Harrow Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

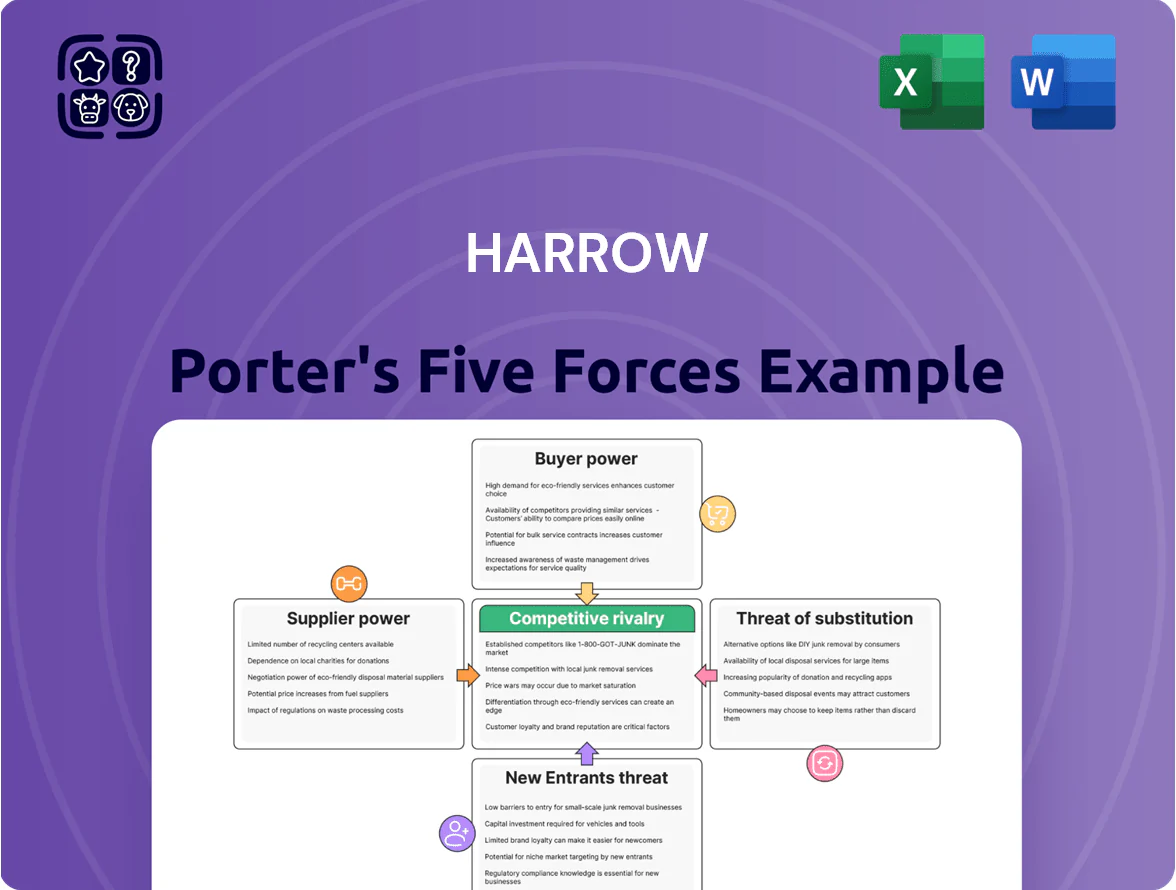

Suppliers Bargaining Power

Concentration of API Manufacturers

Harrow depends on a small set of qualified API makers for ophthalmic-grade chemicals, a market where 3–5 global suppliers hold ~70% of capacity, raising supplier leverage on price and lead times.

These APIs require strict GMP and USP standards; in 2024 Harrow reported a 12% COGS rise tied to supplier price hikes and longer 10–14 week lead times.

Any shutdown at a specialized vendor could halt production of Harrow’s core drugs within weeks and risk revenue losses exceeding single-quarter net sales (~$8–12M per product line).

Regulatory Compliance and Switching Costs

Suppliers must meet FDA and current Good Manufacturing Practice (cGMP) rules to stay in Harrow’s pharma chain, raising Harrow’s switching cost since qualifying a new supplier takes 18–36 months and often $1–3M in validation and regulatory filings.

Because replacement is slow and costly, incumbent suppliers hold leverage in contract talks; industry data shows qualified-supplier counts fell 12% for mid‑sized CDMOs between 2019–2024, tightening supplier power.

Specialized Manufacturing Requirements

Ophthalmic products need sterile facilities and niche delivery systems, like multi-dose preservative-free bottles, which only about 12–15 CMOs worldwide can reliably produce as of 2025, giving those suppliers outsized leverage; industry reports show CMO margins for specialized ophthalmics run 18–25%, limiting price flexibility. Harrow’s reliance on these few providers reduces its bargaining power, constraining cost cuts and risking supply bottlenecks that could impact gross margin by 100–250 basis points.

Proprietary Input Technology

When third parties hold patents on components and delivery tech used in Harrow’s acquired branded portfolio, suppliers can dictate prices and terms; Harrow faces limited leverage for proprietary advanced formulations that drive its 2025 growth plans.

- Patented inputs raise supplier power

- Harrow’s reliance on advanced formulations increases cost exposure

- Exclusive rights force acceptance of supplier pricing

- Mitigation: licensing, vertical integration, or alternative R&D

Input Price Volatility and Scale

Global raw-material price swings—active since 2021 and with active 2024 drug-API spot-price rises of ~12–18% for key inputs—push suppliers to pass costs to firms like Harrow.

Harrow’s smaller scale (estimated 2024 revenues ~USD 350m vs. Pfizer’s USD 58.4bn) limits volume discounts, reducing its bargaining leverage.

This makes Harrow sensitive to vendor pricing strategies and macro conditions; a 5% input-cost shock could cut margins by ~2–3 percentage points based on 2024 COGS ratios.

- 2024 API spot prices up 12–18%

- Harrow revenue ~USD 350m (2024 est.)

- Large peers: Pfizer USD 58.4bn (2024)

- 5% input shock → ~2–3 pp margin hit

Tight supplier grip: few API/CMO sources lift costs—5% shock trims margins 2–3pp

Suppliers hold high leverage: 3–5 global API makers supply ~70% capacity, 12–15 CMOs handle niche ophthalmic delivery, and 2019–24 qualified-supplier counts fell 12%, raising switching costs (18–36 months, $1–3M). Harrow’s 2024 revenue ~USD 350m and 12% COGS rise show sensitivity; a 5% input shock could cut margins ~2–3 pp.

| Metric | Value |

|---|---|

| Global API suppliers | 3–5 (70% capacity) |

| Qualified CMOs | 12–15 (2025) |

| Supplier count change | -12% (2019–24) |

| Switch cost | 18–36 months; $1–3M |

| Harrow rev | ~USD 350m (2024) |

| COGS rise | 12% (2024) |

| Input shock impact | 5% → -2–3 pp margin |

What is included in the product

Concise Porter's Five Forces assessment for Harrow that uncovers competitive pressures, supplier and buyer power, threat of substitutes and entrants, and strategic levers to protect market share and profitability.

Harrow Porter's Five Forces delivers a one-sheet strategic snapshot—instantly reveal competitive pressure with an editable radar chart and copy-ready layout for rapid boardroom decisions.

Customers Bargaining Power

Influence of Pharmacy Benefit Managers

PBMs and insurers act as powerful intermediaries that set formulary placement and patient access for Harrow, often dictating coverage tiers that shape demand.

If Harrow's drug lands outside a favorable cost tier, patients face higher co-pays and prescription volumes drop—US studies show a 30–40% volume decline when out-of-tier.

To secure preferred placement, Harrow typically pays large rebates; industry averages show manufacturer rebates to PBMs reached about 35% of list price in 2024.

These rebate pressures compress Harrow's net price and margins, forcing trade-offs between access, volume, and profitability.

Concentration of Large Eye Care Groups

The consolidation of US ophthalmology practices into large, private‑equity‑backed groups—over 40% of practices were in MSOs (management services organizations) by 2024—gives buyers strong negotiating leverage. These groups can demand bulk discounts, standardized protocols, and preferred‑vendor status, steering purchases toward specific brands across hundreds of clinics. Harrow must tailor pricing and service bundles to win these high‑volume channels, where a single contract can represent $5M–$50M+ in annual device and supply spend.

Price Sensitivity of Healthcare Providers

Availability of Generic Alternatives

For many of Harrow's off-patent drugs, buyers can switch to generics sold by multiple firms; US generic market share topped 90% by prescriptions in 2024, pressuring list prices and margins.

Price transparency and identical substitutes let purchasers demand steeper discounts—Harrow reported gross margin of 28% in FY2024, down 4 pts versus peers due to discounting.

Harrow must prove clinical or service value continually to avoid churn to commodity-priced generics, or face volume and revenue erosion.

- High generic availability: >90% U.S. prescription share (2024)

- Margin impact: Harrow gross margin 28% FY2024

- Buyer leverage: multiple suppliers, transparent pricing

Patient Advocacy and Out-of-Pocket Costs

Rebates Crush Pricing: 35% Cuts & 90%+ Generics Squeeze Harrow's Margins

PBMs, insurers, and consolidated MSOs wield strong leverage over Harrow—rebates averaged ~35% of list price (2024), cutting net price and margins (Harrow gross margin 28% FY2024). High generic share (>90% U.S. prescriptions, 2024) and patient price-sensitivity (68% research, 42% request cheaper options) force steep discounts or risk volume loss.

| Metric | 2024 |

|---|---|

| Manufacturer rebates | ~35% |

| Generic Rx share | >90% |

| Harrow gross margin | 28% |

| Patients researching | 68% |

| Patients seeking cheaper | 42% |

What You See Is What You Get

Harrow Porter's Five Forces Analysis

This preview shows the exact Harrow Porter Five Forces Analysis you'll receive immediately after purchase—no placeholders, no samples. The document displayed is the fully formatted, ready-to-use analysis you’ll be able to download and apply the moment you buy. You’re viewing the final deliverable, identical to the file sent after payment, complete with conclusions and actionable insights.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Suppliers Bargaining Power

Concentration of API Manufacturers

Harrow depends on a small set of qualified API makers for ophthalmic-grade chemicals, a market where 3–5 global suppliers hold ~70% of capacity, raising supplier leverage on price and lead times.

These APIs require strict GMP and USP standards; in 2024 Harrow reported a 12% COGS rise tied to supplier price hikes and longer 10–14 week lead times.

Any shutdown at a specialized vendor could halt production of Harrow’s core drugs within weeks and risk revenue losses exceeding single-quarter net sales (~$8–12M per product line).

Regulatory Compliance and Switching Costs

Suppliers must meet FDA and current Good Manufacturing Practice (cGMP) rules to stay in Harrow’s pharma chain, raising Harrow’s switching cost since qualifying a new supplier takes 18–36 months and often $1–3M in validation and regulatory filings.

Because replacement is slow and costly, incumbent suppliers hold leverage in contract talks; industry data shows qualified-supplier counts fell 12% for mid‑sized CDMOs between 2019–2024, tightening supplier power.

Specialized Manufacturing Requirements

Ophthalmic products need sterile facilities and niche delivery systems, like multi-dose preservative-free bottles, which only about 12–15 CMOs worldwide can reliably produce as of 2025, giving those suppliers outsized leverage; industry reports show CMO margins for specialized ophthalmics run 18–25%, limiting price flexibility. Harrow’s reliance on these few providers reduces its bargaining power, constraining cost cuts and risking supply bottlenecks that could impact gross margin by 100–250 basis points.

Proprietary Input Technology

When third parties hold patents on components and delivery tech used in Harrow’s acquired branded portfolio, suppliers can dictate prices and terms; Harrow faces limited leverage for proprietary advanced formulations that drive its 2025 growth plans.

- Patented inputs raise supplier power

- Harrow’s reliance on advanced formulations increases cost exposure

- Exclusive rights force acceptance of supplier pricing

- Mitigation: licensing, vertical integration, or alternative R&D

Input Price Volatility and Scale

Global raw-material price swings—active since 2021 and with active 2024 drug-API spot-price rises of ~12–18% for key inputs—push suppliers to pass costs to firms like Harrow.

Harrow’s smaller scale (estimated 2024 revenues ~USD 350m vs. Pfizer’s USD 58.4bn) limits volume discounts, reducing its bargaining leverage.

This makes Harrow sensitive to vendor pricing strategies and macro conditions; a 5% input-cost shock could cut margins by ~2–3 percentage points based on 2024 COGS ratios.

- 2024 API spot prices up 12–18%

- Harrow revenue ~USD 350m (2024 est.)

- Large peers: Pfizer USD 58.4bn (2024)

- 5% input shock → ~2–3 pp margin hit

Tight supplier grip: few API/CMO sources lift costs—5% shock trims margins 2–3pp

Suppliers hold high leverage: 3–5 global API makers supply ~70% capacity, 12–15 CMOs handle niche ophthalmic delivery, and 2019–24 qualified-supplier counts fell 12%, raising switching costs (18–36 months, $1–3M). Harrow’s 2024 revenue ~USD 350m and 12% COGS rise show sensitivity; a 5% input shock could cut margins ~2–3 pp.

| Metric | Value |

|---|---|

| Global API suppliers | 3–5 (70% capacity) |

| Qualified CMOs | 12–15 (2025) |

| Supplier count change | -12% (2019–24) |

| Switch cost | 18–36 months; $1–3M |

| Harrow rev | ~USD 350m (2024) |

| COGS rise | 12% (2024) |

| Input shock impact | 5% → -2–3 pp margin |

What is included in the product

Concise Porter's Five Forces assessment for Harrow that uncovers competitive pressures, supplier and buyer power, threat of substitutes and entrants, and strategic levers to protect market share and profitability.

Harrow Porter's Five Forces delivers a one-sheet strategic snapshot—instantly reveal competitive pressure with an editable radar chart and copy-ready layout for rapid boardroom decisions.

Customers Bargaining Power

Influence of Pharmacy Benefit Managers

PBMs and insurers act as powerful intermediaries that set formulary placement and patient access for Harrow, often dictating coverage tiers that shape demand.

If Harrow's drug lands outside a favorable cost tier, patients face higher co-pays and prescription volumes drop—US studies show a 30–40% volume decline when out-of-tier.

To secure preferred placement, Harrow typically pays large rebates; industry averages show manufacturer rebates to PBMs reached about 35% of list price in 2024.

These rebate pressures compress Harrow's net price and margins, forcing trade-offs between access, volume, and profitability.

Concentration of Large Eye Care Groups

The consolidation of US ophthalmology practices into large, private‑equity‑backed groups—over 40% of practices were in MSOs (management services organizations) by 2024—gives buyers strong negotiating leverage. These groups can demand bulk discounts, standardized protocols, and preferred‑vendor status, steering purchases toward specific brands across hundreds of clinics. Harrow must tailor pricing and service bundles to win these high‑volume channels, where a single contract can represent $5M–$50M+ in annual device and supply spend.

Price Sensitivity of Healthcare Providers

Availability of Generic Alternatives

For many of Harrow's off-patent drugs, buyers can switch to generics sold by multiple firms; US generic market share topped 90% by prescriptions in 2024, pressuring list prices and margins.

Price transparency and identical substitutes let purchasers demand steeper discounts—Harrow reported gross margin of 28% in FY2024, down 4 pts versus peers due to discounting.

Harrow must prove clinical or service value continually to avoid churn to commodity-priced generics, or face volume and revenue erosion.

- High generic availability: >90% U.S. prescription share (2024)

- Margin impact: Harrow gross margin 28% FY2024

- Buyer leverage: multiple suppliers, transparent pricing

Patient Advocacy and Out-of-Pocket Costs

Rebates Crush Pricing: 35% Cuts & 90%+ Generics Squeeze Harrow's Margins

PBMs, insurers, and consolidated MSOs wield strong leverage over Harrow—rebates averaged ~35% of list price (2024), cutting net price and margins (Harrow gross margin 28% FY2024). High generic share (>90% U.S. prescriptions, 2024) and patient price-sensitivity (68% research, 42% request cheaper options) force steep discounts or risk volume loss.

| Metric | 2024 |

|---|---|

| Manufacturer rebates | ~35% |

| Generic Rx share | >90% |

| Harrow gross margin | 28% |

| Patients researching | 68% |

| Patients seeking cheaper | 42% |

What You See Is What You Get

Harrow Porter's Five Forces Analysis

This preview shows the exact Harrow Porter Five Forces Analysis you'll receive immediately after purchase—no placeholders, no samples. The document displayed is the fully formatted, ready-to-use analysis you’ll be able to download and apply the moment you buy. You’re viewing the final deliverable, identical to the file sent after payment, complete with conclusions and actionable insights.