircraft, missile systems, avionics—that Hanwha increasingly exports, with defense exports reaching roughly 1.1 trillion KRW in 2024.

- Reliable domestic demand: rising defense budget 55.6T KRW (2025)

- Stable revenues: Hanwha defense sales ~2.3T KRW (FY2024)

- Export leverage: defense exports ~1.1T KRW (2024)

International Export Control Regimes

Navigating export control regimes like the Wassenaar Arrangement, US ITAR and EAR, and EU dual-use rules is critical as Hanwha Aerospace supplies military and space systems; noncompliance risks fines, export bans, and lost contracts—US ITAR violations have led to fines exceeding $1m in recent cases. In 2024 Hanwha reported defense segment revenue of KRW 1.2tn, so sanctions or tighter controls could materially affect procurement and sales.

- Compliance imperative: ITAR/EAR/Wassenaar adherence

- Financial exposure: fines and contract losses (>$1m precedent)

- Revenue risk: 2024 defense sales ~KRW 1.2tn

- Trade shifts: sanctions/trade deals directly affect sourcing and exportability

Hanwha surges on NATO/Indo‑Pacific wins—24% revenue jump amid 18% global defense demand rise

Geopolitical conflicts raised global rapid-response defense demand ~18% since 2022, supporting Hanwha’s multi-year NATO/Indo-Pacific contracts >$3.2bn and a 24% rise in defense revenue in 2024; Seoul’s export push targets $10.2bn by 2026, aiding state-backed financing and market access; domestic defense budget 55.6T KRW (2025) underpins KRW 2.3T FY2024 sales, while ITAR/EAR/Wassenaar compliance is critical to avoid >$1m fines and revenue disruption.

| Metric | Value |

|---|---|

| Global demand change (since 2022) | ~+18% |

| Multi-year contracts | >$3.2bn |

| Defense rev growth (2024) | +24% |

| SK defense budget (2025) | 55.6T KRW |

| Hanwha defense sales (FY2024) | ~2.3T KRW |

| Defense exports (2024) | ~1.1T KRW |

| Compliance risk precedent | Fines >$1m |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal factors uniquely affect Hanwha Aerospace, with data-backed trends and region-specific regulatory context to reveal industry threats and opportunities for executives and investors.

A concise, shareable Hanwha Aerospace PESTLE summary that’s visually segmented by category for quick interpretation, easily droppable into presentations and editable with notes for regional or business-line context to support planning, risk discussions, and client reports.

Economic factors

Rising Global Defense Budgets

Many nations pledged defense spending rises—NATO members aim for 2% of GDP and global military expenditure hit 2.4 trillion USD in 2023, up 6% year-on-year—directly boosting demand for Hanwha Aerospace’s offerings.

Increased allocations target modernization and replacement of Cold War–era platforms, reversing prior deprioritization of conventional warfare preparedness.

Hanwha’s diversified portfolio across land systems, aircraft engines, and munitions aligns with these budget shifts, supporting revenue growth as procurement cycles accelerate.

Currency Exchange Rate Volatility

As a major exporter, Hanwha Aerospace is highly sensitive to KRW volatility versus USD and EUR; a 10% KRW appreciation in 2023 would have reduced export competitiveness by a similar margin on dollar-priced contracts, and 2024 FX swings saw KRW move roughly 6–8% vs USD. Significant moves affect bid pricing in international tenders and repatriated earnings—Hanwha reported 2024 FX losses around KRW 45bn in disclosure. The firm uses forwards, options and natural hedges to stabilize results.

High Capital Intensity of R&D

Hanwha Aerospace faces high R&D capital intensity: the aerospace and defense sector typically allocates 8–12% of revenue to R&D, and Hanwha invested roughly KRW 350 billion in 2024 (~USD 265M) toward propulsion and space launch programs, pressuring short-term margins.

These outlays—targeting next-gen engines and small-satellite launchers—are critical to capture projected space market CAGR of ~12% through 2030 and defend long-term share in advanced aviation.

Supply Chain Inflation and Disruptions

- Titanium +8% YoY (2024)

- Electronic component premiums ~+12% vs pre-2020

- Increased capex for vertical integration and localized sourcing

- Long-term contract management critical to prevent margin erosion

Expansion of the MRO Market

The global MRO market reached about USD 88 billion in 2024 and is projected to grow to ~USD 115 billion by 2030, driven by a rising fleet of 40,000+ commercial aircraft and expanded defense platforms; this enlarges demand for engine and systems maintenance.

Hanwha is scaling MRO capacity—aiming for double-digit service revenue growth—to capture higher-margin, recurring income that cushions cyclical new-equipment dips.

Shifting industry mix toward services reduces revenue volatility and improves lifetime-value capture from installed bases, with services often yielding margins 5–10 percentage points above OEM new-builds.

- Global MRO ~USD 88bn (2024); ~USD 115bn by 2030

- Commercial fleet 40,000+ aircraft driving aftermarket

- Services margin premium ~5–10 pp vs new equipment

- Hanwha targeting double-digit MRO revenue growth

Defense spending hits $2.4T; Hanwha navigates FX, R&D and booming MRO opportunity

Defense spending rose to USD 2.4T in 2023 (+6% YoY); NATO 2% GDP pledges boost procurement. Hanwha faces KRW FX volatility (2024 ±6–8% vs USD; KRW 45bn FX loss 2024) and high R&D (KRW 350bn in 2024). Titanium +8% YoY; component premiums ~+12%. Global MRO USD 88bn (2024) → USD 115bn by 2030; Hanwha targets double-digit MRO growth.

| Metric | Value |

|---|---|

| Global defense spend 2023 | USD 2.4T |

| KRW FX move 2024 | ±6–8% vs USD |

| Hanwha R&D 2024 | KRW 350bn |

| Titanium price YoY 2024 | +8% |

| Global MRO 2024 | USD 88bn |

Full Version Awaits

Hanwha Aerospace PESTLE Analysis

The preview shown here is the exact Hanwha Aerospace PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions. The document includes political, economic, social, technological, legal, and environmental factors with concise insights and implications tailored to Hanwha Aerospace. No placeholders or teasers—this is the final file you’ll download immediately after payment.