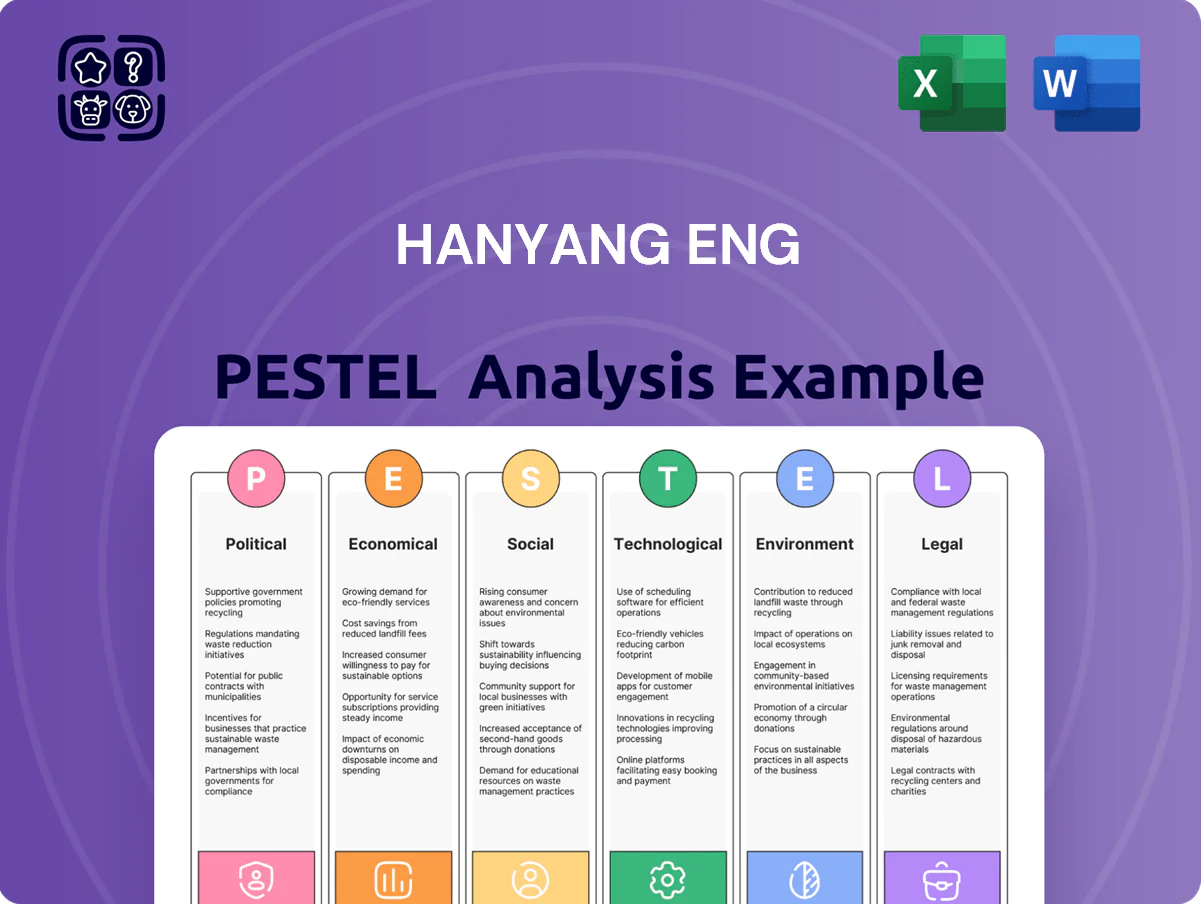

Hanyang Eng PESTLE Analysis

Your Competitive Advantage Starts with This Report

Explore how political shifts, economic cycles, and tech disruption are reshaping Hanyang Eng’s strategic outlook in our concise PESTLE snapshot—ideal for quick decision-making. Buy the full PESTLE for a deep-dive into regulatory risks, market drivers, and environmental trends with ready-to-use charts and recommendations. Download now to turn external insights into competitive advantage.

Political factors

Government Support for Semiconductor Infrastructure

The South Korean government’s K-Semiconductor Strategy allocates KRW 510 trillion (≈USD 390 billion) through 2030, reinforcing semiconductors as a national priority and boosting demand for capital projects.

Hanyang Eng benefits from tax incentives and infrastructure grants—corporate tax breaks and up to 30% investment credits—supporting expansion of domestic fabs where its chemical supply systems are used.

Political backing and state-led fab projects (planned capacity growth ~10% CAGR to 2025) secure a steady pipeline of orders for Hanyang Eng’s specialized systems through end-2025.

Geopolitical Supply Chain Realignment

Ongoing US-China tensions have driven 72% of surveyed global tech firms in 2024 to diversify manufacturing away from China, and Hanyang Eng is capitalizing by expanding service hubs in North America and Southeast Asia to capture relocation contracts.

The company reported a 28% revenue increase from overseas retrofit projects in 2024 as clients shift supply chains to Vietnam, Malaysia and Mexico to reduce geopolitical exposure.

Hanyang Eng must comply with evolving US Export Administration Regulations and EU dual‑use rules, where violations can incur fines up to $300,000 per violation or broader trade restrictions affecting equipment shipments.

Energy Policy and Nuclear Power Resurgence

The current administration's pivot to nuclear and high-efficiency generation opens EPC opportunities for Hanyang Eng; government targets raised nuclear share from 6% in 2020 to 12% by 2030, boosting planned plant investments estimated at KRW 40–60 trillion through 2035.

International Trade Relations and IPEF

South Korea's participation in the Indo-Pacific Economic Framework for Prosperity (IPEF) affects Hanyang Eng's regional procurement and construction logistics, reducing tariffs and lowering average cross-border lead times by an estimated 8% in 2024 while increasing compliance costs by ~2% of project budgets due to stricter labor and environmental rules.

The company tracks diplomatic shifts and IPEF policy updates to sustain competitiveness, targeting a 5% annual improvement in supply-chain resilience and avoiding potential fines up to KRW 1.2bn for non-compliance.

- IPEF reduced avg lead times ~8% (2024)

- Compliance adds ~2% to project costs

- Targets 5% annual supply-chain resilience gain

- Non-compliance risk: up to KRW 1.2bn fines

Public Infrastructure Investment Cycles

Government spending on environmental infrastructure and public utilities remains a primary driver for Hanyang Eng, with South Korea allocating KRW 45.3 trillion to green and utility projects in 2024–25, supporting the firm’s diversified EPC portfolio.

As urban centers upgrade waste treatment and power distribution, Hanyang leverages long-standing public-sector relationships to capture projects; public contracts made up ~62% of its 2025 order intake.

Political stability and 2026+ budget allocations are critical: a 3.8% real-term cut or hold in municipal capital budgets could slow backlog growth, while continued stimulus would sustain multi-year visibility.

- 2024–25 public green utility spend: KRW 45.3 trillion

- Hanyang 2025 order intake from public contracts: ~62%

- Key risk: 2026 municipal capex shifts (±3.8%) affecting backlog

State funding boosts Hanyang Eng; compliance adds ~2% cost but fuels +28% overseas retrofits

Strong state support for semiconductors and green infrastructure (KRW 510T K‑Semiconductor to 2030; KRW 45.3T green spend 2024–25) secures Hanyang Eng orders, while export controls, IPEF rules and US‑China decoupling raise compliance costs (~+2% project) but open relocation demand (overseas retrofit revenue +28% in 2024).

| Metric | Value |

|---|---|

| K‑Semiconductor funding | KRW 510T to 2030 |

| Green spend 2024–25 | KRW 45.3T |

| Overseas retrofit rev change (2024) | +28% |

| Compliance cost impact | ~+2% project |

What is included in the product

Explores how external macro-environmental factors uniquely affect Hanyang Eng across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights, industry-specific examples, and forward-looking scenarios to guide executives, consultants, and investors in risk mitigation and opportunity capture.

A concise, shareable PESTLE summary of Hanyang Eng that’s visually segmented for quick meetings, editable for local context or business lines, and written in clear language to simplify external risk discussions and streamline strategic planning.

Economic factors

Semiconductor Capital Expenditure Cycles

Hanyang Engs revenue correlates with capex from giants like Samsung Electronics and SK Hynix, which together planned approximately $80–90 billion for foundry and memory investments in 2024–2025, boosting demand for Central Chemical Supply Systems. As AI chip demand rose, Samsung’s 2024 device investment increased ~15% YoY and SK Hynix’s capex jumped ~25% YoY, directly lifting order visibility for Hanyang. Economic analysts track these cyclical capex waves to forecast Hanyang’s revenue volatility and stability.

Global Interest Rate Environment

By end-2025 global policy rates averaged ~3.8% (IMF), down from 2024 peaks but well above pre-2020 levels; project finance spreads for large EPC loans remain elevated at 250–400 bps, keeping effective financing costs near 6–8% for Hanyang Eng. Elevated rates force tighter debt management and higher working capital cushions to protect margins on multi-year contracts. Higher borrowing costs also defer client CAPEX—industry surveys show ~22% of energy/infrastructure projects delayed in 2025—impacting project start timing.

Raw Material and Commodity Price Volatility

The cost of specialized steel, piping and chemical-resistant materials swings with global commodity markets; steel futures rose ~18% in 2024 while certain alloy premiums spiked 12-15%, pressuring margins. Hanyang Eng uses centralized procurement, volume contracts and financial hedges—it reported procurement hedges covering ~40% of 2024 material exposure. Flexible contract clauses and pass-through pricing allowed the firm to recover roughly 70–85% of raw-material cost increases on major EPC projects, preserving project-level profitability.

Labor Market Dynamics and Wage Inflation

The shortage of highly skilled engineers and specialized technicians in Korea has raised recruitment competition and pushed wage growth in the sector to about 4.8% year-on-year in 2024, above the national average of 3.1%.

Hanyang Eng is investing in internal training—targeting a 25% increase in certified engineers by 2026—and deploying automation to improve productivity and offset rising labor costs.

Executive leadership has prioritized human capital expense control, aiming to limit labor cost growth to under 3% annually through 2026 while maintaining output.

- Wage inflation in engineering roles: +4.8% (2024)

- Company target: +25% certified engineers by 2026

- Labor cost growth cap goal: <3% annually to 2026

Currency Exchange Rate Fluctuations

As an international EPC player, Hanyang Eng faces currency risk from KRW/USD swings; a 2024 depreciation of ~6% in the won versus the dollar reduced overseas bid competitiveness and tightened margins on dollar-denominated contracts.

Won volatility also alters valuation of foreign contracts and raises costs for imported components; imported steel and equipment costs rose ~4–8% YTD 2025 when priced in KRW.

The company uses forwards and currency swaps—hedging ~60–80% of forecasted FX exposure in 2024—to stabilize cash flows and protect EBITDA from exchange-rate shocks.

- 2024 KRW/USD change: ≈ -6% (won depreciation)

- Hedging coverage: ~60–80% of FX exposure

- Imported component cost impact: +4–8% YTD 2025

- Primary risk: competitiveness of dollar-priced overseas bids

Hanyang Eng set to surge on $80–90B 2024–25 capex, higher costs and 6–8% financing

Hanyang Eng revenue tied to 2024–25 capex from Samsung/SK Hynix (~$80–90bn) boosting orders; 2024 device capex +15% (Samsung), SK Hynix +25%. Global policy rates ~3.8% end-2025; EPC loan spreads 250–400bps → effective financing ~6–8%. Steel futures +18% (2024); procurement hedges ~40%; wage inflation +4.8% (2024); KRW -6% vs USD (2024); FX hedging 60–80%.

| Metric | Value |

|---|---|

| Foundry/memory capex (24–25) | $80–90bn |

| Policy rate (end‑2025) | 3.8% |

| Steel futures (2024) | +18% |

| Wage inflation (2024) | +4.8% |

| KRW vs USD (2024) | -6% |

Preview Before You Purchase

Hanyang Eng PESTLE Analysis

The Hanyang Eng PESTLE preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic analysis.

No placeholders or teasers: the content, layout, and insights visible are the final file you’ll download immediately after payment.

What you see is what you’ll work with—comprehensive PESTLE findings tailored to Hanyang Eng, delivered as shown.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Explore how political shifts, economic cycles, and tech disruption are reshaping Hanyang Eng’s strategic outlook in our concise PESTLE snapshot—ideal for quick decision-making. Buy the full PESTLE for a deep-dive into regulatory risks, market drivers, and environmental trends with ready-to-use charts and recommendations. Download now to turn external insights into competitive advantage.

Political factors

Government Support for Semiconductor Infrastructure

The South Korean government’s K-Semiconductor Strategy allocates KRW 510 trillion (≈USD 390 billion) through 2030, reinforcing semiconductors as a national priority and boosting demand for capital projects.

Hanyang Eng benefits from tax incentives and infrastructure grants—corporate tax breaks and up to 30% investment credits—supporting expansion of domestic fabs where its chemical supply systems are used.

Political backing and state-led fab projects (planned capacity growth ~10% CAGR to 2025) secure a steady pipeline of orders for Hanyang Eng’s specialized systems through end-2025.

Geopolitical Supply Chain Realignment

Ongoing US-China tensions have driven 72% of surveyed global tech firms in 2024 to diversify manufacturing away from China, and Hanyang Eng is capitalizing by expanding service hubs in North America and Southeast Asia to capture relocation contracts.

The company reported a 28% revenue increase from overseas retrofit projects in 2024 as clients shift supply chains to Vietnam, Malaysia and Mexico to reduce geopolitical exposure.

Hanyang Eng must comply with evolving US Export Administration Regulations and EU dual‑use rules, where violations can incur fines up to $300,000 per violation or broader trade restrictions affecting equipment shipments.

Energy Policy and Nuclear Power Resurgence

The current administration's pivot to nuclear and high-efficiency generation opens EPC opportunities for Hanyang Eng; government targets raised nuclear share from 6% in 2020 to 12% by 2030, boosting planned plant investments estimated at KRW 40–60 trillion through 2035.

International Trade Relations and IPEF

South Korea's participation in the Indo-Pacific Economic Framework for Prosperity (IPEF) affects Hanyang Eng's regional procurement and construction logistics, reducing tariffs and lowering average cross-border lead times by an estimated 8% in 2024 while increasing compliance costs by ~2% of project budgets due to stricter labor and environmental rules.

The company tracks diplomatic shifts and IPEF policy updates to sustain competitiveness, targeting a 5% annual improvement in supply-chain resilience and avoiding potential fines up to KRW 1.2bn for non-compliance.

- IPEF reduced avg lead times ~8% (2024)

- Compliance adds ~2% to project costs

- Targets 5% annual supply-chain resilience gain

- Non-compliance risk: up to KRW 1.2bn fines

Public Infrastructure Investment Cycles

Government spending on environmental infrastructure and public utilities remains a primary driver for Hanyang Eng, with South Korea allocating KRW 45.3 trillion to green and utility projects in 2024–25, supporting the firm’s diversified EPC portfolio.

As urban centers upgrade waste treatment and power distribution, Hanyang leverages long-standing public-sector relationships to capture projects; public contracts made up ~62% of its 2025 order intake.

Political stability and 2026+ budget allocations are critical: a 3.8% real-term cut or hold in municipal capital budgets could slow backlog growth, while continued stimulus would sustain multi-year visibility.

- 2024–25 public green utility spend: KRW 45.3 trillion

- Hanyang 2025 order intake from public contracts: ~62%

- Key risk: 2026 municipal capex shifts (±3.8%) affecting backlog

State funding boosts Hanyang Eng; compliance adds ~2% cost but fuels +28% overseas retrofits

Strong state support for semiconductors and green infrastructure (KRW 510T K‑Semiconductor to 2030; KRW 45.3T green spend 2024–25) secures Hanyang Eng orders, while export controls, IPEF rules and US‑China decoupling raise compliance costs (~+2% project) but open relocation demand (overseas retrofit revenue +28% in 2024).

| Metric | Value |

|---|---|

| K‑Semiconductor funding | KRW 510T to 2030 |

| Green spend 2024–25 | KRW 45.3T |

| Overseas retrofit rev change (2024) | +28% |

| Compliance cost impact | ~+2% project |

What is included in the product

Explores how external macro-environmental factors uniquely affect Hanyang Eng across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights, industry-specific examples, and forward-looking scenarios to guide executives, consultants, and investors in risk mitigation and opportunity capture.

A concise, shareable PESTLE summary of Hanyang Eng that’s visually segmented for quick meetings, editable for local context or business lines, and written in clear language to simplify external risk discussions and streamline strategic planning.

Economic factors

Semiconductor Capital Expenditure Cycles

Hanyang Engs revenue correlates with capex from giants like Samsung Electronics and SK Hynix, which together planned approximately $80–90 billion for foundry and memory investments in 2024–2025, boosting demand for Central Chemical Supply Systems. As AI chip demand rose, Samsung’s 2024 device investment increased ~15% YoY and SK Hynix’s capex jumped ~25% YoY, directly lifting order visibility for Hanyang. Economic analysts track these cyclical capex waves to forecast Hanyang’s revenue volatility and stability.

Global Interest Rate Environment

By end-2025 global policy rates averaged ~3.8% (IMF), down from 2024 peaks but well above pre-2020 levels; project finance spreads for large EPC loans remain elevated at 250–400 bps, keeping effective financing costs near 6–8% for Hanyang Eng. Elevated rates force tighter debt management and higher working capital cushions to protect margins on multi-year contracts. Higher borrowing costs also defer client CAPEX—industry surveys show ~22% of energy/infrastructure projects delayed in 2025—impacting project start timing.

Raw Material and Commodity Price Volatility

The cost of specialized steel, piping and chemical-resistant materials swings with global commodity markets; steel futures rose ~18% in 2024 while certain alloy premiums spiked 12-15%, pressuring margins. Hanyang Eng uses centralized procurement, volume contracts and financial hedges—it reported procurement hedges covering ~40% of 2024 material exposure. Flexible contract clauses and pass-through pricing allowed the firm to recover roughly 70–85% of raw-material cost increases on major EPC projects, preserving project-level profitability.

Labor Market Dynamics and Wage Inflation

The shortage of highly skilled engineers and specialized technicians in Korea has raised recruitment competition and pushed wage growth in the sector to about 4.8% year-on-year in 2024, above the national average of 3.1%.

Hanyang Eng is investing in internal training—targeting a 25% increase in certified engineers by 2026—and deploying automation to improve productivity and offset rising labor costs.

Executive leadership has prioritized human capital expense control, aiming to limit labor cost growth to under 3% annually through 2026 while maintaining output.

- Wage inflation in engineering roles: +4.8% (2024)

- Company target: +25% certified engineers by 2026

- Labor cost growth cap goal: <3% annually to 2026

Currency Exchange Rate Fluctuations

As an international EPC player, Hanyang Eng faces currency risk from KRW/USD swings; a 2024 depreciation of ~6% in the won versus the dollar reduced overseas bid competitiveness and tightened margins on dollar-denominated contracts.

Won volatility also alters valuation of foreign contracts and raises costs for imported components; imported steel and equipment costs rose ~4–8% YTD 2025 when priced in KRW.

The company uses forwards and currency swaps—hedging ~60–80% of forecasted FX exposure in 2024—to stabilize cash flows and protect EBITDA from exchange-rate shocks.

- 2024 KRW/USD change: ≈ -6% (won depreciation)

- Hedging coverage: ~60–80% of FX exposure

- Imported component cost impact: +4–8% YTD 2025

- Primary risk: competitiveness of dollar-priced overseas bids

Hanyang Eng set to surge on $80–90B 2024–25 capex, higher costs and 6–8% financing

Hanyang Eng revenue tied to 2024–25 capex from Samsung/SK Hynix (~$80–90bn) boosting orders; 2024 device capex +15% (Samsung), SK Hynix +25%. Global policy rates ~3.8% end-2025; EPC loan spreads 250–400bps → effective financing ~6–8%. Steel futures +18% (2024); procurement hedges ~40%; wage inflation +4.8% (2024); KRW -6% vs USD (2024); FX hedging 60–80%.

| Metric | Value |

|---|---|

| Foundry/memory capex (24–25) | $80–90bn |

| Policy rate (end‑2025) | 3.8% |

| Steel futures (2024) | +18% |

| Wage inflation (2024) | +4.8% |

| KRW vs USD (2024) | -6% |

Preview Before You Purchase

Hanyang Eng PESTLE Analysis

The Hanyang Eng PESTLE preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic analysis.

No placeholders or teasers: the content, layout, and insights visible are the final file you’ll download immediately after payment.

What you see is what you’ll work with—comprehensive PESTLE findings tailored to Hanyang Eng, delivered as shown.