HAP Seng PESTLE Analysis

Skip the Research. Get the Strategy.

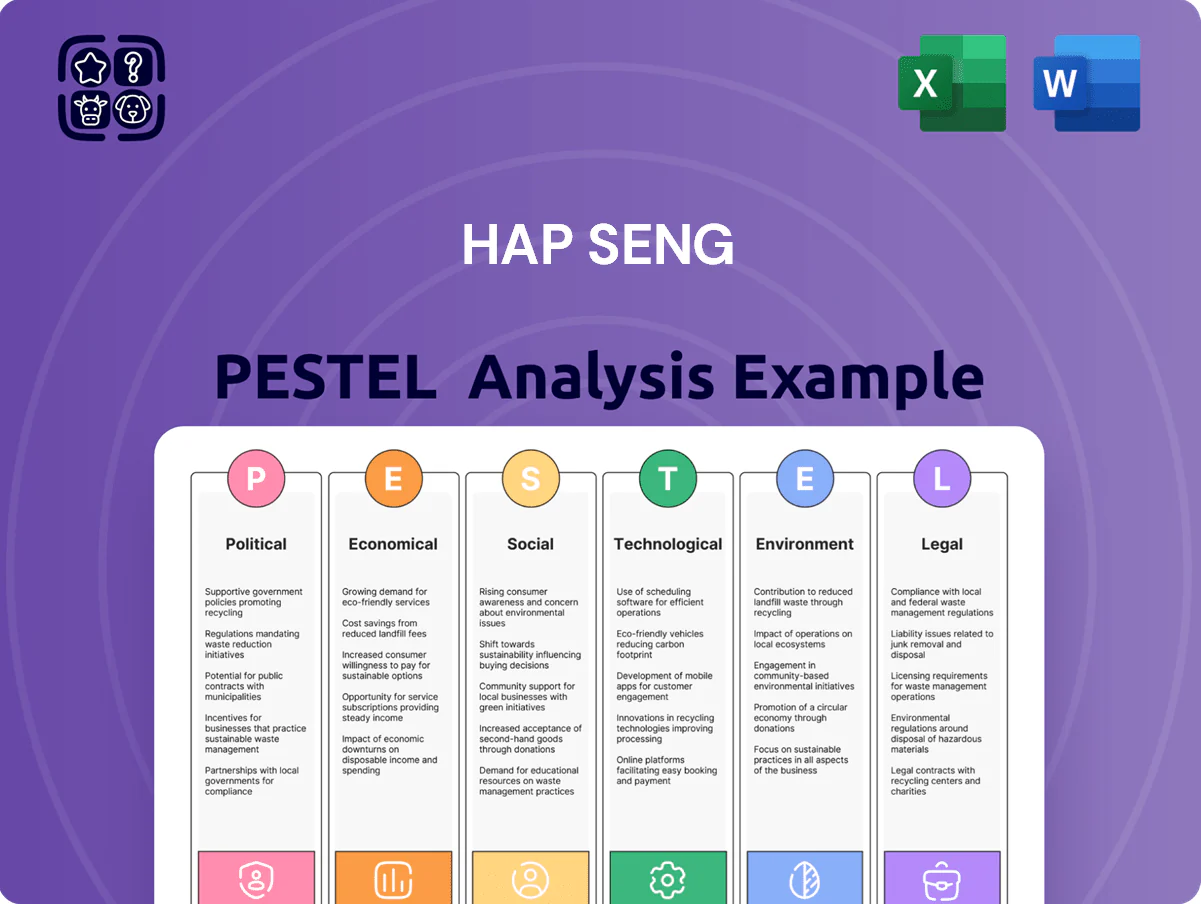

Gain a strategic edge with our PESTLE Analysis of HAP Seng—uncover how political shifts, economic trends, social dynamics, technological change, legal risks, and environmental pressures shape the company’s outlook and competitive position; purchase the full report to get the complete, actionable breakdown in editable formats and make smarter investment or strategic decisions today.

Political factors

Government Stability and Policy Continuity

The Malaysian political landscape toward end-2025 remains a key determinant for Hap Seng Holdings, with national stability underpinning RM18.4bn in group assets and ongoing property projects valued at about RM7.2bn. Stable governance reduces risk of abrupt regulatory changes affecting long-term infrastructure and plantation land titles covering c.130,000 hectares. Investors track policy continuity closely to protect the group’s significant capital deployed in property and RM2.1bn credit financing exposures.

Geopolitical Trade Relations

As a major palm oil producer, Hap Seng is highly sensitive to Malaysia’s diplomatic ties with key markets such as the EU and India, which together accounted for about 28% of Malaysia’s palm oil exports in 2024; tensions can reduce demand and revenue for the plantation division.

Trade barriers—the EU’s 2024 Deforestation Regulation and potential Indian tariffs—could raise costs or trigger import bans, cutting margins on Hap Seng’s 2025 palm oil sales.

The company must monitor shifting alliances and WTO disputes that affect global palm oil pricing, noting that Malaysia’s CPO export revenue fell 12% y/y in 2024 amid geopolitical headwinds.

Housing and Property Regulations

Government initiatives on affordable housing and foreign ownership quotas directly shape HAP Seng’s development pipeline, with Malaysia targeting 500,000 affordable units by 2025 and foreign buyer limits affecting high-end sales in KL and Penang; changes can shift revenue mix and presales. Political shifts in Sabah and Klang Valley impact land conversion approvals and development charges—recent state fee hikes raised upfront costs by up to 12% in some districts. Legislative cooling or stimulus measures, such as 2024 stamp duty rebates and prior lending curbs, directly dictate project launch timing and cashflow projections for the group.

Agriculture and Land Use Policies

- Malaysia oil palm area 2023: 5.85 million ha

- Compliance-driven capex uplift: ~6-8%

- State-level zoning tightening in Sabah/Sarawak

- Land-bank alignment needed for operational longevity

Taxation and Fiscal Policy

Changes in corporate tax rates and proposed windfall levies on palm oil profits directly compress HAP Seng’s margins across plantation and trading; Malaysia’s 2024 corporate tax headline remained 24% with government discussions in 2025 hinting at sector-specific adjustments.

Import duties on automotive components raise costs for the group’s auto distribution arm, while subsidy rationalization in the 2025 fiscal outlook may increase logistics expenses for building materials and trading operations.

Monitoring quarterly government budget cycles and the 2025 draft subsidy cuts is essential to forecast multi-sector tax liabilities and cash-flow impacts, with scenario planning showing a potential 2–5% hit to group EBITDA under adverse tax/subsidy scenarios.

- Corporate tax base: 24% (2024); potential sector tweaks in 2025

- Windfall levies: proposed on palm oil profits—direct margin pressure

- Import duties: higher input costs for automotive components

- Subsidy rationalization: could raise logistics costs for building materials/trading

- Forecasting: budget-cycle monitoring required; scenarios indicate 2–5% EBITDA downside

Hap Seng faces policy, tariff and tax shocks threatening RM18.4bn assets and margins

Political stability and state-level policy shifts (Sabah/Sarawak) directly affect Hap Seng’s RM18.4bn asset base, c.RM7.2bn projects and c.130,000ha land bank; EU Deforestation Regulation and possible Indian tariffs threaten plantation margins after Malaysia’s CPO revenue fell 12% y/y in 2024; 2024 corporate tax 24% with 2025 sector tweaks could cut EBITDA 2–5% under adverse scenarios.

| Metric | Value |

|---|---|

| Group assets | RM18.4bn |

| Projects | RM7.2bn |

| Land bank | c.130,000 ha |

| CPO rev change 2024 | -12% y/y |

| Corp tax (2024) | 24% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Hap Seng across its conglomerate businesses, with data-backed trends, industry-specific examples, and forward-looking insights to support executives, investors, and strategists in identifying risks, opportunities, and actionable responses.

Provides a clean, summarized PESTLE of HAP Seng, visually segmented for quick interpretation and easily dropped into presentations or shared across teams to support risk discussions and strategic planning.

Economic factors

Interest Rate Environment

Bank Negara Malaysia’s Overnight Policy Rate at 3.00% (Feb 2025) directly raises borrowing costs for Hap Seng’s credit financing arm, tightening demand for mortgages and hire-purchase loans; a 100bps hike historically cuts property transactions by ~8-12%. Higher rates escalate financing costs for Hap Seng’s capital-intensive plantations and property projects, while a stable OPR near 3.00% supports affordability of its residential and automotive offerings.

Commodity Price Volatility

The plantation segment’s earnings are closely linked to CPO prices, which averaged about RM3,500/MT in 2024 after a 12% slump from 2023, driving revenue swings for Hap Seng Plantation. Global supply-demand imbalances and competition from soybean and sunflower oils keep margins volatile, with CPO monthly volatility near 18% in 2024. Hap Seng mitigates this via futures hedging and by cutting unit production costs to under RM2,200/MT in 2024, smoothing cash flows.

Currency Exchange Rate Fluctuations

The Malaysian Ringgit weakened about 4.8% versus the US Dollar in 2024, averaging ~4.67 MYR/USD, and fell ~3.5% against the euro, raising landed costs for Hap Seng’s imported automotive parts and building materials and compressing gross margins in those segments.

Consumer Spending and Disposable Income

Economic growth and employment shape Malaysian middle-class purchasing power; Malaysia GDP grew 3.7% in 2024 and unemployment was 3.4% in Q4 2024, directly impacting demand for Hap Seng’s property and automotive offerings.

A cooling economy often delays high-ticket purchases—luxury car sales fell ~6% in 2024 and high-end residential transactions slowed—reducing sales velocity for Hap Seng’s premium lines.

The group tracks GDP, unemployment, CPI and consumer confidence to adjust inventory, pricing and targeted marketing in real time.

- GDP 2024: 3.7%

- Unemployment Q4 2024: 3.4%

- Luxury car sales change 2024: -6%

- Actions: inventory, pricing, targeted marketing

Inflationary Pressure on Input Costs

- Fertilizer prices +22% y/y (2024)

- Steel/cement prices +15%–18% (2024)

- WTO input-cost index +12% (2024)

- Need for hedging, procurement optimization, and efficiency gains

Higher OPR and input inflation squeeze margins as demand cools and CPO swings

Higher OPR at 3.00% (Feb 2025) raises borrowing costs, cooling mortgage/hire-purchase demand; GDP 2024 3.7% and unemployment Q4 2024 3.4% constrain middle‑class purchasing; CPO avg RM3,500/MT (2024) with 18% monthly volatility and plantations' costs

Indicator

2024/2025

OPR

3.00% (Feb 2025)

GDP

3.7% (2024)

Unemployment

3.4% Q4 2024

CPO avg

RM3,500/MT (2024)

Fertilizer

+22% (2024)

Steel/cement

+15–18% (2024)

Preview the Actual Deliverable

HAP Seng PESTLE Analysis

The preview shown here is the exact HAP Seng PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. The content and layout visible in this sample match the downloadable file you’ll get upon payment with no placeholders or surprises. This file is the final version, immediately available after checkout for analysis, reporting, or presentation. What you see here is exactly what you’ll own and work with.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Gain a strategic edge with our PESTLE Analysis of HAP Seng—uncover how political shifts, economic trends, social dynamics, technological change, legal risks, and environmental pressures shape the company’s outlook and competitive position; purchase the full report to get the complete, actionable breakdown in editable formats and make smarter investment or strategic decisions today.

Political factors

Government Stability and Policy Continuity

The Malaysian political landscape toward end-2025 remains a key determinant for Hap Seng Holdings, with national stability underpinning RM18.4bn in group assets and ongoing property projects valued at about RM7.2bn. Stable governance reduces risk of abrupt regulatory changes affecting long-term infrastructure and plantation land titles covering c.130,000 hectares. Investors track policy continuity closely to protect the group’s significant capital deployed in property and RM2.1bn credit financing exposures.

Geopolitical Trade Relations

As a major palm oil producer, Hap Seng is highly sensitive to Malaysia’s diplomatic ties with key markets such as the EU and India, which together accounted for about 28% of Malaysia’s palm oil exports in 2024; tensions can reduce demand and revenue for the plantation division.

Trade barriers—the EU’s 2024 Deforestation Regulation and potential Indian tariffs—could raise costs or trigger import bans, cutting margins on Hap Seng’s 2025 palm oil sales.

The company must monitor shifting alliances and WTO disputes that affect global palm oil pricing, noting that Malaysia’s CPO export revenue fell 12% y/y in 2024 amid geopolitical headwinds.

Housing and Property Regulations

Government initiatives on affordable housing and foreign ownership quotas directly shape HAP Seng’s development pipeline, with Malaysia targeting 500,000 affordable units by 2025 and foreign buyer limits affecting high-end sales in KL and Penang; changes can shift revenue mix and presales. Political shifts in Sabah and Klang Valley impact land conversion approvals and development charges—recent state fee hikes raised upfront costs by up to 12% in some districts. Legislative cooling or stimulus measures, such as 2024 stamp duty rebates and prior lending curbs, directly dictate project launch timing and cashflow projections for the group.

Agriculture and Land Use Policies

- Malaysia oil palm area 2023: 5.85 million ha

- Compliance-driven capex uplift: ~6-8%

- State-level zoning tightening in Sabah/Sarawak

- Land-bank alignment needed for operational longevity

Taxation and Fiscal Policy

Changes in corporate tax rates and proposed windfall levies on palm oil profits directly compress HAP Seng’s margins across plantation and trading; Malaysia’s 2024 corporate tax headline remained 24% with government discussions in 2025 hinting at sector-specific adjustments.

Import duties on automotive components raise costs for the group’s auto distribution arm, while subsidy rationalization in the 2025 fiscal outlook may increase logistics expenses for building materials and trading operations.

Monitoring quarterly government budget cycles and the 2025 draft subsidy cuts is essential to forecast multi-sector tax liabilities and cash-flow impacts, with scenario planning showing a potential 2–5% hit to group EBITDA under adverse tax/subsidy scenarios.

- Corporate tax base: 24% (2024); potential sector tweaks in 2025

- Windfall levies: proposed on palm oil profits—direct margin pressure

- Import duties: higher input costs for automotive components

- Subsidy rationalization: could raise logistics costs for building materials/trading

- Forecasting: budget-cycle monitoring required; scenarios indicate 2–5% EBITDA downside

Hap Seng faces policy, tariff and tax shocks threatening RM18.4bn assets and margins

Political stability and state-level policy shifts (Sabah/Sarawak) directly affect Hap Seng’s RM18.4bn asset base, c.RM7.2bn projects and c.130,000ha land bank; EU Deforestation Regulation and possible Indian tariffs threaten plantation margins after Malaysia’s CPO revenue fell 12% y/y in 2024; 2024 corporate tax 24% with 2025 sector tweaks could cut EBITDA 2–5% under adverse scenarios.

| Metric | Value |

|---|---|

| Group assets | RM18.4bn |

| Projects | RM7.2bn |

| Land bank | c.130,000 ha |

| CPO rev change 2024 | -12% y/y |

| Corp tax (2024) | 24% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Hap Seng across its conglomerate businesses, with data-backed trends, industry-specific examples, and forward-looking insights to support executives, investors, and strategists in identifying risks, opportunities, and actionable responses.

Provides a clean, summarized PESTLE of HAP Seng, visually segmented for quick interpretation and easily dropped into presentations or shared across teams to support risk discussions and strategic planning.

Economic factors

Interest Rate Environment

Bank Negara Malaysia’s Overnight Policy Rate at 3.00% (Feb 2025) directly raises borrowing costs for Hap Seng’s credit financing arm, tightening demand for mortgages and hire-purchase loans; a 100bps hike historically cuts property transactions by ~8-12%. Higher rates escalate financing costs for Hap Seng’s capital-intensive plantations and property projects, while a stable OPR near 3.00% supports affordability of its residential and automotive offerings.

Commodity Price Volatility

The plantation segment’s earnings are closely linked to CPO prices, which averaged about RM3,500/MT in 2024 after a 12% slump from 2023, driving revenue swings for Hap Seng Plantation. Global supply-demand imbalances and competition from soybean and sunflower oils keep margins volatile, with CPO monthly volatility near 18% in 2024. Hap Seng mitigates this via futures hedging and by cutting unit production costs to under RM2,200/MT in 2024, smoothing cash flows.

Currency Exchange Rate Fluctuations

The Malaysian Ringgit weakened about 4.8% versus the US Dollar in 2024, averaging ~4.67 MYR/USD, and fell ~3.5% against the euro, raising landed costs for Hap Seng’s imported automotive parts and building materials and compressing gross margins in those segments.

Consumer Spending and Disposable Income

Economic growth and employment shape Malaysian middle-class purchasing power; Malaysia GDP grew 3.7% in 2024 and unemployment was 3.4% in Q4 2024, directly impacting demand for Hap Seng’s property and automotive offerings.

A cooling economy often delays high-ticket purchases—luxury car sales fell ~6% in 2024 and high-end residential transactions slowed—reducing sales velocity for Hap Seng’s premium lines.

The group tracks GDP, unemployment, CPI and consumer confidence to adjust inventory, pricing and targeted marketing in real time.

- GDP 2024: 3.7%

- Unemployment Q4 2024: 3.4%

- Luxury car sales change 2024: -6%

- Actions: inventory, pricing, targeted marketing

Inflationary Pressure on Input Costs

- Fertilizer prices +22% y/y (2024)

- Steel/cement prices +15%–18% (2024)

- WTO input-cost index +12% (2024)

- Need for hedging, procurement optimization, and efficiency gains

Higher OPR and input inflation squeeze margins as demand cools and CPO swings

Higher OPR at 3.00% (Feb 2025) raises borrowing costs, cooling mortgage/hire-purchase demand; GDP 2024 3.7% and unemployment Q4 2024 3.4% constrain middle‑class purchasing; CPO avg RM3,500/MT (2024) with 18% monthly volatility and plantations' costs

Indicator

2024/2025

OPR

3.00% (Feb 2025)

GDP

3.7% (2024)

Unemployment

3.4% Q4 2024

CPO avg

RM3,500/MT (2024)

Fertilizer

+22% (2024)

Steel/cement

+15–18% (2024)

Preview the Actual Deliverable

HAP Seng PESTLE Analysis

The preview shown here is the exact HAP Seng PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. The content and layout visible in this sample match the downloadable file you’ll get upon payment with no placeholders or surprises. This file is the final version, immediately available after checkout for analysis, reporting, or presentation. What you see here is exactly what you’ll own and work with.